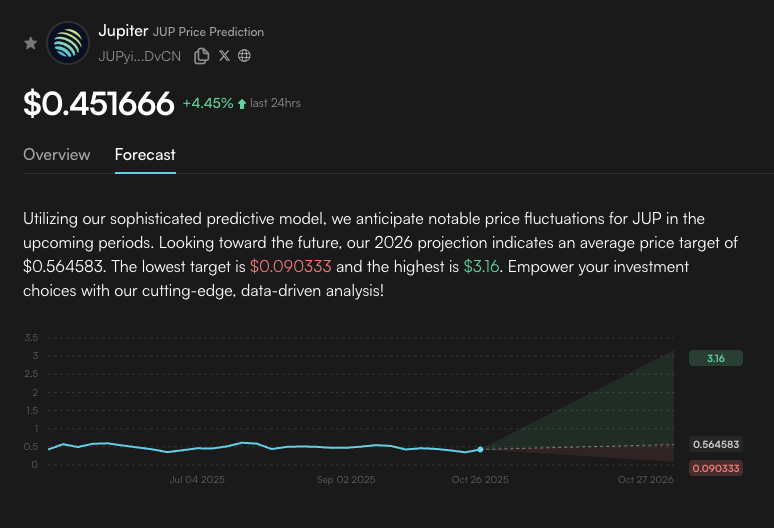

Edgen AI: Your Copilot for Smarter Crypto Trading

Edgen AI: Your Copilot for Smarter Crypto Trading

SEO Title: Navigate Crypto Markets with Edgen AI Copilot

Description: Learn how Edgen AI serves as your intelligent copilot, providing real-time data, trading signals, and portfolio insights for confident crypto investing.

Tag Keywords: Edgen AI, crypto trading, market data, trading signals, portfolio insights, AI investment co-pilot, predictive analytics, on-chain intelligence, market intelligence platform

I. The Rise of AI Companions in Crypto Investing

Crypto markets move without pause. Prices react in seconds, narratives shift in minutes, and traders face a flood of data from exchanges, blockchains, and social channels. The real challenge is knowing which information deserves attention.

Edgen was designed to solve that challenge. It functions as an intelligent companion that transforms scattered data into actionable understanding. Through real-time analytics, predictive modeling, and personalized insights, it allows investors to act with clarity instead of emotion.

Whether you manage a DeFi portfolio or trade major pairs, Edgen provides structure in a market that rarely stands still.

II. How Edgen AI Supports Every Decision

Edgen combines multiple intelligence layers into one adaptive system that learns from market movement and user behavior. It interprets on-chain activity, technical signals, and sentiment in real time to guide decisions across every type of portfolio.

Core Function | Feature Description | How It Helps Traders |

|---|---|---|

Real-Time Market Data | Collects on-chain, exchange, and sentiment data from multiple networks. | Delivers instant insights and faster reactions. |

Trading Signals | Analyzes historical patterns, RSI, MACD, and volatility relationships. | Highlights favorable entry and exit zones. |

Portfolio Insights | Tracks diversification, allocation, and risk concentration. | Improves portfolio balance and resilience. |

Predictive Alerts | Detects anomalies and potential reversals early. | Reduces exposure to sharp corrections. |

These capabilities are powered by Edgen’s Technical Signals Agent, which continuously recalibrates its models as new data flows in, maintaining accuracy across volatile markets.

III. From Noise to Clarity

Markets operate continuously. For investors, the volume of raw information is both opportunity and obstacle. Edgen filters and structures that information through a unified data engine that scans hundreds of centralized and decentralized venues.

Its machine learning models forecast short-term and medium-term movements by studying liquidity flows, network activity, and sentiment interactions. This process converts complex blockchain and exchange data into readable visuals that reveal early signals before narratives catch up.

IV. Portfolio Oversight with AI Precision

Every portfolio carries its own rhythm of risk and reward. Edgen’s 360° Report provides a complete view of holdings, asset health, and concentration levels.

Users can:

- Monitor portfolio exposure in real time.

- Compare performance against sector or market benchmarks.

- Receive AI-guided suggestions for rebalancing and diversification.

With these insights, investors transition from reaction to preparation, allowing long-term positioning instead of short-term guesswork.

V. The Strategic Edge

Edgen’s design simplifies complexity while deepening context. Investors gain:

- A unified interface that centralizes market intelligence.

- Smarter decision frameworks built on verified analytics.

- Predictive awareness of liquidity and sentiment shifts.

- Continuous portfolio diagnostics for resilience and optimization.

- Community perspective from Trading Mindshare, integrating social and behavioral signals.

Each component functions together to align analysis, execution, and adaptation in one consistent rhythm.

VI. The Future of Intelligent Investing

Crypto markets will always be volatile, but the experience of navigating them can be calm and methodical. Edgen AI brings that discipline through adaptive learning and precise forecasting.

It offers a complete environment for understanding what moves markets and how each movement affects your portfolio.

With Edgen as your copilot, you invest with awareness, structure, and purpose.

Start exploring Edgen today and experience how AI transforms information into confidence.

Your money person, finally.

Try Ed free. No credit card. No commitment.