Đánh giá về Moonbirds dưới Orange Cap Games, tập trung vào chiến lược, thực thi, quan hệ đối tác và các kịch bản định giá. Bạn có thể tìm thấy hướng dẫn về Moonbirds tại đây:

Tóm tắt

- OCG đang áp dụng một chiến lược hồi sinh IP đã được chứng minh, chuyển từ cộng đồng sang thương hiệu đến sản phẩm, đã biến sự chú ý thành hoạt động và nhu cầu.

- Sự liên kết của các nhà đầu tư ưu tú, tiện ích hữu hình như Kaito AI social-to-earn, avatar Otherside và các đợt airdrop từ đối tác mang lại cho Moonbirds động lực mạnh mẽ với những con đường rõ ràng để đạt được giá trị bền vững.

Moonbirds là gì

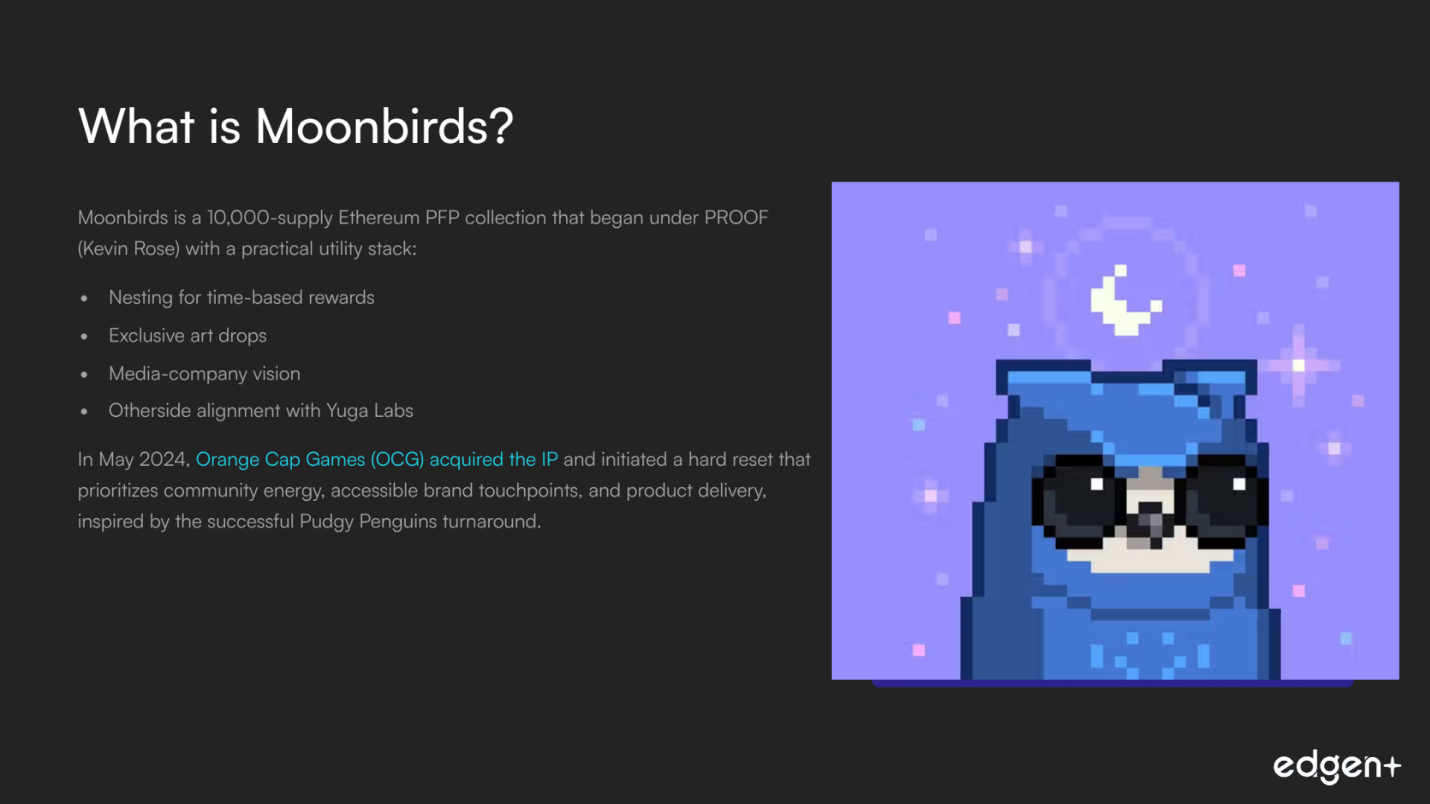

