表情包币、替代币与股票:为什么AI是把握市场趋势的关键

市场永远地改变了。

资金流动迅速。市场变动更快。

投资已经超越了图表、资产负债表和基本面。表情包币、替代币和股票现在开始跟随社交热潮、网红情绪和实时区块链活动。

AI是这场变革的引擎,引导交易者做出更明智的决策、更清晰的预测和更快的行动。Edgen AI将这一新的市场力量称为“Pumpamentals”,即社交动量、影响力和社区驱动的价格波动的交汇点。

没有人工智能的交易意味着错过他人清晰看到的信号。人工智能交易定义了市场成功。

梗币、替代币和股票详解

meme币:带有严肃收益的玩笑

表情币最初是网络玩笑:狗狗币(DOGE)、柴犬币(SHIB)、佩佩币(PEPE)。这些资产缺乏传统金融实力,却因社交媒体的关注和病毒式传播的梗而飙升。

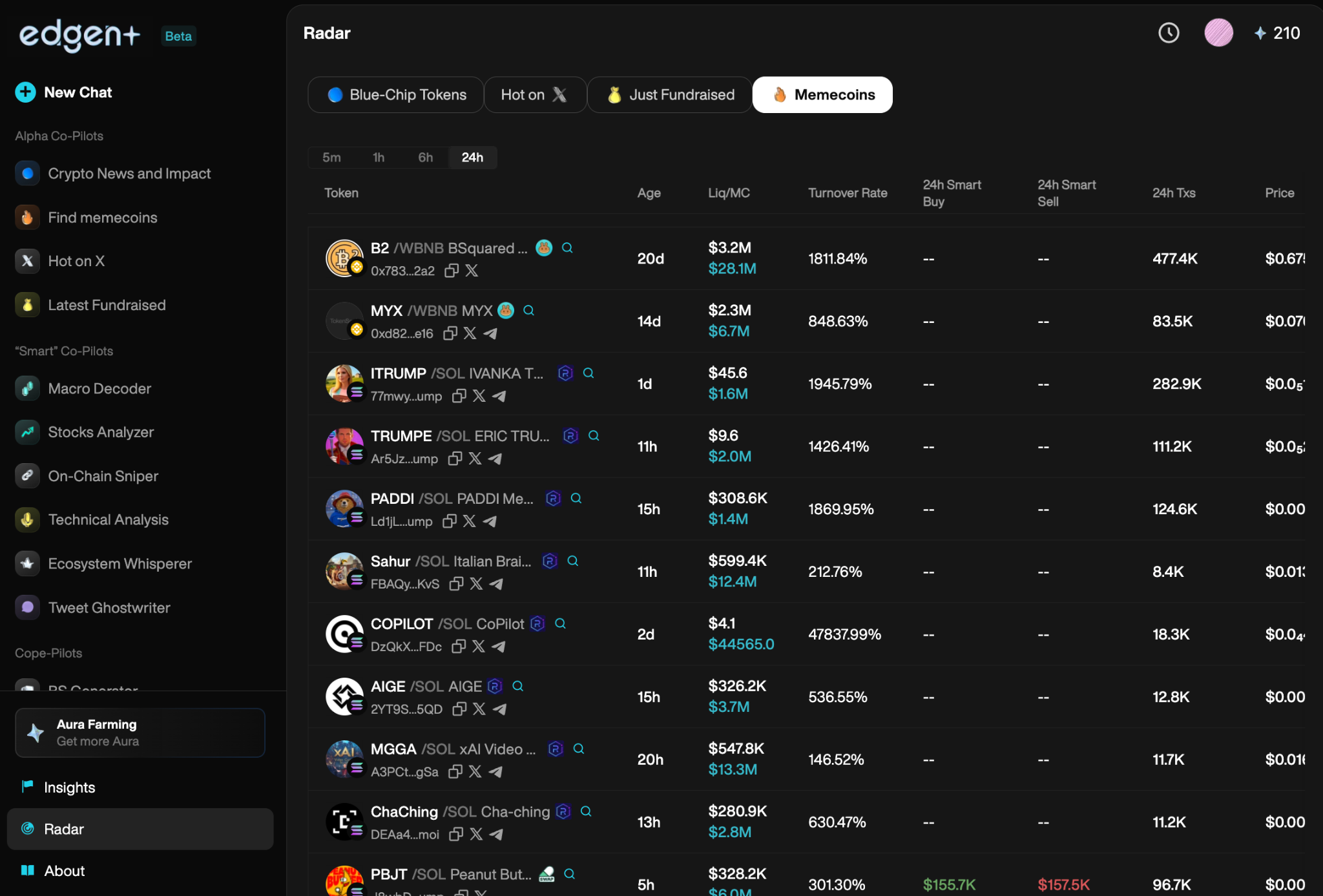

Memecoin价格迅速上涨后又暴跌。Edgen AI跟踪Twitter情绪、社交参与度和意见领袖的动向,在炒作发生前识别出潜在的炒作。

山寨币:不仅仅是比特币的替代品

其他加密货币(Altcoins)指的是除比特币以外的加密货币,包括以太坊(ETH)、Solana(SOL)和专注于人工智能的代币。 Learn more about altcoins, their types, and how they differ from Bitcoin与迷因币不同,替代币(altcoins)通常提供明确的用例、功能或现实世界的价值。

Edgen AI追踪小市值加密货币市场信号、链上钱包变动以及社区情绪变化,以尽早发现交易机会。

股票:传统资产的演变

股票代表苹果、特斯拉和亚马逊等大型公司的股份。虽然传统的投资规则仍然适用,但人工智能正在改变股票市场的投资方式。现在,公司使用人工智能驱动的平台,即时分析财报、新闻标题和投资者情绪,使得人工智能驱动的交易变得至关重要。

