Pop Mart International: The LABUBU Phenomenon Propels a Global IP Empire Into Uncharted Territory

Pop Mart International: The LABUBU Phenomenon Propels a Global IP Empire Into Uncharted Territory

David Hartley · April 14, 2026 · markets / consumer-retail · BUY $246

By David Hartley | 2026-04-14

Rating: Buy | Price Target: HK$246 | Sector: Consumer Discretionary — Designer Toys & Collectibles

Category: Markets > Consumer & Retail | Earnings | Ticker: $09992.HK

Summary

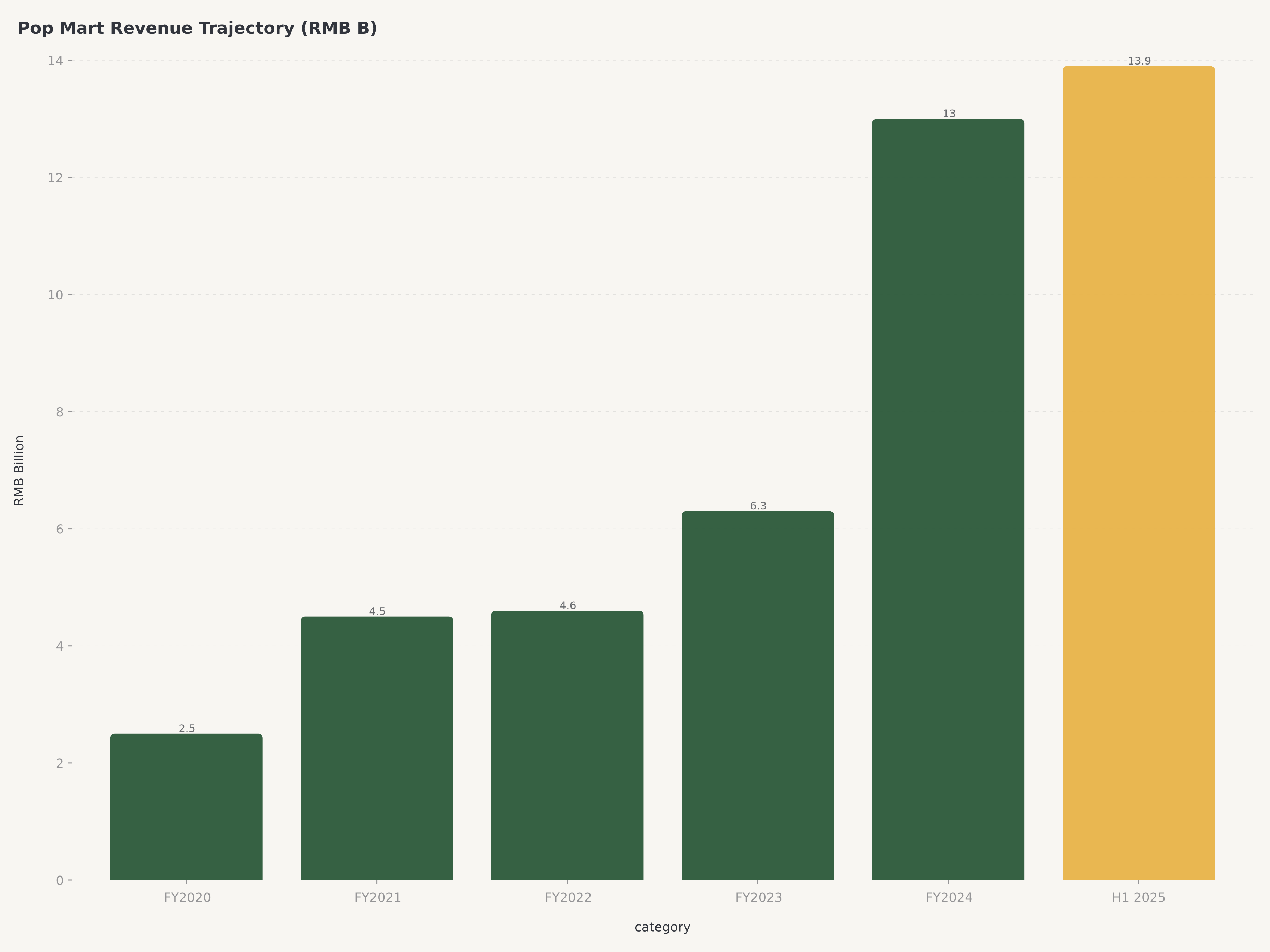

- H1 2025 revenue RMB 13.88B (+204.4% YoY), nearly matching full-year FY2024 revenue of RMB 13.04B in just six months; gross margin expanded to 70.3% from 64.0%

- THE MONSTERS franchise (led by LABUBU) generated RMB 4.81B in H1 2025 alone, a viral global phenomenon that single-handedly transformed Pop Mart from a China-centric collectibles company into a global cultural brand

- At HK$150.90, the stock trades at approximately 13.8x forward P/E after a severe correction from all-time highs — probability-weighted target price of HK$246 implies 63% upside from current levels

