EDGEN · AI基礎設施與HPC託管股票分析

Applied Digital Corporation 2026財年第一季度回顧:AI工廠核心,市場尚未充分定價

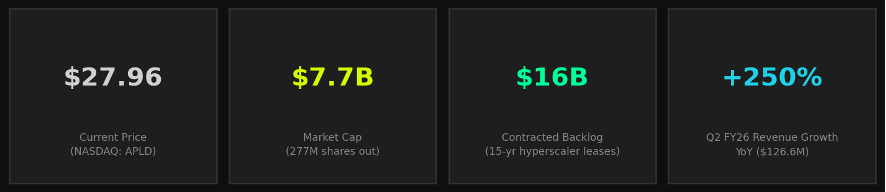

NASDAQ: APLD

評級 | 目標價 | 當前價格 | 上行空間 | 報告日期 |

|---|---|---|---|---|

買入 | $42.50 | $27.96 | +52% | 2026年3月17日 |

投資摘要

Applied Digital Corporation (APLD) 正成為公共市場中最引人注目的純AI基礎設施公司之一。該公司設計、建設並營運專為GPU密集型高性能計算 (HPC) 工作負載優化的超大規模數據中心,這些工作負載是AI訓練和推論革命的支柱。

我們首次將其評級定為買入,12個月目標價為$42.50,意味著較當前價格$27.96有+52%的上行空間。關鍵催化劑包括$50億的Polaris Forge 2租約、CoreWeave $110億協議的加速推進,以及營收的持續增長。

看漲論點

– 與投資級超大規模企業簽訂的$160億合同積壓訂單提供15年的營收可見性

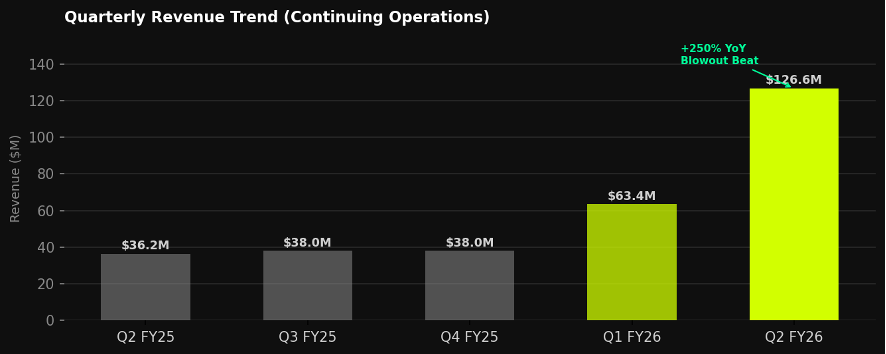

– 2026財年第二季度營收達$1.266億(同比增長250%),表明HPC增長超出預期

– 位於成本低、電力充沛的北達科他州園區的專用設施將建設時間壓縮至12-14個月

– Polaris Forge 2園區與第二家美國超大規模企業簽署了200MW租約 — 15年內$50億

– 在為超大規模企業建設AI工廠而非与之競爭方面擁有先行者優勢

看跌風險

– 客戶集中度高:CoreWeave佔$110億合同積壓訂單的大部分

– 高槓桿:截至2026財年第二季度,債務為$26億,現金為$23億 — 建設階段的資產負債表

– 持續淨虧損(2025財年-$1.61億);盈利能力取決於規模和發展時間表

– 賣空興趣高,佔流通股的約26-33%;負面催化劑將帶來下行壓力

– 執行風險:大規模設施建設複雜、資本密集且時間敏感

產業概覽

AI數據中心基礎設施市場正處於長期超高速增長之中。包括微軟、谷歌、亞馬遜和Meta在內的主要超大規模企業已集體承諾在2025財年和2026財年投入超過$3000億的資本支出,其中很大一部分用於GPU密集型計算園區。這為APLD等專業營運商創造了多年的發展順風。

財務概覽

Applied Digital 的財年截止日期為5月31日。該公司從2024財年開始果斷地從加密貨幣挖礦基礎設施轉向AI/HPC託管,營收拐點現已大規模顯現。

營收趨勢

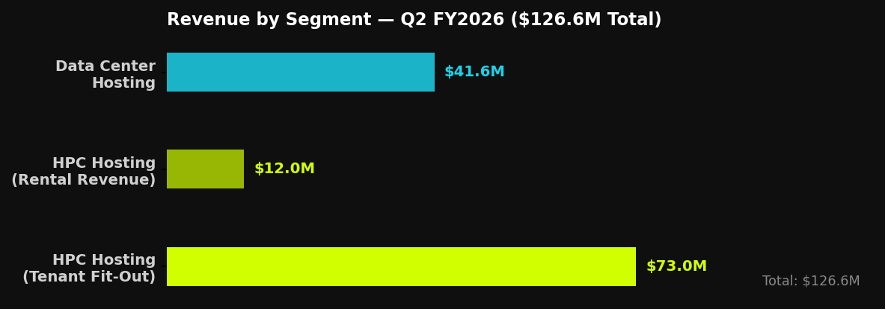

2026財年第二季度(截至2025年11月30日)是一個決定性時刻:總營收飆升至$1.266億,同比增長250%,超出市場普遍預期$8670萬的46%。HPC託管貢獻了$8500萬,數據中心託管貢獻了$4160萬(同比增長15%)。

