Edgen Radar を使用して AI で収益性の高い仮想通貨取引機会を特定する方法

暗号通貨取引の未来: AIがゲームをどのように変革しているか

暗号通貨取引はワープ速度で進み、従来の方法では対応できない。

エンターアイ:市場をうまく乗り切るためのあなたの最良の相棒。プラットフォームは次の通りです。Edgen Radar人工知能を活用して、収益性の高い暗号通貨トレード機会を迅速に特定し、オフチェーンデータ、ソーシャルセンチメント、AI駆動の分析を1つのシームレスなインターフェースに統合します。

この記事では、AIが暗号通貨取引戦略をどのように変革するかを説明し、特にどのようにしてそのような変革をもたらすかについてガイドします。 Edgen AIブロックチェーンのトレンドから実用的なインサイトを提供し、ソーシャル暗号通貨に関する正確な分析を通じて、トレーダーを強化します。ポンプメンタルズ。

1. アイ・エー・アイは暗号通貨取引においてなぜ不可欠なのか

暗号通貨は決してスリープ:価格は一瞬で変動し、すべての動きを手動で追跡するのは不可能である。だからこそ、AIを活用することは完全なゲームチェンジャーとなるのだ。

AIが取引意思決定をどのように向上させるか:

- AI-based sentiment analysis for crypto以下の英語を日本語に翻訳します。専門的な意味を保ち、書式を変更せず、過度な意訳は避けています:

:即座に暗号通貨のツイッター(X)、およびニュースフィードをスキャンし、トレンドとなるトークンやコミュニティを特定します。感情・感情の傾向 - Real-Time On-Chain Monitoring以下の英語を日本語に翻訳します。専門的な意味を保ち、書式を変更せず、過度な意訳は避けています:

:トークン価格に影響を与える前に、スパットホエール取引、流動性の変化、スマートウォレットの活動を監視します。 - Crypto Alpha Signal powered by Edgen AI以下の英語を日本語に翻訳します。専門的な意味を保ち、書式を変更せず、過度な意訳は避けています:

「:」価値が見直されている資産を特定し、他の人が気づく前にトレードの機会を知らせます。

エッジンは、暗号通貨分析、AI、ソーシャルメディアの洞察をユニークに統合することで、さらに一歩進んでおり、ゼロの盲点を確保しています。

2. 着実な仮想通貨取引のための強力なAI戦略

AIの力は、膨大なデータセットを迅速に選別し、パターンを認識し、正確で即座に戦略を立てることにあり、それは人間の能力をはるかに超えています。以下に、AIがどのようにしてあなたの暗号通貨取引のパフォーマンスを加速するかをお伝えします:

1. 感情分析:市場の過熱を活用して

暗号通貨市場は主にホットな話題や予測に基づいて動いている。AIを活用した感情分析は、以下を分析することで上昇相場または下落相場のトレンドを検出する:

