Somniaのメタバースとゲームに特化したL1の見通しについて、戦略、パートナー、トークンモデル、カタリスト、評価を網羅します。新規ユーザー向けのシンプルなガイドはこちらをクリックしてください。

概要

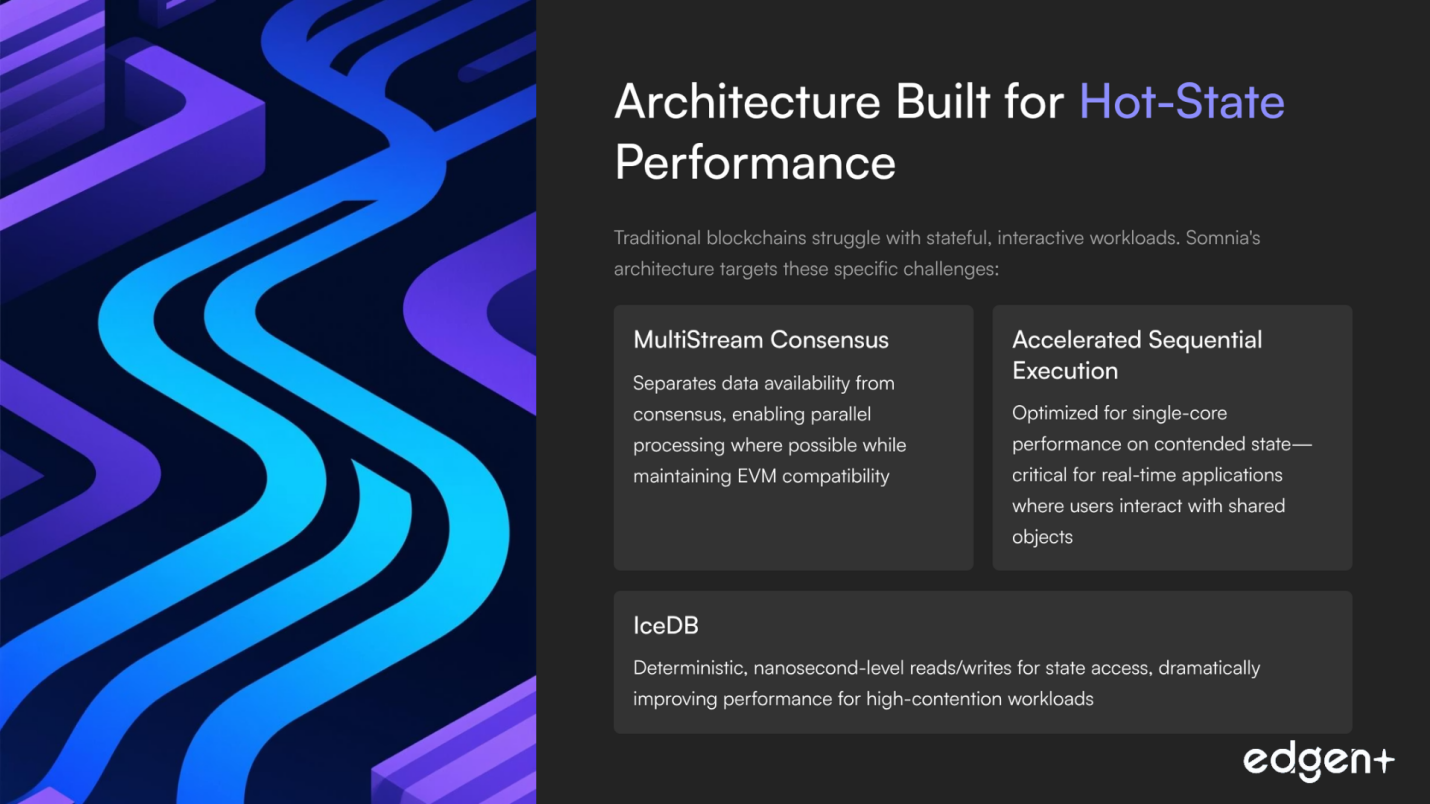

- リアルタイムアプリ向けの専用L1:アーキテクチャ(MultiStream Consensus、Accelerated Sequential Execution、IceDB)は、他のチェーンが苦労するホットステートワークロードをターゲットとしています。

