Comment trader les jetons alimentés par l'IA et les memecoins : un guide pour investir plus intelligemment en crypto

L'avenir du trading crypto est l'IA : découvrez Edgen AI

Le trading de cryptomonnaies évolue à une vitesse fulgurante. Clignez des yeux, et vous manquerez la prochaine grande tendance. Récemment, deux tendances ont dominé les titres de presse : les jetons alimentés par l'intelligence artificielle etmemecoinsle commerce. Qu'est-ce que ce sont exactement, et pourquoi cela devrait-vous importer ?

Les jetons alimentés par l'intelligence artificielle utilisent l'intelligence artificielle pour prédire les mouvements du marché, repérer les tendances et exécuter des opérations avec une précision millimétrique.Les mémo-coïns, sont des cryptomonnaies ludiques inspirées des canulars d'internet et de la culture en ligne. Elles commencent souvent comme des blagues mais peuvent parfois se transformer en investissements sérieux (regarde-toi, Dogecoin).

Avec des plateformes commeEdgen AI, les traders obtiennent une analyse du marché en temps réel, suivant tout, des sentiments sociaux aux données sur la chaîne. Si vous êtes débutant, accrochez-vous : ce guide explique exactement ce que sont les jetons etmémecoinle commerce, comment il fonctionne, et comment investir intelligemment et en toute sécurité.

Qu'est-ce que le trading de jetons alimenté par l'intelligence artificielle ?

En bref, le trading alimenté par l'intelligence artificielle utilise des algorithmes avancés pour analyser les échanges de cryptomonnaies plus intelligemment et plus rapidement. Il est guidé par des données, des modèles prédictifs et l'apprentissage automatique.

Pourquoi l'IA est-elle importante dans le trading de cryptomonnaies :

- Puissance de traitement des données :L'IA analyse instantanément des montagnes de données du marché.

- Précision prédictive :Les variations des prix à l'actif avant la meute.

- Le commerce dépourvu d'émotion :Élimine les biais humains et les erreurs causées par la panique.

