リアルタイム AI 市場インサイト:すべてのトレーダーが Edgen Trading Radar を必要とする理由

暗号通貨は急速に変化する。ついていくか、取り残されるかである。

暗号通貨市場は常に活動を止めません。価格は急速に上昇し、暴落し、方向転換します。即時の最新の市場洞察がなければ、あなたのトレード戦略は純粋な推測になります。

タイミングとはすべてである。暗号通貨市場は伝統的な市場よりもより積極的に動くため、一つの遅い取引が利益を失うことになる。成功するトレーダーは即時で実行可能なデータに頼っている。

Edgen RadarリアルタイムAI分析を提供し、ブロックチェーン上の洞察、ソーシャルセンチメントの追跡、強力なアルファシグナルを統合しており、すべてが1つのプラットフォームで明確に表示されています。

仮定や推測は不要。迷いはなし。リアルタイム取引の明確さ。

リアルタイム市場インサイト:なぜそれが重要なのか

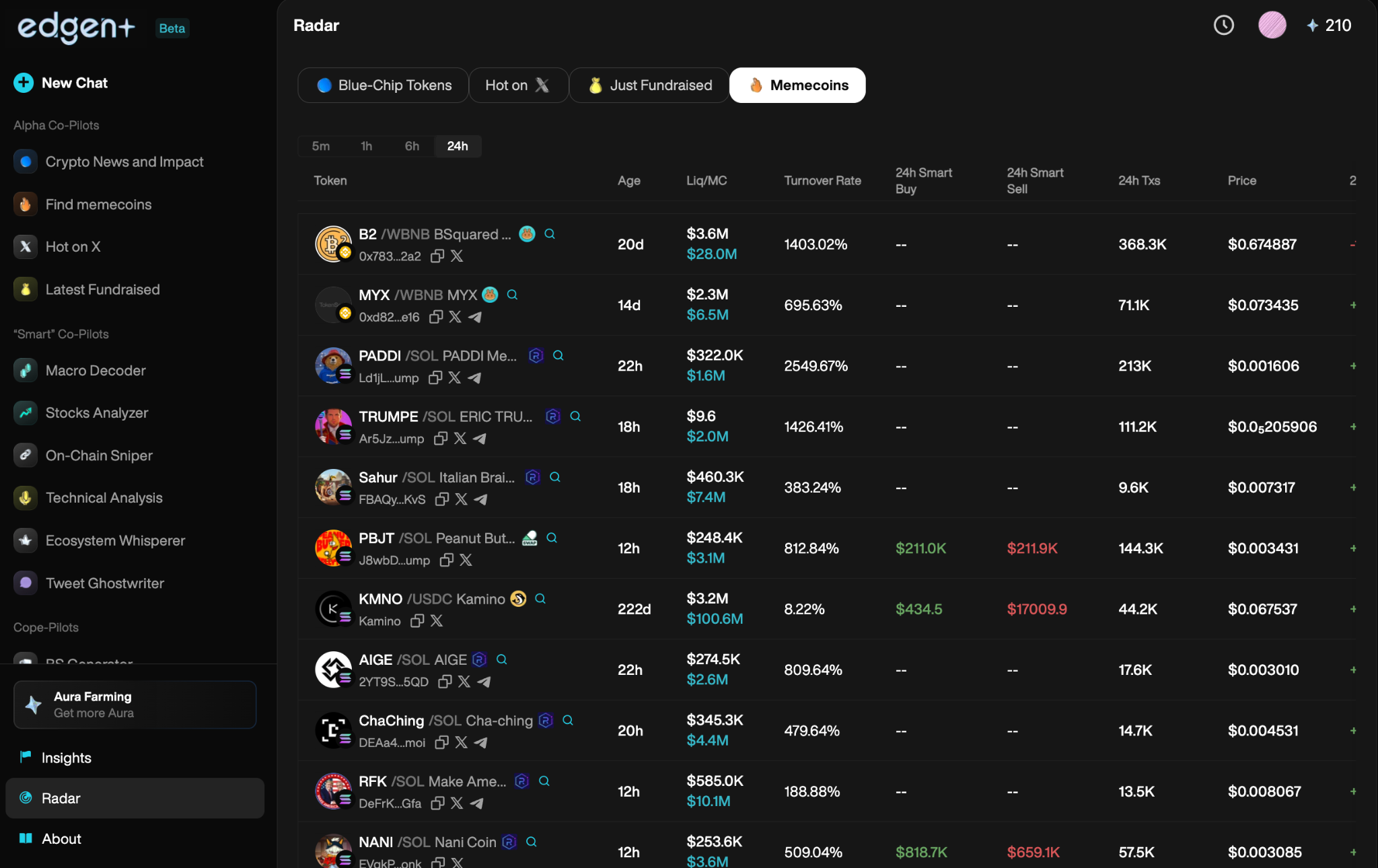

リアルタイムのシグナルによる暗号通貨取引

チャートはもはや全体の物語を伝えられなくなっている。市場の牽引要因が変わった。

- ソーシャルメディアの盛り上がり

- ホエールウォレットの移動

- オフチェーン取引

リアルタイムのインサイトにより、市場の動向を即座に把握し、市場状況が変化する前に利益を上げる取引が可能になります。

伝統的な投資家は過去のトレンドに頼るが、暗号通貨は現在を正確に読み取る者に報酬を与える。

トレーディング・ブラインドとはお金の損失を意味する

遅延したデータですか?あなたは最適なエントリーやエグジットのポイントを失います。

古くなったシグナルですか?あなたは遅れて取引することになります。

偽りのブームに陥りますか?あなたはその代償を払うことになります。

リアルタイムのインサイトにより、よりスマートな対応、迅速な反応、一貫した収益性が可能になります。

エッジンAIラジオがトレーダーに究極の優位性を提供する方法

Edgen Radar高度なAI、詳細なブロックチェーン分析、正確なソーシャルセンチメント分析を統合したパワフルなリアルタイム取引ツールです。ミシガン経済学ジャーナルが指摘したように、 AI is transforming financial markets by enhancing speed, efficiency, and precision in trading and market prediction.LSA Technology Services

キーフィーチャー:

- AIを駆動する市場分析:膨大なデータセットを即座にスキャンし、重要なトレンドを特定し、実行可能なインサイトを提供します。

- オンチェーン追跡機能:ウォールレットのアクティビティ、流動性の変化、重要なトークンの移動に関する即時アラート。

