Markets Confusing? Ask Edgen Search.

Instant answers, zero BS, and trading decisions your future self will thank you for.

Try Search Now

Tesla vs BYD - The EV Throne: Who Leads the Global Electric Vehicle Race?

EDGEN · GLOBAL EV SECTOR

Tesla vs BYD

The EV Throne: Who Leads the Global Electric Vehicle Race?

March 2026 · Comparison Report v1 · Edgen Research

TSLA (Tesla Inc.) | BYDDY (BYD Co. ADR) |

|---|---|

Rating: HOLD | Rating: BUY |

PT: $308 · +15% upside | PT: $82 · +32% upside |

Current: ~$267 · Mkt Cap ~$855B | Current: ~$62 · Mkt Cap ~$90B |

Summary

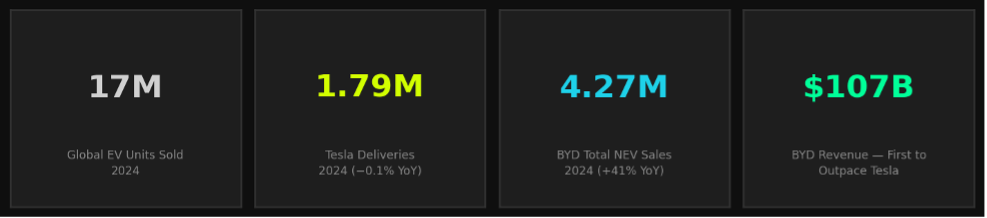

– BYD surpassed Tesla in total revenue for the first time in FY2024 — $107B vs $97.7B — driven by 41% volume growth to 4.27M total NEV sales, cementing its position as the world's top EV producer by units.

– Tesla's FY2024 net income fell 52.7% YoY to $7.09B as aggressive price cuts compressed margins; gross margin dropped to 17.9%, while BYD's full-year gross margin held at ~20.8%.

– Tesla's strategic advantage remains software and autonomy: FSD v13 and the upcoming Cybercab robotaxi fleet represent a monetisation pathway BYD does not yet have. Elon Musk's AI narrative keeps TSLA's P/S multiple at ~8.8x vs BYD's ~0.8x.

– BYD dominates on manufacturing scale, geographic reach (especially China, Southeast Asia, and emerging Europe), and cost leadership — its vertically integrated battery supply chain (BYD Blade) is the most durable structural moat in global EV manufacturing.

Sector Snapshot

The EV Wars: Why 2026 Is the Inflection Year

The global electric vehicle market delivered approximately 17 million units in 2024, growing roughly 25% year-on-year. China — the world's largest auto market by volume — accounted for nearly 60% of global EV sales, giving BYD a structural home-market advantage that no Western competitor can replicate without decade-long investment. For Tesla, 2024 was a year of brutal price compression: the company cut prices on core models up to 25% globally in an effort to defend market share, which successfully maintained delivery volumes but destroyed profitability as measured by gross margin.

The central thesis that separates these two companies is not volume or revenue — it is valuation thesis. Tesla is priced as an AI and autonomy company that manufactures cars as a near-term revenue bridge. BYD is priced as an automotive manufacturer executing at exceptional scale. The $855B vs $90B market cap gap reflects this entirely: investors who buy TSLA are betting on FSD, Optimus, and Dojo; investors who buy BYDDY are buying the world's most efficient EV manufacturing machine at 0.8x trailing revenue.

The inflection in 2026 is driven by two simultaneous developments: Tesla's Cybercab robotaxi launch (expected H2 2026), which would be the first commercially deployed autonomous vehicle at scale, and BYD's aggressive European and Southeast Asian market expansion — the company is targeting 500,000+ units outside China annually by 2027. Whichever catalyst arrives first will set the narrative for the next 24 months.

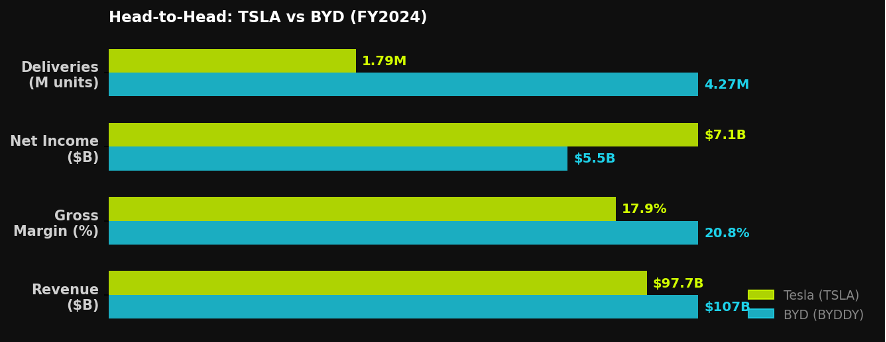

Head-to-Head: Key Metrics (FY2024)

Revenue, gross margin, net income, and deliveries — normalized for comparison. Bars reflect each company's score relative to the higher figure in each category.

