人工智能如何助你获得优势:阿尔法交易的秘诀

阿尔法交易:人人都追逐的优势(但很少有人能抓住)

每个交易者都在追寻阿尔法(Alpha)。这是每个人都想要的超越市场的洞察力,但很少有人能尽早发现以获得巨大收益。

剧透:基于人工智能的交易就是作弊码。

一旦阿尔法进入加密推特,它就不再是阿尔法,而只是残余物。传统市场分析根本无法跟上链上、技术性和社交数据的持续涌入。

输入 Edgen AI—将混乱转化为清晰,将模式转化为利润,将交易者变为传奇。

那么,什么是Alpha交易呢?

Alpha意味着超越市场基准。这就是对冲基金、巨鲸和去中心化交易者无论市场上涨还是下跌都能保持盈利的方式。

传统的交易工具,如图表和基本指标?它们对婴儿潮一代的股票投资组合来说已经很不错了,但并不适合加密货币快速且无情的市场环境。

今天的Alpha需要解读社交情绪(“泵 fundamentals”)),通过链上数据追踪鲸鱼实时动向,并在普通投资者跟风之前识别隐藏趋势。

Edgen AI 准确地实现了这一组合,具体包括:

- 🔥 基于人工智能的分析,实现更智能、更快的交易操作。

- 🐳 跟踪鲸鱼动向和实时资金流动的链上情报。

- 📢 社交智能解码关键意见领袖(KOL)的炒作。

这个三重边角意味着更少的盲区、更锐利的阿尔法(Alpha),以及更少的时间用于在推特上消极浏览以寻找信号。

AI:你的交易大脑的强化版

交易中的人工智能就像把生锈的自行车换成火箭。EdgenAI可在几秒钟内处理大量数据,而人类交易员可能需要数周时间才能理清。

AI驱动的阿尔法信号:你的新超能力

- 模式检测:AI能看到人类无法察觉的趋势。

- 快速决策:即时数据处理。

- 无情绪逻辑:告别恐慌性抛售和错失恐惧(FOMO)买入。

