Edgen AI 如何用AI洞察力重塑加密货币交易

加密货币交易的未来是人工智能驱动的

加密货币交易是一个无情的挑战。价格在几秒钟内波动,受到从大型鲸鱼交易和机构交易到病毒式传播的推文以及市场情绪突然上升等各种因素的影响。无论人类多么熟练,都无法同时分析所有的链上数据、社交热度和交易模式。

输入Edgen AI为这种混乱而精确打造的加密货币交易助手。

Edgen AI利用实时链上分析、尖端人工智能和深度社交智能,在市场其他参与者做出反应之前发现有利可图的加密货币机会。传统交易工具可能过于关注历史价格图表和技术指标,而Edgen则更进一步:它处理实时区块链活动、社交情绪和AI驱动的见解,从而提供明确的交易优势。

本文详细解析了Edgen AI如何改变加密货币交易,以及为什么基于人工智能的洞察力代表了金融市场的一次重大飞跃。

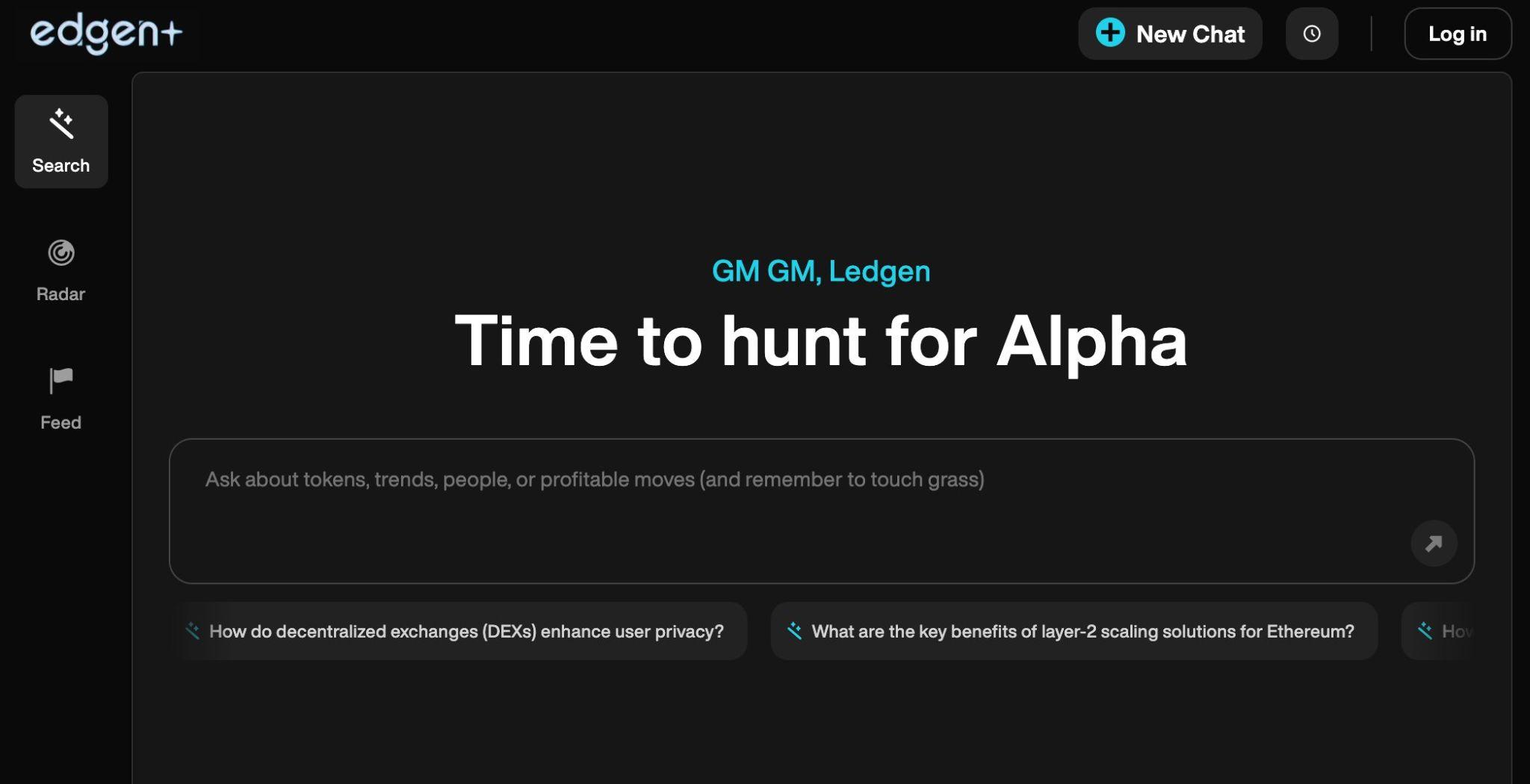

什么是Edgen AI?更聪明地交易,而非更辛苦地交易

下一代人工智能交易基础设施

Edgen AI是一个面向需要精准、速度和实时清晰度的加密货币交易者的下一代买方AI交易基础设施。它结合了:

- Real-time On-chain Analysis即时追踪区块链交易、巨鲸动向、流动性流动和关键代币活动。

- 人工智能驱动的市场洞察:在显而易见之前锁定隐藏的交易机会。

- 社交智能追踪实时监控影响者、关键意见领袖(KOL)和社区情绪,以检测新兴的叙事。

通过Edge AI,交易者可以自信地应对加密货币市场的复杂性,并持续获取超额收益。

为什么传统工具无法与Edgen AI竞争

传统的加密货币工具主要依赖历史价格数据、基本趋势线和技术指标。虽然这些方法在慢速市场中可能足够,但在如今快速演变的、由人工智能驱动的市场中却显得不足。

Edgen AI 打破了这种传统方法,通过:

- 即时分析实时链上数据在传统交易员注意到之前发现隐藏的市场走势。

- 跟踪实时社会情绪了解市场心理和加密货币社区驱动的“泵基础“.”

