Markets Confusing? Ask Edgen Search.

Instant answers, zero BS, and trading decisions your future self will thank you for.

Try Search Now

OKLO vs SMR vs NNE Nuclear Microreactor Competitive Analysis

EDGEN · ADVANCED NUCLEAR

OKLO vs SMR vs NNE Nuclear Microreactor Competitive Analysis

March 16, 2026 · Comparison Report

OKLO | SMR (NuScale) | NNE (Nano Nuclear) |

|---|---|---|

Rating: BUY | Rating: HOLD | Rating: SPEC BUY |

PT: $114.50 · +95% upside | PT: $28.00 · +39% upside | PT: $40.00 · +33% upside |

Current: ~$58.37 | Current: ~$20.18 | Current: ~$30.00 |

Summary

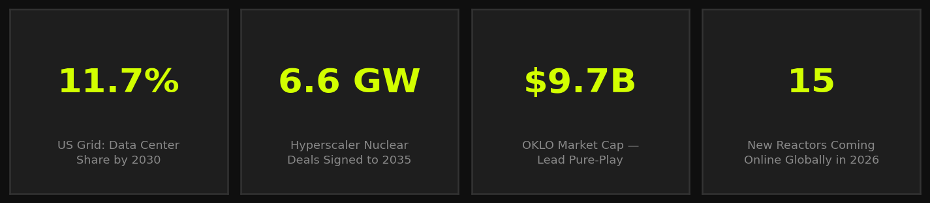

– U.S. data center power demand is on track to grow from 4.3% to 11.7% of total grid consumption by 2030, creating the largest structural tailwind in nuclear energy history.

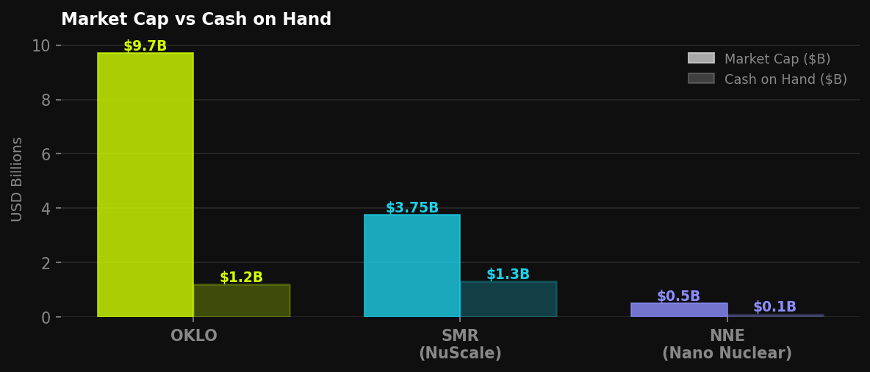

– OKLO leads on commercial momentum: a 1.2 GW Meta MOU, $1.2 billion in cash, and a July 2026 criticality test at Idaho National Laboratory make it the clearest first-mover at a $9.7 billion market cap.

– SMR (NuScale) holds the sector's only NRC Standard Design Approval — a genuine regulatory moat — but has diluted shareholders by 150% in twelve months and faces a class-action lawsuit; the stock is 80% off its all-time high.

– NNE (Nano Nuclear) is the highest-risk, highest-optionality name: 62 employees, zero revenue, but a differentiated portable-reactor thesis (ZEUS and ODIN) targeting defense, remote industrial, and off-grid data center use cases.

The New Nuclear Supercycle: Why 2026 Is the Inflection Year

The energy crisis underpinning advanced nuclear is not cyclical — it is structural. Generative AI and the data center buildout it demands have created a power consumption trajectory that no existing grid architecture can satisfy cleanly. The International Energy Agency projects that data centers, AI compute clusters, and cryptocurrency operations combined could account for4% of global electricity consumption by 2026, roughly double their 2022 share. In the United States, the math is even more extreme: grid-connected data center load is forecast to reach11.7% of total U.S. consumption by 2030, up from 4.3% just six years earlier.

Traditional renewable sources cannot serve this demand alone. Their intermittency is antithetical to the 99.9999% uptime requirements of hyperscale compute. Natural gas can fill the gap in the near term, but it undermines the carbon-neutrality pledges that Microsoft, Meta, Google, and Amazon have all made binding. That leaves one technology with the density, reliability, and zero-carbon profile to thread the needle: nuclear fission, specifically in the compact, modular formats that can be deployed on a data center campus rather than a utility grid.

