迷因幣、替代幣與股票:為何AI是掌握市場趨勢的關鍵

市場已經改變。永遠地。

資金流動迅速。市場移動更快。

投資已超越了走勢圖、資產負債表和基本分析。迷因幣、替代幣和股票現在也跟隨社群熱潮、意見領袖的情緒以及即時區塊鏈活動。

AI 是這項變化的驅動引擎,引導交易者做出更智慧的決策、更明確的預測和更快的行動。Edgen AI將這個新的市場力量稱為「Pumpamentals」,即社會動能、影響者權力與社群驅動的價格走勢的交叉點。

沒有AI的交易等於錯過別人清楚看到的訊號。AI交易定義了市場的成功。

迷因幣、替代幣與股票解析

meme幣:帶有 Serious 利潤的玩笑

meme幣最開始只是網際網路的玩笑:狗狗幣(DOGE)、柴犬幣(SHIB)、佩佩幣(PEPE)。這些資產缺乏傳統金融的實力,卻因社會關注與病毒式傳播的迷因而迅速上漲。

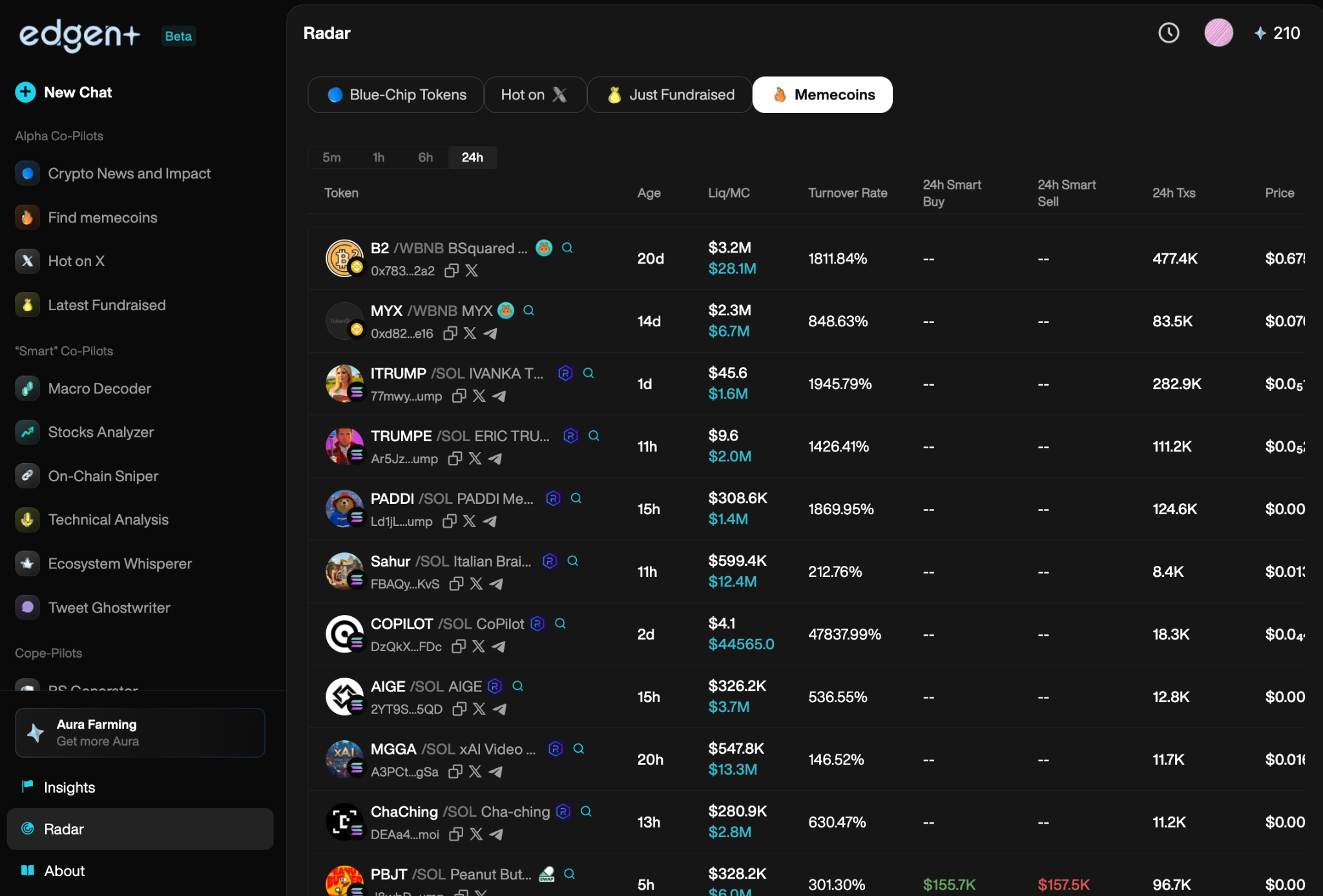

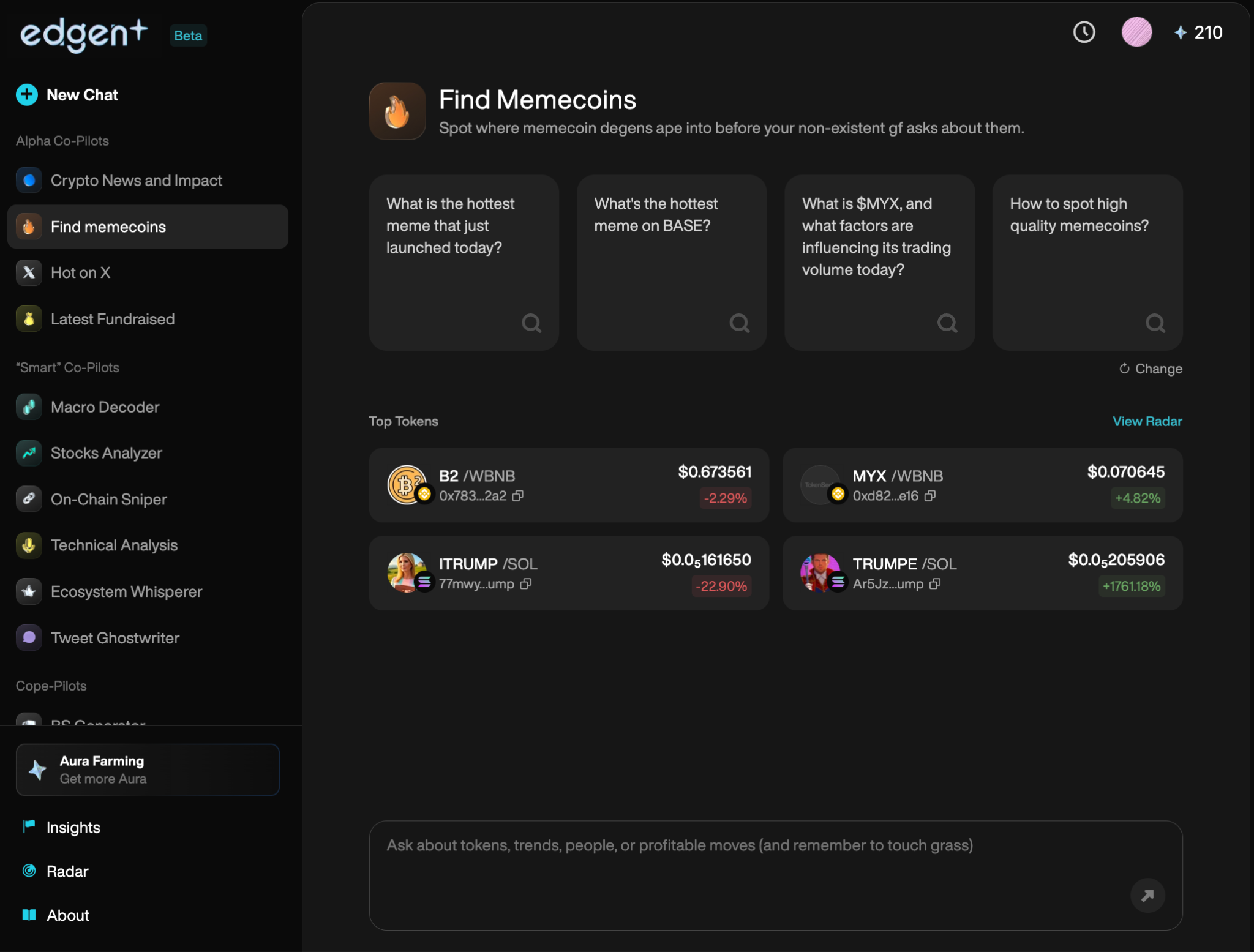

Memecoin 價格快速上漲並暴跌。Edgen AI追蹤 Twitter 的情緒、社群互動及影響者動向,在市場炒作發生前進行識別。

其他加密貨幣:不只是比特幣的替代品

其他加密貨幣(Altcoins)指的是除了比特幣以外的加密貨幣,包括以太坊(ETH)、索拉納(SOL)以及專注於人工智慧的代幣。 Learn more about altcoins, their types, and how they differ from Bitcoin與迷因幣不同,替代幣通常提供明確的使用場景、功能或實體價值。