- Primary risk: extreme IP concentration on LABUBU/THE MONSTERS (35% of H1 2025 revenue), regulatory scrutiny of collectibles in China, and execution risk in scaling a culturally-driven business across 18 countries

The Global Collectibles Phenomenon: Why Pop Mart Matters Now

The global toy market is projected to expand at a CAGR of 5.98% between 2026 and 2034, reaching a value of $207.5 billion. More importantly, the high-margin segments where Pop Mart specializes are expected to dramatically outpace this growth. The global toy collectibles market, valued at $20.82 billion in 2026, is forecast to surge at a CAGR of 11.68% to reach $56.26 billion by 2035. This robust, double-digit growth outlook for collectibles validates Pop Mart's IP-centric strategy and its alignment with the market's primary value-creation vector.

Pop Mart's core market, China, presents an even more compelling growth trajectory. The Chinese toy market is projected to expand at a rate that outpaces global growth, solidifying its status as a key regional market. The rationale for this strong market growth is multi-faceted. Key drivers include the "kidult" trend, where adults purchase toys for themselves, and the phenomenon of "spiritual consumption," where products are valued for their emotional and aesthetic appeal over pure functionality. Pop Mart's business model is directly built to serve these evolving consumer behaviors.

What makes this moment uniquely compelling is the speed at which Pop Mart has internationalized. In H1 2025, overseas revenue (ex-China) surged to 40.3% of total sales, up from 22.8% in H1 2024, with Americas revenue exploding by 1,142.3% and Asia Pacific by 257.8%. This is not incremental international expansion — this is a company that has stumbled upon a global cultural phenomenon in LABUBU and is now racing to build the infrastructure to sustain it.

Wang Ning's Vision: From Blind Box Pioneer to Global IP Platform

Pop Mart's transformation from a niche collectibles retailer into a global entertainment platform is inseparable from the vision of its founder and CEO, Wang Ning (age 37). Wang established the company in 2010, and the executive team — including Mr. Si De as Chief Operating Officer, Mr. Moon Duk Il as VP of International Business, and Ms. Liu Ran as Executive Director — reflects a deliberate focus on maintaining domestic leadership while aggressively pursuing global growth.

The company's strategic evolution can be traced through three distinct phases. The first phase (2015-2020) established the "blind box" format as a commercial innovation in China, leveraging the psychological drivers of collectibility — surprise, scarcity, and social validation — to build a fiercely loyal customer base. The second phase (2021-2024) deepened the IP portfolio and vertical integration, with Pop Mart building capabilities spanning artist incubation, product design, manufacturing, retail distribution, and themed experiences. The third phase (2025-present) represents the explosive international breakout, catalyzed almost entirely by the viral success of LABUBU, a member of THE MONSTERS family created by artist Kasing Lung (龍家升).

The LABUBU phenomenon deserves particular attention. What began as one character within a broader IP portfolio became a global cultural moment when celebrities, influencers, and consumers across Southeast Asia, Europe, and the Americas embraced the character's distinctive "mischievous elf" aesthetic. This organic viral adoption — not driven by traditional marketing spend — created a self-reinforcing cycle of social media visibility, store traffic, and brand desirability that management is now working to institutionalize through flagship stores in landmark locations (the Louvre in Paris, Oxford Street in London, Ba Na Hills in Vietnam) and a rapidly expanding retail network.

