实时AI市场洞察:每个交易者都需要的Edgen交易雷达

加密货币变化迅速。跟上步伐,否则将被甩在后面。

加密货币市场从不停歇。价格迅速上涨、暴跌并快速转向。如果没有及时准确的市场洞察,你的交易策略就变成了纯粹的投机。

时机就是一切。加密货币市场的波动比传统市场更剧烈;一次交易延迟就意味着利润的损失。成功的交易者依赖于即时且可操作的数据。

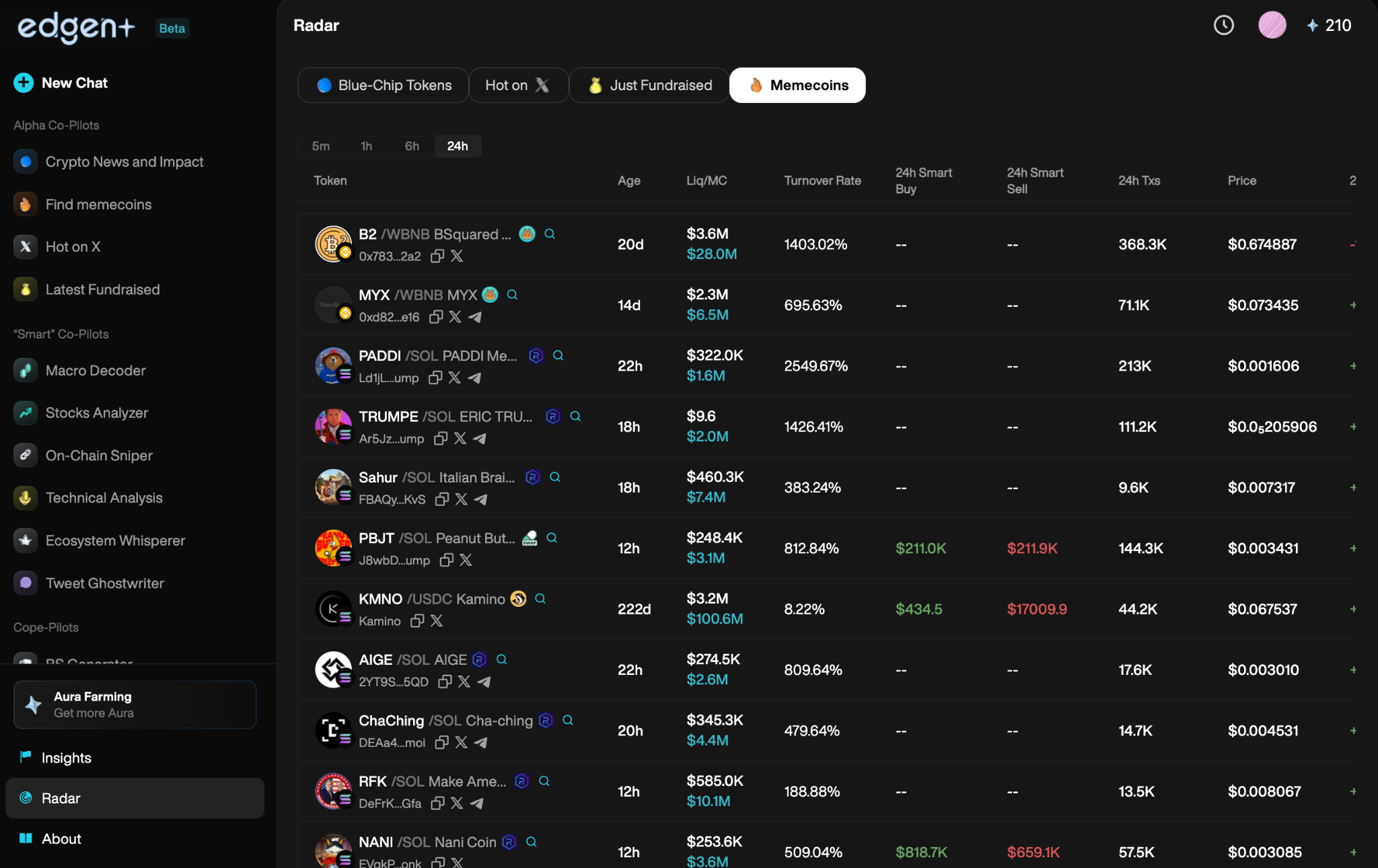

Edgen Radar提供实时人工智能分析,融合链上洞察、社交情绪追踪和强大的阿尔法信号,所有内容都在一个平台上清晰展示。

无需猜测。无需犹豫。实时交易清晰度。

实时市场洞察:为什么它们很重要

实时信号上的加密货币交易现在

图表已无法完整反映实际情况。市场驱动因素发生了变化:

- 社交媒体炒作

- 鲸钱包交易

- 链上交易

实时洞察可让您立即看到市场驱动因素,从而在市场状况发生变化之前进行有利可图的交易。

传统投资者依赖过去的趋势,而加密货币则奖励那些能清晰解读当前情况的人。

“盲目的交易意味着亏损”

延迟的数据?你会错过最佳的入场和出场点。

过时的信号?你会落后于市场。

陷入虚假炒作?你将付出代价。

实时洞察有助于做出更明智的决策,更快地反应,并保持持续的盈利。

如何让Edge AI雷达为交易者提供终极优势

Edgen Radar将先进的AI、详细的链上分析和精准的社会情绪分析融合成一个强大的实时交易工具。正如密歇根大学经济学期刊所指出的, AI is transforming financial markets by enhancing speed, efficiency, and precision in trading and market prediction请将以下英文翻译成简体中文。保持结构和技术术语准确。避免过度翻译。LSA Technology Services

主要特点:

- 基于人工智能的市场分析:可即时扫描大规模数据集,识别关键趋势,并提供可操作的洞察。