- 更准确的预测:Edgen从历史和实时数据中学习,以实现更精准的预测。

最棒的是?EdgenAI整合社会趋势、新闻资讯和区块链数据,比你还没说完“文月”就能更快提供全面的360°市场视角。

事实上,一个 study by NBER展示机器学习模型可以预测交易量并产生阿尔法级回报,这证明了像Edgen这样的AI交易工具的潜力。

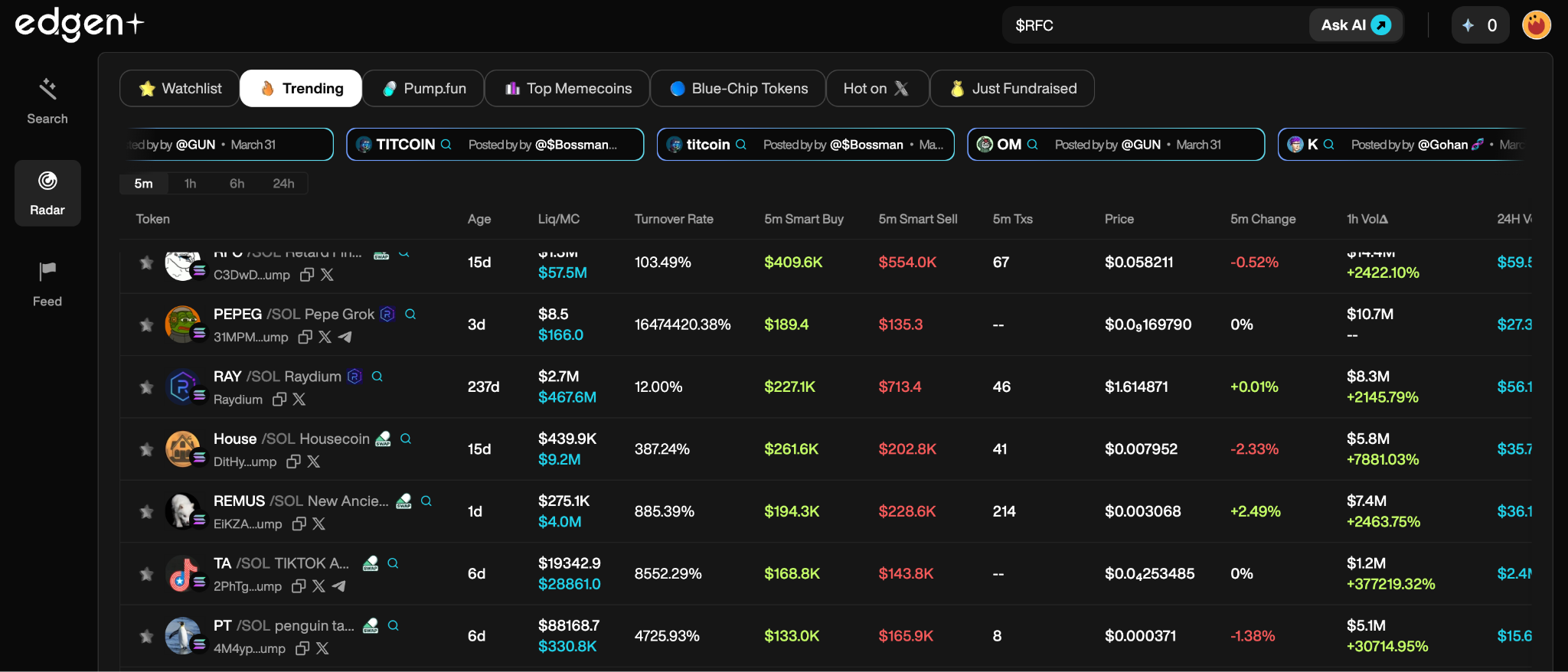

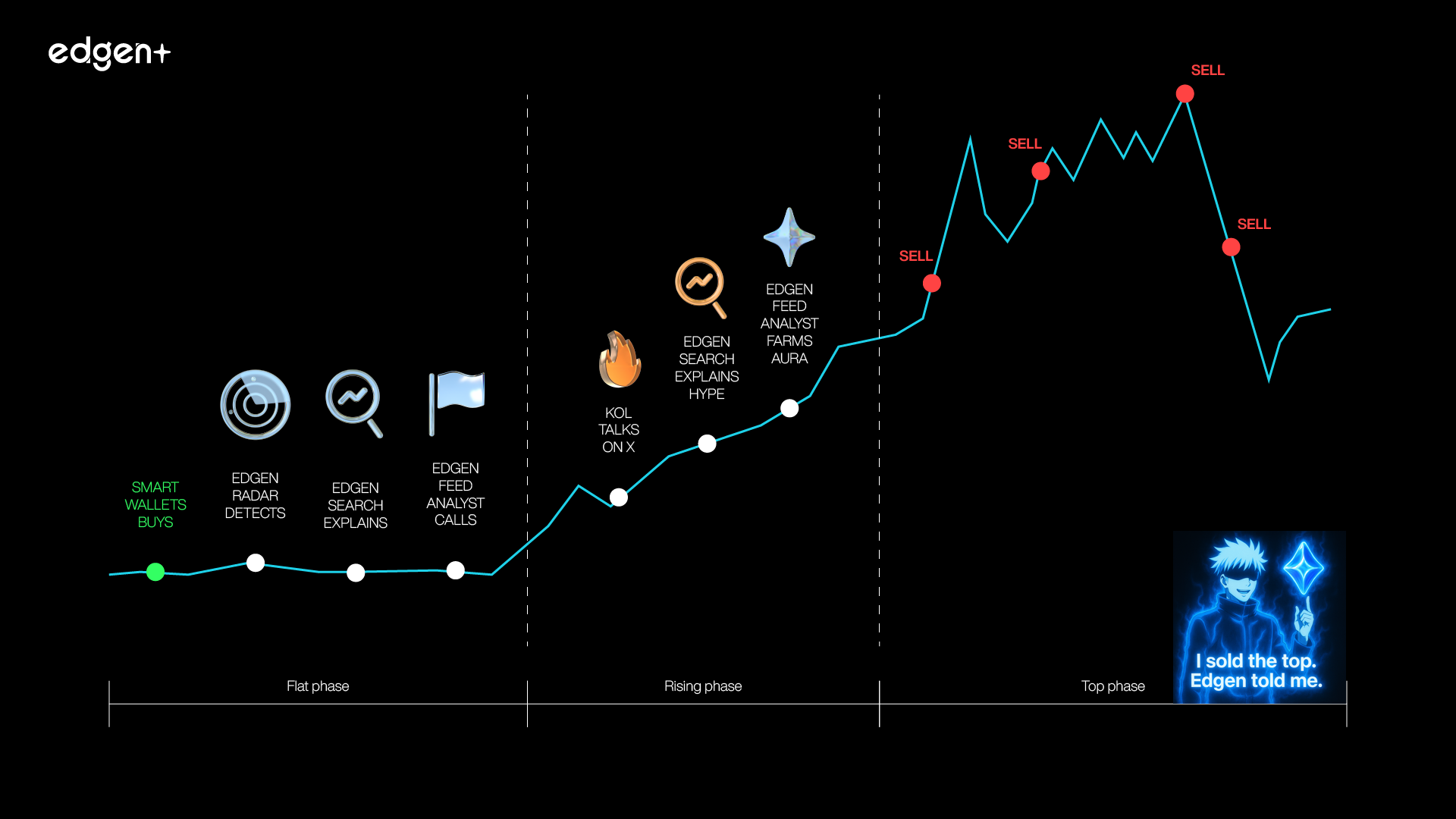

观鲸2.0:链上数据的力量

区块链的透明性意味着大玩家再也无法隐藏他们的行动。通过链上数据,你将看到:

- 智能钱包正在积累(或抛售)多少?

- 代币迅速加速。

- 社交热度和智能账户如何直接影响代币价格。

不要再猜测了。凭借EdgenAI的实时区块链追踪功能使Alpha变得明显且人人可及。

现实世界的优势:

- 在价格飙升前识别聪明资金的动向。

- 跟踪中心化交易所(CEX)和去中心化交易所(DEX)之间的流动性变化。

- 解码社会情绪对市场行为的影响。

结果是:交易达到目标,风险管理更加精准,你的投资组合终于出现了些许阳线。

通过人工智能和阿尔法信号最大化利润的4个步骤

准备好从普通玩家升级为专业玩家了吗?这是你的蓝图:

1. 使用EdgeN搜索进行快速侦察

即时获取AI驱动的洞察和链上深度分析Edgen Search了解一切,而不必阅读一切。

2. 通过Edgen Radar跟踪热门趋势

Edgen Radar在其他人察觉之前,及早捕捉鲸鱼信号和社交基本因素。反应要快,不要迟缓。

3. 风险管理:别像菜鸟一样交易

AI提供冷静、无偏见的风险评估。不要盲目支付租金。像专业人士一样交易。