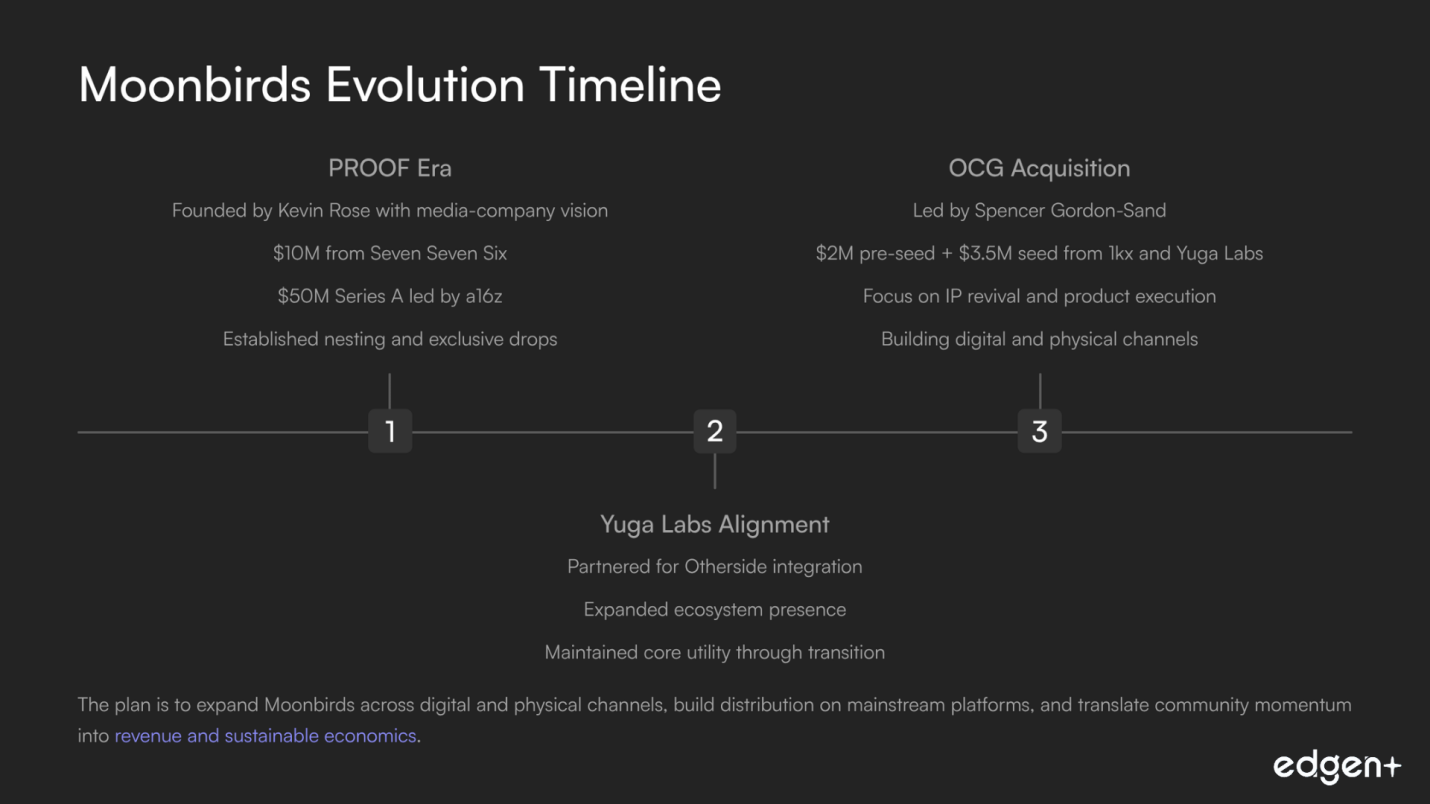

Moonbirds là bộ sưu tập Ethereum PFP có số lượng 10.000, ban đầu được phát triển bởi PROOF (Kevin Rose) với một bộ tiện ích thực tế: Nesting để nhận phần thưởng dựa trên thời gian, các đợt phát hành tác phẩm nghệ thuật độc quyền và tầm nhìn về một công ty truyền thông. Sau đó, nó liên kết với Yuga Labs cho Otherside. Vào tháng 5 năm 2025, Orange Cap Games (OCG) đã mua lại IP này và khởi xướng một quá trình tái khởi động mạnh mẽ, ưu tiên năng lượng cộng đồng, các điểm tiếp cận thương hiệu dễ dàng và phân phối sản phẩm, lấy cảm hứng từ sự thành công của Pudgy Penguins.