Operating Performance: Numbers That Demand Attention

FY2024 — The Breakout Year

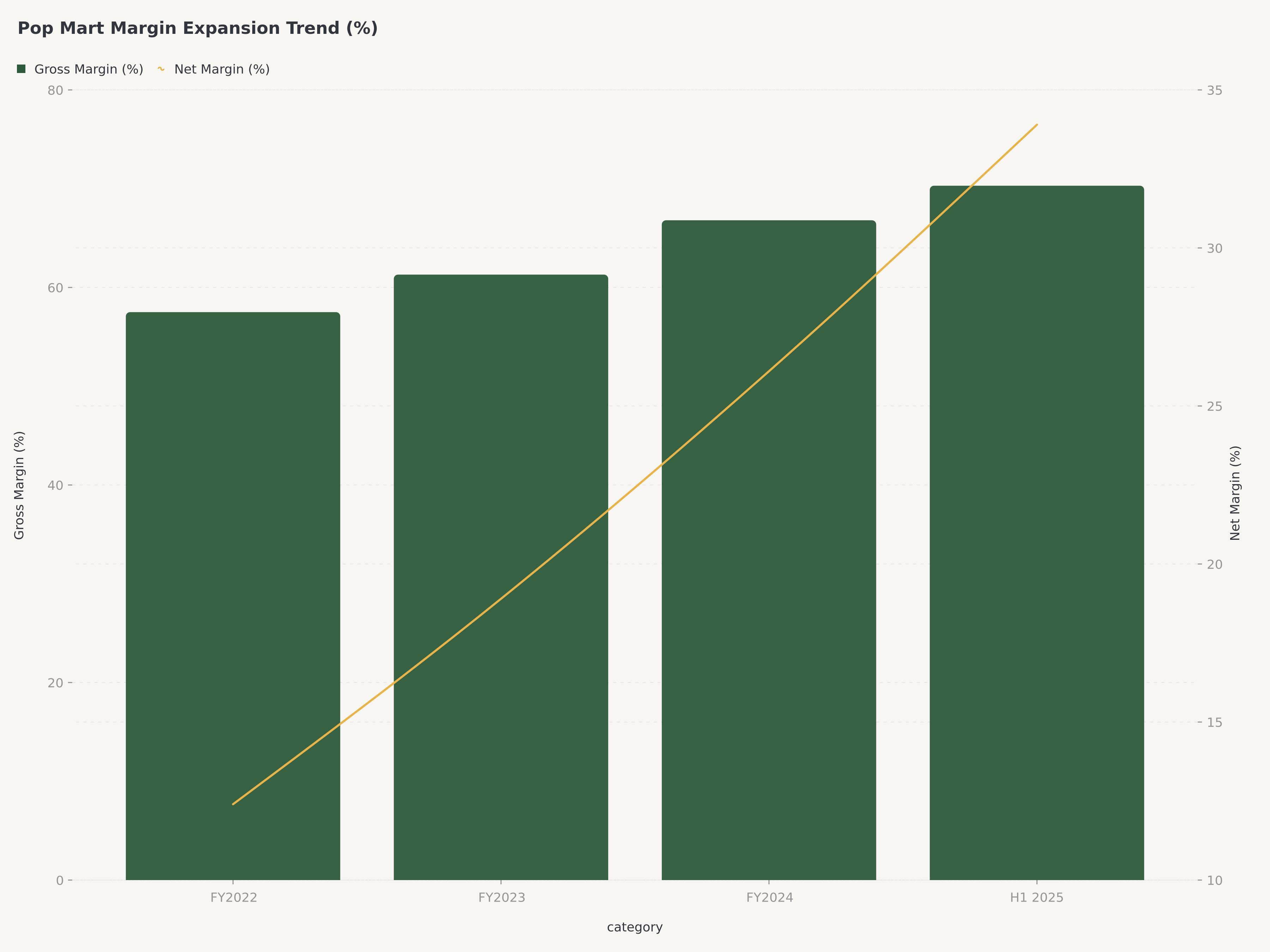

FY2024 marked Pop Mart's emergence as a genuine growth phenomenon. Full-year revenue reached RMB 13.04B, representing a staggering 106.9% year-on-year increase from RMB 6.30B in FY2023. To contextualize this: the company doubled its revenue in a single year, a feat that is extraordinary for a company of this scale. Gross profit margin expanded to 66.8% from 61.3%, driven by favorable sales mix shifts toward higher-margin plush products and international markets. Non-IFRS adjusted net profit surged to RMB 3.40B (+185.9% YoY), with adjusted net profit margin expanding from 18.9% to 26.1%.

The IP portfolio demonstrated remarkable breadth. For the first time, four IPs — THE MONSTERS, MOLLY, SKULLPANDA, and CRYBABY — each surpassed RMB 1 billion in annual revenue. A total of 13 artist IPs generated revenue exceeding RMB 100 million each. THE MONSTERS led the charge with RMB 3.04B (+726.6% YoY), propelled by the LABUBU phenomenon. MOLLY, the company's most iconic classic IP, contributed RMB 3.04B as well, demonstrating resilience in the original franchise. SKULLPANDA generated RMB 2.09B (+27.7%), while CRYBABY reached RMB 1.31B (+1,537.2%) as the fastest-growing emerging IP.

The revenue breakdown by channel reveals the power of Pop Mart's omni-channel model. Mainland China offline channels generated RMB 7.97B (+52.3%), supported by a net increase of 38 physical stores (to 401 total) and 110 roboshops (to 2,300). Online channels in China delivered RMB 2.37B, with Pop Draw (the digital blind box platform) at RMB 1.11B (+52.7%), Tmall at RMB 627.8M (+95.0%), and DouYin at RMB 601.2M (+112.2%). The company ranked first in the Tmall toy category during the 618 shopping festival.

International revenue was the standout, reaching RMB 5.07B (+375.2% YoY), accounting for 38.9% of total revenue — up from approximately 16% in FY2023. By year-end 2024, Pop Mart operated 130 physical stores and 192 roboshops in Hong Kong, Macao, Taiwan, and overseas markets, having opened its first offline stores in five new countries: Vietnam, Indonesia, the Philippines, Italy, and Spain.

H1 2025 — An Even More Extraordinary Half-Year

If FY2024 was the breakout, H1 2025 was confirmation that the growth trajectory is steepening, not plateauing. Revenue of RMB 13.88B (+204.4% YoY) in just six months nearly matched the entirety of FY2024. To state this plainly: Pop Mart generated almost as much revenue in the first half of 2025 as it did in all of 2024, which itself was a doubling year.

