アルファトレード:市場に打ち勝つ賢い方法

アルファトレーディングとは何か?

ほとんどの暗号通貨トレーダーは損失を被ります。なぜなら、彼らには「アルファ」と呼ばれる重要な優位性が欠けているからです。

アルファ取引は、市場のベンチマークを一貫して上回ることを意味します。これは、基本的なチャートやファンダメンタルズを越えたものです。現在の市場は、物語、データトレンド、および社会的勢いに従って動いています。

AIを駆動とするプラットフォームなどEdgen AI 膨大な市場データを即座に処理し、人間のトレーダーが見落とす隠れたパターンやアルファ信号を特定します。ブロックチェーン分析、ソーシャルセンチメント、そして高度なAIを組み合わせることで、Edgenは盲点を解消し、競争上の優位性を提供します。

トレーディングにおけるアルファの定義

アルファは、標準的な市場パフォーマンスを超えた収益を測定します。

例えば:

- 市場のベンチマークが7%上昇したが、あなたのポートフォリオが12%上昇した場合、アルファは+5%になります。

- 追加の5%は、より良い市場情報、迅速な対応、そして賢い意思決定から生じます。

その追加の5%は、より良い市場情報、迅速な対応、そして賢い意思決定から生じます。ポートフォリオパフォーマンスにおけるアルファの仕組みについてより詳細な概要が必要な場合は、以下のリンクを確認してください。Corporate Finance Institute’s explanation of alpha.

トレーダーが現在どのようにアルファを発見するか

アルファ信号は識別可能なソースから現れる:

- AI駆動型のインサイト:マシンは人間の能力を超えて膨大なデータセットを分析する。

- ソーシャルセンチメントトラッキング:市場の動きはしばしばソーシャルメディアに駆け引きされた物語に従う。

- オンチェーン分析:重要なウォレット活動は、潜在的な変化を示している。

- 迅速な市場対応:ボラティリティの高い市場において、利益は素早い反応で決まる。

伝統的な取引方法では、完全な可視性が得られません。プラットフォームなど likeEdgen AIリアルタイムのアルファ信号を明らかにし、トレーダーが先手を打つことを可能にする。

AIがアルファトレーディングをどのように変えるか

AIはもはや取引の未来を表すものではなく、現在では市場の成功を定義している。

AI取引の利点:

- 即時データ処理: AIは大規模なデータセットを評価し、即時に処理します。

- 初期パターン検出:AIは人間のトレーダーよりも前にトレンドを認識します。

- 感情を排除したトレード:パニック売りや衝動的な買いを排除します。

- リアルタイム・アルファ検出:一般の認識よりも早く隠れた機会を発見します。

エッジンAIは、アルファトレーディング向けに特化したツールを提供しています:

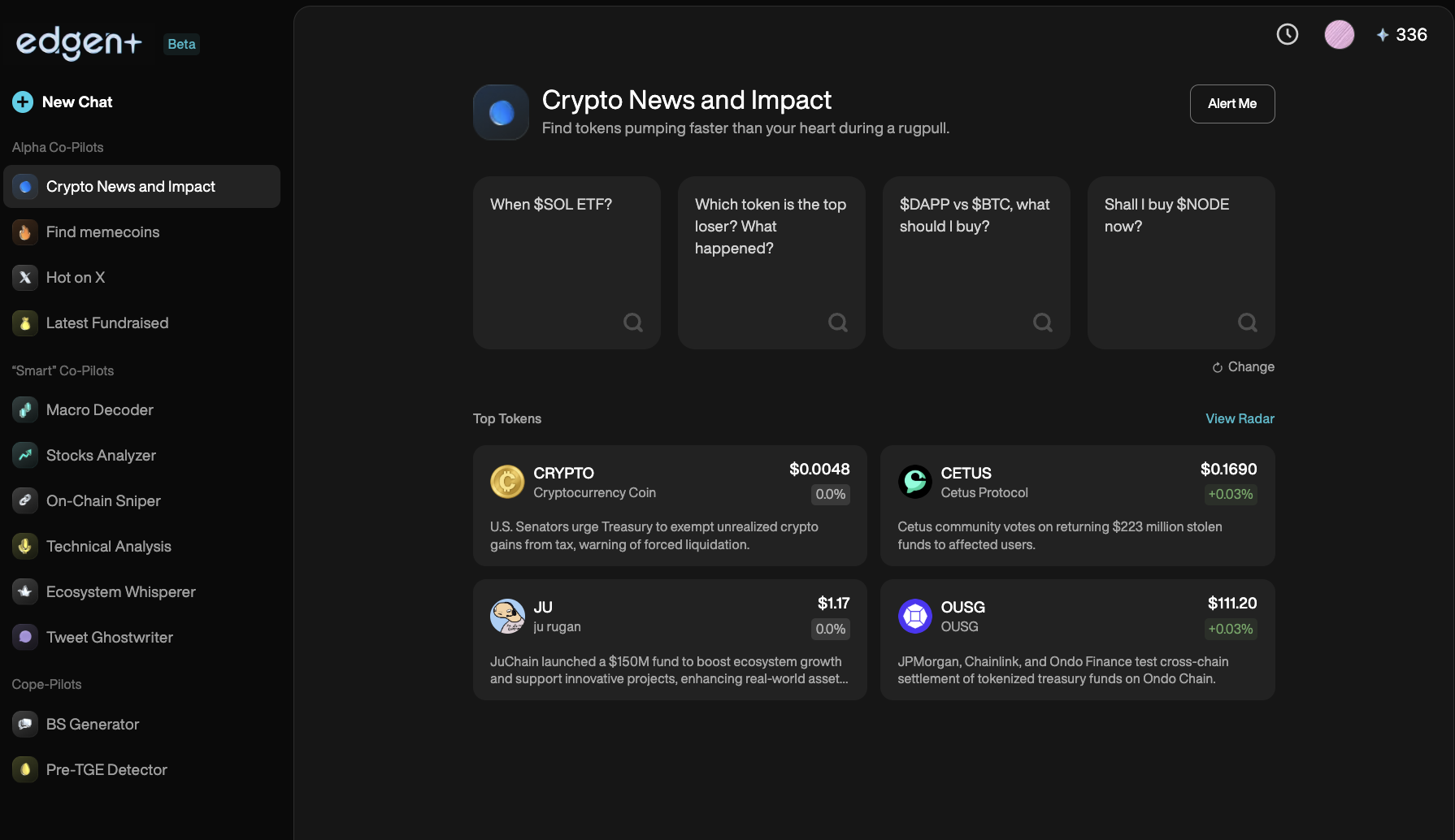

- Edgen Radar: 実時間での市場の感情、価格の変動、およびアルファ信号を表示します。

- Edgen Search: 検証されたデータを使用して、詳細な市場に関する質問に答え、ノイズを排除します。

- Edgen Insights: トレーダーが即座に洞察を共有できる協力的なハブを提供します。

AIなしでのトレーディングは市場の可視性を大きく制限します。Edgen AIは、他の人が見落とすものをトレーダーが見えるようにします。

アルファ・シグナル・トレーディング:勝ちトレードの見つけ方

アルファ信号は、利益をもたらす取引の早期の兆しを提供します。

アルファシグナルの例:

- 急な価格変動:急激な上昇または下落は、アクションポイントを示します。

- ボリューム急増:高い取引活動は機会を示しています。

- オンチェーン活動:ウォーリアーウォレットおよび影響力のあるウォレットの動きは、市場の動向を予測する。

- ソーシャルセンチメント:コミュニティの盛り上がりが暗号通貨価格の急騰を予測する。

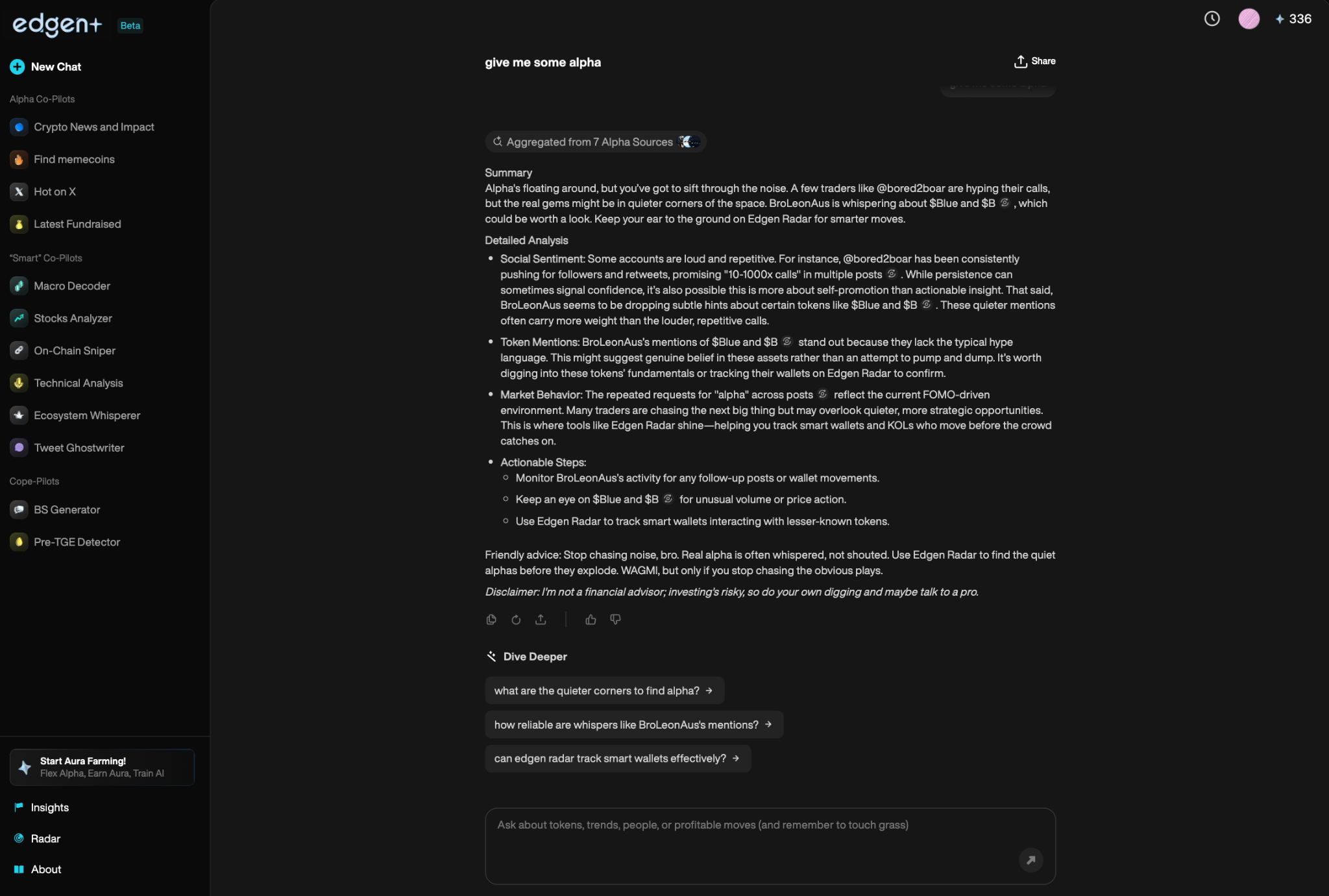

Edgen Radarこれらの信号を即座に特定し、ながらもEdgen Search影響力のあるトレーダーとトレンド話題を追跡し、トレーダーが先に行動できるようにします。

アルファ取引のための最適な戦略とは何かが定義されている

利益を上げるために、検証されたアルファ戦略に従ってください:

1. テンダーフォローアイテム

市場の強いトレンドを早期に特定する。適切なエントリーやエグジットのためにAIアラームを使用する。

2. 平均回帰

トレードが過熱した買われすぎまたは売られすぎの状態を適正価値に戻して特定しました。AIは最適なトレードタイミングを特定します。

3. スマート・アービトラージュ

エクスチェンジ間の価格差を即座にキャプチャする。AIボットが効率的に実行を自動化する。

エッジンAIは、これらの戦略を正確に実行するための専門的なツールを開発しています。

アルファ取引におけるブロックチェーンデータの重要性

ブロックチェーン取引は、重要なトレーディングシグナルを明らかにするインサイトを提供します:

- スマートウォレットの動き:メジャーウォレットが暗号通貨市場価格に影響を与える。

- スマートコントラクトの活動:DeFiのトレンドはアクティブなdAppsから現れる。

- 流動性の流れ:取引所への資金の流入・流出は、今後の市場の変化を示唆している。

Edgen Radarリアルタイムなブロックチェーンの洞察を提供し、他の人よりも先に取引者が迅速に対応できるようにします。

一般的なトレーダーのミスの説明(そしてその回避方法)

- ミス:計画なしでの取引

解決策:取引を開始する前にエントリーポイントとエグジットポイントを定義してください。

- ミス:ソーシャルおよびブロックチェーンデータを無視すること。

解決策:現在の市場は、物語とブロックチェーン上の活動によって駆動されていることを認識する。

- ミス:FOMO(後悔の感情)による過度な取引

解決策:質を量よりも優先する。AIは感情的なバイアスを除去するのを手伝う。

- ミス:通常の小口投資家のように取引すること。

解決策:決定的な優位性を得るために、AI、ブロックチェーン分析および自動化ツールを使用してください。

アルファ取引とAIの未来

トレーディング戦略はAI、ブロックチェーン分析、ソーシャルインテリジェンスへとシフトした。

アルファトレーディングの今後の展開:

- AIの優位性:マシンは人間よりも取引を予測し、実行する能力が優れている。

- ブロックチェーン分析:オンチェーンデータが標準的な市場分析となる。

- ソーシャルインテリジェンス:感情を新たな基本指標として捉える。

エッジンAIはこの変化をリードし、ブロックチェーンの洞察、ソーシャルセンチメント、そしてAI駆動型の戦略をシームレスに統合しています。

トレーダーが先んじて行動する方法

アルファ取引で成功するトレーダーは常に次のゴールドルールに従っています:

- 使用するEdgen Radar、Edgen Search、およびEdgen Feed正確な洞察を得るために。

- ブロックチェーンの活動をモニタリングし、特にワイルドウォレットの動きを注視する。

- ソーシャルセンチメントのトレンドを追跡し、過熱が市場を決定的に動かすことを考慮する。

- データ駆動型のAIシグナルに厳密に従って、感情的な取引を避ける。

- 柔軟に対応し続けること; マーケットの動態は常に変化し続けている。

最も優れたトレーダーは、他の人が従う前に市場の動きを予測する。

投資、もうひとりじゃない

Ed を無料で試そう。クレカ不要、縛りなし