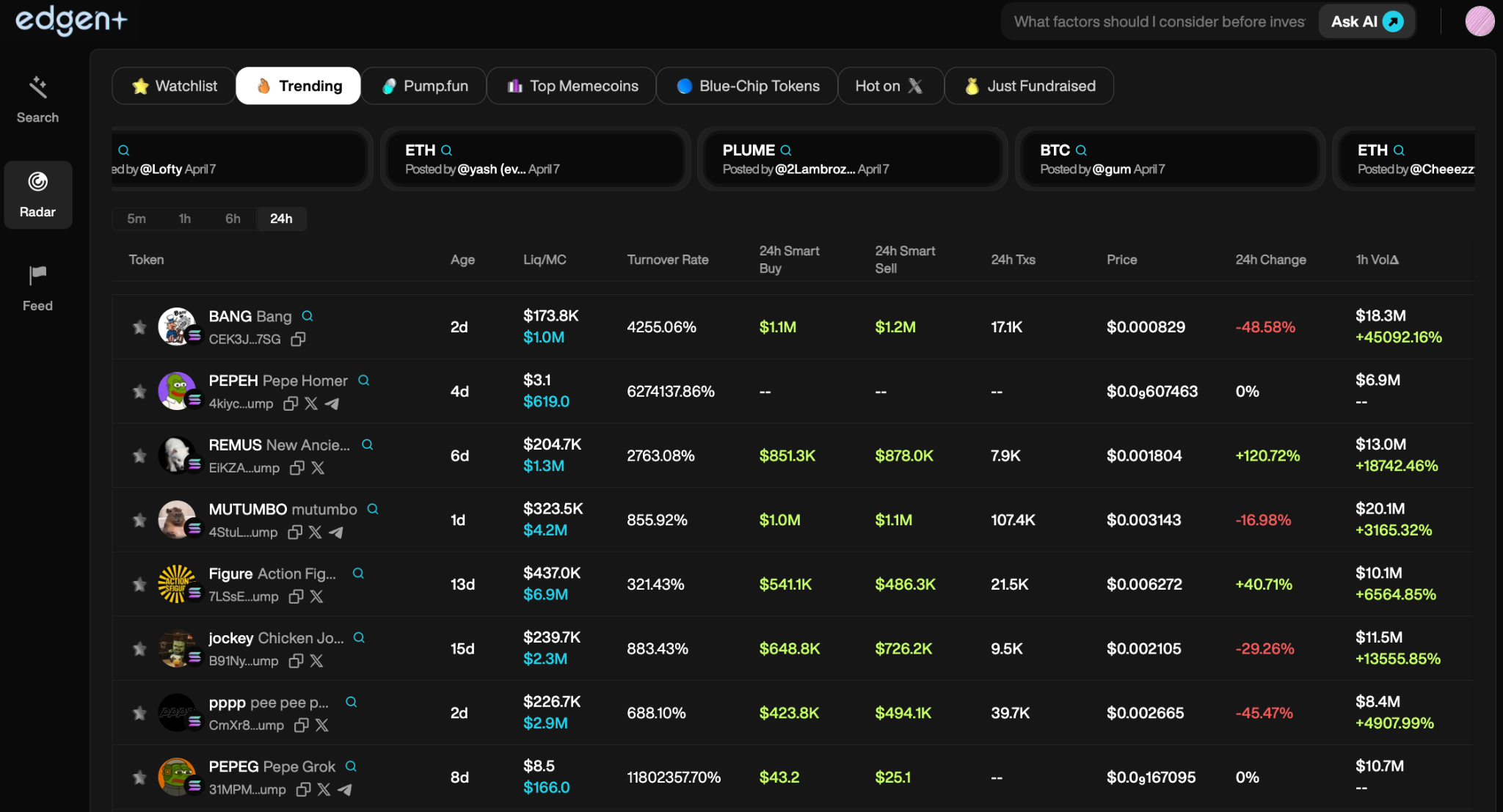

- Suivi de l'opinion sociale :Détecte les excès précocement en utilisant des outils comme Edgen Radar

Échanger des cryptomonnaies sans IA ? C’est mignon… mais obsolète.

Les mémo-coïnsExpliqué : Plus que des blagues ?

Les mémo-coïnssont des cryptomonnaies qui capturent la culture et l'humour d'internet, transformant la popularité virale en valeur crypto. Nées à partir de récits, elles prospèrent grâce à l'excitation de la communauté et à la dynamique virale.

ConnuLes mémo-coïns:

- Dogecoin (DOGE) :Veuillez traduire la phrase suivante en français. Conservez la structure et les termes techniques précis. Évitez la surtraduction.

Originalmémecoinné d'une blague, maintenant un acteur sérieux. - Shiba Inu (SHIB) :Rival populaire de Dogecoin, grande communauté, forte volatilité.

- Pepe Coin (PEPE) :S'inspirant du célèbre motif de Pepe le Grenouille, a rapidement acquis un statut de culte.

Pourquoi investir dansLes mémoïdes?

- Croissance guidée par la communauté :Les mémo-coïnsexplose quand l'hype rencontre le FOMO.

- Grand potentiel de récompense :Les gains (et les pertes) rapides sont fréquents.

- Divertissements culturels :Investir dansmemecoinssignifie souvent rejoindre une communauté dynamique.

Maismemecoinsviennum avec une mention de risque élevé : ils sont volatils et imprévisibles. UtiliserEdgen Radar, les traders peuvent suivre les tendances sociales en temps réel, offrant un avantage pour naviguer dans lemémecoinmontagnes russes

Comment l'intelligence artificielle révolutionne le trading de cryptomonnaies

L'IA n'est pas seulement un luxe ; c'est la nouvelle norme dans l'investissement moderne. Du pronostic du marché à l'exécution automatisée, l'IA aide les traders à opérer avec précision. Si vous souhaitez explorer comment ces technologies transforment la finance traditionnelle, consultez le CFA Institute’s report on AI in asset management.

1. Analyse prédictive du marché

L'IA analyse les tendances et prédit les mouvements du marché plus rapidement que les traders humains ne peuvent réagir.

2. Bots de trading automatisé

Les bots d'IA exécutent des stratégies 24/7, maximisant l'efficacité de votre trading sans interruption.

3. Sentiment en temps réel ("Pumpamentals)

Edgen AIsuivi des comptes intelligents, des KOL et de la hype sociale. Vous repérerez la prochaine tendance virale.mémecointôt, pas tard.

4. Suppression de l'émotion

Les humainsla panique,L'IA ne le fait pas. Les décisions de trading sont fondées sur les données, disciplinées et fiables.