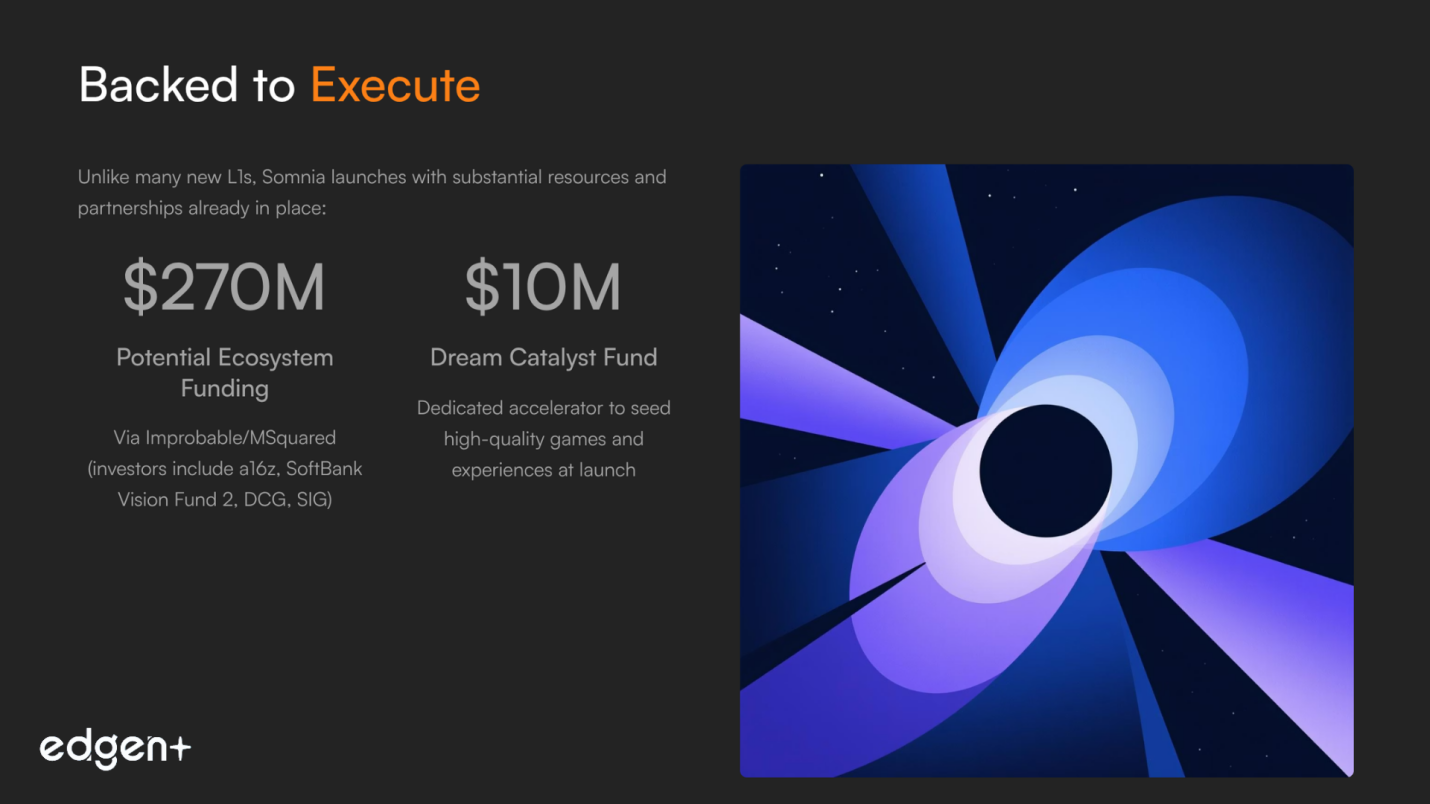

- 実行のための支援:Improbable/MSquaredを通じた最大2億7,000万ドルのエコシステム資金、Google Cloudのバリデーター/インフラストラクチャ、およびゲームを育成するための1,000万ドルのDream Catalystにより、Somniaは物語を出荷された製品に転換する位置付けにあります。

