Aura 101: Piyasa İçgörülerinizi Nasıl Etki ve Ödüllere Dönüştürürsünüz?

TLDR

- Aura, Edgen içinde anlamlı eylemler (görevler, abonelikler ve yönlendirmeler) tamamlanarak kazanılır.

- Krediler, Edgen'in yapay zeka özelliklerine güç verir – piyasa zekası, raporlar, uyarılar.

- Yüksek Aura puanları, erken erişim özelliklerini, özel ödülleri ve liderlik tablosu statüsünü açar.

- Çarpanlar (100 kata kadar), plan seviyenize göre kazanma hızınızı artırır.

Aura Nedir?

Edgen'in Aura'sı size Edgen içinde gerçek, pratik avantajlar sunar.

Aura puanınız arttıkça, erken özellik yayınlarına, özel beta programlarına ve gelecekteki etkinliklerle bağlantılı potansiyel ödüllere erişim kazanırsınız.

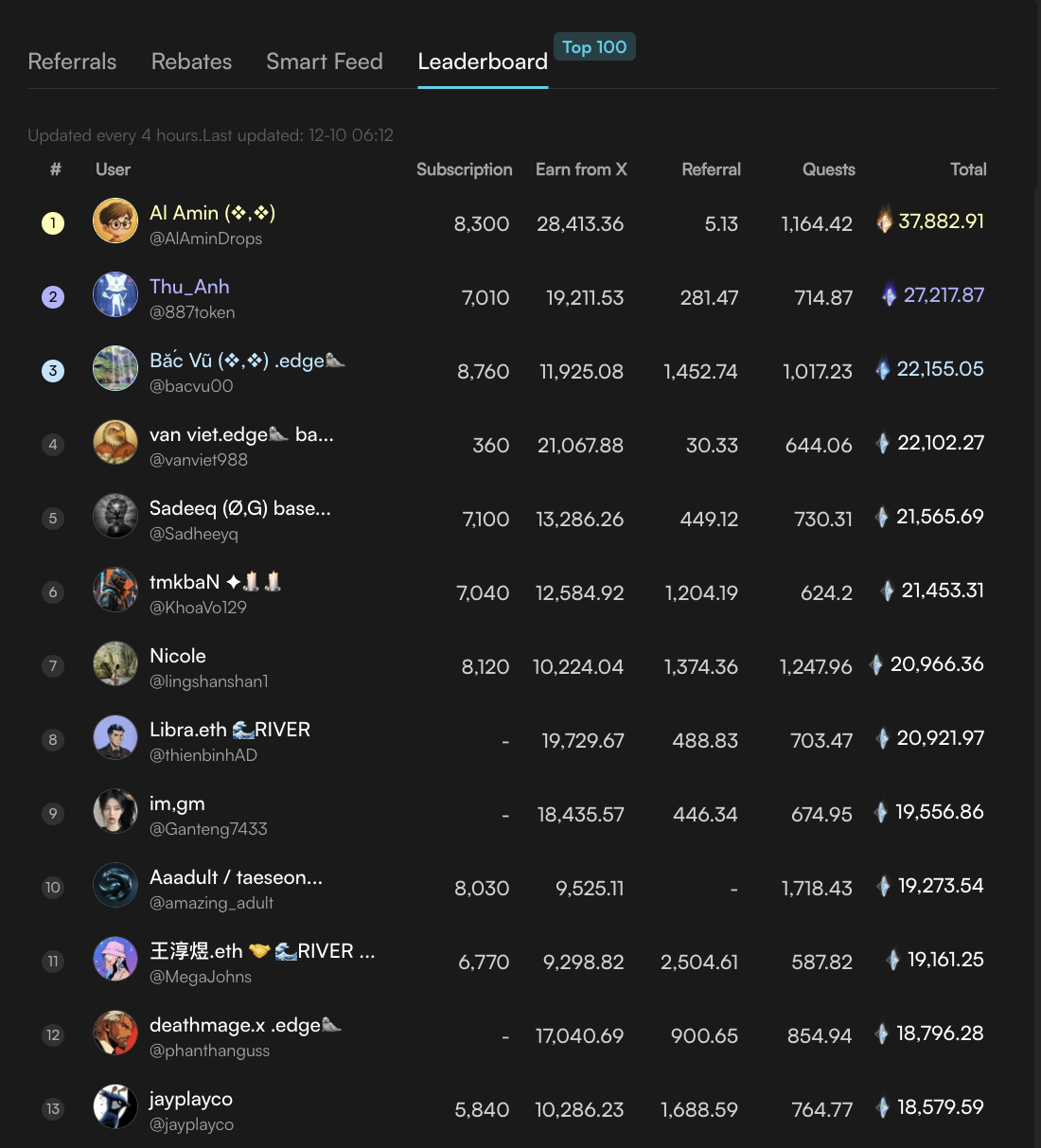

Aura'nın bir liderlik tablosu vardır. Buraya tırmanmak sizi farklı bir tüccar sınıfına sokar. Ne kadar yükselirseniz, o kadar özel ödüllere, benzersiz ayrıcalıklara ve başkalarının göremeyeceği erişime yaklaşırsınız.

Aura ayrıca diğer tüccarların topluluğa olan bağlılığınızı fark etmelerine yardımcı olur. Basitçe söylemek gerekirse, Aura, Edgen'deki varlığınızı kalıcı bir değere dönüştürür.

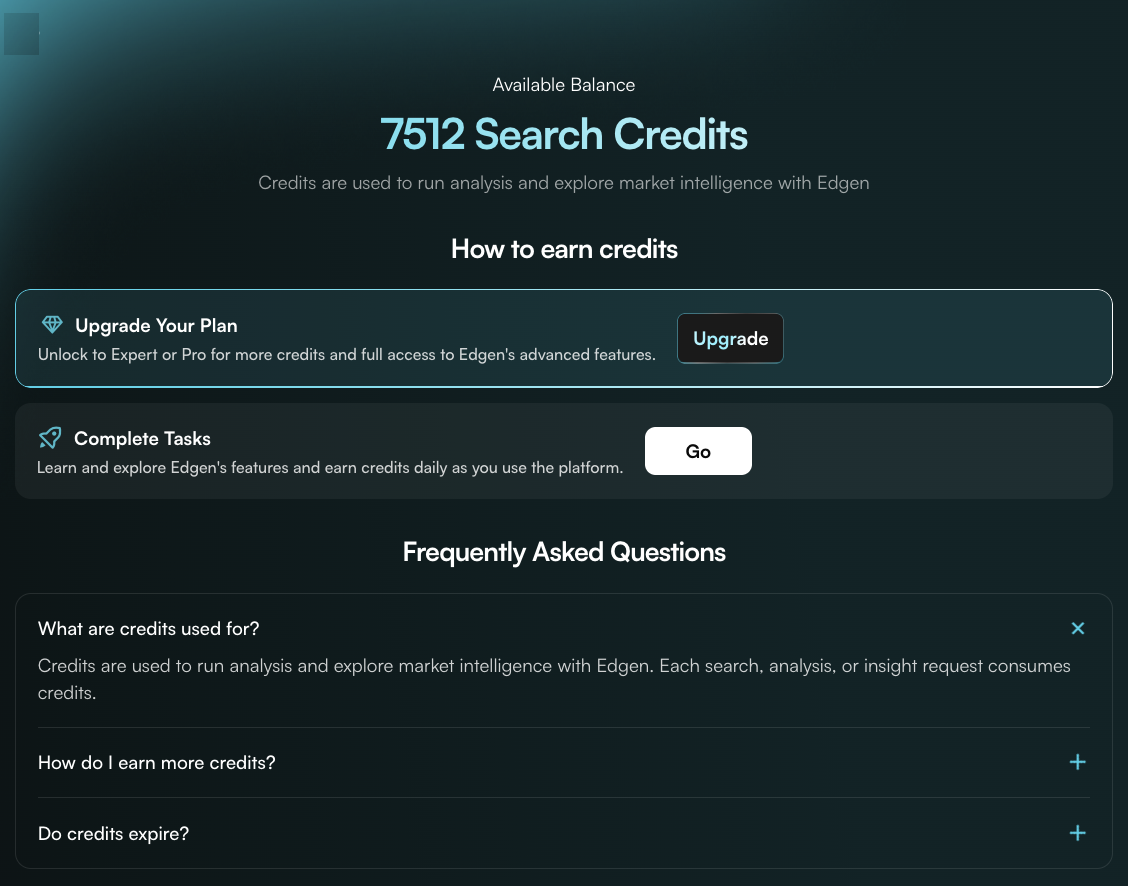

Krediler Nedir?

