Alpha Trading: La forma inteligente de superar al mercado

¿Qué es el Trading Alfa?

La mayoría de los traders de criptomonedas pierden dinero. ¿Por qué? Les falta una ventaja crítica. Una ventaja llamada "alpha".

El trading alfa implica superar consistentemente los índices del mercado. Va más allá de gráficos básicos o fundamentos. Los movimientos del mercado actual siguen narrativas, tendencias de datos y momentum social.

Plataformas impulsadas por IA comoEdgen AI procesar datos del mercado en grandes cantidades de forma inmediata, identificando patrones y señales de alpha que los traders humanos pasan por alto. Al combinar análisis de blockchain, sentimiento social y inteligencia artificial avanzada, Edgen elimina puntos ciegos y proporciona una ventaja competitiva.

Definir Alpha en el trading

Alpha mide los rendimientos por encima del rendimiento estándar del mercado.

Por ejemplo:

- Si la referencia del mercado crece un 7 %, pero su cartera sube un 12 %, su alpha es igual a +5 %.

- Esos 5% adicionales se deben a una mejor inteligencia de mercado, reacciones más rápidas y decisiones más inteligentes.

Esos 5% adicionales se deben a una mejor inteligencia de mercado, reacciones más rápidas y decisiones más acertadas.Para una vista más detallada de cómo funciona el alpha en el rendimiento del portafolio, consulte laCorporate Finance Institute’s explanation of alpha.

Cómo los operadores encuentran Alpha hoy en día

Las señales Alpha provienen de fuentes identificables:

- Insights impulsados por IA: Las máquinas analizan grandes conjuntos de datos más allá de la capacidad humana.

- Seguimiento de Sentimiento Social: Los movimientos del mercado a menudo siguen narrativas impulsadas por las redes sociales.

- Análisis en cadena: Las actividades significativas de billeteras indican posibles cambios.

- Respuesta Rápida del Mercado: Las reacciones rápidas determinan la rentabilidad en mercados volátiles.