Gross margin expanded further to 70.3% from 64.0% in H1 2024, reflecting the dual tailwinds of geographic mix shift toward higher-margin international markets and product mix shift toward plush products. Operating profit exploded to RMB 6.04B (+436.5%), and net profit reached RMB 4.68B (+385.6%). Non-IFRS adjusted net profit margin hit 33.9%, up from 22.3% — a level of profitability that positions Pop Mart among the most profitable consumer companies globally.

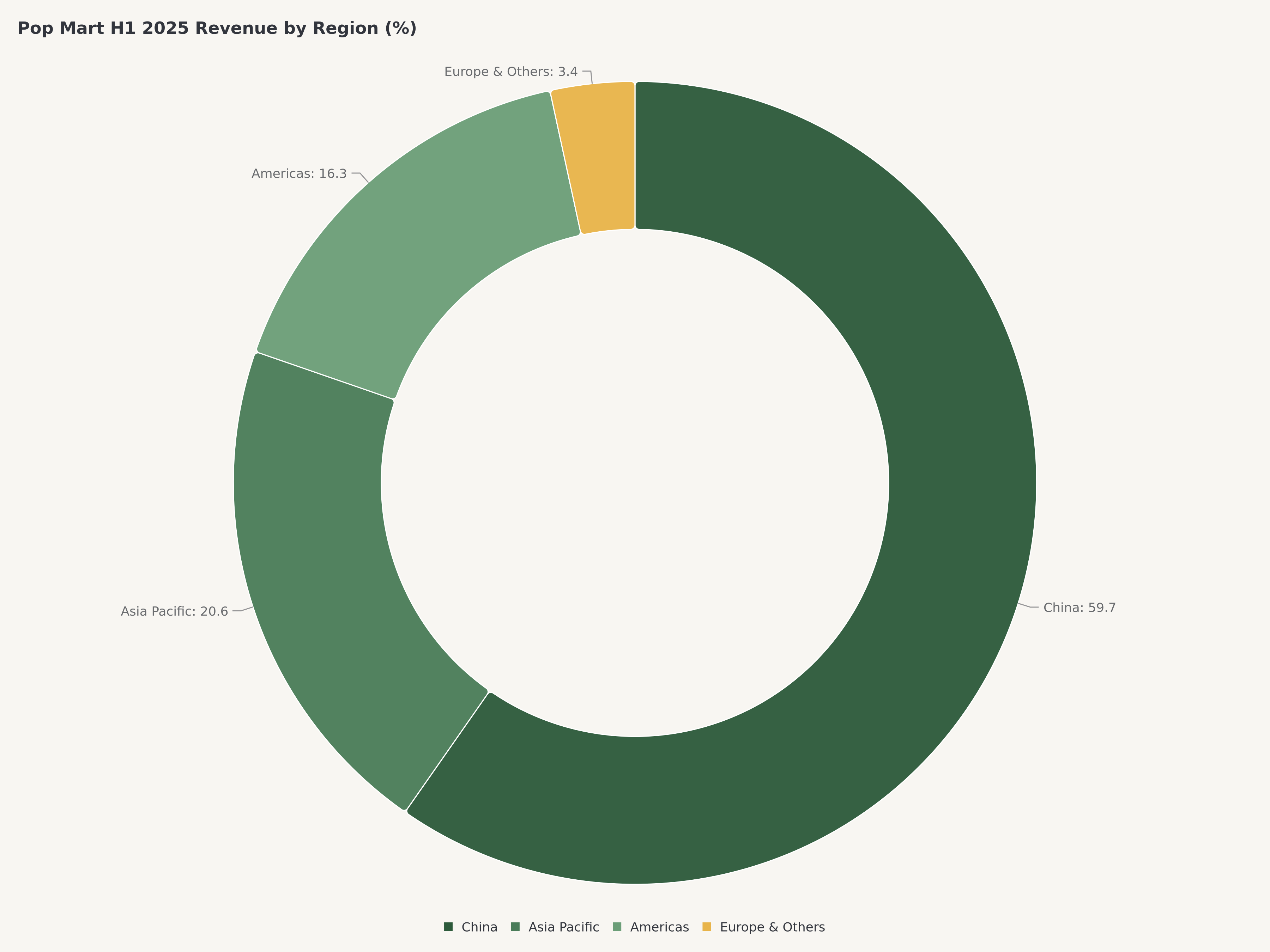

Revenue by geography paints a picture of genuinely global demand. China remained the largest market at RMB 8.28B (59.7% of total, +135.2% YoY), with 443 physical stores and 2,437 roboshops. Asia Pacific surged to RMB 2.85B (20.6%, +257.8%), with retail stores expanding from 39 to 69 and online channels growing 546.7%. The Americas delivered RMB 2.26B (16.3%, +1,142.3%), the most explosive growth in any region. Europe and other regions contributed RMB 477.7M (3.4%, +729.2%).