人工智能如何定义现代市场趋势

AI即时预测市场情绪

投资者情绪决定资产价格。Edgen AI 检测社交媒体(推特/X)和区块链数据,可在市场情绪发生转变被广泛认知之前识别出这种变化。

- 即时跟踪影响者和社区的情绪。

- 预测市场变动前的叙事变化。

用人工智能掌握链上数据

链上分析揭示了如钱包活动、资金流动和智能资金行为等隐藏的市场信号。Edgen AI 清晰地解析区块链数据,在大多数交易者注意到之前提供实时警报。

Edgen AI 发现一个主要钱包正在积累一种低市值的替代币。使用 Edgen 的 Radar 的交易者会立即收到警报,从而捕捉早期利润。

阿尔法信号:人工智能的终极优势

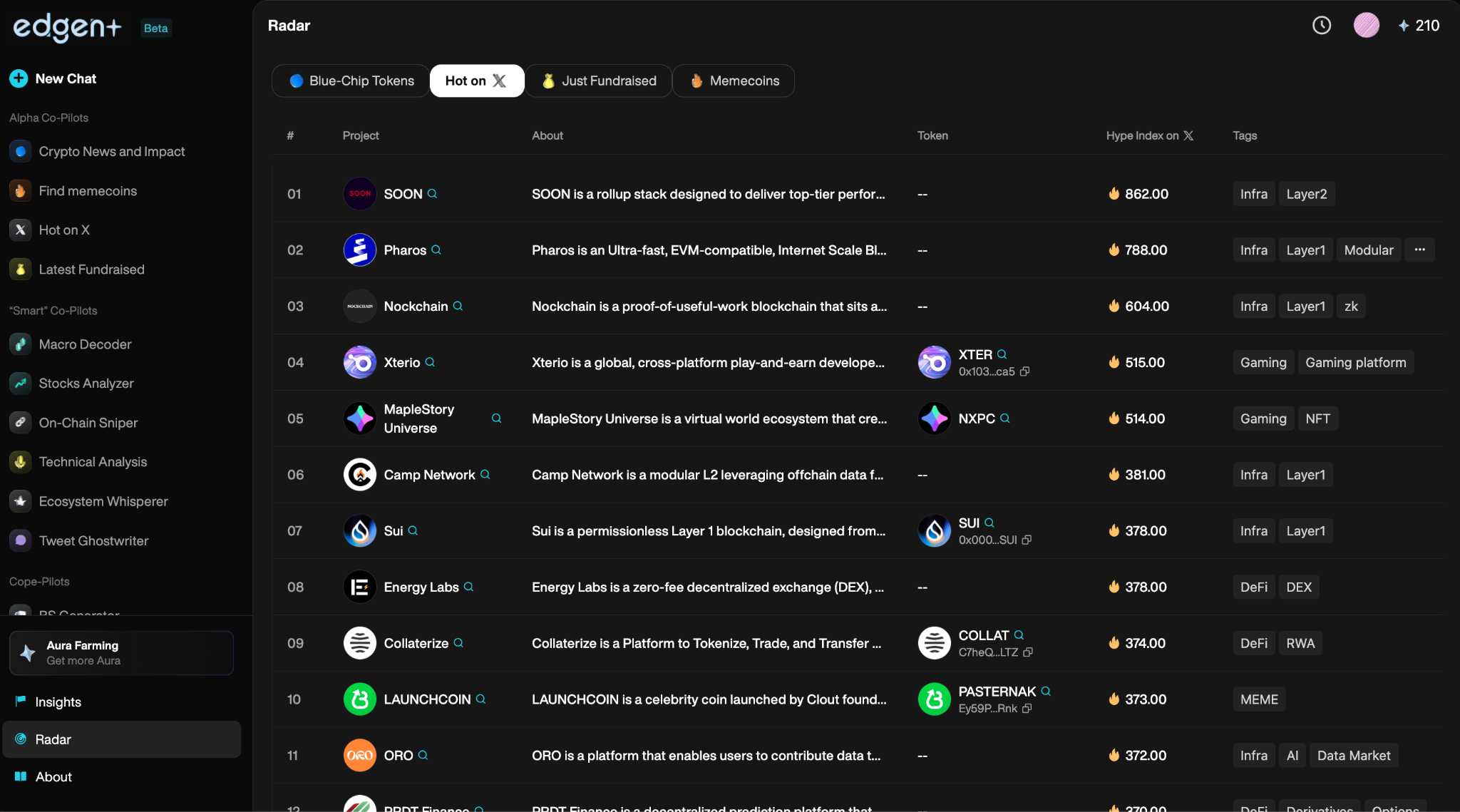

Alpha信号突出显示了具有增长潜力的被低估资产。Edgen AI可即时处理大量数据,迅速揭示突破性指标。通过运行实时查询来探索隐藏的Alpha。 Edgen Search交易员的AI驱动搜索引擎。

- 增加的开发者活动

- 不断增长的持币者数量

- 社交媒体提及量上升

AI在价格反映这些机会之前就能识别它们。

加密货币和股票中的AI驱动交易算法

AI交易机器人:新标准

人工智能交易更快、更智能,且没有情绪。

AI精准、冷静且以极快的速度进行交易。高频交易(HFT)机器人能在毫秒级别内完成交易,超越人类的反应能力。

Edgen Radar专注于快速交易执行、实时阿尔法识别和全面的市场洞察。

人工智能与社会共识

仅靠技术分析是不够的。Edgen AI 融合了社交情绪和社区叙事,以捕捉市场的集体心态:

- 智能钱包操作(买入/卖出动作)

- 关键意见领袖(KOL)活动

- 推特/X上的热门话题和意见领袖动态

AI比人类更快地检测社会情绪

社会动量、网红趋势和社区参与度在一夜之间推动价格变化。Edgen AI 持续监控并清晰评估这些信号。实时监测市场对话和社区内幕信息。 Edgen Feed:

- 看涨信号:病毒式参与、网红关注度上升、巨鲸囤积。

- 看跌警告:社会兴趣下降、叙事转变、参与度降低。

AI首先捕捉情感变化,从而在市场反应之前做出果断交易。

人工智能在未来市场趋势中的关键作用

AI + DeFi:下一个市场前沿

DeFi 持续革新金融行业,AI 加速其发展。

Edgen AI演进为完整的买方交易基础设施:

- 自动化借贷策略。

- 在DeFi中主动管理风险。

- 优化收益挖矿以获得最大回报。

仅靠人工分析无法跟上DeFi的规模。AI现在正引领潮流。

区块链与人工智能:一种强大的交易组合

结合人工智能和区块链技术可显著提高市场透明度和效率:

- AI对智能合约进行审计以发现潜在漏洞。

- 预测最优的Gas费用和交易时间。

- 提升去中心化交易所(DEX)分析以实现更好的交易执行。

人工智能和区块链共同构成了一个强大的交易环境。

为什么现在AI对交易员至关重要

AI变得不可或缺,塑造了交易成功的未来。

交易员需要人工智能的原因是:

- 更快的决策:对数百万个数据点进行即时处理。

- 更高的准确性:人工智能消除人类情感偏见。

- 保持持续警觉:AI 提供持续的市场监控。

- 即时的阿尔法洞察:AI能够清晰追踪实时情绪和链上活动。

没有人工智能的交易会使投资者处于严重不利的地位。

聪明交易,否则落后于人

市场已经永久性地发生了变化。表情包币、替代币和股票在很大程度上依赖于AI驱动的洞察、社交叙事和实时分析。

忽视人工智能的交易者会遇到困难。而采用Edge AI等平台的交易者则利用社交情绪、阿尔法检测和区块链分析,从而远远领先。

未来已经到来。人工智能驱动的交易决定了胜负。你的操作定义了你的市场地位。 Learn more about Edgen AI请将以下英文翻译成简体中文。保持结构和技术术语准确。避免过度翻译。

投资这事,终于不用一个人了

免费试用 Edgen。不用信用卡,不绑约