Edgen AI 跟蹤代幣市場訊號、鏈上錢包動態和社群情緒變動,以早期識別交易機會。

股票:傳統資產的演進

股票代表蘋果、特斯拉和亞馬遜等大型公司的股份。雖然傳統的投資規則仍然適用,但人工智能改變了股市投資。現在公司使用由人工智能驅動的平台,即時分析收益報告、新聞頭條和投資者情緒,使得人工智能驅動的交易變得不可或缺。

AI 如何定義現代市場趨勢

AI 即時預測市場情緒

投資者情緒決定資產價格。Edgen AI 掃描社交媒體(Twitter/X)和區塊鏈數據,於市場情緒出現變化時率先識別。

- 即時追蹤影響者與社群情緒。

- 預測市場波動前的敘事轉變。

以AI掌握鏈上資料

鏈上分析能揭示隱藏的市場訊號,如錢包活動、資金流動和智能資金行為。Edgen AI 能清晰解讀區塊鏈數據,在大多數交易員注意到之前提供即時警示。

Edgen AI 發現一個主要錢包正在累積一種低市值的替代幣。使用 Edgen 的 Radar 的交易者會立即收到通知,從而捕捉早期利潤。

Alpha 優勢:AI 的終極優勢

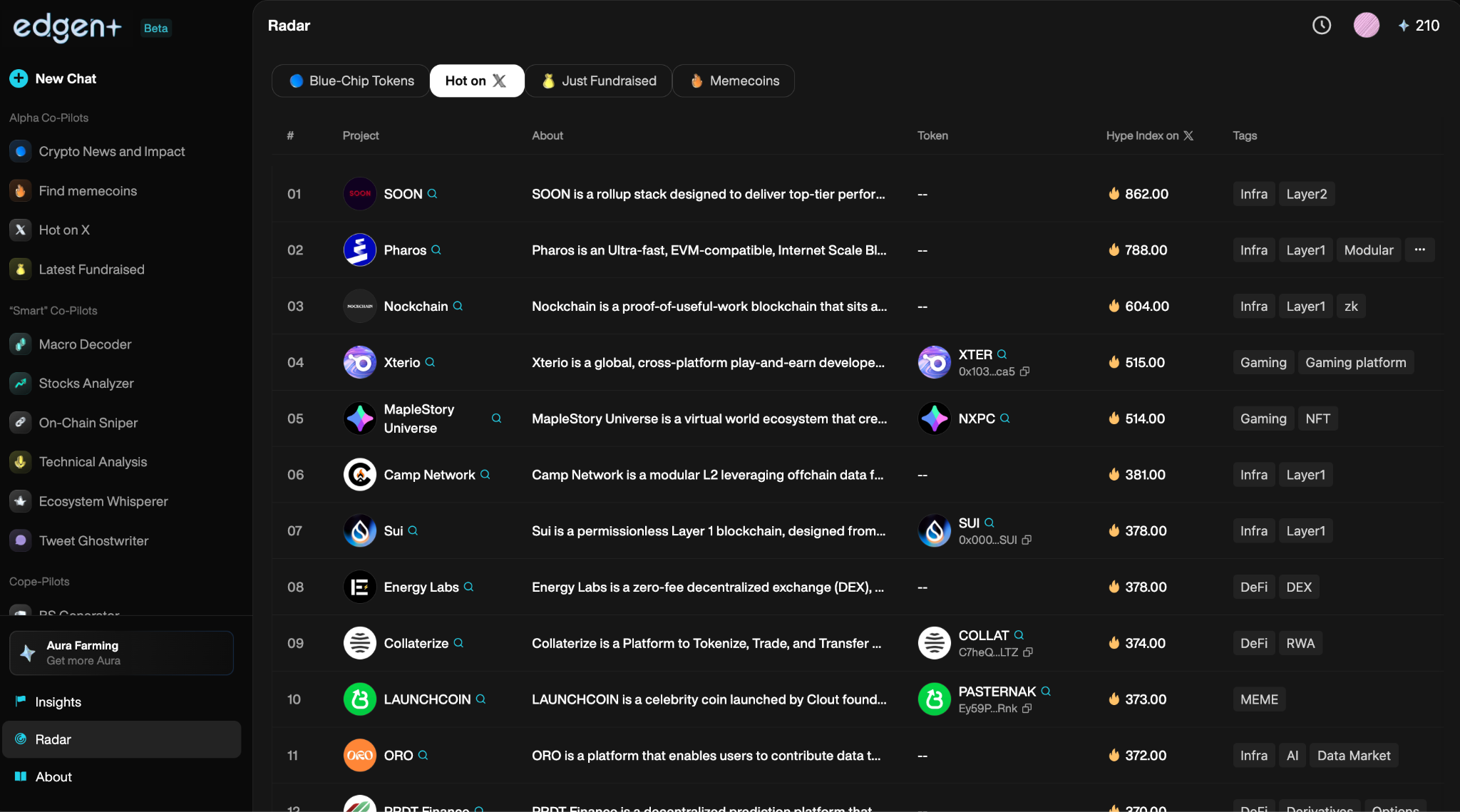

Alpha信號突出具有增長潛力的被低估資產。Edgen AI 可即時處理大量數據,迅速揭示突破性指標。通過運行即時查詢來探索隱藏的Alpha。 Edgen Search交易員使用的AI驅動搜尋引擎。

- 增加的開發者活動

- 增加的代幣持有者數量

- 日益增加的社會媒體提及

AI在價格反映這些機會之前就已識別出來。

AI驅動的加密貨幣與股票交易演算法

AI交易機器人:新常態

人工智慧交易更快、更聰明,且沒有情緒。

AI 嚴謹、無情緒且以驚人的速度進行交易。高頻率交易(HFT)機器人能在毫秒內完成交易,超越人類的處理能力。

Edgen Radar專注於快速交易執行、即時alpha識別與全面的市場洞察。

人工智慧與社會共識的結合

單純的技術分析是不夠的。Edgen AI 結合社會情緒與社群敘事,以捕捉市場的集體心態:

- 智慧錢包的動作(買/賣操作)

- 關鍵意見領袖(KOL)活動