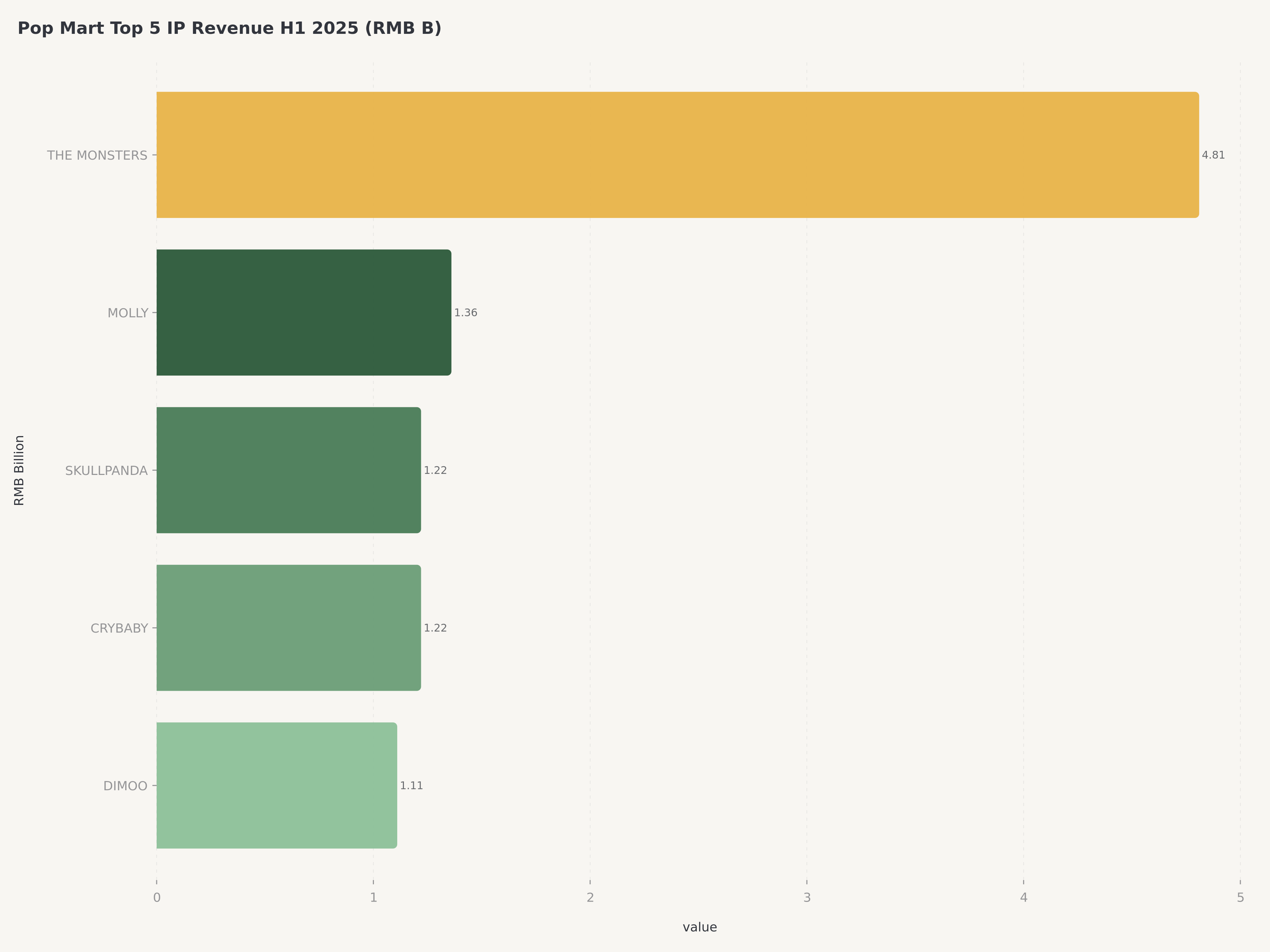

IP performance in H1 2025 underscored the LABUBU effect. THE MONSTERS generated RMB 4.81B, representing approximately 35% of total revenue. MOLLY contributed RMB 1.36B, SKULLPANDA RMB 1.22B, CRYBABY RMB 1.22B, and DIMOO RMB 1.11B — five IPs each exceeding RMB 1 billion in a single half-year.

The plush product category — a newer format featuring rotocast plush accessories — reached RMB 6.14B in H1 2025, accounting for 44.2% of revenue. This category did not exist at meaningful scale two years ago and is now nearly half of the business, illustrating the speed at which Pop Mart can capitalize on product-format innovation.

Competitive Analysis: The Moat

Pop Mart has constructed a formidable portfolio of strategic assets, anchored by a deeply entrenched intellectual property (IP) ecosystem and a sophisticated, data-driven product development engine.

Pillar 1 — IP Assets & Creative Pipeline. Pop Mart's core strength is a powerful, self-reinforcing data flywheel. The registered membership base in Mainland China surged by over 57% to 59.12 million by end of H1 2025 (from 46.08 million at end of FY2024), with member sales contributing 91.2% of total sales and a repeat purchase rate of 50.8%. This is not merely a customer loyalty program — it is a real-time consumer intelligence platform that informs IP development, product design, and inventory allocation. The company's legally fortified IP library, which by 2024 included over 1,200 trademarks, 1,600 copyrights, and 48 patents, translates directly into brand equity.