Company Profiles

Tesla Inc. (NASDAQ: TSLA) — The AI Trojan Horse

Tesla was founded in 2003 and went public in 2010. It operates five Gigafactories globally (Fremont, Austin, Berlin, Shanghai, and Nevada) with combined annual capacity exceeding 2.35 million units. FY2024 revenue was $97.69B — essentially flat year-on-year (0.95% growth) — as energy storage (+67% YoY to $10B) offset declining automotive revenue growth. Net income collapsed 52.7% to $7.09B due to price cuts, warranty reserves, and higher R&D spend on FSD and Optimus.

The long-term bull case is not cars — it is Full Self-Driving monetisation, the Cybercab robotaxi network, and Optimus humanoid robots. Tesla's in-house Dojo supercomputer and FSD v13 (achieving a 5-6x improvement in miles per intervention vs v12) represent genuine AI infrastructure. Analyst bear cases centre on execution risk: Musk's simultaneous commitments to X, SpaceX, xAI, and DOGE create distraction risk at a company that requires intense founder-level operational focus.

BYD Company Limited (OTC: BYDDY) — The Manufacturing Juggernaut

BYD was founded in 1995 as a battery manufacturer and pivoted into electric vehicles in 2003. It is the only major automaker in the world that manufactures its own batteries, chips, motors, and body structures — a vertical integration stack that gives it a cost advantage of approximately 15-20% versus peers on comparable vehicle segments. FY2024 revenue was CNY 777.1B (~$107B USD), up 29% YoY, with net profit of CNY 40.25B (~$5.5B USD), up 34% YoY.

BYD's product portfolio spans 30+ models across the Dynasty (Han, Tang, Qin) and Ocean (Seal, Dolphin, Atto) series, priced from $10,000 to $150,000 — the widest EV price range of any manufacturer. The Blade Battery's safety performance (passing nail penetration tests that cause thermal runaway in competitors' cells) is a genuine technical differentiator. BYD's primary risk is geopolitical: EU tariffs reached 27% in 2025, and U.S. tariffs of 100% effectively exclude BYD from the American market entirely.

Peer Comparison: The Numbers Side by Side

Metric | TSLA | BYDDY |

|---|---|---|

Market Cap | ~$855B | ~$90B |

FY2024 Revenue | $97.7B | ~$107B (~CNY 777B) |

Revenue Growth YoY | +0.95% | +29% |

Gross Margin FY2024 | 17.9% | ~20.8% |

Net Income FY2024 | $7.09B | ~$5.5B |

Net Income Growth YoY | −52.7% | +34% |

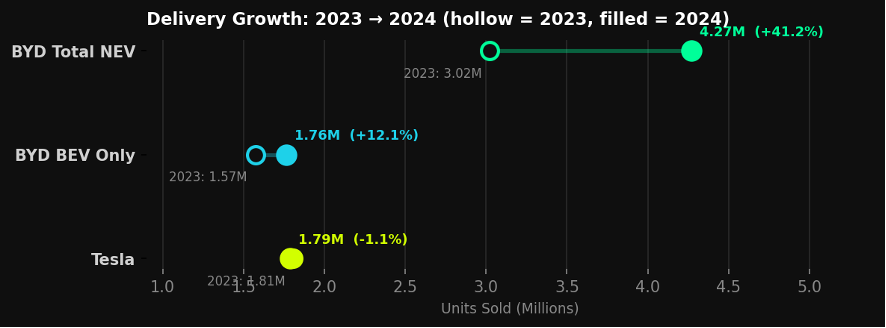

Total Deliveries 2024 | 1.789M | 4.27M (NEV total) |

BEV-Only Volume 2024 | 1.789M | 1.764M |

P/S Multiple | ~8.8x | ~0.8x |

Cash & Equivalents | ~$36.6B | ~$14B+ (est. USD) |

Employees | ~125,000 | ~900,000 |

Home Market | USA (global) | China (60% of sales) |

Key Moat | FSD / AI / Brand | Battery verticalisation |

Analyst Consensus PT | $308 | ~$82 (ADR) |

Delivery Growth: 2023 → 2024

Hollow circle = 2023 volume · Filled circle = 2024 volume · BYD Total NEV includes both BEV and PHEV models

Deep Dive: FSD vs Blade Battery — The Real Competitive Moats

The most important fact in the TSLA vs BYD debate is that these two companies are not competing on the same dimension. Tesla is building an autonomous vehicle software platform; BYD is building the world's most efficient EV manufacturing system. The question is not which is better — it is which moat has a larger long-term TAM.