- Twitter/X上的熱門話題與意見領袖動態

AI比人類更快偵測社會情緒

社會動能、意見領袖趨勢與社群互動驅動價格一夜之間變動。Edgen AI 持續監測並明確評估這些訊號。即時監控市場談話與社群資訊。 Edgen Feed:

- 看漲信號:病毒式互動、受關注的影響者人數增加、巨鯨買入

- 看跌警告:社會關注度下降、敘事轉變、參與度減弱。

AI首先捕捉情緒變動,使交易員能在市場反應之前做出果斷的交易。

AI在未來市場趨勢中的關鍵角色

AI + DeFi:市場的新邊疆

DeFi持續革新金融體系,而AI加速其成長。

Edgen AI 進化為完整的買方交易基礎設施:

- 自動化借貸策略。

- 主動管理DeFi中的風險。

- 最大化收益挖礦的收益。

僅靠人工分析無法與DeFi的規模相比。AI現在正領先進軍。

區塊鏈與人工智慧:一種強大的交易合作關係

結合人工智慧與區塊鏈技術,大幅提升了市場的透明度和效率:

- AI審計智慧合約以尋找潛在漏洞。

- 預測最佳手續費與交易時機。

- 提升DEX分析以實現更佳的交易執行。

AI與區塊鏈共同形成強大的交易環境。

為何AI對交易員現在至關重要

AI成為不可或缺的一部分,塑造了交易成功的未來。

交易員需要人工智慧的原因是:

- 更快的決策:即時處理數百萬個數據點。

- 優越的準確性:AI 消除人類的情感偏見。

- 持續監控:AI 提供持續的市場監測。

- 即時alpha洞察:AI能清晰追蹤即時情緒與鏈上活動。

沒有AI的交易會讓投資者處於嚴重不利的地位。

智慧交易,否則將落後於人

市場已經永久性地轉變。 meme幣、替代幣和股票高度依賴AI驅動的洞察、社會敘事和即時分析。

忽略AI的交易者會遇到困難。那些採用Edgen AI等平台的交易者,能運用社群情緒、alpha偵測與區塊鏈分析,遠遠領先於他人。

未來來臨了。AI驅動的交易決定了勝負。你的行動定義了你的市場地位。 Learn more about Edgen AI請將以下英文翻譯成繁體中文。保持結構和技術術語準確。避免過度翻譯。

投資這事,終於不用一個人了

免費試用 Ed。不用信用卡,不綁約