Somniaとは

Somniaは、メタバース規模のパフォーマンスのために設計されたEVM互換のレイヤー1(L1)であり、サブ秒のファイナリティ、サブセントの手数料、そして100万TPS以上の目標を掲げています。Somniaは一般的なDeFiスループットを追求するのではなく、ホットコンテンションのためのシングルコア実行を加速し、ハードウェア並列性を活用する設計を用いることで、MMO、ソーシャルグラフ、オンチェーンエコノミーといったステートフルでインタラクティブなワークロードに最適化されています。そのMultiStream Consensusはデータ可用性をコンセンサスから分離し、IceDBは決定論的なナノ秒レベルの読み書きを目指しています。

Improbable/MSquaredの仮想世界における深い経験に支えられ、Somniaは開発者の現実とインフラを一致させています。つまり、馴染みのあるEVMツール、ローコードビルダーズスタック(パートナー経由)、そして初日からコンテンツを提供するための資金豊富なアクセラレーターです。Google Cloudが検証およびAI/データセキュリティサービスをサポートし、Realm(Variance)のようなスタジオが開発準備を進める中、Somniaの提案は明確です。Web3体験が瞬時で構成可能に感じられる「夢のコンピュータ」であり、主流ユーザー向けに準備ができています。

I. 基本および戦略的分析

1) ビジョンと投資家のアライメント

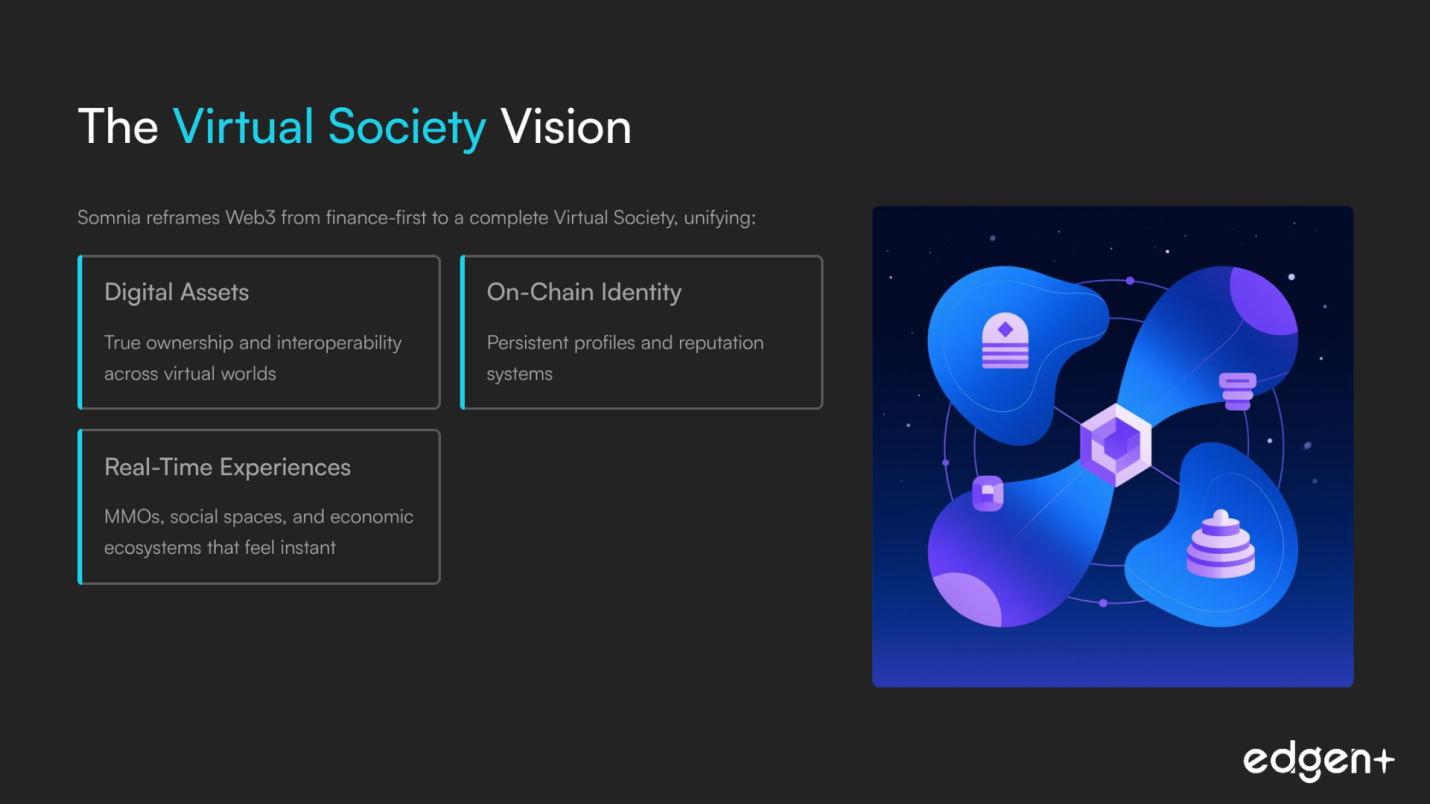

Somniaの論文は、メタバース/ソーシャル/ゲーム向けの特化型L1となることに焦点を当てています。ここでは、パフォーマンス、レイテンシー、コストが勝者を決定します。この戦略は、Web3を金融ファーストから仮想社会へと再構築し、資産、アイデンティティ、体験を統合します。パートナーシップ(例:Yuga Labsとの連携)と1,000万ドルのアクセラレーターは、コンテンツと開発者の成功に対する長期的なコミットメントを示しています。

2) チームと実行力