Dưới sự lãnh đạo của Spencer Gordon-Sand, OCG mang đến uy tín về tiền mã hóa bản địa và kinh nghiệm thực thi sản phẩm, bao gồm trò chơi thẻ giao dịch Vibes. Kế hoạch là mở rộng Moonbirds trên các kênh kỹ thuật số và vật lý, xây dựng phân phối trên các nền tảng chính thống, và chuyển động lực cộng đồng thành doanh thu và kinh tế bền vững. Các đối tác như Kaito AI (social-to-earn) và quyền truy cập airdrop với các dự án như Monad và Towns bổ sung giá trị tức thì cho người nắm giữ trong khi đội ngũ xây dựng một nền tảng IP và trò chơi rộng lớn hơn.

Với đội ngũ lãnh đạo mới, những người ủng hộ có tín hiệu cao và mô hình hoạt động rõ ràng, Moonbirds được định vị để phát triển từ một bộ sưu tập NFT nổi tiếng thành một thương hiệu bền vững, dựa trên tiện ích.

I. Phân tích nền tảng và chiến lược

1. Tầm nhìn và sự liên kết của nhà đầu tư

Chiến lược đã phát triển qua ba thời kỳ, từ PROOF đến Yuga đến OCG, hướng tới một sứ mệnh tập trung: hồi sinh IP, kích hoạt cộng đồng và ra mắt sản phẩm.

Sự hỗ trợ của nhà đầu tư phản ánh quỹ đạo này, từ việc a16z tài trợ cho luận điểm truyền thông của PROOF đến 1kx và Yuga Labs đồng dẫn dắt vòng hạt giống của OCG, liên kết vốn với kế hoạch chuyển đổi.

2. Đội ngũ và năng lực thực thi xuất sắc

- Thực thi do nhà điều hành đứng đầu từ CEO Spencer Gordon-Sand, một nhà đầu tư NFT sớm và lãnh đạo cộng đồng nổi bật, kết hợp với kinh nghiệm sản phẩm thực tế.

- Vibes TCG thể hiện khả năng thực thi vật lý và kỹ thuật số, cộng với một lộ trình vận hành để sản xuất và mở rộng quy mô thông qua các năng lực có trụ sở tại châu Á.

3. Sức mạnh vốn và sự chứng thực

Các đợt gây quỹ trước đây bao gồm 10 triệu đô la từ Seven Seven Six và 50 triệu đô la Series A do a16z dẫn đầu với sự tham gia của các bên hàng đầu.

Hiện nay, OCG được hỗ trợ bởi 3,5 triệu đô la hạt giống từ 1kx và Yuga Labs, sau 2 triệu đô la pre-seed, và được bổ sung bởi doanh thu từ Vibes. Điều này tạo ra một nguồn tài chính lành mạnh, tập trung vào thực thi.