FSD monetisation is Tesla's make-or-break variable. At $12,000 per purchase or $199/month subscription, FSD contributes near-100% gross margin revenue. If the Cybercab robotaxi network achieves commercial deployment in 2026, Tesla has the potential to generate $50-100B+ annually in software and robotaxi licensing revenue by 2030 — an asset class that BYD cannot replicate without a decade of AI R&D investment. The counter-argument is regulatory: robotaxi approval in the U.S. involves 50 state regulatory frameworks, and a single high-profile accident could trigger multi-year setbacks.

BYD's Blade Battery advantage is more durable in the near term. By manufacturing its own LFP cells at gigawatt-scale, BYD controls the largest single cost component (~35-40%) of an EV. This allows sub-$10,000 EV pricing in China — a market segment Tesla cannot profitably serve. The upcoming BYD's next-generation solid-state battery announcement (expected 2027-2028) would, if successful, extend this moat for another decade.

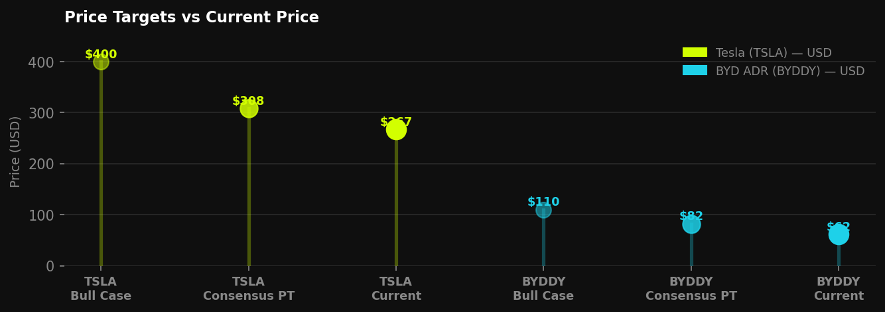

Price Targets vs Current Price

Current price (darkest dot) vs consensus PT vs bull case. TSLA priced for AI optionality. BYDDY priced on manufacturing fundamentals.

Valuation: Two Different Pricing Frameworks

TSLA trades at ~8.8x trailing revenue and ~120x trailing earnings — a premium that is only justifiable if FSD generates meaningful software revenue within 24 months. The base case ($308 PT) assumes Cybercab launches on schedule, FSD subscriber count doubles to 4M+, and gross margin recovers to 21%+ by FY2026. The bear case ($150) is triggered by Cybercab delays beyond Q2 2027 combined with further margin compression from Chinese competition in global markets.

BYDDY trades at 0.8x trailing revenue and ~16x earnings — a valuation that implies the market is pricing in significant geopolitical discount (EU + U.S. tariffs) and limited recognition of the global brand premium BYD is building outside China. The base case ($82 PT) assumes 15-20% international revenue growth in 2026, stable China margins, and no further tariff escalation. The bull case ($110) is triggered by a successful European manufacturing hub announcement (likely Germany or Hungary) and sustained net profit growth above 30%.

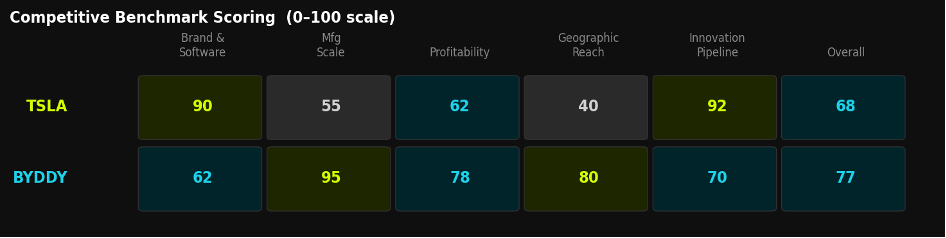

Competitive Benchmark Scoring

Five-dimension assessment · 0–100 scale · Overall = equal-weighted average

Three-Scenario Valuation

TSLA — Bull $400 / Base $308 / Bear $150. Bull requires Cybercab on schedule H2 2026, FSD subscriber count to 4M+, and gross margin recovery to 21%+. Bear is triggered by Cybercab delay + continued margin compression from Chinese competition.