- 赋能人工智能驱动的决策让交易员能够迅速执行策略,这些策略基于数据而非直觉。

使用Edge AI可直接转化为更智能的策略、更深入的洞察以及更快的交易执行。

人工智能在加密货币交易中的力量:Edge的不公平优势

1. 基于人工智能的预测分析

加密货币市场看起来可能随机……但当你引入人工智能时情况就不同了。Edgen AI 利用先进的预测分析技术,发现人类无法迅速察觉的隐藏模式:

- 每秒扫描数百万个数据点以预测价格波动。

- 在主流趋势形成之前,发现新兴的市场趋势和异常情况。

- 跟踪社会情绪以确定影响市场的叙事和炒作周期。

通过Edge AI,交易者可以保持主动,而不是追逐昨日的新闻。

2. 基于链上数据的实时市场分析

忽略区块链数据成本交易者有价值的机会。Edgen AI 深入分析实时链上活动以发现:

- 鲸鱼移动即时识别暗示价格大幅波动的大额交易。

- 智能合约交互通过DeFi协议检测关键的钱包交互。

- 流动性转移通过监控跨交易所的代币流动性流动来预测价格变化。

访问 Edgen Radar探索实时区块链分析。

3. 人工智能辅助交易与人工交易

手动交易令人疲惫、情绪化,并容易导致代价高昂的错误。Edgen AI 通过以下方式消除了这种不确定性:

- 持续全天候扫描市场,从不错过任何节奏。

- 基于精确的数据驱动信号自动执行交易。

- 完全消除情感偏见,严格专注于数据和策略。

利用人工智能驱动策略的交易者始终优于仅依赖直觉的交易者。

让Edgen AI脱颖而出的关键特性

1. 实时全面市场分析

- 对链上和链下数据的即时处理。

- 流动性、巨鲸动向和关键钱包活动的持续监控。

- 加密货币推特、电报和意见领袖网络中的情绪追踪。

探索 Edgen 的 real-time Feed监控市场活动。

2. 人工智能驱动的交易信号

- 实时警报,精准识别高概率交易机会。

- 预测性分析提前识别被低估的代币。

- 先进的算法在主流认知之前就能揭示隐藏的买入和卖出信号。

3. 智能风险管理工具

- 基于人工智能的风险评估以标记潜在风险操作。

- 根据市场状况定制的智能止损和仓位管理建议。

- 灵活的风险配置,可适应交易员的偏好。

4. 自动交易策略

- 基于实时市场洞察的即时AI驱动交易执行。

- 情绪中立交易,消除冲动决策。

- 持续监控,确保您把握每一个可能的机会。

开始使用 Edgen search发现交易信号和市场机会。

人工智能在加密货币交易中的未来:Edge的愿景

1. 改进的人工智能市场预测

在接下来的几年里,像Edgen这样的AI驱动平台将:

- 更早地准确预测市场趋势。

- 发现人类交易员无法察觉的隐藏阿尔法信号。

- 通过更先进的预测模型进一步降低交易风险。

2. 链上数据变得至关重要

- AI将标准化地追踪DeFi趋势、巨鲸交易和社会情绪。

- 透明度来自blockchain data将成为成功策略的基础。

3. 自动化AI交易的主导地位

- 基于人工智能的交易机器人将变得司空见惯,而非例外。

- 人工交易将因人工智能持续展现出更高的效率而大幅减少。

Edgen AI 完美地处于引领这一变革的位置。

通过Edgen AI,现在开始更聪明地交易

加密货币交易正在迅速发展,未来显然属于由人工智能驱动的交易者。Edgen AI 为您提供所需的工具,以:

- 揭示更深入的市场洞察,提升决策能力和利润。

- 利用实时区块链分析,领先一步。

- 交易中去除情绪,让数据引领方向。

不要更努力地交易:要更聪明地交易。今天就拥抱由人工智能驱动的加密货币交易未来,与 Edgen AI并始终领先于市场。

文章的SEO优势

✅强有力的标题和元描述:

- 标题包含关键词且具有吸引力。

- 元描述简洁且具有吸引力,概括了要点,并包含了相关的关键词,如“基于人工智能的洞察”,“加密货币交易”等。

✅标题的有效使用(H1、H2、H3 等)

- 文章结构清晰,有明确的标题。

- 它以逻辑顺序涵盖关键子主题,这有助于提高可读性和SEO。

✅关键词优化:

- 文章包含高价值的加密货币和人工智能相关关键词,例如:

- “基于人工智能的洞察”

- “在“链数据”,

- “阿尔法交易信号,

- “实时市场分析”,

- 这些关键词有助于提升与AI驱动的加密货币交易相关搜索的排名。

✅内容深度与专业知识:

- 文章提供了详细的见解、案例研究和解释,显示出对这一主题的权威性。

- 谷歌重视为SEO排名而进行的深入研究和详尽内容。

✅可读性与参与度:

- 简短的段落和简洁明了的语言能提升用户体验和停留时间。

投资这事,终于不用一个人了

免费试用 Edgen。不用信用卡,不绑约