4. 紧密关注市场变化

加密货币不会等待任何人。定期利用Edgen Search和Radar比市场变化更快地调整你的策略。

AI与链上数据结合的交易:专业交易者必看的5个常见问题

1. Alpha交易是什么?

阿尔法交易意味着持续战胜市场及早发现有利可图且风险较低的交易。EdgenAI为您提供实时AI信号和链上数据,助您更智能、更快地交易。

2. 人工智能如何具体地加速阿尔法交易?

AI可以迅速扫描大量数据,发现隐藏的模式,消除情感偏见,并提高市场判断的准确性。凭借EdgenAI会看到这些动作,而迟到的人还来不及在推特上问“什么在飙升?”

3. 为什么我应该关注链上数据?

实时区块链数据揭示鲸鱼活动、代币动量和流动性变化。基于事实交易,而非情绪——始终优先模仿,其次盈利。

4. 什么让Edgen AI更优秀?

Edgen结合人工智能的精准性、实时区块链洞察力以及社交情绪分析。没有盲点,无需猜测——只有干净、可操作的阿尔法。

5. Edgen是否保证盈利交易?

不,这里没有魔法。但是Edgen实时情报和预测分析可显著提升你的胜算。稳健的风险管理仍然至关重要。Edgen帮助你更聪明地模仿,而不是盲目地硬干。

为交易优势做好未来准备

AI和链上洞察现在已成为必备工具。Edgen AI 提供您在当今加密货币市场中取得主导地位所需的一切:

- 🧠 基于人工智能的分析。

- ⛓️ 实时区块链数据。

- 📈 社会趋势解码(“pumpamentals”)

通过Edge AI,任何交易者都不必再盲目交易。率先发现趋势,自信交易,最终开始获取真正的阿尔法收益。

欢迎来到新的交易标准。您的阿尔法优势现已升级。

投资这事,终于不用一个人了

免费试用 Edgen。不用信用卡,不绑约