按業務分部的營收 — 2026財年第二季度

關鍵財務指標

指標 | 2024財年 | 2025財年 | 2026財年第一季度 | 2026財年第二季度 | 註釋 |

|---|---|---|---|---|---|

營收(百萬美元) | $136.6M | $144.2M | ~$63.4M | $126.6M | 同比增長250% |

淨虧損(百萬美元) | -$73.8M | -$161.0M | — | — | 虧損擴大 |

現金及約當物 | — | $114M | $114M | $2.3B | 融資後激增 |

總債務 | — | $687M | $687M | $2.6B | 建設階段槓桿 |

已發行股份 | — | 209M | — | 277M | 稀釋32% |

公司簡介

Applied Digital Corporation(前身為Applied Blockchain)成立於2014年,總部位於德克薩斯州達拉斯。公司主要營運兩個業務部門:

HPC託管(Polaris Forge園區)

HPC託管部門在北達科他州埃倫代爾建設和營運專用的AI工廠園區。這些設施旨在實現極致計算密度,採用直達晶片液冷、高密度配電,並將模組化建設時間壓縮至12-14個月。旗艦園區Polaris Forge 1 (ELN-02) 在2026財年第二季度完全通電,從而實現了租賃營收的階躍式增長。Polaris Forge 2 正在建設中,並已簽署200MW的租約。

數據中心託管

傳統的數據中心託管部門在北達科他州營運兩個共286兆瓦的設施,主要為基於ASIC的加密貨幣挖礦和GPU計算客戶提供託管服務。該部門在2026財年第二季度貢獻了$4160萬(同比增長15%),並仍是一個穩定的現金生成基礎。

屬性 | 詳情 |

|---|---|

股票代碼 | NASDAQ: APLD |

行業 | 技術 — AI基礎設施 / 數據中心 |

總部 | 德克薩斯州達拉斯 (營運地:北達科他州埃倫代爾) |

主要客戶 | CoreWeave($110億,15年)+ 第二家美國超大規模企業($50億,15年) |

總積壓訂單 | ~$160億合同收入(截至2026財年第二季度) |

容量 | 286MW營運中(數據中心託管)+ 200MW建設中(Polaris Forge 2) |

技術優勢 | 直達晶片液冷、模組化建設、專為GPU密度設計 |

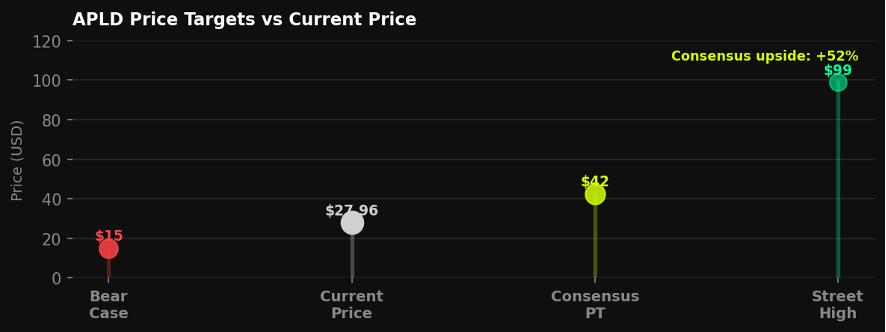

目標價分析

隨著APLD營收增長的實現,分析師覆蓋範圍顯著擴大。共識12個月目標價$42.50(14位分析師,全部為買入/強力買入)反映了HPC增長潛力和積壓訂單的轉化。市場最高目標價$99意味著在完全實現積壓訂單的情況下,基於DCF的多年期估值。

情境 | 目標價 | 上行空間 | 關鍵假設 | 機率 |

|---|---|---|---|---|

看漲 | $99 | +254% | 全部$160億積壓訂單按計劃轉化;無客戶違約 | 25% |

基準 | $42.50 | +52% | 積壓訂單滯後12個月增長;適度股權融資稀釋 | 50% |

看跌 | $15 | -46% | CoreWeave交易對方風險或建設延誤成為現實 | 25% |

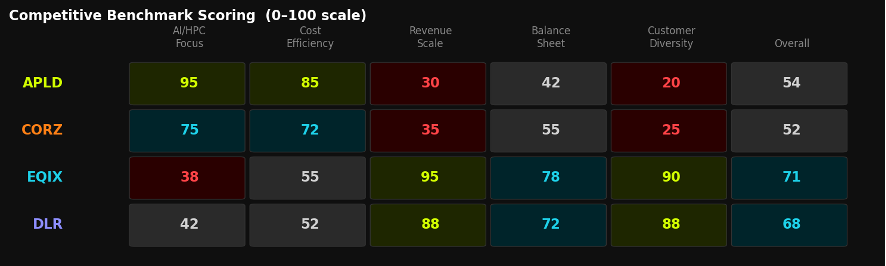

競爭格局

APLD 業務橫跨傳統數據中心REIT和下一代AI雲基礎設施。其最接近的競爭對手是Core Scientific (CORZ),該公司也已從加密貨幣轉向AI託管。Equinix (EQIX) 和 Digital Realty (DLR) 等老牌企業在規模和地理多樣性方面具有競爭力,但缺乏APLD的HPC原生設計優勢。

