机器学习在加密货币认知中的作用

人工智能如何帮助交易员在市场波动前追踪注意力并预测阿尔法收益

什么是加密领域影响力?

“注意力份额”字面意思是指在加密货币交易者和社区中,一个项目所获得的关注度份额。在加密货币市场中,关注度会推动价格波动。那些在推特话题、电报群组讨论、意见领袖提及或钱包活动方面占据主导地位的代币,通常会迅速获得动力。如果这些信号变得明显,真正的价格走势很可能已经开始或已经发生。

强势心智份额的典型指标包括:

- 推特上的持续提及

- 电报群组中的活跃对话

- 影响者经常讨论该代币

- 智能钱包的活动增加

及早识别注意力份额有助于交易者在更广泛的市场之前捕捉价格波动。Here’s a breakdown of how social sentiment can directly move crypto markets,强调为什么注意力常常是第一个真正的信号。

为什么心智份额在短期内往往表现更优

在加密货币领域,市场关注推动价格变化的速度快于基本面因素。缺乏明确用例甚至实物产品的代币,可能仅因炒作而迅速增长。同时,如果市场忽视它们或不够兴奋,具有坚实基本面的代币可能会停滞数月,甚至数年。极端的例子就是模因币(memecoins),它们在没有实际用途的情况下抢占了市场注意力。

由需求驱动的代币优先获得流动性。交易者需要流动性来从短期价格波动中获利。这一过程通常如下所述:

- 社交热潮推动即时需求。

- 社区热情强化了叙述。

- 流动性转向趋势代币。

- 零售交易者关注可见的炒作,而非基本面变化。

及早识别注意力具有优势,可在动作发生前捕捉到动作。

为什么大多数交易者会错过早期关注信号

“注意力份额”并非源自单一来源,但通常可以被密切关注加密货币市场和社区的人察觉。它同时在各种信号中形成,包括:

- 智能钱包交易

- Twitter趋势和提及

- Discord社区参与

- 影响者轮换至新代币

- 增加的智能合约部署

大多数交易者难以捕捉这些早期信号,因为它们:

- 不要密切监控智能钱包活动

- 注意市场情绪的细微变化

- 过于迟缓地认识到趋势,等到先行者已经退出后才反应过来

机器学习通过在人类观察者察觉之前识别和解释复杂模式来解决这些挑战。

如何将注意力转化为阿尔法(Alpha)——机器学习的作用

机器学习通过快速处理复杂、多维的模式来增强交易决策。在加密货币交易中,机器学习特别擅长于:

- 检测早期智能钱包入账

- 识别社交提及中的快速增长

- 区分真实叙述与表面炒作

- 根据历史表现对新兴趋势进行评分

- 预测初始关注与后续价格波动之间的时间关系

Edgen AI利用机器学习来实现这些功能,将市场关注转化为可操作的阿尔法收益。

如何让EdgeN使注意力资源对交易者更具可操作性

Edgen帮助零售交易者复制通常只为资金雄厚的投资者保留的策略。它持续跟踪多个平台、区块链和钱包中的加密货币关注度,将实时数据转化为可交易的信号。

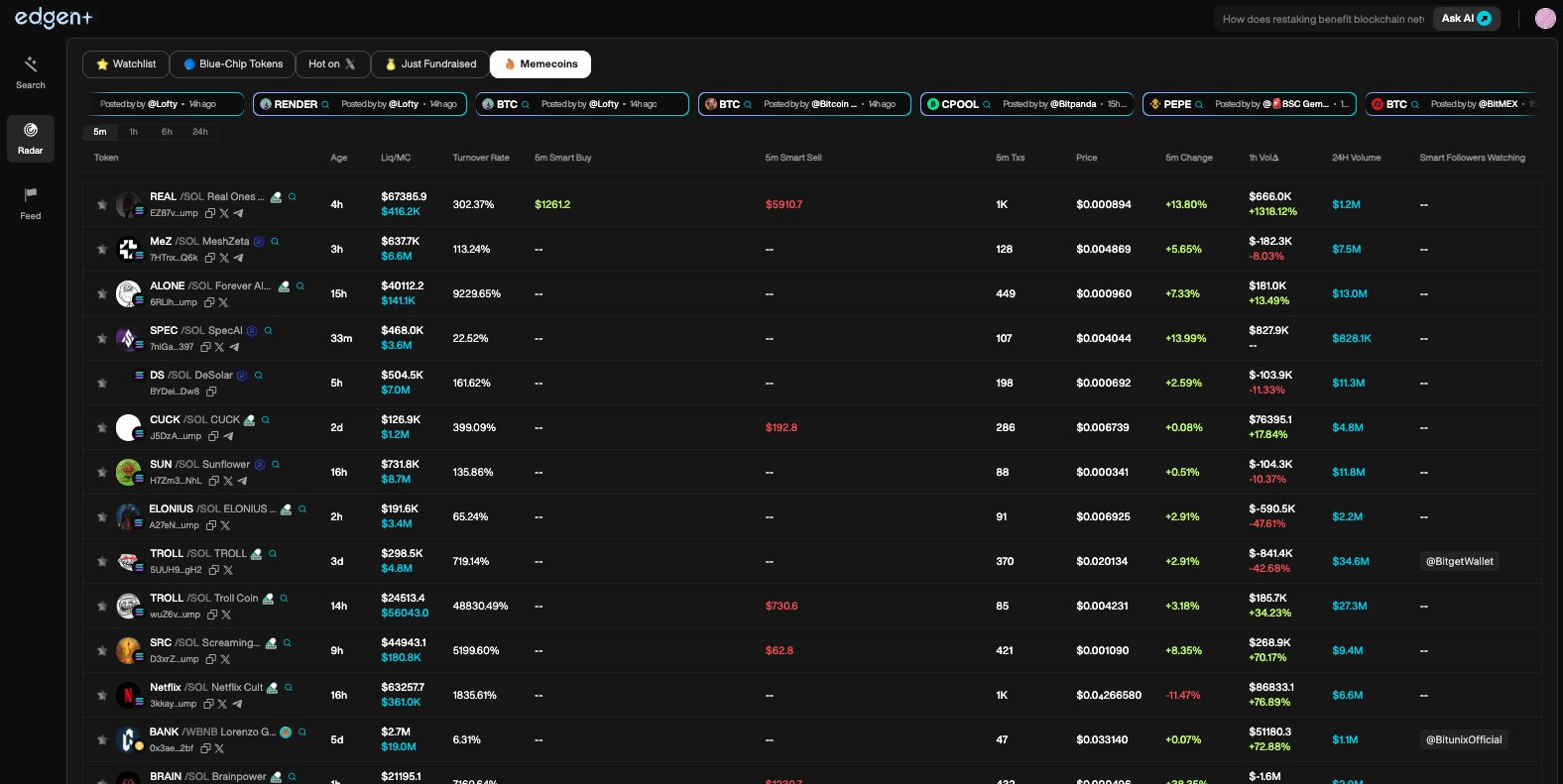

边缘雷达:实时注意力追踪

Edgen Radar监视器:

- 吸引大量智能钱包流量的代币

- 项目刚刚通过提高流动性完成筹款

- 与代币相关的社交对话的传播和速度

雷达持续运行,在价格做出反应之前提供早期信号。

AI对注意力与价格动态的预测

Edge的AI模型通过以下方式分析注意力模式:

- 社交提及的速度和加速度

- 在线社区讨论的增长率

- 每个叙述背后智能钱包活动的强度

- 历史模式及类似趋势的持续时间

每个代币都会获得一个预测评分,明确表明其趋势是否会延续、反转或失败。这种预测方法有助于交易者避免追逐过时的叙事。

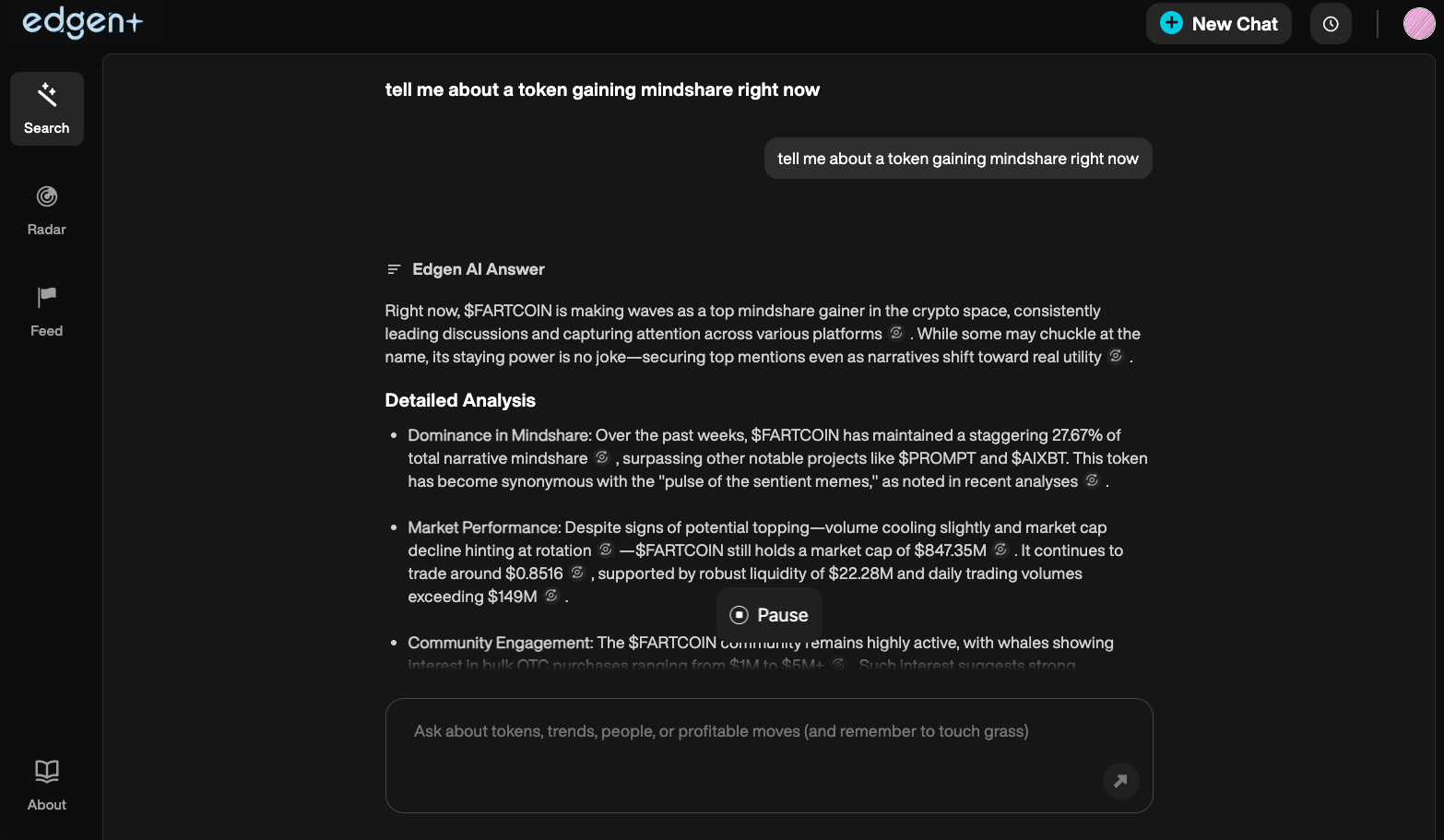

边缘搜索:无干扰的即时研究

当交易者遇到新代币时,Edgen Search提供即时上下文:

- 代币概述

- 社交媒体提及的近期增长或下降

- 实时钱包收支

- 有影响力账号的提及

- 链上智能合约活动

这消除了花费数小时从多个来源中筛选零散信息的时间。

集成诈骗检测过滤器

注意力驱动的交易经常被操控。Edgen 在交易者成为受害者之前,通过向用户发出以下警告来识别危险信号:

- 智能钱包在社交热潮高峰期进行销售

- 重复的促销复制粘贴行为

- 流动性池的突然移除

- 从已知的诈骗中复用的智能合约

这种主动的方法能区分真正的关注与被操控的炒作。

高性能智能钱包的早期追踪

Edgen监控持续盈利的钱包集群。当这些钱包悄悄开始转向新代币时,Radar会提前识别出这种活动,早于社交情绪的变化。

这种时间优势使交易者能够在趋势形成时入市,而不是在趋势达到顶峰之后。

边缘洞察:成功交易员的已验证阿尔法

Edgen Insights 从有验证交易记录的交易者那里提供可操作的内容。每条贡献都明确地:

- 按时间戳准确记录

- 与实际绩效对比跟踪

- 根据历史成功率排名

交易者从具有经证实市场远见的贡献者那里获得可靠的阿尔法。

光环:通过实际业绩建立交易商声誉

Aura 是 Edgen 的声誉系统,用于奖励交易员在持续准确性以及早期趋势识别方面的表现。用户可通过以下方式获得 Aura:

- 分享有价值的市场洞察

- 在主流认可之前识别趋势

- 向Edgen的预测模型贡献高质量的数据

- 在他们的判罚中保持一致且可验证的准确性

Aura 作为一种信任信号,证明交易者发现可操作阿尔法的能力。

理解“心智份额循环”:从话题到突破

在加密货币领域,注意力才是真正的阿尔法生成器。它决定了交易量,推动价格波动,并在早期被发现时创造盈利机会。

Edgen 利用机器学习来实现:

- 持续的实时新兴关注度监测

- 基于注意力转移预测价格走势的预测分析

- 在主流采用之前有效交易的全面工具包

交易者不再需要追逐既有的趋势。他们只需在市场反应之前识别出正在引起关注的代币。

现在想追踪市场关注点吗?

从……开始Edgen Radar您的专用实时仪表板,用于追踪热门代币、智能钱包流动情况和可操作的市场信号。

在价格飙升前识别关注点。智慧地争夺市场份额,摆脱市场噪音。

投资这事,终于不用一个人了

免费试用 Edgen。不用信用卡,不绑约