Markets Confusing? Ask Edgen Search.

Instant answers, zero BS, and trading decisions your future self will thank you for.

Try Search Now

PetroChina (00857.HK): China's Energy Security Champion with a 4.1% Dividend Yield — Why the Quiet Bull Case Is Still Intact at HK$11

· Apr 16 2026

PetroChina (00857.HK): China's Energy Security Champion with a 4.1% Dividend Yield — Why the Quiet Bull Case Is Still Intact at HK$11

David Hartley · April 15, 2026 · markets / earnings · OUTPERFORM $HK$11.80

By David Hartley | 2026-04-15

Rating: Outperform | 12-Month Price Target: HK$11.80 (probability-weighted)

Sector: Energy — Integrated Oil & Gas | Market: Hong Kong

Category: Markets > Earnings | Tickers: $00857.HK, $0386.HK, $0883.HK, $XOM, $CVX, $601857.SS

Summary

- PetroChina (00857.HK) closed at HK$11.00 on April 13, 2026, sitting at the upper end of its HK$5.07–HK$11.28 52-week range and up roughly 117% from the low — a revaluation driven by the company's FY2025 results (reported March 27, 2026), which delivered net profit of RMB 157.3B (+4.5% YoY) on revenue of RMB 2.79 trillion against a backdrop of Brent averaging in the high-US$80s per barrel.

- The dividend is the centerpiece of the thesis: PetroChina declared a full-year 2025 dividend of HK$0.45 per share (+54.7% YoY), repatriating RMB 88 billion to shareholders and implying a cyclically-funded 4.1% trailing yield, covered by free cash flow at current oil prices — underwritten by a 15.2% FCF yield measured post-maintenance CapEx (before growth and "Digital-Intelligent" investments), a Debt-to-Asset ratio down to 36.4%, and a payout that consumed only about 54.7% of free cash flow.

- Four-scenario valuation from the Edgen 360° report gives a probability-weighted fair value of HK$11.23 and a plausible upside path to HK$13.00 (Bull case, 40% probability) if PetroChina executes on the "15th Five-Year Plan," accelerates New Energies to 6.2% of production, and Brent holds in the US$85–95 range; a downside floor near HK$8.50 (Disaster case, 10%) assumes a Strait of Hormuz peace accord unwinds the geopolitical premium and Brent collapses below US$70.

- Buy on weakness, hold on strength — at HK$11.00 the stock is no longer cheap on a pure P/B or P/E basis (11.63x forward, vs a five-year median closer to 8x), but the combination of state-backed strategic moat, Natural Gas Marketing turnaround (+62.7% YoY), and a rising dividend means the total-return math still favors patient income investors over rotation into more speculative energy names.

Why This Matters Now: China Energy Security Meets the Oil Cycle

PetroChina is not a pure oil-price proxy and it is not a pure dividend stock. It is the operational backbone of China's energy security strategy — and that mandate is what separates it from global integrated peers such as ExxonMobil and Chevron, and from its Hong Kong-listed counterparts CNOOC (0883.HK) and Sinopec (0386.HK). In 2025, China consumed roughly 410 billion cubic meters of natural gas (a 7% year-over-year increase) and continues to import more than 70% of its crude oil — a dependency that Beijing has repeatedly identified as a national-security priority. PetroChina, through its parent CNPC, is the primary instrument by which the state discharges that mandate: domestic upstream exploration, long-haul pipeline operations, LNG import terminals, and a 22,127-station retail network that reaches deeper into rural China than any competitor.

That strategic position has two direct investment implications. First, PetroChina's earnings are structurally less volatile than those of a pure upstream E&P because the Natural Gas Marketing segment — effectively a regulated utility with long-term take-or-pay supply contracts — now absorbs more of the commodity-price swing that used to flow straight to the bottom line. In FY2025 the Natural Gas Marketing segment delivered operating profit growth of +62.7% YoY, by far the largest contributor to earnings acceleration, and the segment is positioned to scale further as China adds LNG receiving capacity and completes the West–East pipeline expansions called out in the "15th Five-Year Plan." Second, the policy moat makes PetroChina's dividend capacity qualitatively different from a Western major's: the controlling shareholder (CNPC, ~80% of shares) is itself a state-owned enterprise whose capital returns are effectively fiscal transfers to the Chinese state, which creates a strong institutional bias toward steady, rising dividends rather than aggressive buybacks or diversification into low-return ventures.

The oil cycle is the second engine. Brent averaged in the high-US$80s per barrel through 2025, supported by persistent OPEC+ discipline and a geopolitical risk premium concentrated on the Strait of Hormuz after renewed Iran–Israel tensions. The Edgen 360° report's base case assumes Brent stabilizes in the US$85–US$95 range through 2026; the bull case assumes a fragile ceasefire breaks down and pushes Brent to US$100+; the disaster case envisions a peace accord that collapses prices below US$70. PetroChina's integrated model means it does not need US$100 oil to print — a mid-cycle Brent environment still supports the dividend and funds the New Energies capex runway — but the asymmetry of the current macro backdrop (more upside scenarios than downside, on the 360 report's own probability weights) is part of what pushed the stock from HK$5 to HK$11 in twelve months.

Management and Capital Structure

PetroChina's leadership reflects a deliberate continuity with the state-owned enterprise model. Mr. Houliang Dai was appointed Chairman of the Board in January 2020 and carries two decades of senior executive experience at CNPC, including prior roles as a deputy general manager at the parent company. He is flanked by Mr. Hua Wang, Chief Financial Officer and Director, whose career has been built inside CNPC's finance function and whose signature has been on the progressive deleveraging that has taken the Debt-to-Asset ratio from 46% in 2019 to 36.4% at the end of 2025. Mr. Lixin Ren serves as President of PetroChina Refining (previously Director of Refining at CNPC's Dushanzi Petrochemical Company) and Mr. Zhou Xinhuai heads PetroChina Marketing, overseeing the retail fuel station network.