公司 | 股票代碼 | 市值 | 營收(過去十二個月) | 毛利率 | AI/HPC 重點 | 評級 | 目標價 |

|---|---|---|---|---|---|---|---|

Applied Digital | APLD | $7.7B | ~$254M* | — | 純AI | 買入 | $42.50 |

Core Scientific | CORZ | ~$3.8B | ~$610M | ~45% | 轉型中 | 買入 | — |

Equinix | EQIX | ~$73B | $8.8B | ~47% | 間接 | 買入 | — |

Digital Realty | DLR | ~$50B | $5.6B | ~34% | 間接 | 持有 | — |

* TTM估計截至2026財年第二季度年化。

主要催化劑

– Polaris Forge 2 (200MW):建設進展更新和通電里程碑

– 2026財年第三季度財報(2026年3月):確認HPC租賃營收持續增長

– 額外的超大規模企業租約:管理層已表示Forge 3+園區的潛在管道

– CoreWeave IPO相關性:CRWV的公開市場表現反映了AI雲的健康狀況

– 電力接入擴展:北達科他州新的互連協議將釋放容量

– 潛在的REIT轉換或基礎設施貨幣化:策略選擇權

風險因素

– 客戶集中度:CoreWeave佔積壓訂單約70% — CoreWeave的任何壓力將直接影響APLD

– 執行風險:大規模建設項目存在成本超支和時間線風險

– 資本結構:建設階段$26億的債務負擔需要持續進入資本市場

– 稀釋:2026財年已發行股份同比增長32%;未來可能進行股權融資

– 競爭:超大規模企業可能加速內部建設或與EQIX/DLR大規模合作

– 宏觀風險:利率環境影響REIT類估值;信貸緊縮可能影響再融資

– 監管:能源許可、電網互連和數據主權規則不斷變化

結論

買入 | 目標價 $42.50 | +52% 上行空間 | 評級:強力買入 (共識)

Applied Digital 正在執行當前科技週期中最重要的基礎設施建設。2026財年第二季度的爆炸性財報 — 營收$1.266億,同比增長250% — 表明HPC託管的增長是真實的,並且超出計劃,由投資級超大規模企業合同承諾的營收支持。憑藉$160億的合同積壓訂單、低於$80億的市值,以及通過長期租約進行資本融資和去風險化的建設管道,APLD 提供了一個罕見的高確定性近期催化劑和多年複合增長潛力的組合。

主要風險在於CoreWeave的客戶集中度 — 這是一個眾所周知但對APLD未來2-3年增長故事具有結構性影響的風險。對這種風險敞口和建設階段資產負債表感到放心的投資者將發現APLD是AI基礎設施領域中風險/回報最不對稱的設置之一。

常見問題

APLD與傳統數據中心REIT有何不同?

EQIX和DLR等傳統REIT專注於為跨地區的企業和雲客戶提供託管服務。APLD則在低成本電力地區為訓練基礎模型的超大規模企業建設定制的GPU優化園區。APLD的設施每平方英尺密度高出5-10倍,並且是專用租賃而非多租戶模式。

何時能實現盈利?

管理層已指導,隨著ELN-02完全通電,調整後的EBITDA將在園區層面轉為正。由於$26億建設債務的折舊和利息將對GAAP收益造成壓力,淨利潤盈利可能還需要2-3年。營運現金流應在淨利潤之前轉為正,可能在2027財年。

CoreWeave的信用度是否值得擔憂?

CoreWeave在C輪融資中籌集了$15億,估值達到$190億,並於2025年IPO。其營收在OpenAI、Meta和Microsoft的AI模型訓練推動下同比增長超過500%。雖然不是傳統的投資級交易對手,但其與APLD的合同承諾是擔保租賃,相對於無擔保應收賬款,這限制了APLD的風險敞口。

為何賣空興趣如此之高,達到26-33%?

高賣空興趣反映了看跌情況:建設階段虧損、CoreWeave集中度以及執行不確定性。然而,2026財年第二季度的營收超出預期以及$160億積壓訂單的宣布已引發顯著的空頭回補。如果催化劑軌跡持續改善,高賣空興趣可能成為逆向看漲信號。

免責聲明

本報告由Edgen Research編制,僅供參考,不構成投資建議、招攬或買賣任何證券的要約。本文所含信息基於據信可靠的來源,但對其準確性或完整性不作保證。過往業績不代表未來結果。投資於小盤股和中盤股涉及重大風險,包括流動性風險和本金損失的潛在風險。本研究不考慮個人投資目標、財務狀況或需求。接收者在做出投資決策前應尋求獨立的財務建議。Edgen Research及其關聯公司可能持有討論證券的頭寸。

投資這事,終於不用一個人了

免費試用 Ed。不用信用卡,不綁約