從迷因幣到股票:AI交易如何重塑全球市場

AI正在改寫遊戲規則

金融市場已經改變。從迷因幣到股票交易時,交易已超越了圖表和人工分析。傳統策略已顯不足,使交易者仍停留在過去。

由AI驅動的工具,以...為引領Edgen AI即時解碼市場情緒、社交動能與鏈上行為。這項優勢意味著比以往更銳利、更聰明且更快地進行交易。

為何AI交易現在主宰市場

AI在讀取市場趨勢方面超越人類交易員。以驚人的速度處理數十億個數據點,AI能捕捉市場變動、影響者信號和隱藏的敘事。

AI驅動的交易是指:

- 預測分析:看到市場敘事在他人注意到之前逐漸形成。

- 演算法交易:在微秒級執行交易。

- 情感分析:立即捕捉Twitter的熱潮與影響者趨勢。

- 進階風險管理:在它發動前偵測到空頭信號。

重點是:AI 預測市場。人類反應;AI 預測。

Edge:能讀懂氣氛的AI

Edgen AI 整合即時鏈上資料與社群“泵基礎知識,並將其轉化為可執行的見解。它能識別關鍵意見領袖(KOLs),監測智能錢包,並在群眾之前提供alpha。

核心功能:

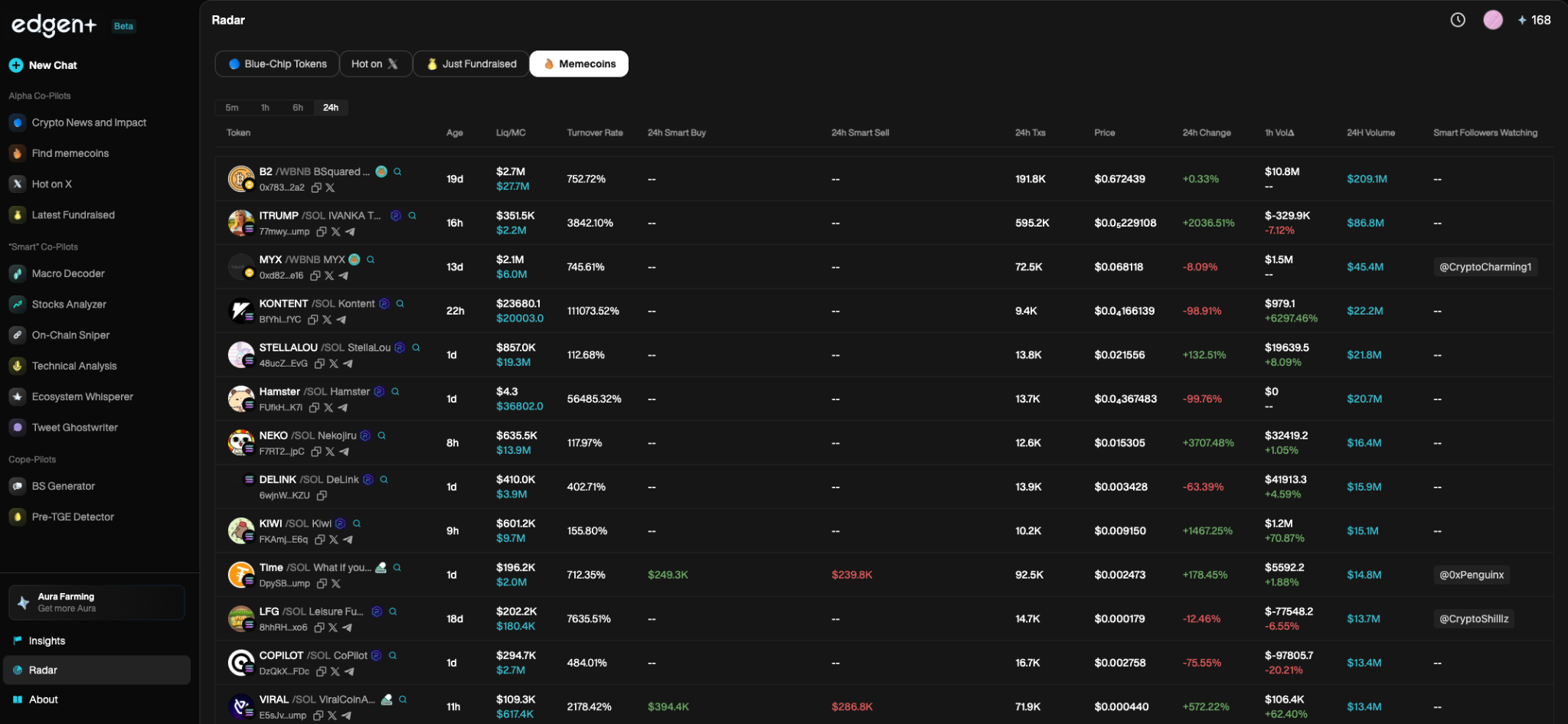

- 即時資產監控:Edgen Radar追蹤價格走勢與社群情緒。

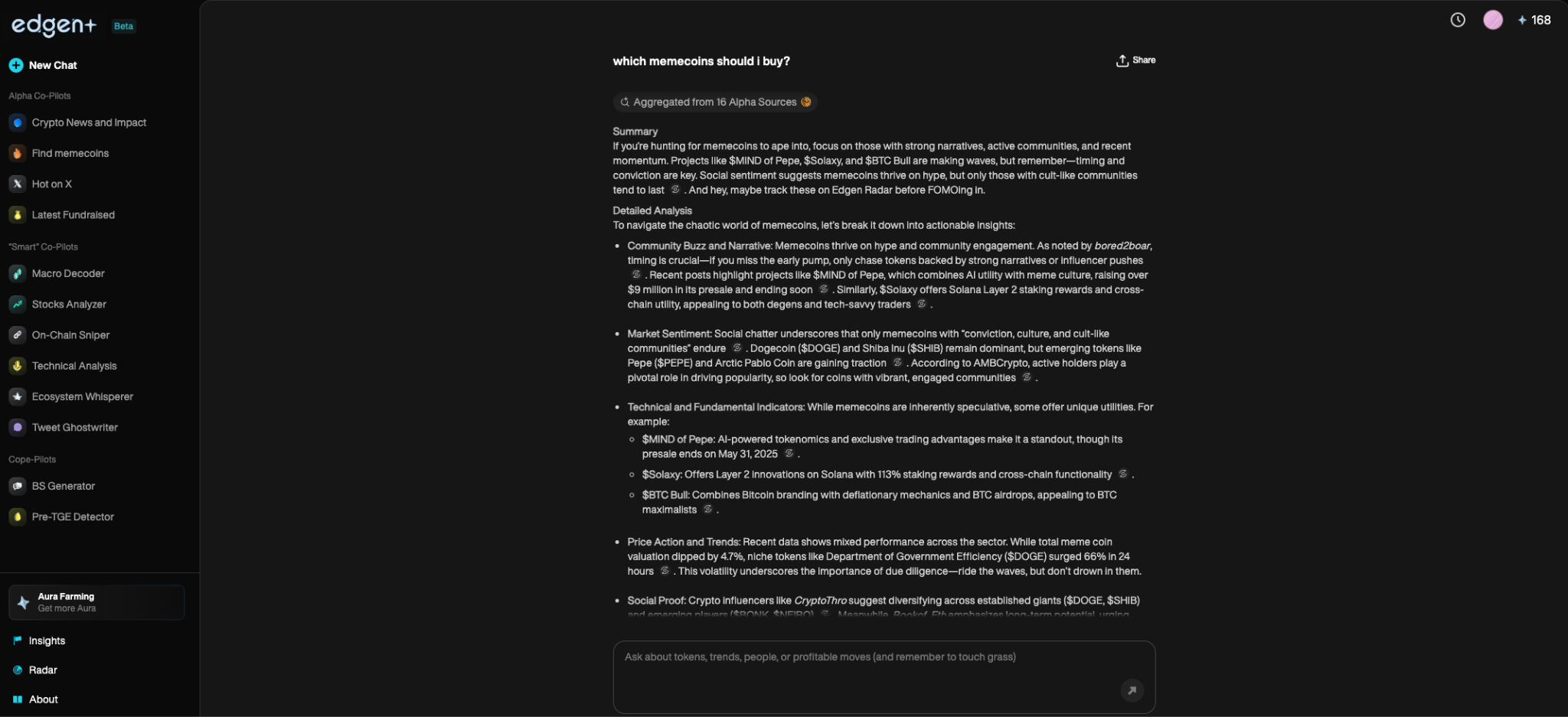

- AI驅動的搜尋:Edgen Search從聚合資料中即時提供市場洞察。

- 社群驅動的分析:Edgen Feed提供即時的群眾產生的alpha訊號。