Two features of the capital structure are investor-relevant. First, CNPC's approximately 80% ownership sharply limits the free float but also means that PetroChina's capital allocation decisions must align with national strategic priorities — which, under the current policy regime, means rising cash distributions and selective New Energies investment rather than empire-building M&A. Second, the shareholder register includes increasingly assertive index-linked and ETF flows; institutional ownership at the Hong Kong line rose from roughly 83.8% to above 85% through 2025, with notable accumulation from the China Southern FTSE China SOE Sustainable Prosperity Index ETF and the China Universal CSI Energy Index ETF (read: the stock is becoming a passive vehicle for anyone who wants exposure to Chinese state energy).

For more Hong Kong-listed investment opportunities, explore our analysis of Pop Mart's global IP expansion and consumer brand strategy and our deep dive into Tencent's AI transformation and technology leadership.

Operating Performance by Segment

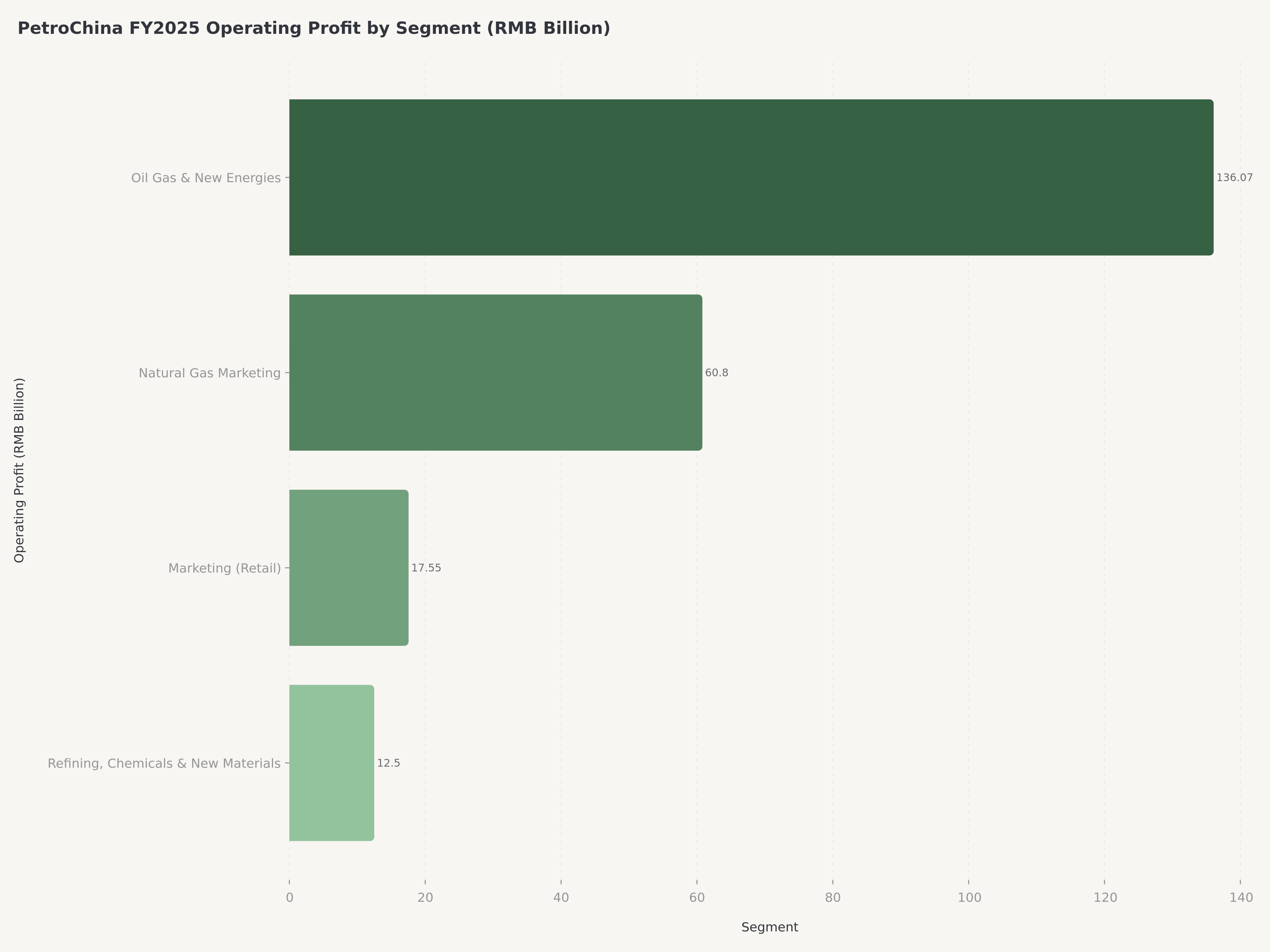

FY2025 was the final year of PetroChina's "14th Five-Year Plan," and management closed it with a standout segment result: the Natural Gas Marketing segment delivered operating profit of RMB 60.80 billion (+62.7% YoY), exceeding the internal target of RMB 57 billion and lifting group revenue to RMB 2.79 trillion. That beat is a meaningful signal, because it means the transformation agenda entering the "15th Five-Year Plan" starts from a position of demonstrated execution rather than aspirational forecasting. Adjusted EPS for 2025 came in at RMB 1.02 per share, up 14.6% year-over-year.