- 实时链上追踪:对巨鲸钱包活动、流动性变化和关键代币流动的即时警报。

- 社交情绪扫描器:实时监测影响力人物、KOL和正在升温的币种。

- 阿尔法信号检测:AI精选的交易信号,在价格飙升前发现被低估的资产。

- 即时通知:在重大市场波动发生前的实时警报。

Alpha信号:以内部人士视角看市场

定义Alpha信号

Alpha信号为盈利交易提供了早期指标,在大众意识到之前清晰地显示出市场变化。

Edge AI 的 Alpha 优势:

- 过滤市场噪音,锁定盈利机会。

- 及早捕捉上升的社会热潮。

- 快速检测鲸鱼聚集和分布信号。

停止猜测。使用Alpha信号,自信交易。

为什么实时洞察是必要的,而不是可选的

没有它们的交易风险:

- 因入场延迟而完全错过有利可图的交易。

- 成为被操控市场炒作的受害者。

- 不断做出反应而非主动交易,导致错失盈利机会。

Edgen AI 明显的优势:

- 市场预判:在价格反映市场波动之前,了解市场动向。

- 精准执行:AI驱动的洞察带来自信决策。

- 早期优势:在主流交易者反应之前捕捉大幅价格波动。

实时数据等于专业级交易。没有它,成功将遥不可及。

人工智能与实时数据:交易革命已经到来

市场每天都在变得更智能、更灵活、更具竞争力。成功的交易员利用人工智能驱动的工具来保持他们的优势。

Edgen Radar 明确地展现了这一边缘。

Edgen Radar 对交易未来愿景

未来交易将超越传统指标和静态图表。人工智能驱动的分析、实时数据追踪和自动化执行将定义交易。

清晰地看到:

- 每一次重大的市场波动都会被人工智能立即识别。

- 即将上涨的代币被提前发现。

- 基于社交情绪和区块链活动的实时通知。

Edgen AI打造的就是这个未来,使用Edgen Radar的交易者将成为其中的一部分。

贸易。迅速行动。持续获胜。

提升您的交易水平。试用Edgen Radar 今天。

投资这事,终于不用一个人了

免费试用 Edgen。不用信用卡,不绑约