Krediler, Edgen'in yapay zekasını nasıl kullandığınızdır.

Piyasa zekası, portföy ve 360º raporları, akıllı uyarıların tümü Kredilerle desteklenir. Bunları Edgen araçlarınız için yakıt olarak düşünebilirsiniz.

Görev Merkezindeki görevleri tamamlayarak ücretsiz Kredi kazanabilir veya abonelik seviyeniz aracılığıyla daha fazlasını elde edebilirsiniz.

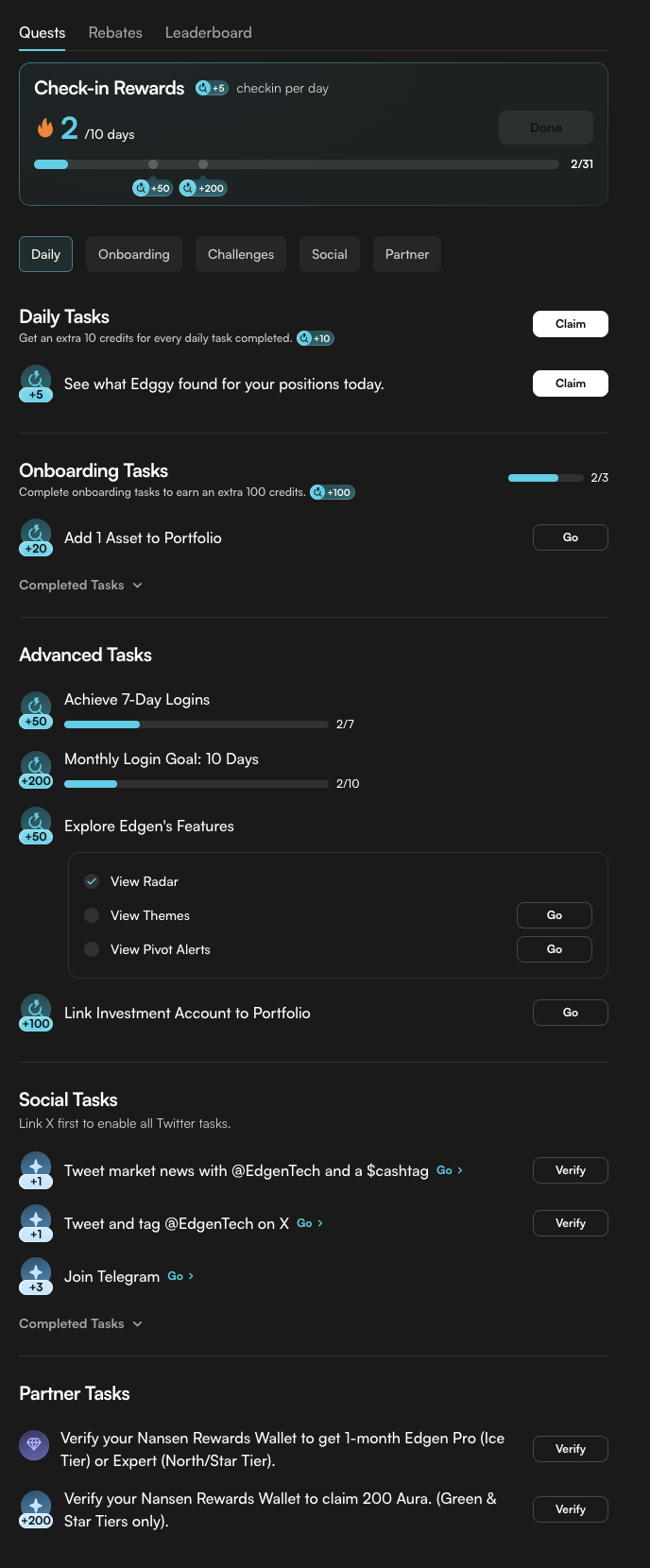

Görev Merkezi: Nasıl Kazanılır

Görev Merkezi, hem Aura hem de Kredi kazanmak için merkez noktanızdır.