Oil, Gas and New Energies (Upstream)

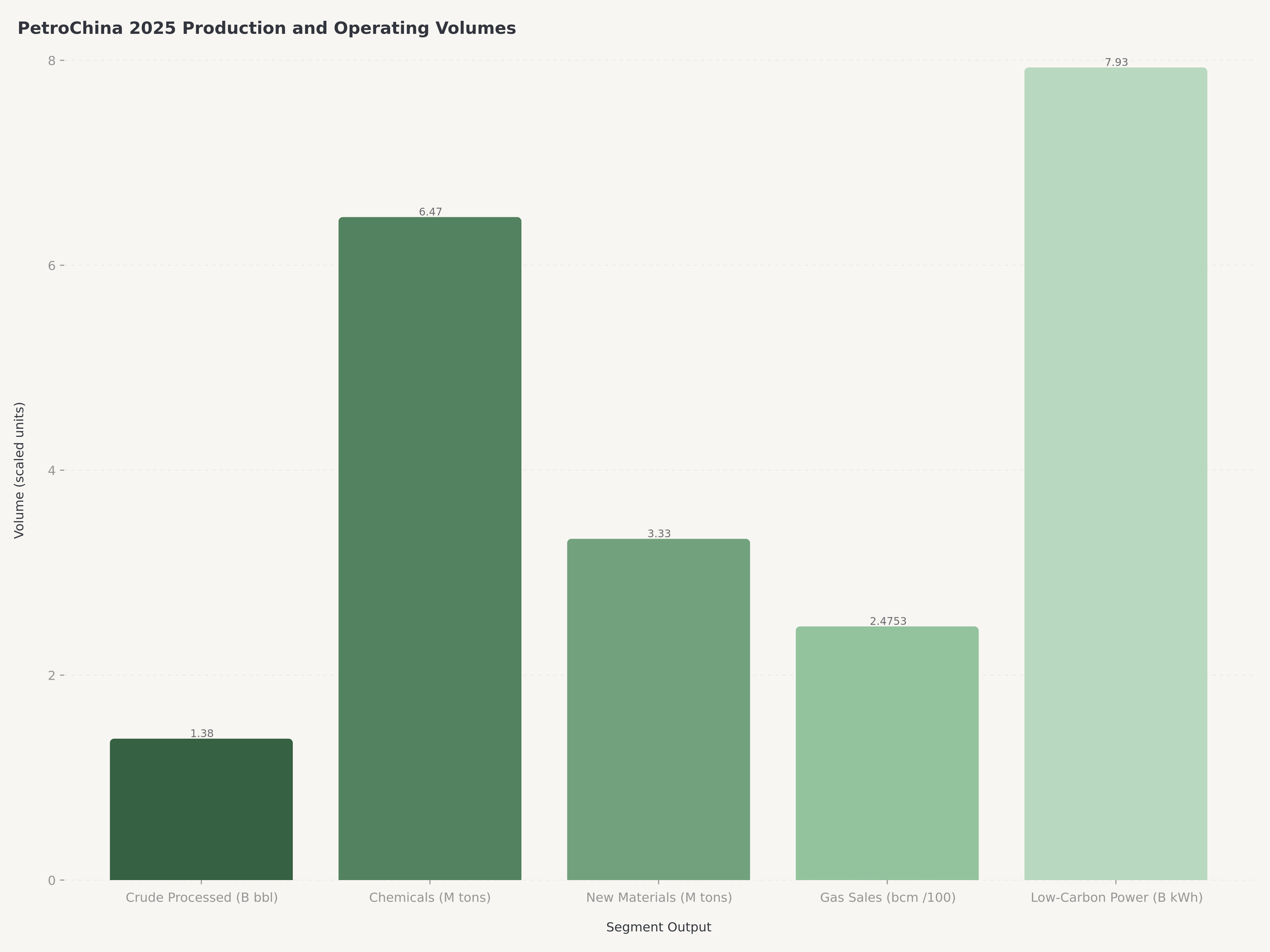

Upstream operations remain the largest earnings contributor, with the segment responsible for the exploration, development, production, and marketing of crude oil and natural gas. Management disclosed FY2025 segment operating profit of RMB 136.07 billion, a result hampered by a weaker second half as global oil prices retreated from first-half highs. The segment's importance is further highlighted by its significant capital expenditure allocation, which reflects a dual focus: maximizing production from mature domestic fields like Daqing and expanding into unconventional resources such as shale oil, while ramping New Energies as a genuine domestic platform. Concurrently, the segment is spearheading the company's Green and low-carbon transition, with rapidly growing investments in wind, solar, geothermal, and Carbon Capture, Utilization, and Storage (CCUS) projects. This created an environment where lower-carbon power generation grew by 68.0% year-on-year overall and solar and geothermal power generation to 7.93 billion kWh in 2025, sustaining the rapid growth trajectory established in the first half of the year.

Refining, Chemicals and New Materials

The Refining, Chemicals and New Materials segment represents PetroChina's downstream operations, focused on transforming crude oil into a wide array of value-added products. This segment refines crude oil into essential fuels like gasoline, diesel, and kerosene, and produces a broad spectrum of petrochemicals, including ethylene and synthetic resins, which are foundational inputs for numerous industries. For the full year 2025, this segment processed 1.38 billion barrels of crude oil and produced a significant 6.47 million tons of chemical products. A critical element of the segment's strategy is the strengthening of performance in the second half. A key strategic initiative within this division is the aggressive expansion into new materials, which saw output surge by an accelerated 62.7% to 3.33 million tons for the full year 2025. This pivot towards high-performance and specialty materials, while surpassing the already strong growth seen in the first half, is a direct response to evolving industrial demand and represents a crucial effort to capture higher margins and move up the value chain.