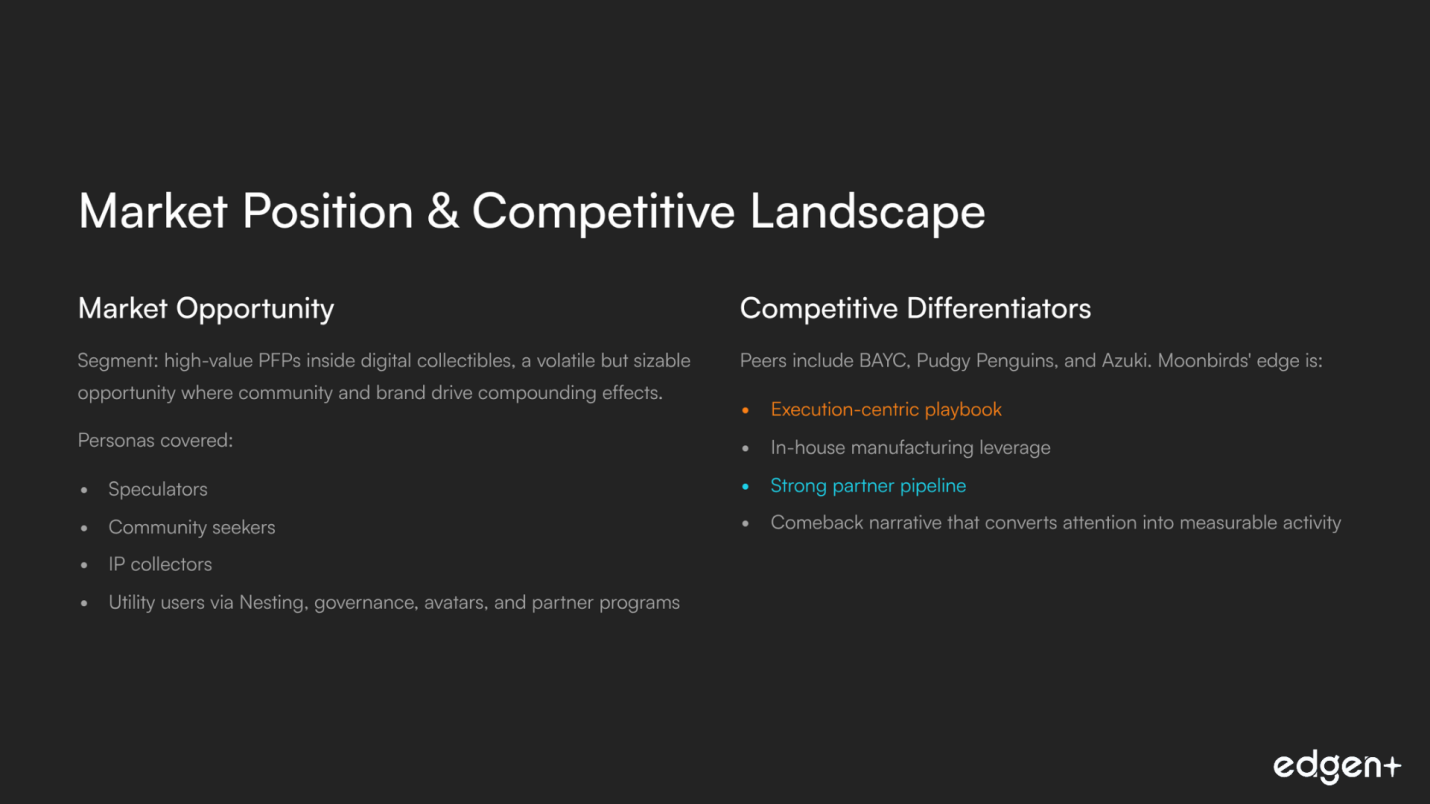

4. Cơ hội thị trường và sự phù hợp

- Phân khúc: Các PFP giá trị cao trong bộ sưu tập kỹ thuật số, một cơ hội biến động nhưng đáng kể, nơi cộng đồng và thương hiệu thúc đẩy hiệu ứng kép.

- Các nhân vật được bao phủ: Các nhà đầu cơ, những người tìm kiếm cộng đồng, nhà sưu tập IP và người dùng tiện ích thông qua Nesting, quản trị, avatar và các chương trình đối tác.

5. Cảnh quan cạnh tranh & Điểm khác biệt

Các đối thủ bao gồm BAYC, Pudgy Penguins và Azuki. Lợi thế của Moonbirds là một chiến lược tập trung vào thực thi, đòn bẩy sản xuất nội bộ, một đường ống đối tác mạnh mẽ và một câu chuyện trở lại biến sự chú ý thành hoạt động có thể đo lường được.

Đánh giá nền tảng: Sức mạnh nền tảng đáng kể với các nhà đầu tư liên kết, các nhà điều hành thực tế và lộ trình do sản phẩm dẫn dắt.

II. Hệ sinh thái trước khi ra mắt & Chiến lược tiếp cận thị trường

1. Động lực cộng đồng & câu chuyện

Việc OCG mua lại đã xúc tác một sự thay đổi trong câu chuyện. Giao tiếp lãnh đạo nhất quán và các thông báo tiện ích hữu hình, chẳng hạn như Kaito AI, đã tái tạo năng lượng cho hoạt động xã hội và trên chuỗi. Các tín hiệu cho thấy chất lượng tương tác được cải thiện và một cơ sở người nắm giữ phản ứng nhanh.

2. Dấu chân trên chuỗi

Một cơ sở người nắm giữ đáng kể, kiên cường cung cấp một bệ phóng vững chắc cho các sản phẩm và cơ chế token. Hành vi nắm giữ dài hạn, hoạt động thứ cấp được đổi mới và các bộ sưu tập phụ hỗ trợ quyền truy cập trong khi vẫn duy trì trạng thái thương hiệu.