創設者であるPaul Thomas(Improbable)は、分散システムにおける稀有な深い経験をもたらし、Michelle KangはL1/L2の成長に関する専門知識を加えています。インフラの厳密さとGTM(Go-to-Market)のノウハウの融合は、複雑なプロトコルの提供とエコシステムのオンボーディングを支援し、新しいL1にとって非常に有望です。

3) 資本と承認

Somniaは従来の資金調達ラウンドではなく、Improbable/MSquaredを通じて最大2億7,000万ドルのエコシステム資金から恩恵を受けています(投資家にはa16z、SoftBank Vision Fund 2、DCG、SIGが含まれます)。Google Cloudはエンタープライズレベルでの検証(バリデーター + AI/データ/セキュリティ)をサポートし、SequenceとRaribleは開発者と市場の準備を加速させます。

4) 市場機会と適合性

オンチェーンゲーム/メタバースは大規模で拡大している市場です。Somniaは、EVMに精通し、信頼性の高い、高競合性能を必要とするビルダーにサービスを提供し、さらに助成金、SDK、流通を提供することで、技術的および金銭的な移行コストの両方を削減します。

5) 競争上の地位と差別化要因

ゲーム中心のEVMチェーン(Ronin、Immutable zkEVM、GalaChain)および高スループットのL1(Solana、Aptos)と競合します。差別化要因:ホットステート実行に焦点を当てた設計、完全なEVM、野心的な「仮想社会」の物語、そしてImprobable社が持つ確かな仮想世界での実績です。

基本的な見解:整合された資本、信頼できるパートナー、そしてリアルタイムのオンチェーン世界向けに特別に構築されたデザインにより、目覚ましい基盤的強みを持っています。

II. プレローンチエコシステムとGo-to-Market

1) コミュニティと物語の勢い

テストネットとインセンティブによって、ファネルの上位の成長は大規模です。現在の機会は、広範な関心を深い関与へと転換し、コミュニケーションを制度化し、出荷されたdAppsを強調し、コミュニティのエネルギーをメインネット利用へと導くことです。