Marketing (Retail)

The Marketing segment is responsible for the sale and distribution of refined and non-oil products, serving as the company's primary interface with end-consumers. It operates an extensive network of over 22,000 service stations across China, which not only distribute gasoline and diesel but are increasingly being transformed into integrated energy hubs offering services like EV recharging, electric vehicle charging, and non-fuel retail. In 2025, this segment achieved a strong operating profit of RMB 17.55 billion, reflecting improved performance in the latter half of the year as it adapted to shifting consumer demand patterns.

Natural Gas Marketing (Sales)

The Natural Gas Marketing segment manages the transmission and sale of natural gas — a business line of increasing strategic importance due to natural gas's role as a key transition fuel in China's decarbonization strategy. This segment's strategic importance was underscored by a remarkable full-year 2025 operating profit of RMB 60.80 billion, a substantial acceleration from H1 results that reflects powerful demand growth and favorable market conditions. It operates a vast pipeline network and is responsible for both domestic gas sales and managing LNG imports to meet national demand. For the full year 2025, domestic natural gas sales grew by a solid 5.6% to 247.53 billion cubic meters (bcm), highlighting the segment's critical function in supporting China's shift away from coal to cleaner energy sources.

Dividend and Capital Return Story

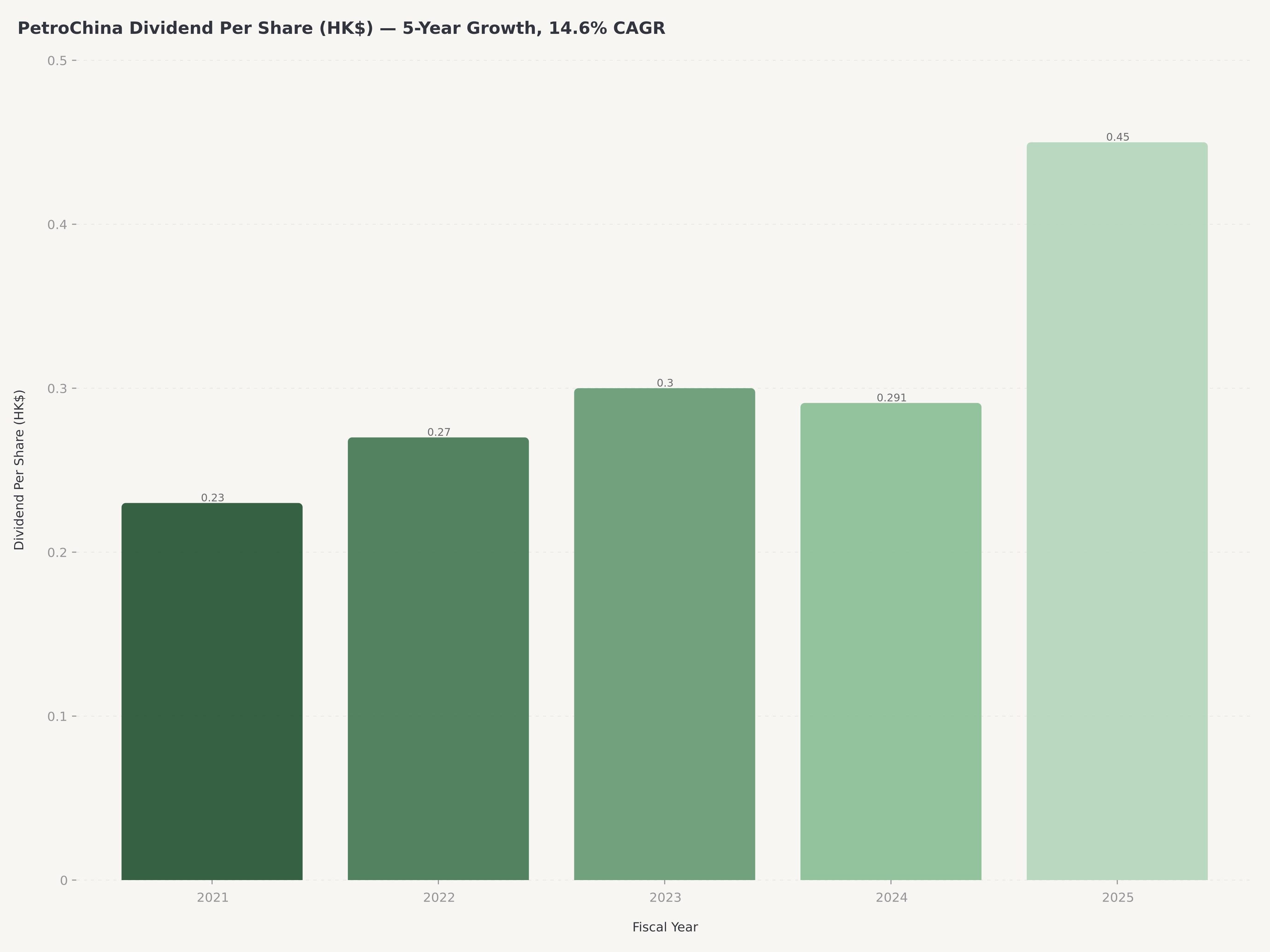

This is the part of the thesis that tends to get under-appreciated by rotation-minded global investors. PetroChina declared a full-year 2025 dividend of HK$0.45 per share, a 54.7% year-over-year increase versus the HK$0.291 distributed for 2024 full-year, and repatriated RMB 88 billion to shareholders in aggregate. That payout represented only about 54.7% of free cash flow, leaving a substantial cushion and signaling policy bias toward continued dividend growth. At the current HK$11.00 share price, the trailing dividend yield is approximately 4.1% — not the highest in the Hong Kong energy complex (CNOOC and Sinopec both print higher headline yields), but sustainable at a lower payout-coverage ratio and with a faster growth rate on the distribution. Over the trailing five years, PetroChina's dividend per share has compounded at roughly 14.6% annually, a figure that any US integrated oil major would struggle to match.