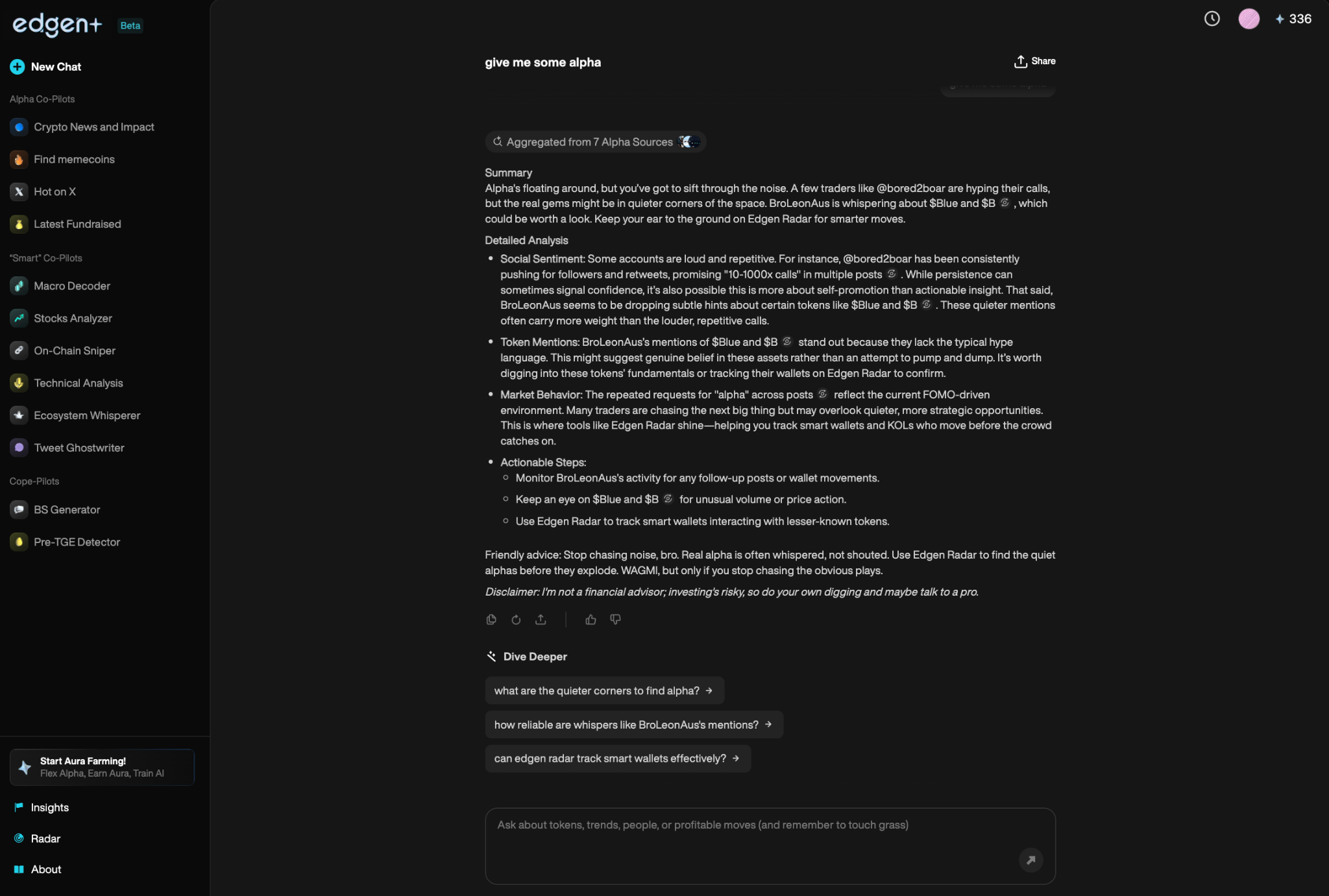

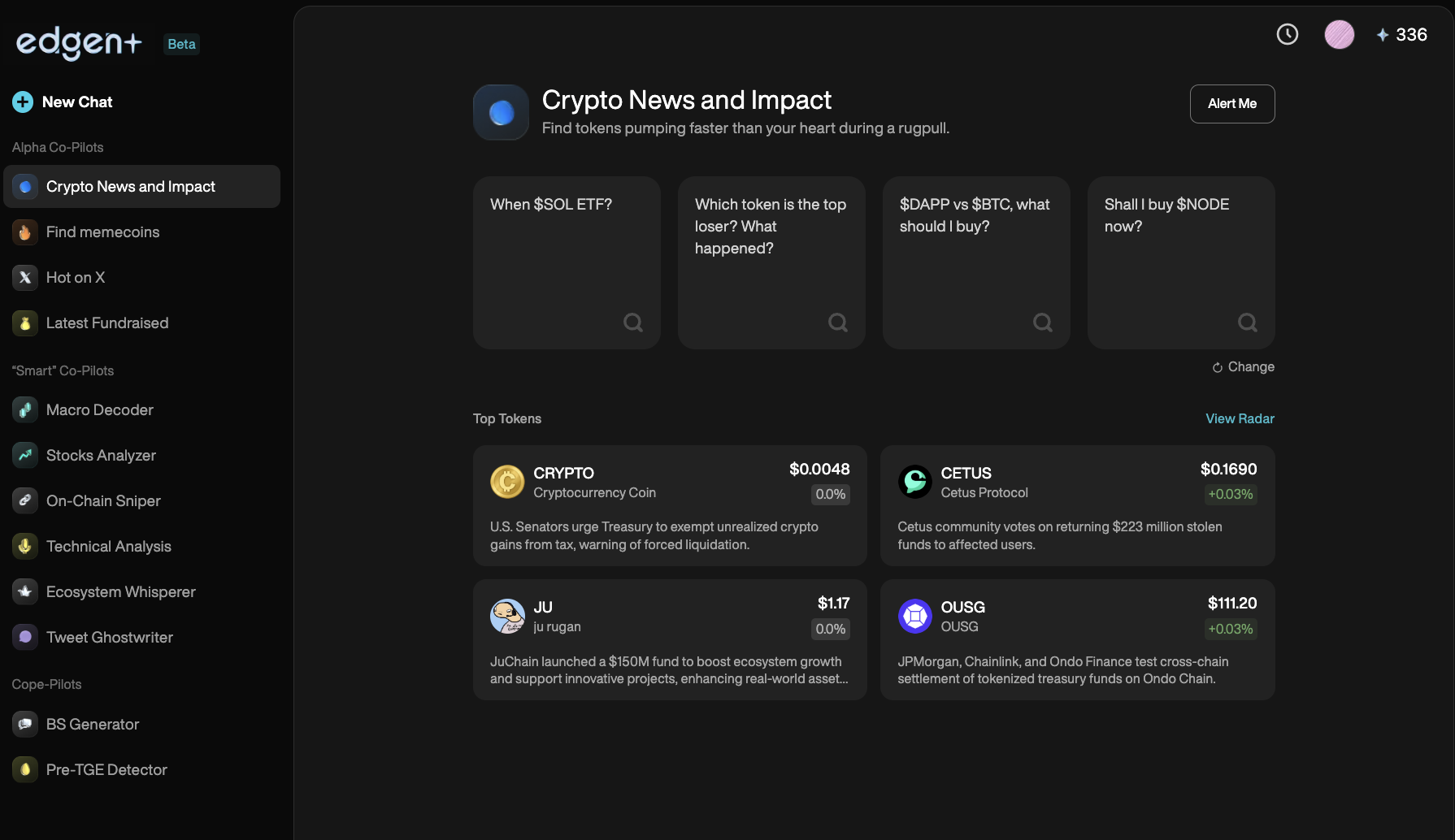

Los métodos tradicionales de comercio proporcionan una visibilidad incompleta. Las plataformas comoEdgen AIrevelar señales alfa en tiempo real, permitiendo a los operadores actuar primero.

Cómo la IA Cambia Alpha Trading

La inteligencia artificial ya no representa el futuro del comercio. Actualmente define el éxito en los mercados.

Las ventajas del trading con inteligencia artificial:

- Procesamiento de Datos en Tiempo Real: La IA evalúa grandes conjuntos de datos y lo hace de inmediato.