3. Quan hệ đối tác bổ sung tiện ích

- Kaito AI social-to-earn chuyển đổi nội dung thành phần thưởng, biến việc nắm giữ thụ động thành sự tham gia và khám phá tích cực.

- Các tuyến airdrop như Monad và Towns thưởng cho người nắm giữ và thu hút các đối tác phù hợp tìm kiếm phân phối chất lượng; avatar 3D sẵn sàng cho Otherside mở rộng tiện ích đa hệ sinh thái.

4. Tokenomics & Tích lũy giá trị (Hiện tại)

- Nesting tạo ra các phần thưởng dựa trên thời gian hỗ trợ hành vi nắm giữ và chuẩn bị hệ thống cho một token $TALONS trong tương lai.

- Quản trị thông qua Lunar Society liên kết ảnh hưởng với các NFT cốt lõi và một kho bạc, củng cố sự liên kết lâu dài giữa những người tham gia và thương hiệu.

Đánh giá sự sẵn sàng GTM: Rất hứa hẹn. Các quan hệ đối tác định hướng tiện ích và kỷ luật phân phối tạo thành một nền tảng vững chắc. Sự sẵn sàng của Token TGE sẽ được hưởng lợi từ việc chuẩn bị hoạt động và pháp lý liên tục.

III. Phân tích tương lai (Chất xúc tác & Cơ hội)

Ngắn hạn (≤1 tháng)

Kaito AI kích hoạt làm tăng cường vòng lặp người sáng tạo, cải thiện khả năng khám phá và hỗ trợ sự gắn kết bền vững có thể dẫn đến giao dịch và sự quan tâm của đối tác.

Trung hạn (1–3 tháng)

Sản phẩm đầu tiên của kỷ nguyên OCG có thể củng cố các yếu tố cơ bản ngoài câu chuyện và xác nhận mô hình hoạt động.

Dài hạn (6+ tháng)

$TALONS TGE thiết lập giá công khai cho nền kinh tế rộng lớn hơn, cho phép DeFi và khả năng kết hợp, đồng thời tăng diện tích bề mặt cho các đối tác.

Quan điểm tương lai: Các cơ hội đáng kể, với nhịp độ thực hiện là đòn bẩy chính chuyển động lực thành giá trị bền vững.