2) オンチェーンフットプリント

テストネットの活動はストレステストの規模に達しており、有用なシステム実証の場となっています。TGE後の主要なKPIは、生のトランザクション数ではなく、質の高い利用(DAU、保持されているウォレット、稼働中のdApps)です。

3) パートナーシップと準備状況

- Google Cloud: ビルダー向けのバリデーター + AI/データ/セキュリティ統合。

- Sequence: Somnia Builder向けのスマートウォレット、Unity/Unreal SDK、マーケットプレイススタック。

- Uprising Labs: 高品質なゲームを育成するための1,000万ドルのDream Catalyst。

これら全体で、コードからユーザーへの摩擦を減らし、初日からのコンテンツを確保するのに役立ちます。

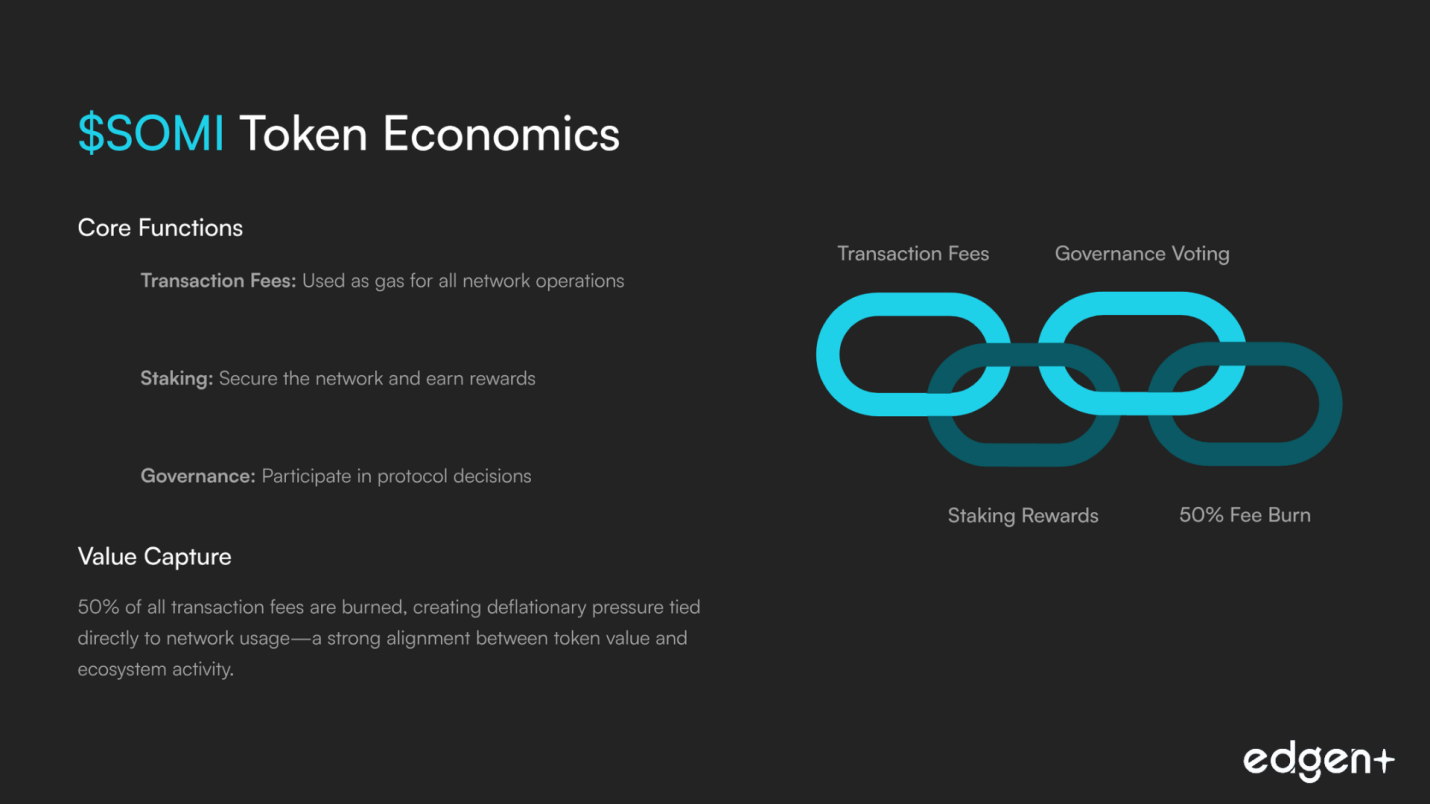

4) トークノミクスと価値の蓄積(現在)

$SOMI:ガス、ステーキング、ガバナンスに使用されます。50%の手数料バーンは、使用量と価値を連動させます。エアドロップ(供給量の5%)は、週ごとのメインネットクエストを通じてベスティングされます(TGE時に20%が流動化。約80%は、約60日間にわたる活動によって制限されます)。これにより、開始時から実際の参加が促進されます。

GTMの見解:非常に有望です。技術スタック、プログラム、パートナーは、強力な開発者ベロシティを示唆しています。初日の信頼を最大化するために、ローンチオペレーション(カストディ/MM/流動性通信)を明確にする必要があります。