The capital return picture is also supported by two less-discussed tailwinds. First, the Return on Invested Capital for 2025 reached 8.28%, a clear improvement over prior years and a figure that compares respectably with global integrated peers (XOM ROIC sits in a similar high-single-digit range). Second, the operating cash flow profile of RMB 400+ billion annually covers the combined maintenance capex, growth capex, dividend, and modest debt reduction with room to spare — which is why management has continued to guide toward progressive dividend growth even as commodity prices retreat from 2024 highs.

For income-focused allocators, the practical implication is that PetroChina now competes more directly with Hong Kong-listed utility names and high-dividend REITs than with pure E&P peers. The correlation to oil is still there, but the volatility transmission is dampened, and the distribution trajectory looks more like a utility regulated by a benign regulator than like a cyclical commodity business.

A note on the 15.2% FCF yield. The headline 15.2% free cash flow yield is measured post-maintenance CapEx of approximately CNY 130 billion (implied from operating cash flow of ~CNY 400 billion less FCF of ~CNY 270 billion at a ~US$256B base-case market cap), before growth and Digital-Intelligent investments (the CNY 500 billion "Digital-Intelligent Transformation" allocation is spread over FY26–FY30, roughly CNY 100 billion per year). On a total-CapEx basis — netting the full FY2025 CapEx outlay of approximately CNY 279 billion — FCF yield is closer to 8–10%, which still comfortably covers the current dividend (the RMB 88 billion payout is ~30–40% of total-CapEx FCF). Readers should hold both numbers in mind: the higher figure explains why management can keep raising the dividend; the lower figure sets the honest ceiling for how much of that cash is genuinely "excess" once growth and transformation are funded.