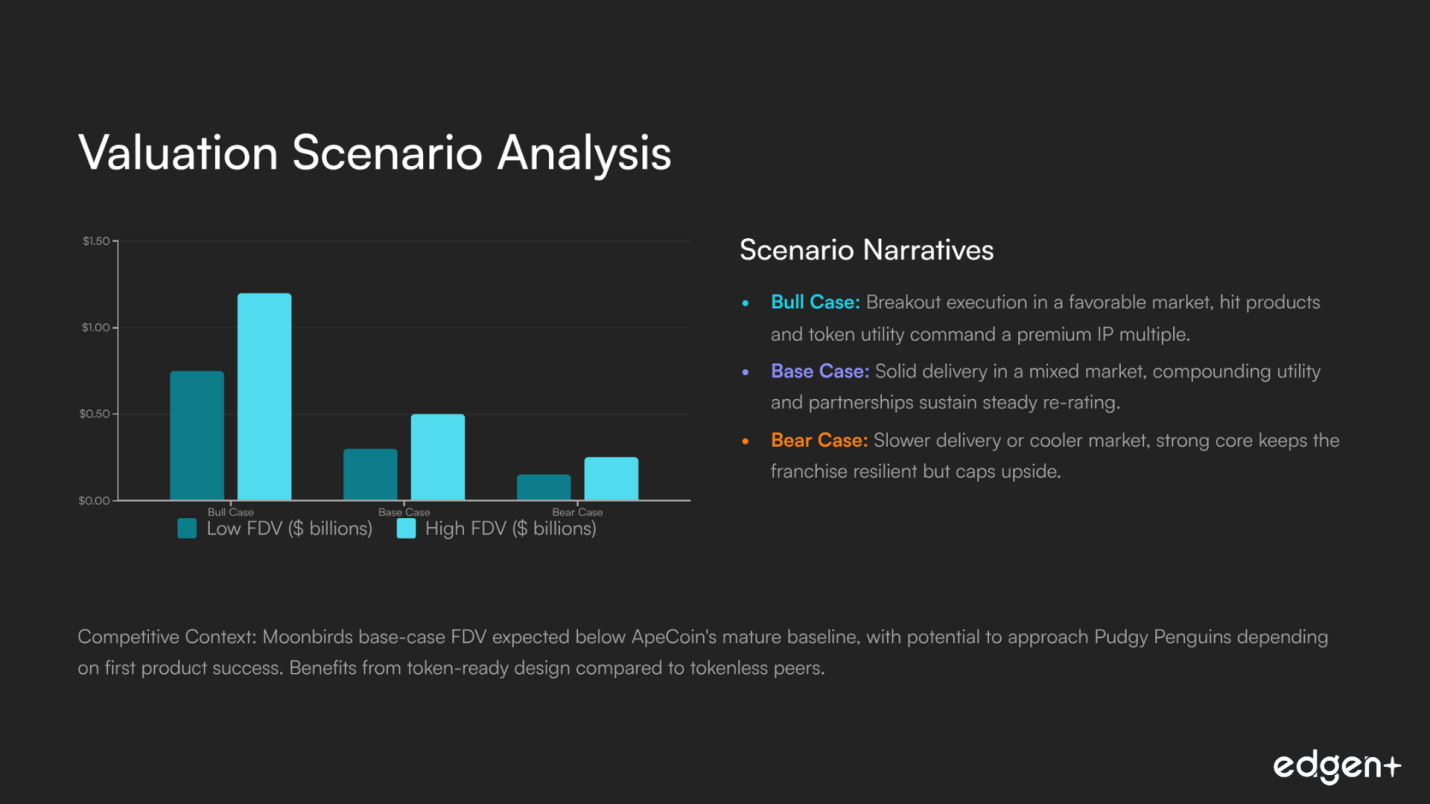

IV. Phân tích kịch bản định giá (TGE FDV)

Kịch bản | FDV (tỷ USD) | Tóm tắt câu chuyện |

Trường hợp lạc quan | 0.75 – 1.20 | Thực thi đột phá trong một thị trường thuận lợi, sản phẩm hit và tiện ích token tạo ra mức bội số IP cao cấp. |

Trường hợp cơ sở | 0.30 – 0.50 | Phân phối ổn định trong một thị trường hỗn hợp, tiện ích và quan hệ đối tác tích lũy duy trì mức định giá lại ổn định. |

Trường hợp bi quan | 0.15 – 0.25 | Phân phối chậm hơn hoặc thị trường lạnh hơn, cốt lõi mạnh mẽ giữ cho thương hiệu kiên cường nhưng giới hạn tiềm năng tăng trưởng. |

Cảnh quan đối thủ cạnh tranh (Góc độ Token tại hoặc gần TGE)

Dự án | Token | Góc độ TGE/Token | Liên kết với người nắm giữ | Phong cách phân phối | Vị trí so với Moonbirds (Trường hợp cơ sở) |

ApeCoin / Otherside | Tiện ích và quản trị hệ sinh thái | Liên kết BAYC | Airdrop cộng với niêm yết | FDV cơ sở của Moonbirds dự kiến thấp hơn đường cơ sở trưởng thành của $APE, các liên kết chiến lược với Yuga là bổ sung. | |

Pudgy Penguins | Vòng lặp IP, đồ chơi và trò chơi | Người nắm giữ Penguin | Định hướng cộng đồng | FDV cơ sở của Moonbirds gần hoặc thấp hơn $PENGU, tùy thuộc vào thành công của sản phẩm đầu tiên. | |

Azuki | (không có) | IP định hướng thương hiệu và anime | Theo bộ sưu tập | Không áp dụng | Điểm chuẩn ngang hàng không token, Moonbirds hưởng lợi từ thiết kế sẵn sàng token để tăng thêm tích lũy. |

Kết luận cuối cùng

Moonbirds cho thấy tiềm năng mạnh mẽ như một dự án hồi sinh IP được vận hành chuyên nghiệp với nguồn gốc cộng đồng đích thực và các lộ trình sản phẩm thực tế. Với sự liên kết của các nhà đầu tư ưu tú và lực kéo tiện ích sớm, dự án trông rất hứa hẹn. Tốc độ và chất lượng thực thi vẫn là chìa khóa để mở khóa các dải giá trị trên của phạm vi định giá.

Nội dung giáo dục, không phải lời khuyên tài chính.

Đầu tư, cuối cùng không phải một mình nữa.

Dùng thử Edgen miễn phí. Không cần thẻ, không ràng buộc.