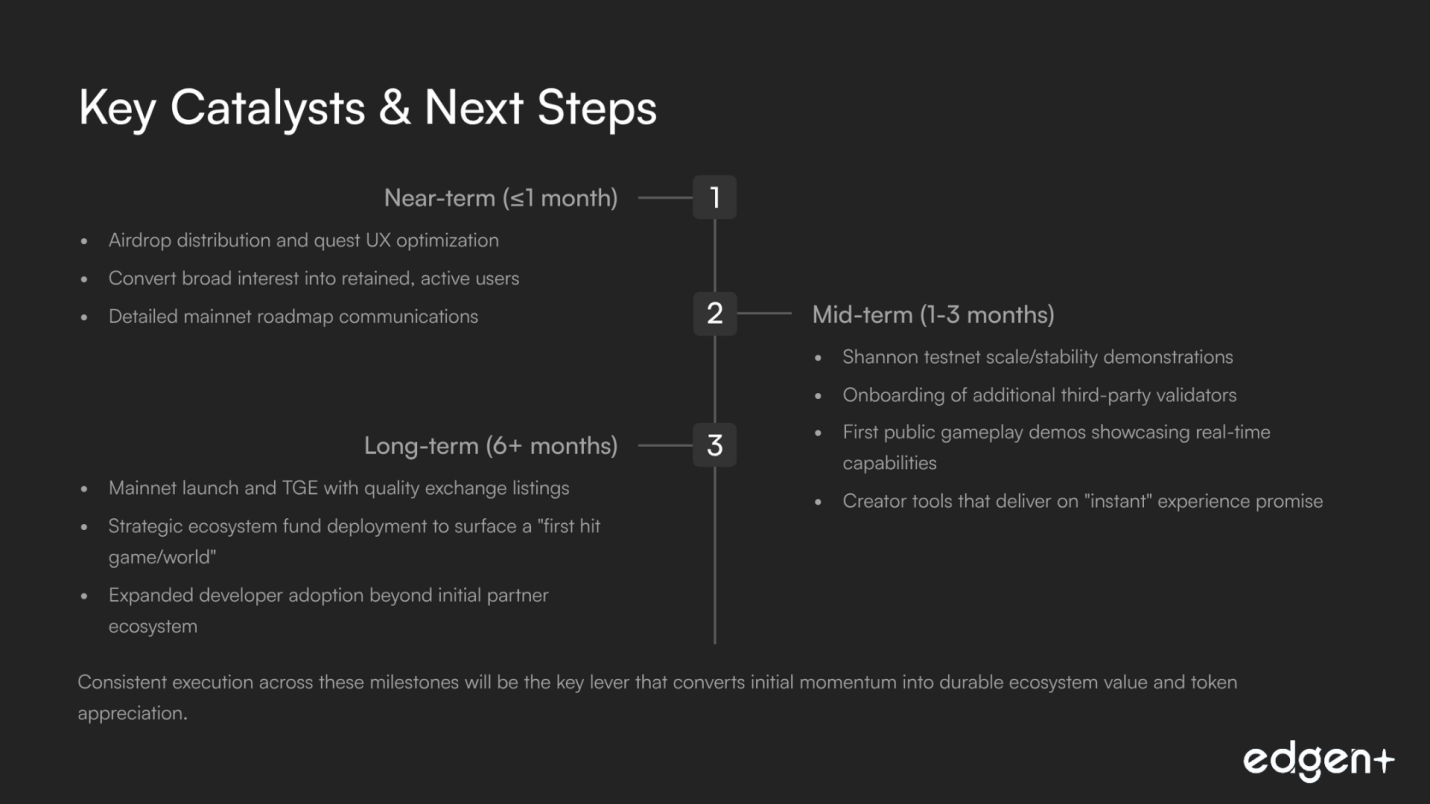

III. 将来分析(触媒と機会)

短期(1ヶ月以内):

- エアドロップからの学びと、非常に分かりやすいクエストUXを伝えること。広範な関心を満足し、定着したユーザーに変えることで、感情を迅速にリセットできます。

中期(1〜3ヶ月):

- Shannonテストネットの規模/安定性の証明、およびより多くのサードパーティバリデーター。即座に感じられる初の公開ゲームプレイとクリエイターツール。

長期(6ヶ月以上):