- トークンの言及ツイッター(X)などのプラットフォームを通じて

- エンゲージメントメトリクススマートアカウントによるリツイート、コメント、フォローなど。

- インフルエンサーの意見キーパーソン(KOL)から。

Edgen Radarすぐにソーシャルでの注目を集めるトークンをマークし、収益性の高い動きに対して早期に立場を取るようになります。

2. オンチェーンデータのインサイト:スマートウォレット活動の読み取り

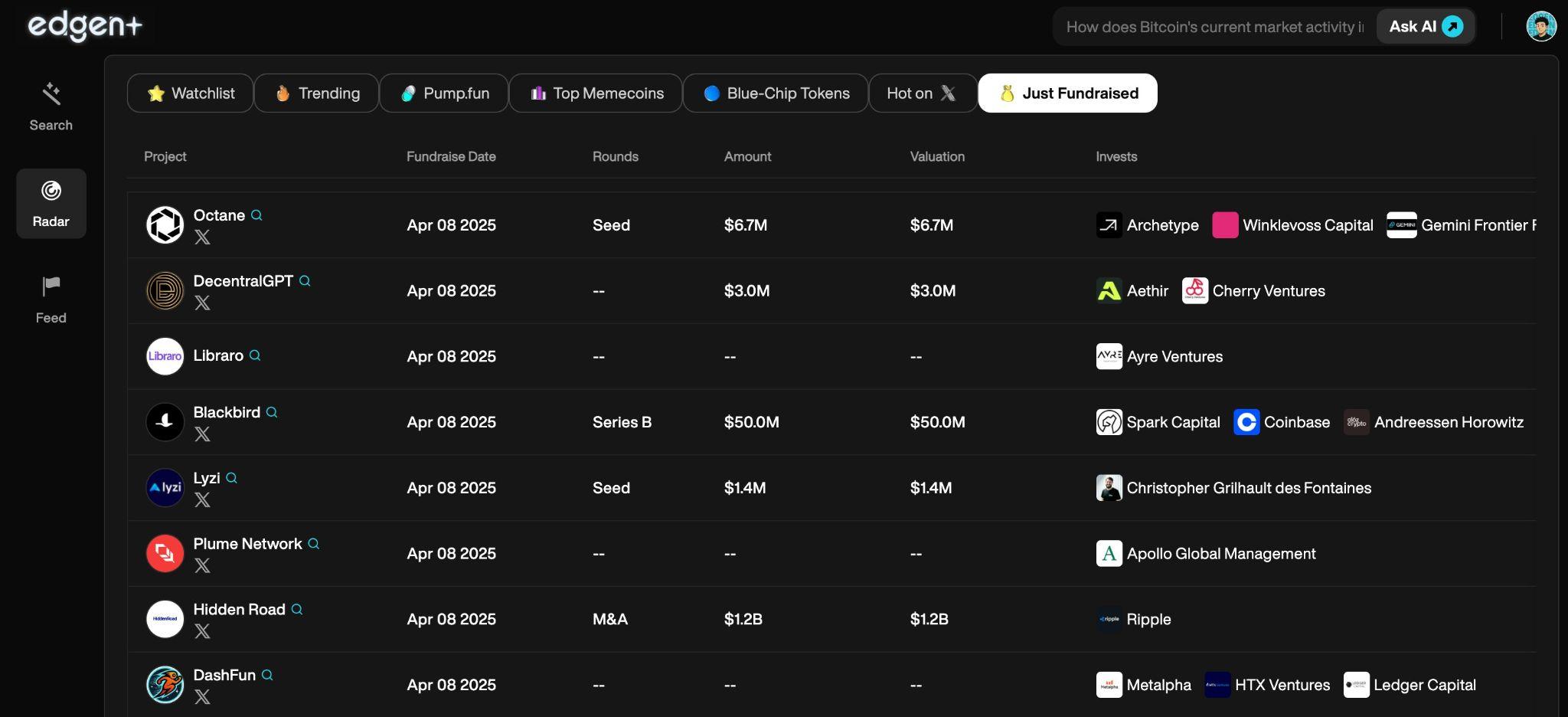

エッジンから提供されるAI駆動のブロックチェーン分析は、トレーダーに重要な市場の変化を強調することで支援します:

- クジラの行動:大規模なスマートウォレットの移動は、しばしば重要な価格変動を示唆することがある。

- 流動性フロー:中央取引所(CEX)および非中央集権型取引所(DEX)におけるトークンの移動を追跡する。

- スマートウォレットシグナル:DeFiプロトコル内のアクティビティ、ステーキングの行動、トークンのユーティリティ指標を追跡する。

エッジンの包括的なダッシュボードは、推測を必要としない明確でリアルタイムのブロックチェーンの洞察を提供します。

3. 技術的・基本分析:包括的なAI駆動のインサイト

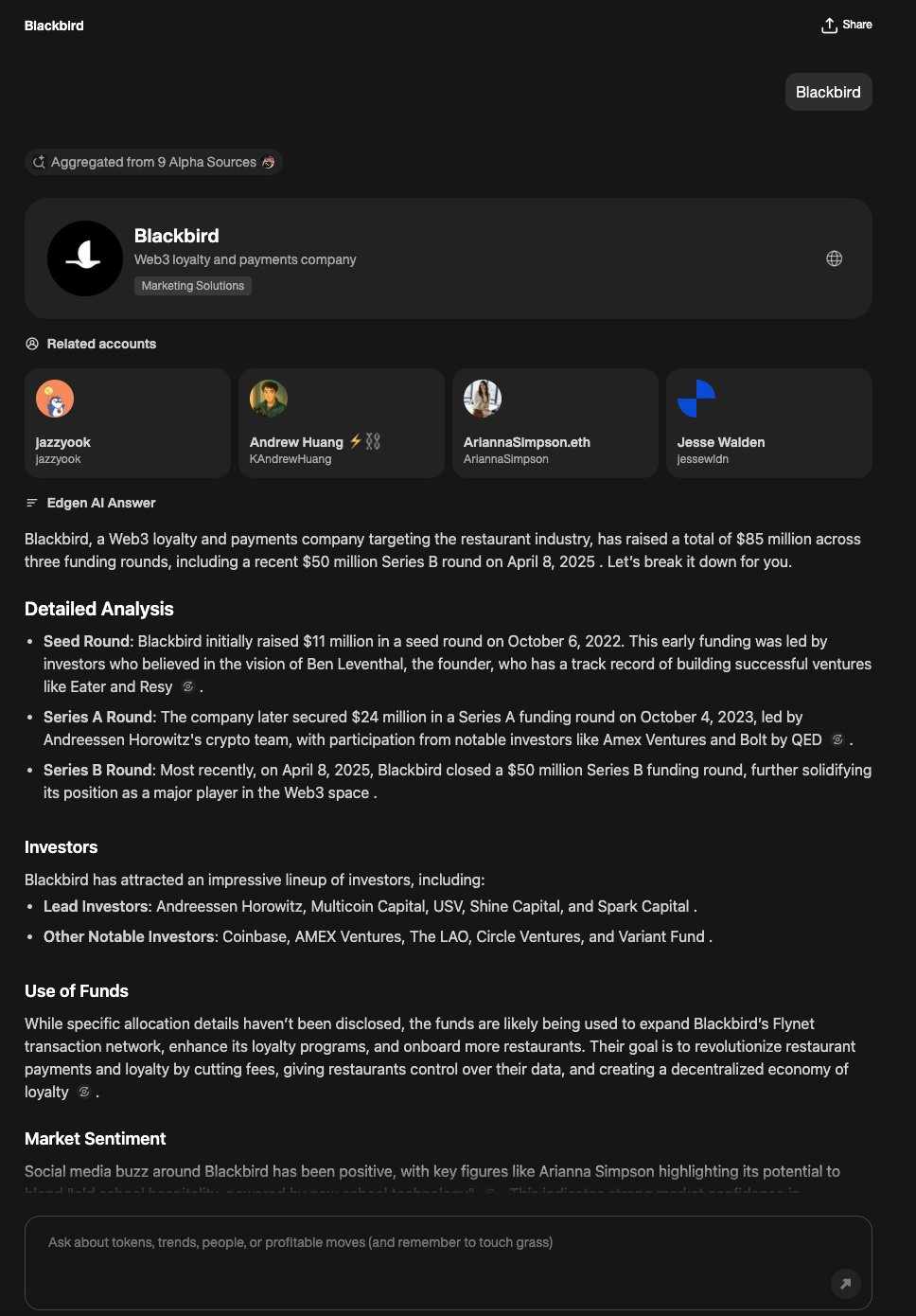

技術チャートパターン、オンチェーンデータ、ソーシャルセンチメントメトリクスを組み合わせ、Edgen AIの知能アルゴリズムは自動的に高く実行可能な取引機会を浮き彫りにします。手動でノイジーで断片的な市場データを整理する時間を無駄にすることなく、トレーダーはこれに頼ることができます。 Edgen Search’s AI-powered crypto trading engine数秒で迅速かつ正確でデータに基づいたインサイトを提供します。プラットフォームのLLM(大規模言語モデル)技術により、直感的な検索機能が可能となり、ユーザーは「どのトークンがホワイトの関心を獲得しているか?」や「今日はどのDeFiトークンがトレンドですか?」などの質問を入力し、即座で詳細な回答を得ることができます。これは、スピード、スケール、精度を重視したより知的な取引方法です。

3. アルファトレーディングとは:AIが隠れた機会を見つける方法

アルファとは何か?

アルファとは、それらが広く認識される前に、市場のベンチマークを常に上回る取引機会を発見することを指します。

エッジンAIがアルファ信号を識別する方法:

- スマートウォレットおよびホワイトの重要な動きをトラックする。

- ハイリスク・ハイリターンのトレードセットアップを強調しています。

- オフチェーンの基本的な要素をソーシャル駆動型の「に統合します。ポンプメンタルズ。

さらに、Edgen独自の「Aura(オーラ)」インセンティブシステムを導入し、ユーザーが自身の知見を共有することでエッジンのAIをトレーニングすることを促し、積極的な貢献に報酬を与え、プラットフォームの予測精度を継続的に向上させます。

4. コイン取引におけるEdgen AIの使い始め

AIを使って暗号通貨トレーディングをパワーアップする準備はできましたか?始め方をご覧ください:

- サインアップ:「プラットフォームに参加する」ようなものを翻訳すると、以下のようになります:

「〜のようなプラットフォームに参加してください」Edgen RadarそしてAI駆動型の市場インテリジェンスへのアクセスを提供します。 - リアルタイムデータをモニタリングする:Radarから直接、進行中のオンチェーンのトレンドや登場するソーシャルな感情を把握してください。

- バックテスト戦略:AIで駆動される歴史的市場分析を活用して、戦略をシミュレーションし最適化してください。

- リスク管理:リスク管理を常に保つために、ストップロスを設定し、ポートフォリオを多様化してください。

思い出してください。AIはあなたの戦略を補強しますが、規律あるトレーディングの原則を置き換えるものではありません。AIは強力ですが、賢い人間の監督が必要です。 Edgen連続的でリアルタイムのブロックチェーン上およびソーシャルモニタリングを統合することで、より安全で知的なトレード意思決定を可能にします。

ポイント:AIは暗号通貨取引の未来である

暗号通貨の急速に変化する世界において、AIはただ役立つだけでなく、必須です。With Edgen’s AI crypto toolsあなたは明確な優位性を得ます。正確なアルファ信号、リアルタイムデータ、そして市場のトレンドに先駆けて賢く取引するのに役立つソーシャルインテリジェンスが得られます。

ブロックチェーンや暗号通貨エコシステム、そしてAIなどの技術が金融イノベーションとどのように交差するかについてさらに深く掘り下げたい場合は、 MIT Digital Currency Initiative世界有数の学術機関の一つから、最先端の研究とリーダーシップをもつ考察を提供しています。

もっと賢く取引し、より頻繁に勝つ準備はできていますか? Start using Edgen today.

投資、もうひとりじゃない

Ed を無料で試そう。クレカ不要、縛りなし