Pillar 2 — Global Distribution Network. As of June 30, 2025, Pop Mart operated 571 stores in 18 countries, with a net increase of 40 stores in H1 2025. The company also maintained 2,597 roboshops globally. The combination of physical retail (stores + roboshops), online DTC platforms (official website covering 37 countries, self-developed APP in 34), and third-party e-commerce (Shopee, Lazada, Amazon, TikTok) creates an omni-channel distribution moat that is extremely difficult to replicate. Flagship stores in globally recognized landmarks — the Louvre, Oxford Street, Ba Na Hills — serve as brand amplifiers that generate organic social media content worth far more than traditional advertising.

Pillar 3 — Operational Excellence. The inventory turnover acceleration from 102 days in FY2024 to 83 days in H1 2023 to just 37 days for H1 2025 is a remarkable achievement. This demonstrates a company that has mastered demand forecasting and supply chain management during a period of explosive growth — the opposite of what typically happens when consumer companies scale rapidly. The asset-light manufacturing model (partnering with factories in Mexico, Cambodia, and Indonesia) mitigates geopolitical risk and improves supply chain resilience.

Pillar 4 — Cultural & Emotional Moat. Perhaps most importantly, Pop Mart is not merely selling products — it is selling emotional and cultural experiences. The "blind box" mechanic taps into psychological drivers of surprise and collectibility. The IP characters (LABUBU, MOLLY, CRYBABY) develop emotional connections that create switching costs measured in sentiment, not economics. POP LAND (the theme park in Beijing), pop-up stores, artist signing events, and the POP TOY SHOW create real-world touchpoints that deepen community bonds. This is the moat that quantitative analysis struggles to capture but that drives repeat purchase behavior.

Valuation: A High-Stakes Opportunity at a Discount

What the Market Sees (Above Water): Pop Mart's stock has declined sharply from its all-time highs, with the stock price falling approximately 26.3% from peak levels. Forward P/E has compressed to approximately 13.8x, and the TTM P/E ratio has also compressed to approximately 13.8x. Analyst consensus has fractured following the FY2025 annual results release, with multiple downgrades triggering a wave of price target reductions. The market is repricing from hyper-growth expectations to a more moderate growth assumption, and the sentiment is decidedly cautious.

What Is Actually True (Below Water): At the current price of HK$150.90, the market is pricing Pop Mart as though the LABUBU phenomenon is a one-time event and international growth will decelerate sharply. The reality is that H1 2025 demonstrated continued acceleration, with gross margins expanding (not contracting) and operational leverage improving. The company holds approximately CNY17.2 billion (RMB) in cash and short-term investments, operating with virtually zero debt and a debt-to-equity ratio of just 12.8%. The current ratio stands at 3.01x, and the company's fortress balance sheet provides the financial flexibility to invest aggressively in international expansion without diluting existing shareholders.

The disconnect between operational performance (revenue nearly tripling, margins expanding, cash flow surging) and stock price behavior (significant decline from highs) creates the type of asymmetric opportunity that fundamentals-driven investors seek.