BYDDY — Bull $110 / Base $82 / Bear $35. Bull requires European manufacturing hub announcement, 30%+ net profit growth, and tariff de-escalation. Bear case is a severe EU trade war + China domestic margin compression below 15%.

Stock | 🔴 Bear | Current | ⭐ Base PT | 🟢 Bull | Upside |

|---|---|---|---|---|---|

TSLA | $150 | $267 | $308 | $400 | +15% |

BYDDY | $35 | $62 | $82 | $110 | +32% |

Risks

Risk 1 — TSLA: FSD Regulatory & Execution Risk

Autonomous vehicle deployment is not a technical problem alone — it is a regulatory, legal, and political problem. A single high-profile Cybercab fatality could trigger federal investigations, congressional hearings, and 12-18 month deployment freezes. The FSD revenue model also depends on consumer willingness to pay $12,000+ for a feature that most drivers will never fully utilise, creating potential subscriber churn once the initial novelty wears off.

Risk 2 — BYDDY: Geopolitical & Tariff Escalation

BYD's TAM outside China is effectively zero today in the United States (100% tariff) and significantly compressed in Europe (27% tariff). Any further tariff escalation — particularly from a second-term trade policy focused on EV manufacturing — would eliminate the growth optionality that the $82 base case price target depends on. The company's entire international expansion thesis rests on tariff stability.

Risk 3 — Both: Chinese Price War Intensification

NIO, Li Auto, Xiaomi, Huawei-backed Aito, and dozens of smaller Chinese OEMs are in a structural price war that has compressed average selling prices 18-22% since 2022. BYD's cost leadership provides some buffer, but if Chinese domestic margins compress below 15%, the profitability thesis for BYDDY collapses. For Tesla, the Chinese market (25%+ of global deliveries) is simultaneously its fastest-growing market and the one most exposed to this dynamic.

Conclusion and Recommendations

These are two of the most asymmetric investment theses in global equity markets — not because one is obviously better, but because they represent radically different bets on what matters in the EV industry.

TSLA — HOLD | PT $308

Tesla is simultaneously the most overvalued car company and the most undervalued AI company in the world, depending on which model you use. The Hold rating reflects this tension: the base case upside (+15%) is modest, but the bull case ($400+) is substantial if Cybercab achieves commercialisation on schedule. Investors with a 3+ year horizon and conviction in autonomous vehicle regulation should use any pullback below $220 to build positions. Near-term, the stock is hostage to Musk's headline risk, which remains elevated.

BYDDY — BUY | PT $82

BYD is the most undervalued major automaker in the world at 0.8x revenue. Its manufacturing moat, battery technology lead, product breadth, and domestic market dominance are each worth more individually than the combined market cap implies. The primary catalysts to watch are European manufacturing hub announcements, which would remove the tariff overhang, and the next-generation solid-state battery timeline. For risk-tolerant investors seeking EM exposure to the EV secular theme, BYDDY at current levels offers a compelling margin of safety.

Frequently Asked Questions

Is TSLA a buy in 2026?

TSLA carries a Hold rating at $267 with a base case PT of $308 (+15%). The stock's fair value depends entirely on FSD commercialisation timelines. For investors who believe autonomous vehicles will be broadly deployed by 2028, the bull case ($400) is achievable; for investors who think regulatory approval takes until 2030+, the bear case ($150) is more credible.

Can BYD overtake Tesla globally?

BYD has already overtaken Tesla on revenue ($107B vs $97.7B in FY2024) and total NEV units (4.27M vs 1.79M). The one dimension where Tesla remains ahead is pure BEV volume: Tesla sold 1.789M vs BYD's 1.764M BEV-only units in 2024. By 2026, BYD's BEV volume is expected to reach 2.4-2.6M, definitively surpassing Tesla on every volume metric.

What is the biggest risk for each stock?

For TSLA: FSD regulatory failure or a Cybercab execution delay. One serious autonomous vehicle incident could reset the AI premium by 40-60%. For BYDDY: geopolitical tariff escalation. European tariffs moving from 27% to 40%+ would fundamentally alter the international expansion thesis that justifies the current price target.

Disclaimer

This document is for informational purposes only and does not constitute financial or investment advice. All investments involve risk. Past performance is not indicative of future results. Edgen does not hold positions in any securities mentioned. Ratings and price targets reflect the author's independent analysis as of March 2026 and are subject to change without notice. Consult a qualified financial advisor before making investment decisions.

Recommend

.32b68d3b2129e802.png)