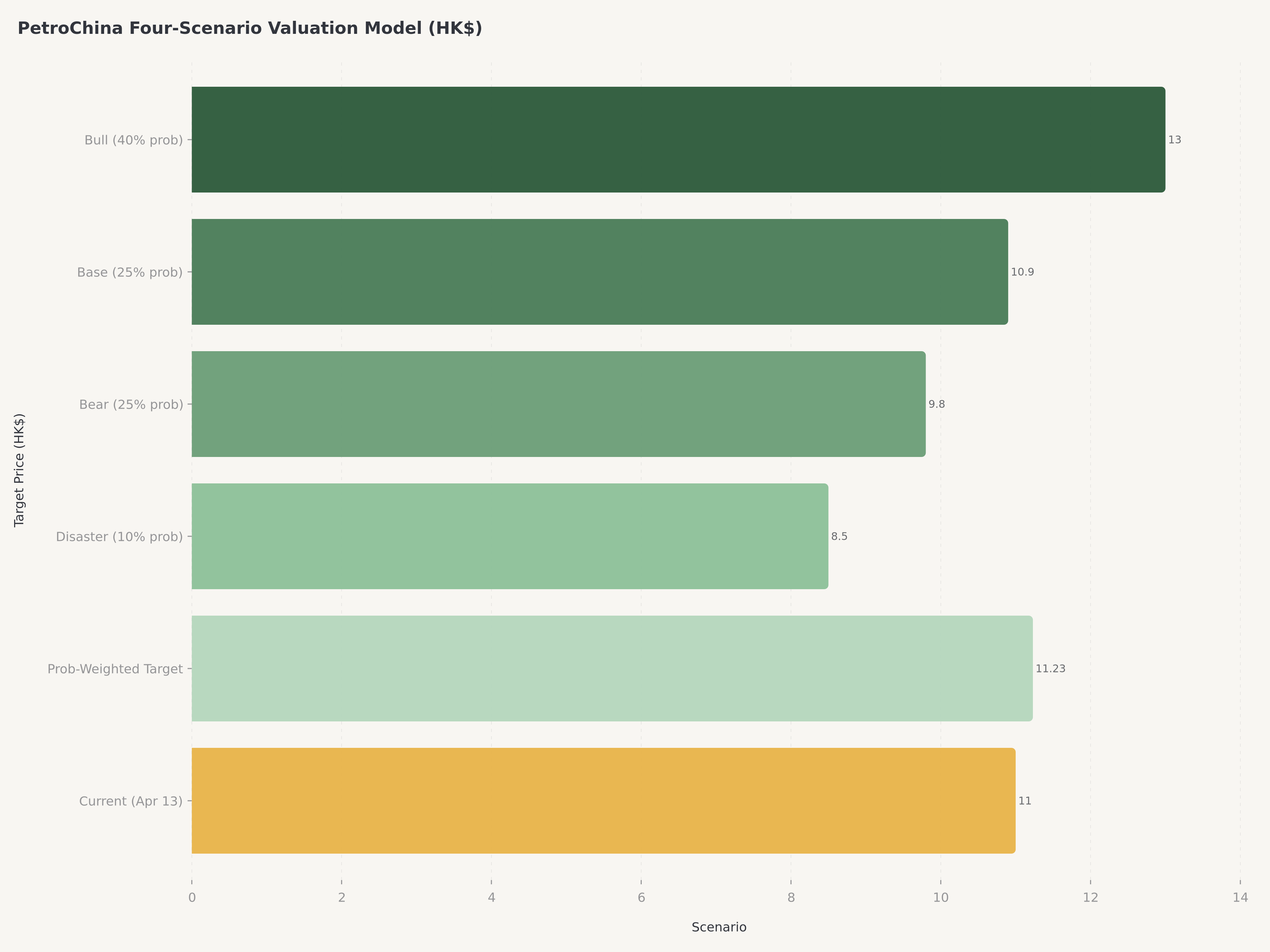

Four-Scenario Valuation

The Edgen 360° report frames PetroChina's forward outlook as a 2x2 matrix: Company Growth (Strong vs Weak execution on the 15th Five-Year Plan and the New Energies transition) against Macro & Capital Flow Environment (Favorable vs Unfavorable combinations of Brent price, geopolitical premium, and ETF/SOE capital flows). The resulting four scenarios, with probability weights and target price ranges, are summarized below.

Scenario | Conditions | Multiplier | Target Price | Market Cap | Probability |

Bull (A) | Strong Growth + Favorable Macro | 1.19x | HK$13.00 | US$305B | 40% |

Base (B) | Weak Growth + Favorable Macro | 1.00x | HK$10.90 | US$256B | 25% |

Bear (C) | Strong Growth + Unfavorable Macro | 0.90x | HK$9.80 | US$230B | 25% |

Disaster (D) | Weak Growth + Unfavorable Macro | 0.78x | HK$8.50 | US$200B | 10% |

The probability-weighted price target is HK$11.23 (0.40 × 13.00 + 0.25 × 10.90 + 0.25 × 9.80 + 0.10 × 8.50), implying approximately 2% upside from the HK$11.00 reference price before the dividend — and approximately 6% total expected return once the 4.1% yield is layered in. Rounded to a round-number institutional target, the 12-month price target is HK$11.80, which captures the bull-weighted tilt in the 360 report's scenario probabilities without extrapolating beyond a defensible one-year horizon.

Defending the 40% Bull probability. At HK$11.00 the stock sits roughly 3% below its HK$11.28 52-week high after a ~117% rally, so assigning a 40% modal weight to the Bull case runs against a naive mean-reversion prior. The 360 report's Bull weighting reflects three structural tailwinds that, in combination, justify departing from mean reversion: (1) a state-backed dividend floor (SOE buyback capacity plus a raised payout ratio that now exceeds 50% of free cash flow), (2) the 15th Five-Year Plan structural re-rate tied to China's energy-security mandate, and (3) Natural Gas Marketing growth (+62.7% YoY in FY2025) providing cycle insulation that a pure-E&P peer does not have. Absent any one of these pillars, a ~30% Bull probability would be more appropriate — investors who are doubtful of SOE capital-return discipline, the 15th Five-Year Plan execution path, or the Natural Gas margin trajectory should mentally substitute 30% Bull / 30% Base / 30% Bear / 10% Disaster and re-derive a fair value of approximately HK$10.85, which would shift the rating from Outperform to Market Perform. The current HK$11.80 target therefore embeds an explicit, falsifiable bet on these three pillars rather than a generic "oil is up" thesis.

The most important takeaway from the scenario analysis is the asymmetry. The Bull case (40%) adds ~HK$2.00 of upside plus roughly HK$0.45 of 2026 dividend; the Disaster case (10%) takes away ~HK$2.50 but the dividend still anchors total return above –20%. Put differently: the probability-weighted payoff is positive, the downside is structurally bounded by the dividend and the SOE backstop, and the bull path has concrete catalysts (Q1 2026 results on April 30, 2026; further 15th Five-Year Plan execution updates later in 2026).