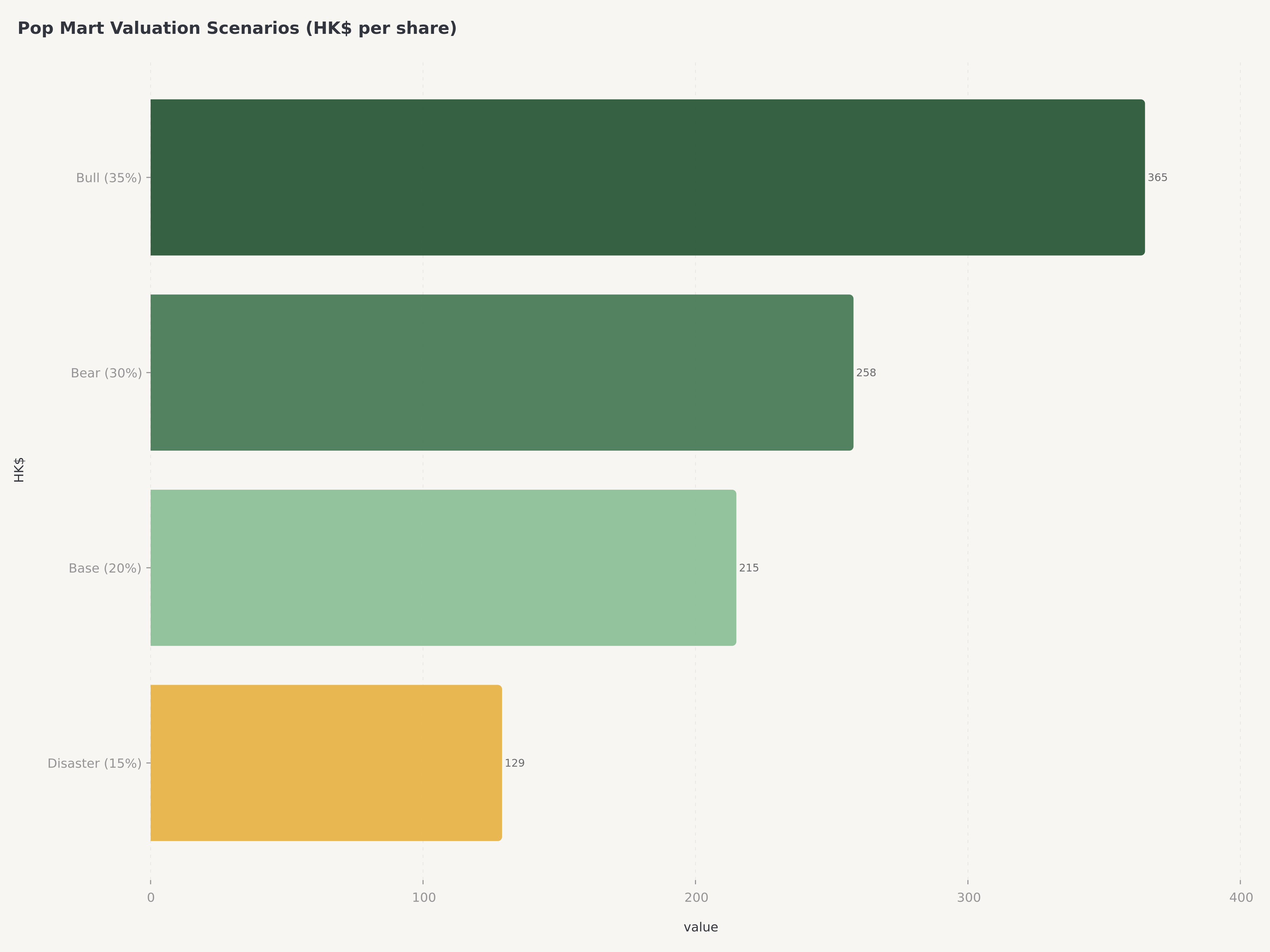

Four-Scenario Valuation Model:

Scenario | Target Market Cap (HK$B) | Per-Share Estimate | Key Assumptions | Probability |

Bull (A) | HK$423.8B – $480.8B | ~HK$322 – $365 | Strong growth execution + favorable macro; LABUBU momentum sustains; IP diversification succeeds; international revenues continue to accelerate | 35% |

Bear (C) | HK$282.8B – $339.8B | ~HK$215 – $258 | Strong company growth + unfavorable macro; broad market downturn compresses multiples despite solid operational execution | 30% |

Base (B) | HK$226.8B – $283.8B | ~HK$172 – $215 | Weaker company growth + favorable macro; LABUBU fever fades, growth decelerates to a more moderate profile, stock trades at a premium to consumer peers | 20% |

Disaster (D) | HK$113.8B – $169.8B | ~HK$86 – $129 | Weak growth + unfavorable macro; core LABUBU IP collapses, recessionary environment decimates discretionary spending | 15% |

Probability-Weighted Target Price: ~HK$246, implying approximately 63% upside from the current price of HK$150.90.

The consensus analyst target prices currently stand at: High HK$392.70, Mean HK$263.89, Low HK$106.03. Following the March 2025 earnings, Goldman Sachs downgraded to Neutral (PT HK$184), BofA Securities to Neutral (PT HK$170), while Deutsche Bank downgraded to Sell. Morgan Stanley maintained Overweight (PT HK$278) and UBS maintained Buy (PT HK$278). CMB International issued the most severe revision, slashing PT by 66.6% to HK$127.

We rate Buy on the probability-weighted analysis because the Bull and Bear scenarios (combined 65% probability) both imply significant upside from current levels. The current price appears to fully reflect the Base and Disaster scenarios, which together carry only 35% probability. The critical variable is whether Pop Mart's international execution — specifically its ability to sustain LABUBU momentum while diversifying the IP portfolio — can maintain the hyper-growth trajectory through H2 2025.

Risks: What Could Go Wrong

Risk 1: Extreme IP Concentration. THE MONSTERS (led by LABUBU) accounted for approximately 35% of H1 2025 revenue and an even larger share of incremental growth. This level of dependence on a single IP franchise is both the company's greatest strength and its greatest vulnerability. If LABUBU popularity fades — as all cultural phenomena eventually do — the company must have a credible successor IP ready to absorb the lost revenue. The encouraging sign is that MOLLY, SKULLPANDA, CRYBABY, and DIMOO each generate over RMB 1 billion, providing a diversification floor. The risk is that LABUBU's decline may be sudden rather than gradual if it follows the trajectory of other viral consumer trends.

Risk 2: Regulatory & Geopolitical Risks. The Chinese government's regulatory stance toward collectibles and "blind box" commerce remains a persistent background risk. While national guidelines from 2023 set the stage, the environment continues to be clarified through legal precedent, and recent court rulings reinforcing merchant liability for product quality defects highlight the evolving regulatory landscape. Additionally, Pop Mart's rapid international expansion exposes the company to an increasingly complex web of trade regulations, customs procedures, and local compliance requirements across 18 countries.