BloombergNEF estimates that approximately15 reactors will come online globally in 2026, adding nearly 12 gigawatts of new capacity. The more significant signal, however, is on the demand side. Meta signed long-term agreements with Vistra, TerraPower, and Oklo that could unlock up to6.6 gigawatts of nuclear capacity by 2035. Microsoft signed a landmark deal to restart Three Mile Island. The hyperscalers are no longer hedging — they are placing concentrated, binding bets on nuclear as their long-term power foundation.

Company Profiles: Three Bets on the Same Thesis

Oklo Inc. (NYSE: OKLO) — The AI-Native Microreactor

Oklo was founded in 2013 by Jacob DeWitte and Caroline Cochran in Santa Clara, California, and went public via SPAC in 2024. It designs theAurorapowerhouse — a compact fast reactor in the 15–75 MWe range that runs on recycled nuclear fuel. The Aurora's size is precisely calibrated for the AI use case: a single unit can power a mid-sized data center campus, and multiple units can be co-located and scaled modularly without the multi-decade lead times of conventional gigawatt-scale plants.

As of Q3 2025, Oklo held$1.2 billion in cash and marketable securities, giving it the longest runway in the cohort. Its January 2026 announcement of a1.2 GW clean energy agreement with Metawas the company's most significant commercial milestone to date. The U.S. Department of Energy has also backed a$1.7 billion fuel recycling project in Tennessee, which would give Oklo a proprietary closed-loop HALEU supply chain that no competitor currently replicates. The near-term binary event is theAurora criticality test at Idaho National Laboratory, targeted for July 2026— a successful demonstration would be the most important technical de-risking event in the company's history. Current stock price is approximately $58.37, up roughly305% over the trailing twelve months, with a consensus analyst price target of $114.50.

NuScale Power Corporation (NYSE: SMR) — The Regulatory Pioneer

NuScale, founded in 2007 and headquartered in Corvallis, Oregon, holds a distinction no other company in this report can claim: it is theonly SMR designer to have received Standard Design Approval from the U.S. NRCfor its 77 MWe NuScale Power Module. The NPM is a light-water reactor built in modular, prefabricated units that can be assembled on-site, with a VOYGR plant configuration allowing up to 12 modules for a combined 924 MWe output.

NuScale generated$37.05 million in fiscal 2024 revenue— a 62% increase versus 2023 — primarily from front-end engineering and design studies on Romania's RoPower project. The picture darkens on the financial and legal fronts. Losses widened to$136.62 million in 2024, a 134% increase year-over-year. Shares outstanding increased by nearly150% over the trailing twelve months, and a class-action lawsuit filed March 15, 2026 in Oregon adds litigation overhang to an already complicated story. The stock is trading nearly 80% below its all-time high of $53.43.

NANO Nuclear Energy Inc. (NASDAQ: NNE) — The Asymmetric Option

NANO Nuclear Energy, listed on NASDAQ and headquartered in New York City, is the smallest and most nascent of the three. With just62 employees, NNE is effectively a deep technology startup. Its two flagship platforms —ZEUS(solid core battery reactor) andODIN(low-pressure coolant reactor) — target extreme portability: remote locations, military forward operating bases, off-grid data center nodes, and eventually space applications. NNE has raised over$100 millionthrough follow-on public offerings. Quarterly net loss has narrowed to$6.52 million in Q3 2025versus $8.05 million the prior quarter — a positive EPS surprise suggesting improving capital efficiency. Revenue remains zero.

Peer Comparison: The Numbers Side by Side

Metric | OKLO | SMR (NuScale) | NNE |

|---|---|---|---|

Market Cap | ~$9.7B | ~$3.75B | ~$500M |

Current Price | ~$58.37 | ~$20.18 | ~$28–32 |

52-Week Performance | +305% | ~−75% (ATH) | High vol. |

Cash on Hand | $1.2B | $1.3B | ~$100M+ |

Trailing Revenue TTM | $0 | ~$37M | $0 |

Annual Net Loss | ~$120M est. | −$136.6M (FY24) | ~$26M est. |

Share Dilution 12mo | Moderate | +150% | Moderate |

Reactor Size | 15–75 MWe | 77 MWe | Sub-10 MWe portable |

NRC Approval Status | Pre-application | SDA Approved ✓ | Pre-application |

First Revenue Est. | ~$16M (2027) | ~$31.5M (2025E) | <$10M (2026E) |

Consensus PT | $114.50 | $36.56 | ~$40 |

Key Commercial Deal | Meta 1.2 GW MOU | Romania RoPower FID | No binding deal |

Key Legal Risk | None | Class-action (OR 2026) | None |

Employees | ~200 | ~400 | 62 |

Sector Deep Dive: The Nuclear Licensing Gauntlet and HALEU Supply Chain

Every investor in this space must understand the NRC licensing process as the single most consequential variable in any financial model. The NRC operates on its own timeline, and that timeline does not compress under commercial pressure. A Standard Design Approval — the milestone NuScale has achieved and Oklo is pursuing — typically takes6 to 10 yearsand costs hundreds of millions of dollars in engineering submissions, testing data, and iterative review. The key metrics to monitor are not revenue multiples or EBITDA margins. The operative signals are NRC milestone progression, pipeline conversion rate (MOUs to binding PPAs), fuel supply chain security, and cost per installed MWe.