5. Sécurité renforcée

L'IA détecte plus rapidement la fraude, les activités suspectes et les escroqueries, protégeant ainsi votre crypto-monnaie.

Guide étape par étape : Investir en jetons etLes mémo-coïnsAvec l'intelligence artificielle

Prêt à trader plus intelligemment ? Voici votre manuel :

Étape 1 : Rechercher comme un professionnel

UtilisezEdgen Searchpour explorer en profondeur l'histoire des jetons, les cas d'utilisation, les mouvements du marché et le buzz social.

Étape 2 : Sélectionner un échange de confiance

Choisissez un DEX réputé (Uniswap,Pancakeswapou CEX (Binance, Coinbase, Kraken) après s'être connecté de manière transparente àEdgen Radar.

Étape 3 : Achetez votre cryptomonnaie

Déposez des fonds, échangez vos jetons et stockez-les en toute sécurité.

Étape 4 : Surveiller les marchés avec l'intelligence artificielle

Utiliser l'avantageEdgen Radarpour des signaux de marché en temps réel, en suivant à la fois les activités sur la chaîne et les tendances sociales.

Étape 5 : Gérer les risques de manière prudente

Investissez de manière responsable. Les deux jetons etmemecoinssont à risque élevé,haute récompenseJoue. Ne YOLO pas ton épargne entière.

Risques et réalités : Ce que tout trader devrait savoir

Excitant ? Absolument. Sans risque ? Absolument pas. Voici ce à quoi faire attention :

1. Volatilité extrême

Les marchés cryptographiques sont imprévisibles, et même l'intelligence artificielle ne peut pas attraper chaque seule surprise.

2. Les arnaques de type Rug Pull et les escroqueries

Vérifiez toujours les projets avant d'investir. Utilisez Edgen Searchpour filtrer les fraudes.

3. L'IA n'est pas de la magie

L'IA repose sur des données historiques, qui ne prédisent pas toujours parfaitement les mouvements futurs à 100 %.

4. Risques réglementaires

Les actions du gouvernement peuvent modifier rapidement le paysage des cryptomonnaies en une seule nuit.

FAQ : Ce que les débutants posent le plus souvent

1.Le trading de jetons avec l'intelligence artificielle est-il un bon investissement ?

Potentiellement, oui. Il offre des analyses basées sur les données et une exécution rapide des transactions, mais il comporte toujours un risque de marché. Faites toujours une recherche approfondie.

2.Comment fonctionnent les bots de trading en intelligence artificielle ?

Les bots analysent les données du marché et sociales en temps réel, puis automatisent les échanges instantanément. Des plateformes commeEdgen Radarsuivre les portefeuilles intelligents et les tendances du marché, vous maintenant en avance.

3.Qu'est-ce quemémecoinrisques ?

Les mémo-coïnssont extrêmement volatils et spéculatifs. Le prix est déterminé par la communauté et le buzz plutôt que par des fondamentaux solides. Faites attention aux opérations de pompage et de vidange ainsi qu'aux arnaques.

4.Peut l'IA prédire précisément les prix des cryptomonnaies ?

L'IA améliore considérablement les prévisions, mais la crypto reste imprévisible. Les facteurs externes toutefois (régulation, actualité, événements majeurs) peuvent encore surprendre les marchés.

5.Comment les débutants commencent-ils à investir ?

Utilisez Edgen Searchchoisissez une bonne plateforme d'échange, investissez en toute sécurité et suivez votre parcours via Edgen Feed.

Dernières réflexions : L'IA +MémecoinRévolution du commerce

L'avenir du trading crypto intègre l'intelligence artificielle et la hype portée par la communauté. L'intelligence artificielle aide les traders à naviguer dans la complexité, tandis quememecoinsoffrir des investissements culturels excitants, bien que risqués.

Les plateformes commeEdgen AIdiriger cette révolution, en combinant des analyses en temps réel sur la chaîne de blocs avec l'analyse sociale. C'est une vision claire du présent, plus intelligente et plus rapide que quiconque.

Prêt à adopter des jetons alimentés par l'IA etmemecoinsCommencez petit, négociez intelligemment, restez informé et laissezEdgen AIaidez-vous à dominer le marché dynamique des cryptomonnaies.

Investir, enfin, tu n'es plus seul.

Essaie Edgen gratuitement. Sans carte, sans engagement.