- Detección Temprana de Patrones: La IA detecta tendencias antes que los operadores humanos.

- Comercio sin Emociones: Elimina la venta desesperada y las compras impulsivas.

- Detección en Tiempo Real de Alpha: Descubre oportunidades ocultas antes de la conciencia general.

El AI Edgen ofrece herramientas distintas diseñadas para el trading de alfa:

- Edgen Radarmuestra la sentimiento del mercado en tiempo real, los cambios de precio y las señales de alpha.

- Edgen Searchrespuestas preguntas detalladas del mercado utilizando datos verificados, eliminando el ruido.

- Edgen InsightsProporciona un centro colaborativo para que los comerciantes compartan opiniones de inmediato.

El comercio sin IA limita significativamente la visibilidad del mercado. Edgen AI permite a los traders ver lo que otros pasan por alto.

Alpha Signal Trading: Encontrando Operaciones Ganadoras

Las señales Alpha proporcionan indicaciones tempranas de operaciones rentables.

Ejemplos de Señales Alpha:

- Movimientos Súbitos en el Precio: Subidas o caídas rápidas indican puntos de acción.

- Aumentos de Volumen: Una alta actividad de trading indica oportunidades.

- Actividades en cadena: los billeteras de ballenas y los movimientos de billeteras influyentes predicen los movimientos del mercado.

- Sentimiento Social: El entusiasmo de la comunidad predice aumentos en el precio de las criptomonedas.

Edgen Radaridentifica estas señales de inmediato, mientrasEdgen Searchrastrea a los comerciantes influyentes y temas en tendencia, permitiendo a los comerciantes actuar primero.

Mejores Estrategias para el Trading Alfa Definidas

Para comerciar con beneficios, siga estrategias de alpha probadas:

1. Seguimiento de Tendencias

identificar temprano las tendencias del mercado. Usar alertas de IA para entradas y salidas oportunas.

2. Reversión a la media

El comercio identifica condiciones de sobrecompra o sobreventa hacia el valor justo. La IA detecta los momentos óptimos para operar.

3. Arbitraje Inteligente

Captura instantánea de diferencias de precios entre intercambios. Los bots de IA automatizan la ejecución de manera eficiente.

Edgen AI desarrolla herramientas especializadas para ejecutar estas estrategias con precisión.

¿Por qué los datos en cadena son importantes en el trading de alpha

Las transacciones de blockchain proporcionan información, revelando señales críticas de trading:

- Movimientos de la Cartera Inteligente: Los principales monederos influyen en los precios del mercado criptográfico.

- Actividad de Contrato Inteligente: Las tendencias DeFi surgen de las dApps activas.

- Flujos de liquidez: Los movimientos de dinero hacia y desde las bolsas indican cambios en el mercado.

Edgen Radarproporciona información en tiempo real sobre blockchain, permitiendo a los traders actuar con decisión antes que otros.

Errores Comunes de los Comerciantes Explicados (Y Cómo Evitarlos)

- Error: Comerciar sin un plan.

Solución: Definir los puntos de entrada y salida antes de ingresar a una operación.

- Error: Ignorar los datos sociales y blockchain.

Solución: Reconocer que las narrativas y las actividades de blockchain impulsan los mercados hoy en día.

- Error: Sobreturismo debido a FOMO.

Solución: Priorizar la calidad sobre la cantidad. La IA ayuda a eliminar los sesgos emocionales.

- Error: Operar como inversores minoristas típicos.

Solución: Utilizar inteligencia artificial, análisis de blockchain y herramientas de automatización para obtener una ventaja decisiva.

El Futuro de la Comerciación Alfa y la IA

Los estrategias de trading se centraron en inteligencia artificial, análisis de blockchain e inteligencia social.

¿A dónde va la Dirección de Alpha Trading:

- Dominio de la IA: Las máquinas predicen y ejecutan operaciones mejor que los humanos.

- Análisis de Blockchain: Los datos en cadena se convierten en análisis de mercado estándar.

- Inteligencia Social: captura la sensibilidad como la nueva métrica fundamental.

Edgen AI impulsa este cambio, integrando de manera fluida las perspectivas de blockchain, el sentimiento social y las estrategias impulsadas por inteligencia artificial.

Cómo los operadores se mantienen a la vanguardia

Los traders que tienen éxito en el trading alfa siguen consistentemente estas reglas doradas:

- usarEdgen Radar,Edgen SearchyEdgen Feedpara obtener información precisa.

- monitorear las actividades de la cadena de bloques, especialmente los movimientos de las billeteras de ballena.

- seguir las tendencias de la sentimiento social, ya que la euforia mueve a los mercados de manera decisiva.

- evitar el comercio emocional siguiendo estrictamente las señales de IA basadas en datos.

- permanecer adaptable; las dinámicas del mercado evolucionan constantemente.

Los mejores traders anticipan los movimientos del mercado antes de que otros los sigan.

Invertir, por fin, ya no es cosa de uno solo.

Prueba Edgen gratis. Sin tarjeta, sin compromiso.