Oklo's fuel recycling initiative addresses supply chain security directly — converting existing nuclear waste intoHALEU feedstockreduces dependence on new enrichment capacity and potentially creates a proprietary cost advantage. NuScale's light-water design uses conventional low-enriched uranium and benefits from decades of established supply chains, sidestepping the HALEU bottleneck entirely. NNE's designs sidestep grid interconnection — the key bottleneck that plagues utility-scale nuclear — making them uniquely suited for stranded-load applications.

Valuation Analysis

At $58.37, the market assigns Oklo a $9.7 billion enterprise value on a company with zero revenue. The implied assumption is that the Aurora platform successfully navigates NRC licensing, that Meta's 1.2 GW MOU converts into binding contracts, and that Oklo can price its power at approximately $80–100/MWh — roughly 1.5x current U.S. wholesale power price, justified by its firm, carbon-free profile.

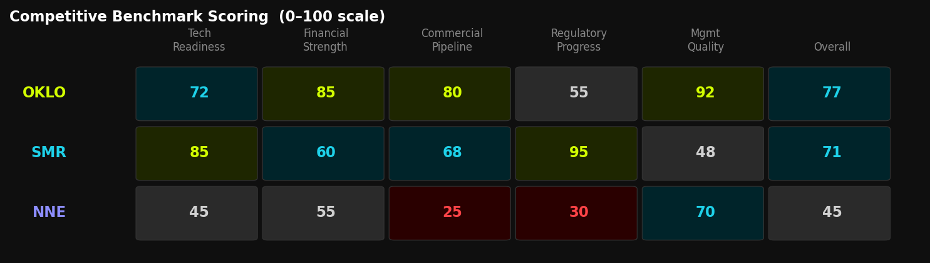

Competitive Benchmark Scoring

Five-dimension assessment · 0–100 scale · Overall score reflects equal-weighted average

Three-Scenario Valuation

OKLO — Bull $175 / Base $114 / Bear $25. INL criticality achieved, NRC commercial license accepted, Meta MOU converted to binding PPA. Base case: criticality achieved with minor delays, Meta deal generates additional binding contracts, revenue begins 2028. Bear: criticality test delayed, NRC raises design questions.

SMR — Bull $50 / Base $28 / Bear $8. Bull requires Romania on schedule, TVA contracts, lawsuit dismissed. Bear is triggered by adverse litigation + continued 150%+ dilution.

NNE — Bull $65 / Base $40 / Bear $9. Bull requires DoD/DARPA portable reactor contract. Bear: technology setbacks and cash runway pressure before commercial proof-of-concept

Stock | 🔴 Bear | Current | Base PT | 🟢 Bull | Upside |

|---|---|---|---|---|---|

OKLO | $25 | $58 | $114 | $175 | +95% |

SMR | $8 | $20 | $28 | $50 | +39% |

NNE | $9 | $30 | $40 | $65 | +33% |

Risks: Be Honest About What Could Go Wrong

Risk 1 — Regulatory Timeline Slippage

Unlike software or pharmaceuticals, nuclear regulatory processes cannot be accelerated by throwing money at them. Each NRC submission is a multi-year endeavor, and a single design question or safety concern can add 18–36 months to a timeline. Investors who model commercial revenue starting in 2027 or 2028 are almost certainly building in more optimism than the NRC's historical throughput supports. The Aurora criticality test at INL in July 2026, if delayed, would not merely miss a quarterly catalyst — it would reset the entire commercial licensing sequence for Oklo by potentially two or more years, and the stock's 95% implied upside to consensus target would evaporate quickly.

Risk 2 — Equity Dilution

NuScale's 150% share dilution over twelve months is the most aggressive in the cohort, and there is no visible path to cash flow positive operations before 2030 without continued equity issuance. Every passing quarter destroys per-share value regardless of commercial progress. Oklo's $1.2 billion cash position provides approximately 10+ years of runway at current burn rates — but that protection disappears the moment reactor construction begins, which will require capital raises measured in the billions.