Edgen AI 識別市場的脈動,即推動每一筆交易的集體心態。

迷因幣以及人工智慧:天生一對

迷因幣超越傳統估值範疇。價格波動跟隨熱潮、社群參與度和病毒式傳播的動能。

AI 在此環境中蓬勃發展。Edgen AI 創新性地具備處理能力迷因幣利用即時情緒追蹤來捕捉快速的市場變動。

Edgen AI 碩士迷因幣由以下方式交易:

- 情感分析:在Twitter/X上即時掃描拉高訊號。

- 鏈上洞察:即時追蹤鯨魚錢包與影響者活動。

- Alpha偵測:在價格爆炸前發現隱藏指標。

迷因幣平均波動性與無情的競爭。沒有AI,交易者毫無勝算。

AI 與現代投資策略

市場已經超越了基本面。社會情緒、預測分析和鏈上交易定義了現代策略。

AI在智慧投資中的角色:

- Alpha Discovery:在市場波動前發現訊號。

- 人工智慧管理的投資組合:AI驅動的基金提供最佳化風險管理。

- 區塊鏈整合:監控錢包動態以追蹤智能資金。

Edgen Radar 設定了新標準,詮釋整個市場生態系統,而非孤立的指標。

解決交易的三體問題

大多數交易者都是部分盲目交易:

- 一些人追蹤鏈上數據,但忽略了社群敘事。

- 其他人跟隨熱潮卻忽視流動性變動。

- 許多人都依賴技術圖表,忽視影響市場的報導。

Edgen AI 透過整合三個維度來解決這份複雜性:

- 鏈上分析:即時追蹤智能資金。

- 社會情緒:捕捉熱潮週期與社群驅動的行動。