5 görev türü vardır:

- Günlük: giriş yapın, ödülleri talep edin

- Başlangıç: Portföyünüzü kurun, piyasa avantajınızı keskinleştirin

- Zorluklar: kilometre taşlarına ulaşın, bonusları açın

- Sosyal: piyasa görüşlerinizi veya haberlerinizi paylaşın

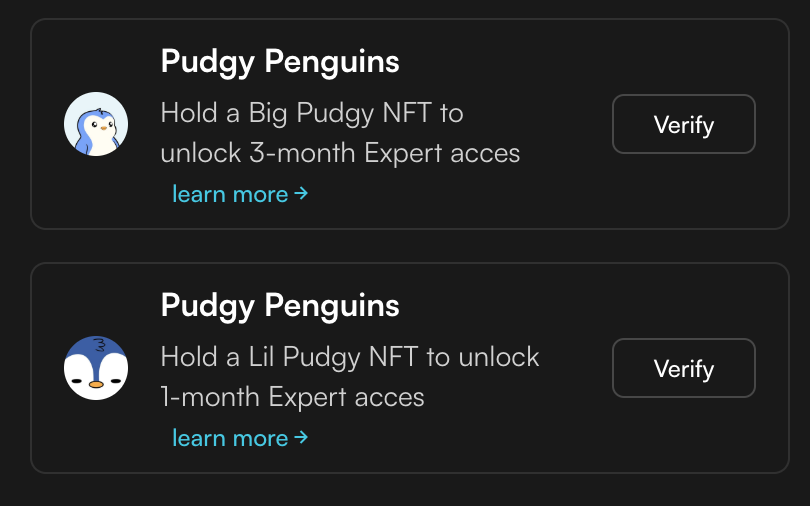

- Ortak: Nansen, Pudgy Penguins ve daha fazlası gibi projelerle sınırlı süreli işbirlikleri

Bazı görevler Kredi kazandırır. Bazı görevler Aura kazandırır.