- ソーシャルセンチメントスキャナー:インフルエンサーやKOL、トレンドに乗っているコインのリアルタイムモニタリング。

- アルファシグナル検出:AIが選別した取引シグナルで、価格上昇前に過小評価された資産を発見する。

- 即時通知:主要な市場動向が起こる前にリアルタイムでアラートを提供します。

アルファ・シグナル:インサイダーのように市場を見る

アルファシグナルの定義

アルファ信号は、大勢がそれに気付く前に市場の変化を明確に示す、収益性の高い取引の早期指標を提供します。

エッジンAIのアルファアドバンテージ:

- 市場のノイズをフィルタリングし、収益性のある機会を正確に特定します。

- 上昇する社会的な注目を早期にキャプチャします。

- クジラの蓄積および分布のシグナルを迅速に検出します。

推測をやめよう。アルファシグナルを使って自信を持って取引しよう。

リアルタイムのインサイトが必須である理由、而不是望むものではない理由

彼らなしでの取引のリスク:

- 遅延したエントリーよって利益を生む取引を完全に見逃す。

- 操作された市場の過剰な宣伝に巻き込まれる。

- 能動的に取引するのではなく、常に反応的に行動することにより、利益を失うことになる。

エッジンAIは明確な利点を提供しています:

- 市場の予見: 価格に反映される前に市場の動きを知る。

- 正確な実行:AIによるインサイトにより、自信を持って意思決定できます。

- 初期の優位性:主流トレーダーが反応する前に大きな価格変動をキャプチャする。

リアルタイムデータはプロレベルの取引に等しい。それがない限り、成功は手の届かないものである。

AIとリアルタイムデータ:トレーディングの革命はすでに到来している

市場は日々、よりスマートで、柔軟で、競争力のあるものになっていく。成功するトレーダーはAIを活用したツールを活用して、自身の優位性を維持している。

エッジン・ラダーラはこのエッジを明確に伝えます。

エッジン・ラダールのトレーディングの未来へのビジョン

将来的な取引は、伝統的な指標や静的なチャートを越えていく。AI駆動の分析、即時のデータ追跡、自動実行が取引を定義するだろう。

はっきりと見ることを想像してください:

- AIによって、すべての重要な市場動向は即座に特定される。

- トークンが急騰する前に早期に発見された。

- ソーシャルセンチメントおよびブロックチェーン活動に基づくリアルタイム通知。

Edgen AIはまさにこの未来を構築しており、Edgen Radarを使用するトレーダーはその一部になります。

貿易。迅速に行動せよ。常に勝利せよ。

トレードをレベルアップしましょう。試してみてくださいEdgen Radar 今日。

投資、もうひとりじゃない

Ed を無料で試そう。クレカ不要、縛りなし