Risk 3: Execution Risk in Scaling a Culturally-Driven Business. Pop Mart's business model is fundamentally built on emotional and cultural resonance. What works in Southeast Asia may not translate to Europe or the Americas without significant localization. The company's store expansion strategy — from 130 international stores at end-2024 to potentially 200+ by end-2025 — creates substantial fixed-cost commitments that become liabilities if foot traffic disappoints. The shift from viral organic growth to sustained institutional growth requires a different set of organizational capabilities, and the management team's ability to make this transition is unproven at this scale.

Conclusion

Pop Mart International represents one of the most compelling high-growth consumer stories in global markets today. The company has achieved what few Chinese consumer brands have accomplished: genuine organic demand for its products across multiple continents, driven by the cultural resonance of its IP characters rather than aggressive price competition or commodity-driven exports. At HK$150.90, the market is pricing the stock as though the LABUBU phenomenon is over and international growth will revert to a moderate trajectory. Our analysis suggests this is too pessimistic — with a probability-weighted target price of HK$246 implying 63% upside, the risk-reward profile is attractive for investors with a 6-12 month horizon.

The investment thesis hinges on a single, critical question: can Pop Mart successfully transition from a company driven by a single viral IP phenomenon into a diversified, global entertainment conglomerate? The evidence from its IP pipeline, rapid international success, and expanding business lines (POP LAND, MEGA COLLECTION, plush products) provides a strong base for the bull case. However, the significant risks — IP concentration, regulatory uncertainty, and the extraordinary expectations baked into a company that needs to sustain triple-digit growth — demand position sizing discipline and ongoing monitoring.

For additional Hong Kong blue-chip analysis, read our coverage of PetroChina's oil and gas value investment case and our assessment of Tencent's AI transformation and platform ecosystem strategy.

FAQ

Is Pop Mart (09992.HK) stock a good investment in 2026?

Pop Mart is rated Buy with a probability-weighted target price of HK$246, implying approximately 63% upside from the current price of HK$150.90 as of April 2026. The company delivered extraordinary H1 2025 results with revenue of RMB 13.88B (+204.4% YoY) and gross margins of 70.3%. However, the stock carries significant risk due to heavy IP concentration on THE MONSTERS franchise (LABUBU) and the inherent unpredictability of culturally-driven consumer trends. Investors should size positions according to their tolerance for high-growth, high-volatility consumer discretionary stocks.

What is LABUBU and why is it important for Pop Mart?

LABUBU is a character within THE MONSTERS IP family, created by Hong Kong artist Kasing Lung. Originally a figure toy, LABUBU became a global viral phenomenon in 2024-2025 when its "mischievous elf" design resonated with consumers across Southeast Asia, Europe, and the Americas. In H1 2025, THE MONSTERS franchise (led by LABUBU) generated RMB 4.81B in revenue, representing approximately 35% of Pop Mart's total sales. The character's popularity has been amplified by celebrity endorsements, social media virality, and Pop Mart's strategic placement of flagship stores in globally iconic locations including the Louvre in Paris and Oxford Street in London.

How fast is Pop Mart growing internationally?

Pop Mart's international expansion is among the fastest in the global consumer sector. In H1 2025, Americas revenue grew by 1,142.3% YoY to RMB 2.26B, Asia Pacific by 257.8% to RMB 2.85B, and Europe by 729.2% to RMB 477.7M. International revenue as a share of total sales increased from approximately 22.8% in H1 2024 to 40.3% in H1 2025. The company now operates 571 stores in 18 countries with 2,597 roboshops globally, having expanded aggressively through both physical retail and e-commerce channels including Shopee, Amazon, and TikTok.

What are the biggest risks of investing in Pop Mart?

The three primary risks are: (1) IP concentration — THE MONSTERS/LABUBU accounts for 35% of revenue, and a decline in the character's popularity would significantly impact growth; (2) Regulatory risk — China's evolving regulations on collectibles and blind box commerce could restrict business practices; (3) Execution risk — scaling a culturally-driven brand across 18 countries requires localization capabilities that are unproven at this scale. Additionally, the stock has experienced significant volatility following the FY2025 results release, with multiple analyst downgrades reflecting concerns about growth sustainability.

How does Pop Mart compare to other toy and collectibles companies?

Pop Mart is unique among global toy companies in its IP-centric, direct-to-consumer model with 70.3% gross margins — significantly higher than traditional toy companies like Mattel (MAT) or Hasbro (HAS) which typically operate at 45-55% gross margins. The closest comparable is MINISO (MNSO), though MINISO operates a licensed-brand retail model rather than owning proprietary IP. Pop Mart's 33.9% non-IFRS net margin in H1 2025 positions it closer to luxury goods companies in profitability profile, despite operating in the mass-market consumer segment.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. The author and Edgen do not hold positions in the securities discussed. Past performance is not indicative of future results. Investors should conduct their own due diligence before making investment decisions.

Your money person, finally.

Try Edgen free. No credit card. No commitment.