Edgen Pro与专家计划上线:立即提升你的交易水平

Edgen

· Mar 31 2026

这每天都在发生:你手里拿着珍珠奶茶,看着市场,试图决定你的下一笔交易。你看到到处都在谈论加密货币、图表和利润。你的屏幕充斥着噪音,却毫无盈利。你需要迅速获得清晰的判断。

我们理解您的困扰。并且我们已经解决了。

Edgen Pro 和 Expert订阅计划已正式上线。它们是您进行更智能、更快交易的通行证。

交易变得更简单:两种强大计划 ✨

让我们保持简单。Edgen 提供两种订阅计划:

Edgen Pro(9.99美元/月)

如果你已准备好更聪明地交易:

- 🔎每月200次市场搜索:快速找到您需要的内容。停止浪费时间。

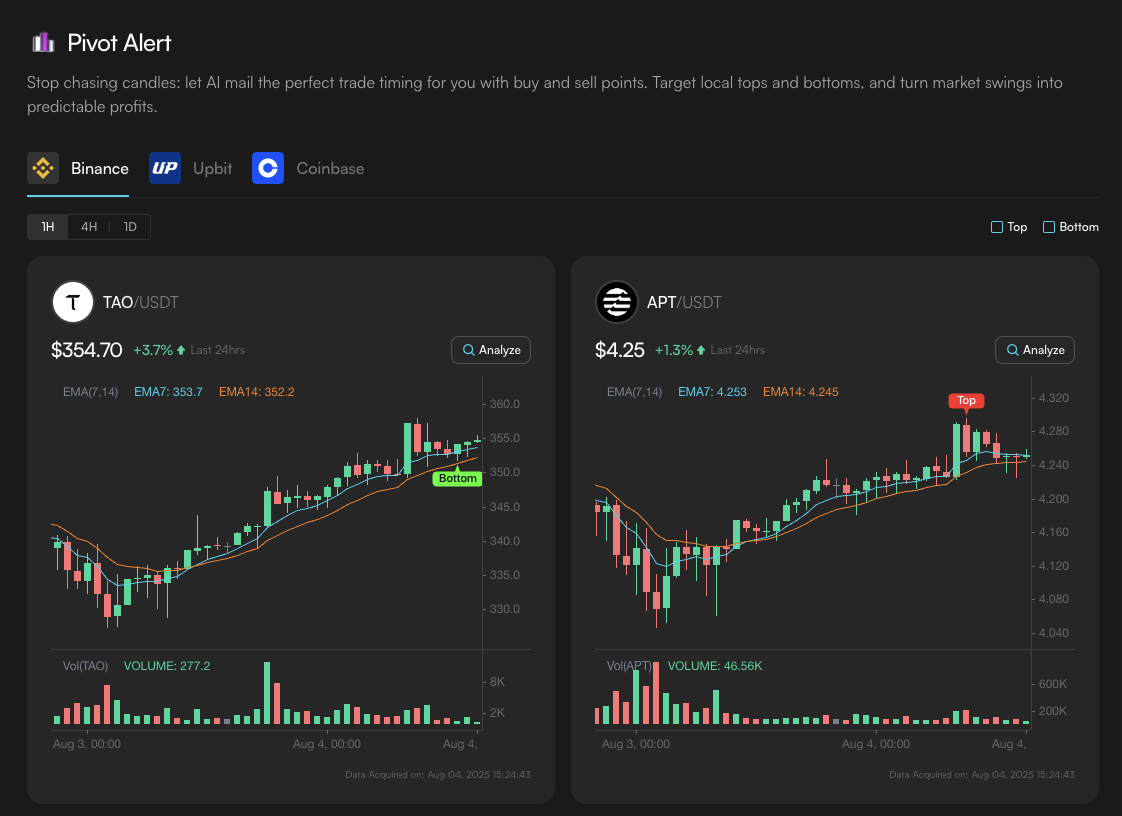

- 📈无限透视警报与技术信号代理:自信交易,即使他人恐慌。

- 💎1000 灵气增益(一次性)+ 从在Edgen上签到获得的10个每日灵 aura 奖励:强势开局,登录即可轻松提升社区等级。轻松灵活。

是的,Pro 很不错。但 Expert?Expert 是个怪物。

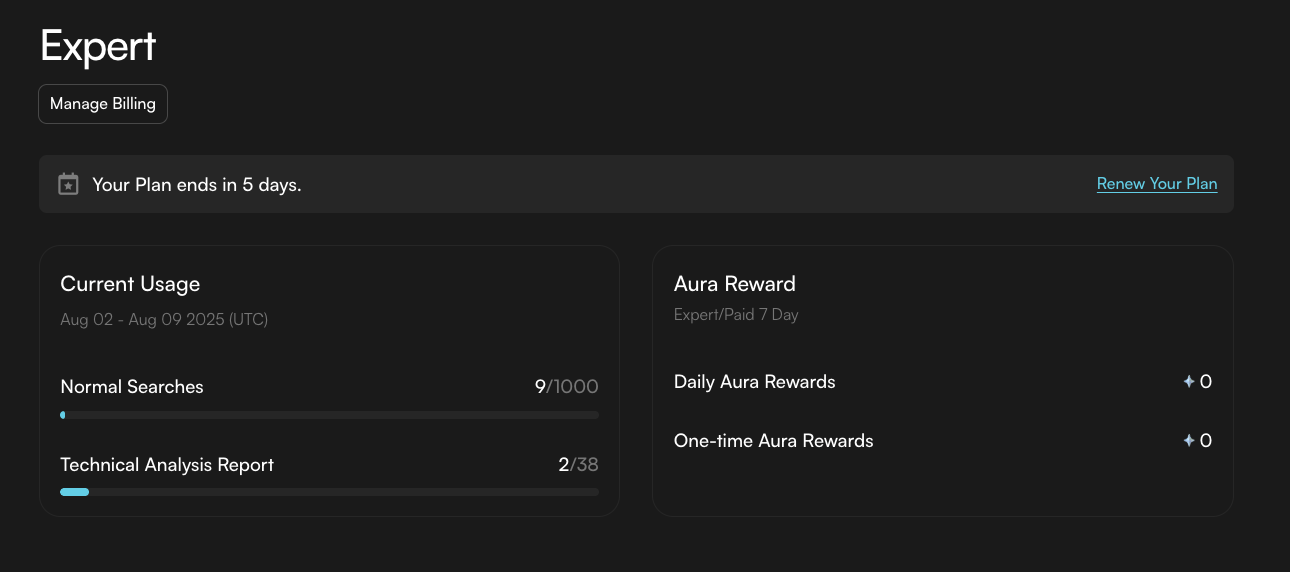

Edgen 专家版 ($17.99/月)