Çarpanlar: Daha Hızlı Kazanın

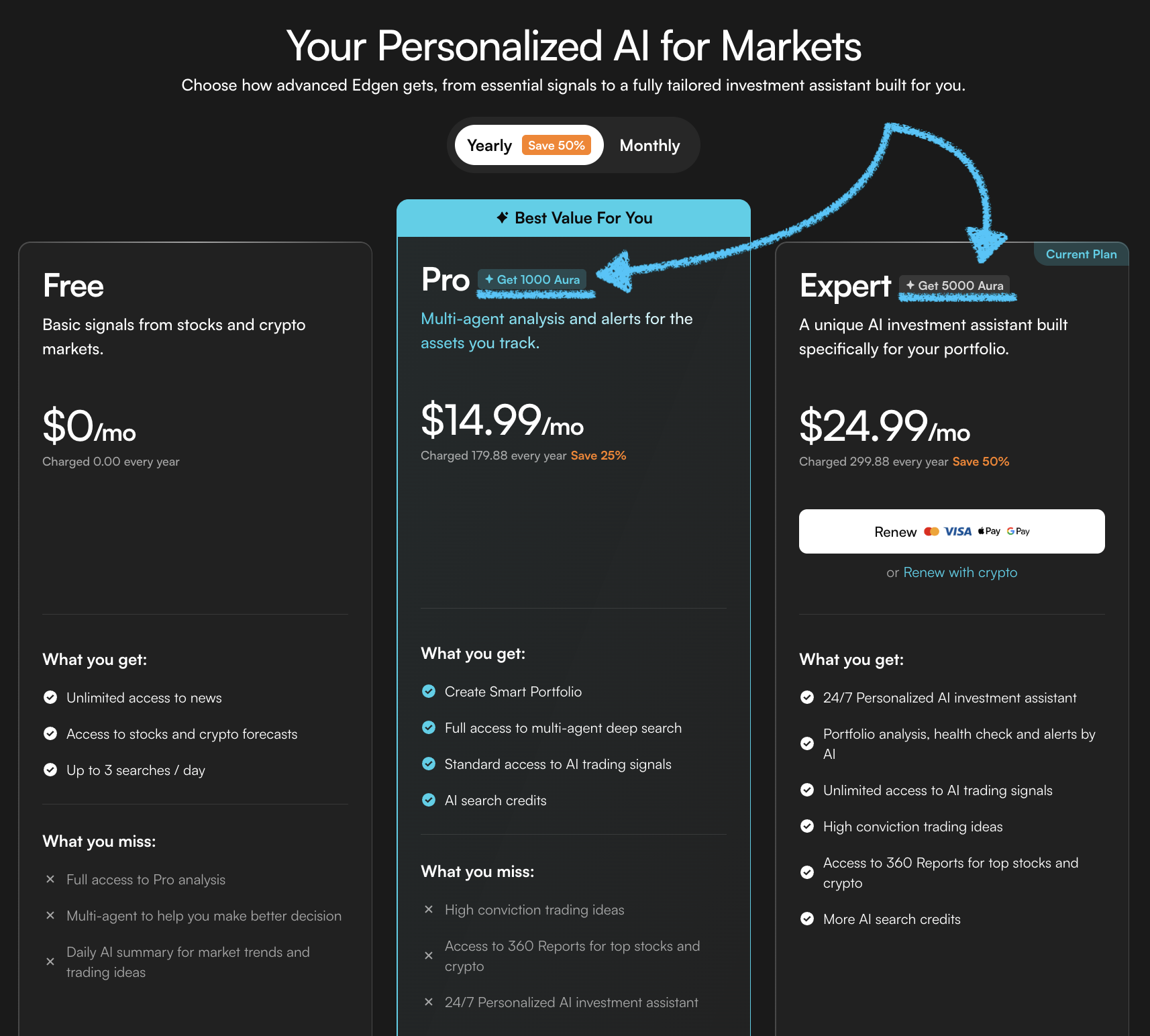

Plan seviyeniz ve süreniz (aylık/yıllık), görevlerden Aura kazanma hızınızı belirler:

- Ücretsiz = 1x

- Pro = 20-30x

- Expert = 80-100x

Aynı görevler, çok farklı ödüller.

Çarpanlar, görevlerden kazanılan Aura için geçerlidir, bu nedenle planınızı yükseltmek sadece özelliklerin kilidini açmakla kalmaz, aynı zamanda liderlik tablosundaki konumunuzu da hızlandırır.

Abonelik Aura'sı

Pro veya Expert'e abone olmak, Edgen'in yapay zeka araçlarına tam erişim sağlar. Ancak aboneliğiniz aynı zamanda Aura avantajları da getirir:

- Aboneliğiniz başladığında bir kerelik Aura bonusu alırsınız.

- Aboneliğiniz süresince, günlük girişler size her gün Aura kazandırır.

Bu istikrarlı ödüller, Aura puanınızı zamanla sürekli olarak artırmanıza yardımcı olur.

Yönlendirme Aura'sı

Arkadaşlarınızı Edgen'e katılmaya davet edin. Onlar kaydolup başlangıç eğitimini tamamladığında, ikiniz de Aura kazanırsınız.

Edgen, bonusunuzu maksimize etmek için hangi arkadaşlarınızı davet etmenizi önerir.

Yönlendirdiğiniz arkadaşlarınız Pro veya Expert abonesi olursa, geri ödemeler yoluyla aboneliklerinin bir kısmını da kazanabilirsiniz.

Ortak Görevler

Zaman zaman Edgen, güvenilir projelerle ortaklık kurarak sınırlı sayıda görevler yayınlar.

Ortak görevleri tamamlamak, ek Aura veya ücretsiz Expert erişimi gibi avantajlar kazandırır ve Edgen'e bağlı yeni araçları ve ekosistemleri keşfetmenizi sağlar.

Şimdi Başlayın

Aura bugün değerli faydalar sunuyor ve ekosistem genişledikçe önemi artacaktır.

Aura'nızı erken inşa etmek, gelecekteki fırsatlar için sizi güçlü bir konuma getirir.

Bugün başlayın: bir görevi tamamlayın, araçları keşfedin, ihtiyaçlarınıza uygunsa abone olun veya bir arkadaşınızı davet edin. Her eylem Aura'nızı artırır ve her puan Edgen içindeki kimliğinizin bir parçası olur.

Yatırım yapmak artık yalnız bir iş değil.

Ed'i ücretsiz dene. Kart yok, taahhüt yok.