Risk 3 — Competitive Displacement

Large utilities with deep balance sheets — Constellation, Vistra, NextEra — are not standing still. Established nuclear vendors like Westinghouse, GE-Hitachi, and Rolls-Royce are pursuing their own SMR designs with regulatory precedent and manufacturing scale that pure-play startups lack. If a utility-backed SMR achieves commercialisation before Oklo or NNE, the premium valuations currently awarded to the pure-plays compress rapidly. The hyperscalers will buy power from whoever can deliver it on time and on budget.

Conclusion and Recommendations

The structural case for nuclear energy as the power backbone of the AI era is not speculative — it is the operating assumption of the largest technology companies in the world. The question for investors in March 2026 is not whether to have nuclear exposure, but which vehicle offers the best risk-adjusted entry point.

Verdicts

OKLO — Buy | $114 PT

The combination of the largest cash reserve in the cohort, the clearest hyperscaler commercial relationship with Meta, the most differentiated technology narrative in fuel recycling plus a fast reactor, and the best management capital allocation track record makes Oklo the risk-adjusted winner. The July 2026 INL criticality test is the pivotal binary event — investors who believe in the engineering team's execution should consider building a position ahead of it, with position sizing calibrated to thebear case at $25.

SMR — Hold | $28 PT

The NRC Standard Design Approval is a genuine moat, and the Romania project provides real, if modest, revenue. But the combination of150% annual dilution, a class-action lawsuit, a stock already 80% off its all-time high, and no reactor deployments before 2030 creates too many headwinds today. The risk-reward improves materially if the lawsuit resolves and share issuance decelerates — watch those two signals before revisiting.

NNE — Spec Buy | $40 PT

The portable microreactor opportunity is genuinely differentiated. The improving quarterly loss trajectory and positive EPS surprise suggest management discipline that consensus underestimates. But with62 employees, zero revenue, and no binding commercial relationships, this is a venture bet embedded in a public equity wrapper. Position sizing must reflect that reality — for risk-tolerant investors only.

One Thing to Watch

The date that changes everything for this sector is the firstbinding power purchase agreementbetween an advanced SMR company and a hyperscaler — not an MOU, not a letter of intent, but a signed, bankable PPA with a specific capacity, delivery date, and pricing schedule. That document will determine which of these three companies is building the energy infrastructure of the 2030s and which is building a compelling slide deck.

Frequently Asked Questions

Q: Is OKLO stock a good buy right now in 2026?

OKLO carries a Buy rating with a base case price target of $114, representing approximately 95% upside from current levels near $58. The investment thesis depends critically on the July 2026 INL criticality test and conversion of the Meta MOU into a binding contract. Investors comfortable with pre-revenue, execution-dependent risk will find the risk-reward compelling; conservative investors should wait for the criticality milestone before initiating a position.

Q: What is the price target comparison for OKLO vs SMR vs NNE?

Our base case price targets are OKLO at $114, SMR (NuScale) at $28, and NNE at $40. Analyst consensus targets are similar: OKLO at $114.50, SMR at $36.56, and NNE at approximately $33–$47. All three companies are pre-revenue or near-pre-revenue, and price targets are highly sensitive to NRC licensing timeline assumptions.

Q: What are the main risks of investing in nuclear microreactor stocks?

The three primary risks are NRC regulatory timeline slippage (common to all three), equity dilution driven by ongoing cash burn before commercial revenue (most severe at SMR/NuScale at 150% annual share issuance), and competitive displacement from utility-backed SMR developers with deeper balance sheets. HALEU supply chain availability is a secondary risk specific to advanced fast reactor designs like Oklo's Aurora.

Q: How does OKLO compare to SMR and NNE on financial strength?

OKLO leads with $1.2 billion in cash and the lowest quarterly burn rate relative to its cash position, providing 10+ years of runway at current rates. SMR holds $1.3 billion but has been diluting shares at 150% annually. NNE has raised $100+ million — appropriate for its 62-person scale — but has the least buffer against unexpected development setbacks.

Q: When will nuclear microreactor companies start generating real revenue?

NuScale currently generates revenue ($37M in FY2024) from engineering and design studies, with projections reaching $286M by 2028. Oklo's first meaningful revenue is projected for 2027–2028 at roughly $16M initial, scaling toward commercial reactor operation in the early 2030s. NNE projects under $10M in FY2026 from consulting and licensing, with significant commercial revenue unlikely before the 2030s.

Disclaimer

This document is for informational purposes only and does not constitute financial or investment advice. All investments involve risk. Past performance is not indicative of future results. Edgen does not hold positions in any of the securities mentioned. Price targets and ratings reflect the author's independent analysis as of March 16, 2026, and are subject to change without notice. Consult a qualified financial advisor before making investment decisions.

Recommend

.32b68d3b2129e802.png)