为真正重视盈利和信誉的交易者而设计:

- 🚀1000 次/月的市场搜索:本质上u无限潜力,即时洞察。

- ⚡️实时技术分析:立即获得市场清晰认知,因为等待属于失败者。

- 🧠所有专业代理 + 交易影响力:了解各交易所顶级投资者所知道的,在其他人之前。

- 🌟5000 灵气增幅(一次性)+ 30 日常灵气奖励:庞大的灵能采集能力。更多的灵能 = 更大的可信度 = 更多的阿尔法。

简而言之,专家意味着你已经不再玩闹了。

你的交易值得更好。试用 1 美元 🪙

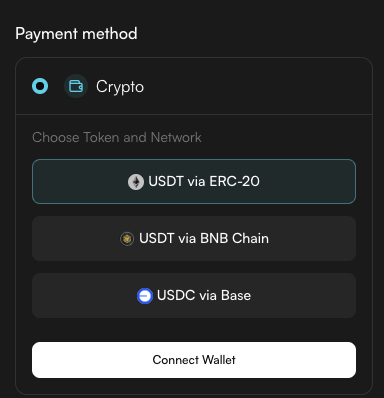

仍然不确定?让我们来简单一点。试试看Edgen Pro 或 Expert 仅售 1 美元没错,只要一美元。可使用法币或加密货币支付。

想一想:1美元即可立即开始更聪明地交易。1美元获得即时的清晰认知、增强的直觉和更明智的决策。如果这还不是你今天做出的最简单决定,那你可能读错了文章。

准备升级了吗? Click here and start your subscription now.

交易现在变得更简单、更智能,也更加盈利。欢迎进入您的新交易现实:只涨不跌。

(认真地说,点击这个链接。将来的你会感谢现在的自己。)

推荐阅读

投资这事,终于不用一个人了

免费试用 Edgen。不用信用卡,不绑约