- AI驅動的執行:在他人發現商機之前,策略性交易。

這種整合性的方法為Edgen交易者在「PvP」、競爭性、零和市場中提供了決定性的優勢。

人工智慧在金融市場的未來

AI驅動交易的未來。忽略這一點的交易者將可能永遠落後。

接下來是什麼:

- 自我學習人工智慧機器人:AI即時適應新興市場趨勢。

- 自動化Alpha發現:在人類識別之前發現隱藏的機會。

- 進階社會智能:即時解讀影響者引導的敘事。

- 完全由AI驅動的基礎設施:Edgen AI正逐步發展為一個全面的投資平台。

來自的研究University of Michigan highlights how AI and algorithmic systems are transforming modern financial markets強化了類似 Edgen AI 這樣的平台所朝向的發展方向。

Edgen AI已經建立了這個現實,將AI塑造成為一個基本的市場力量。

AI交易革命已經來臨

AI重新定義了全球金融市場:迷因幣股票、加密貨幣、外匯。從高頻交易到alpha探測,AI定義了交易的成功。

Edgen AI 引領這場革命,為交易者在殘酷的市場中提供戰略優勢。沒有使用AI的交易者將面對行動更快、思考更清晰且執行無誤的對手。

市場已經演變。人與人之間的交易消失了。現在是人工智慧對人工智慧。

準備好或沒有,這會是Edgen AI 時代已經來臨!

投資這事,終於不用一個人了

免費試用 Edgen。不用信用卡,不綁約