- 質の高い上場と流動性を伴うメインネット+TGE。「初のヒットゲーム/世界」を創出するエコシステム資金の展開。

実行のテンポが、勢いを永続的な価値に変換するレバーとなります。

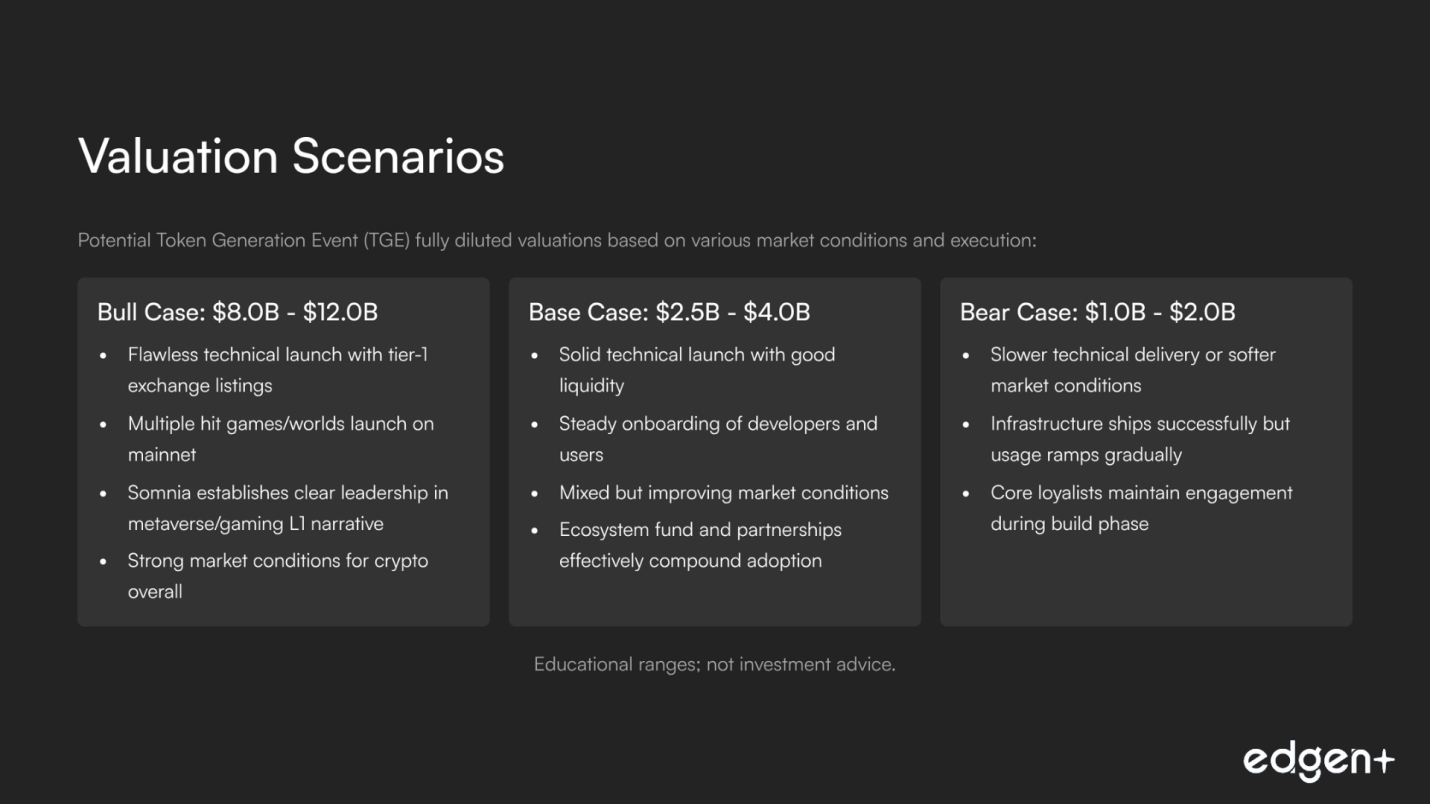

IV. 評価シナリオ分析(TGE FDV)

シナリオ | FDV (10億米ドル) | 概要 |

強気シナリオ | 8.0 – 12.0 | 完璧なローンチ + Tier-1上場;ヒットゲームが稼働;Somniaがメタバース/ゲームL1ストーリーをリード。 |

基本シナリオ | 2.5 – 4.0 | 堅実な技術 + 混合市場での安定したオンボーディング;ファンド + パートナーが採用を加速。 |

弱気シナリオ | 1.0 – 2.0 | 配信の遅延または市場の軟化;インフラは出荷されるが、主要なロイヤルユーザーと共に利用が徐々に増加。 |

教育目的の範囲です。投資アドバイスではありません。

競合環境(TGE時点/付近のトークン視点)

ネットワーク | トークン | 焦点 | Somniaに対する基本ケースのポジション |

Ronin | ゲーム向けEVM L1(パブリッシャー主導) | 強力な実績あるパイプライン。Somniaはより広範なオープンワールドの範囲と生のスループット目標で競合します。 | |

Immutable zkEVM | $IMX | ゲーム向けL2、マーケットプレイスの強み | 深いスタジオとインフラ。SomniaはL1のパフォーマンス + EVM + 手数料バーンで対抗します。 |

Solana | 高スループットL1(並列実行) | 成熟したエコシステム。SomniaはホットステートのパフォーマンスストーリーとEVMの馴染みやすさで差別化します。 | |

Aptos | 高スループットL1(Move) | 強力な技術。SomniaはEVM + 特化されたメタバースの物語を通じて開発者の摩擦を低減します。 |

最終的な見解

Somniaは非常に有望に見えます。リアルタイムのオンチェーン世界を動かす現実的な計画を持つ、特化されたEVM互換L1です。多額のエコシステム資金、優良なパートナー、そしてホットステートワークロードに焦点を当てた設計により、ビジョンを使用へと転換する態勢が整っています。上限帯の評価額への道は明確ですが厳格です。それは、極めて明確なローンチオペレーション、目に見える初期ゲーム、スムーズなTGE、そして一貫した出荷です。

教育コンテンツであり、投資アドバイスではありません。

投資、もうひとりじゃない

Ed を無料で試そう。クレカ不要、縛りなし