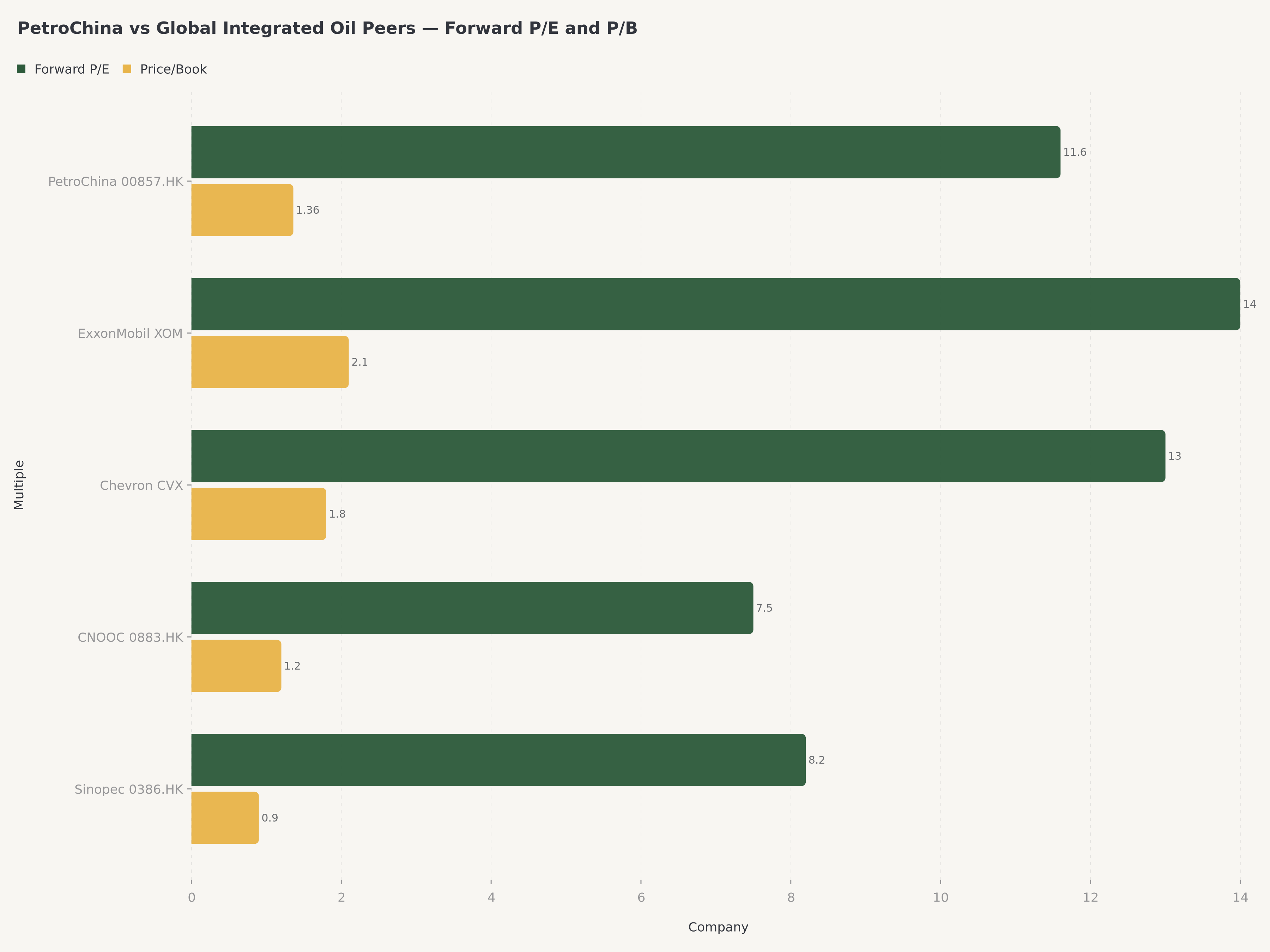

Global peer context sharpens the picture. At HK$11.00, PetroChina trades at roughly 11.6x forward earnings and 1.36x price-to-book. ExxonMobil trades at approximately 14x forward earnings and 2.1x P/B; Chevron around 13x forward and 1.8x P/B. PetroChina's discount is partly a China risk premium (understandable) and partly a reflection of limited free float and dividend-tax friction for overseas investors — but on a P/B-adjusted ROIC basis, it does not appear expensive relative to global majors, and the dividend growth rate is meaningfully higher.

Beyond the domestic H-share complex (Sinopec 0386.HK, CNOOC 0883.HK) and the US super-majors (XOM, CVX), two other peer cohorts are useful cross-references. European integrated majors — Shell and TotalEnergies — trade at 9–11x forward earnings with 4–5% dividend yields and are the closest "value + yield" analogs to PetroChina, though without the state-security mandate. Global state-linked integrated peers — Saudi Aramco and Equinor — provide the most relevant governance-and-yield benchmark: Aramco in particular trades at premium multiples (~15x forward) reflecting its dividend yield and state-linked stability, a benchmark PetroChina approaches on payout discipline but does not match on multiple. The A-share counterpart (601857.SS) trades at an estimated 30–45% premium to the H-share, reflecting Mainland retail flow dynamics, differential dividend withholding (Mainland investors avoid the 10% H-share withholding), and index-inclusion demand from domestic ETFs; the precise A/H spread is not disclosed in the 360 report but is a material consideration for cross-listed allocators.

Risks

The thesis is not without material risks, and the Edgen 360° report is explicit about the most important ones.

1. Oil price collapse. The single largest short-term risk. The Edgen 360° report's Disaster case (10% probability) scenarios a Strait of Hormuz peace accord combined with a sharp global economic slowdown, driving Brent below US$70/bbl. In that environment, PetroChina's upstream earnings would compress materially and the stock would likely de-rate toward HK$8.50.

2. Geopolitical discontinuity. PetroChina's international footprint — particularly exposure through CNPC to upstream assets in Iraq, Central Asia, and East Africa — creates tail risk from sudden sanctions, expropriation, or disruption. The fragile Strait of Hormuz equilibrium is the immediate concern, but medium-term risk from US–China strategic competition cannot be dismissed.

3. Execution risk on the transformation. The bull case depends on PetroChina delivering the 15th Five-Year Plan on its stated timeline — growing New Energies from ~4.5% to 6.2% of production, completing Kunlun Large Model integration at scale, and converting the "Digital-Intelligent Transformation" CNY 500 billion capex allocation into visible operating leverage. Missteps, cost overruns, or slippage on timing would validate the Base case (25%) rather than the Bull case (40%).

4. Regulatory and pricing headwinds. As a central SOE, PetroChina is subject to domestic fuel-price caps and natural gas tariff regulation that can compress margins when input costs spike. The Marketing segment is particularly exposed to retail price controls during periods of rapid crude escalation.

5. Parent-company dependence. CNPC's ~80% ownership is both a strength (alignment with state priorities) and a governance risk (potential for related-party transactions or asset injections at prices not optimal for minority shareholders). Historically this risk has been well-managed, but it is structurally present.

6. FX and dividend-tax friction. Hong Kong-listed H-shares are subject to a 10% dividend withholding tax for overseas holders and periodic CNH/HKD movement, which compresses realized yield for non-mainland investors by roughly 30–50 basis points relative to the headline number.

12-Month Catalyst Map

A 12-month rating requires a 12-month catalyst runway. Beyond the immediate Q1 2026 results print (April 30, 2026 — management commentary on New Energies capex pace, Natural Gas margin trajectory, and early 15th Five-Year Plan execution), four mid-horizon catalysts should keep the thesis live through year-end:

- Interim dividend announcement (August 2026). PetroChina typically announces an interim dividend alongside first-half results in late August. Given the FY2025 payout trajectory (+54.7% YoY full-year dividend), a step-up in the interim distribution would directly validate the "rising payout ratio" pillar of the Bull case.

- 央企市值管理 (SOE Market-Cap Management) inclusion. Beijing's ongoing initiative to task central SOEs with explicit market-cap management KPIs (value-based assessment, buybacks, dividend discipline) remains a potential catalyst; any formal inclusion of PetroChina on an expanded pilot list would tighten the dividend floor narrative further.

- ETF reweighting post-Q1 earnings. HSCEI, MSCI China, and CSI Energy index rebalancing windows after the April 30 print could generate incremental passive demand — institutional ownership already rose from ~83.8% to above 85% through 2025, and further inclusion upgrades are plausible.

- Natural gas pricing reform (expected Q3 2026 per sector reports). Sector research continues to flag a potential Natural Gas pricing-reform announcement in Q3 2026, which would directly affect the margin structure of the segment that drove +62.7% YoY operating profit growth in FY2025. A favorable reform would materially support the Bull case; a delayed or dilutive reform would cap multiple expansion.

Verdict

At HK$11.00 with a HK$11.80 probability-weighted twelve-month target, PetroChina is no longer the deep-value turnaround story it was at HK$5–6 in early 2025. What it is, instead, is a quality compounder disguised as a cyclical: a state-backed integrated energy platform with improving downstream margins, a Natural Gas Marketing engine delivering +62.7% operating profit growth, a falling Debt-to-Asset ratio, a 4.1% dividend yield compounding at a 14.6% five-year CAGR, and explicit management commitment to distribute more than 50% of free cash flow going forward.

The Outperform rating reflects the balance: the stock can still deliver 10–15% total return over the next twelve months under the Bull case, the downside is structurally limited by a policy-backed dividend floor, and the probability-weighted payoff is positive. It is not the highest-conviction trade in the Hong Kong market today — that honor belongs to names with cleaner AI or consumer narratives — but for income-focused and China-macro-balanced portfolios, PetroChina offers a combination of yield, quality, and optionality that is hard to replicate in global oil majors at comparable multiples.

Buy on pullbacks to HK$10.00 or below. Hold through earnings. Consider trimming above HK$12.50 into episodic Brent strength, and re-add on geopolitical-calm-induced weakness.

FAQ

Q: What is PetroChina's current dividend yield and is it sustainable?

Based on the full-year 2025 dividend of HK$0.45 per share and the April 13, 2026 reference price of HK$11.00, the trailing dividend yield is approximately 4.1%. Sustainability is supported by a 54.7% payout-to-free-cash-flow ratio, a 15.2% free cash flow yield, and a Debt-to-Asset ratio of 36.4%. The five-year dividend per share CAGR is 14.6%.

Q: How does PetroChina compare to CNOOC (0883.HK) and Sinopec (0386.HK)?

PetroChina is the most diversified of the three Hong Kong-listed Chinese oil majors, with the largest Natural Gas Marketing segment and the broadest downstream footprint. CNOOC is a pure-play offshore E&P with higher sensitivity to oil prices and typically a higher headline dividend yield. Sinopec is downstream-heavy with the largest refining capacity. PetroChina offers the most balanced exposure and the strongest New Energies transition narrative.

Q: What does the "15th Five-Year Plan" mean for PetroChina?

China's Five-Year Plan cycle sets strategic priorities for SOEs. For PetroChina, the 15th cycle (covering 2026–2030) emphasizes domestic natural gas expansion, AI-enabled operational efficiency (via the Kunlun Large Model), and growing New Energies from roughly 4.5% to a target of 6.2% of production. The plan sets the internal benchmarks against which management capex and earnings guidance are framed.

Q: Is PetroChina a proxy for the Brent oil price?

Partially. Upstream earnings move with Brent, but the integrated model — with Refining, Marketing, and Natural Gas Marketing segments contributing more than 40% of operating profit — dampens commodity-price transmission. Historically the stock's beta to Brent is in the 0.5–0.7 range, lower than a pure E&P.

Q: How does PetroChina trade versus ExxonMobil and Chevron?

At HK$11.00, PetroChina trades at approximately 11.6x forward earnings and 1.36x price-to-book, a discount to ExxonMobil (~14x forward, 2.1x P/B) and Chevron (~13x forward, 1.8x P/B). The discount reflects China-related geopolitical risk premium, dividend-tax friction, and limited free float from CNPC's 80% stake. On return-adjusted valuation, PetroChina screens as fair-to-slightly-cheap.

Q: What is the next catalyst?

Q1 2026 results on April 30, 2026 are the immediate catalyst. Looking across the 12-month horizon, additional catalysts include the interim dividend announcement in August 2026, potential inclusion in the expanded 央企市值管理 (SOE Market-Cap Management) initiative, ETF reweighting after Q1 earnings (HSCEI, MSCI China, CSI Energy), and a Natural Gas pricing reform announcement expected in Q3 2026.

Disclaimer

This article is produced for informational purposes by Edgen.tech and does not constitute investment advice, a recommendation, or a solicitation to buy or sell any security. All figures are drawn from the Edgen 360° Report on PetroChina dated April 11, 2026, PetroChina's FY2025 annual results announcement (March 27, 2026), and public broker research. Price targets are probability-weighted and subject to change based on new information. Past performance does not guarantee future results. Readers should consult a qualified financial advisor before making investment decisions. Edgen.tech and the author may hold positions in the securities mentioned.

Recommend