Análisis de cripto en cadena: Cómo la IA ayuda a los traders a mantenerse al frente del mercado

Mercados Criptográficos Evolucionaron, el Análisis Tradicional Quedó Atrás

Los mercados criptográficos cambian rápidamente. Los métodos tradicionales de análisis no logran proporcionar insights precisos a tiempo. Para mantener una ventaja, los traders requieren analíticas en cadena y estrategias impulsadas por inteligencia artificial.

Edgen AIcombina las perspectivas de blockchain, la inteligencia artificial y las señales sociales en una solución clara. Al analizar datos en tiempo real, Edgen elimina puntos ciegos, permitiendo a los traders capturar movimientos rentables con anticipación.

A medida que la IA supera las capacidades humanas de procesamiento de datos, los verdaderos ventajas del mercado radican en las actividades de blockchain y sociales "pumpamentals" en lugar de los gráficos técnicos solos.

Comprensión del análisis de criptomonedas en cadena

El análisis en cadena significa seguir las transacciones de blockchain en tiempo real para anticipar tendencias futuras del mercado. MIT Sloan explains this wellmostrando cómo la transparencia en los sistemas de blockchain ayuda a los inversores a tomar mejores decisiones y por qué esa visibilidad está redefiniendo el mercado de criptomonedas.

Como los activos criptográficos operan en registros públicos transparentes, los traders pueden monitorear indicadores críticos con precisión, tales como:

- Transacciones de Cartera Inteligente: Los grandes transferimientos indican posibles cambios en el valor de los activos.

- Entradas y salidas de intercambio: Presiones de compra y venta claramente identificadas a través de las actividades de intercambio.

- Participación en Contratos de Finanzas Descentralizadas: La actividad en contratos de finanzas descentralizadas indica tendencias emergentes.

- Señales de Sentimiento Social: Cuentas influyentes en plataformas como X (anteriormente Twitter) afectan significativamente el sentimiento del cripto.

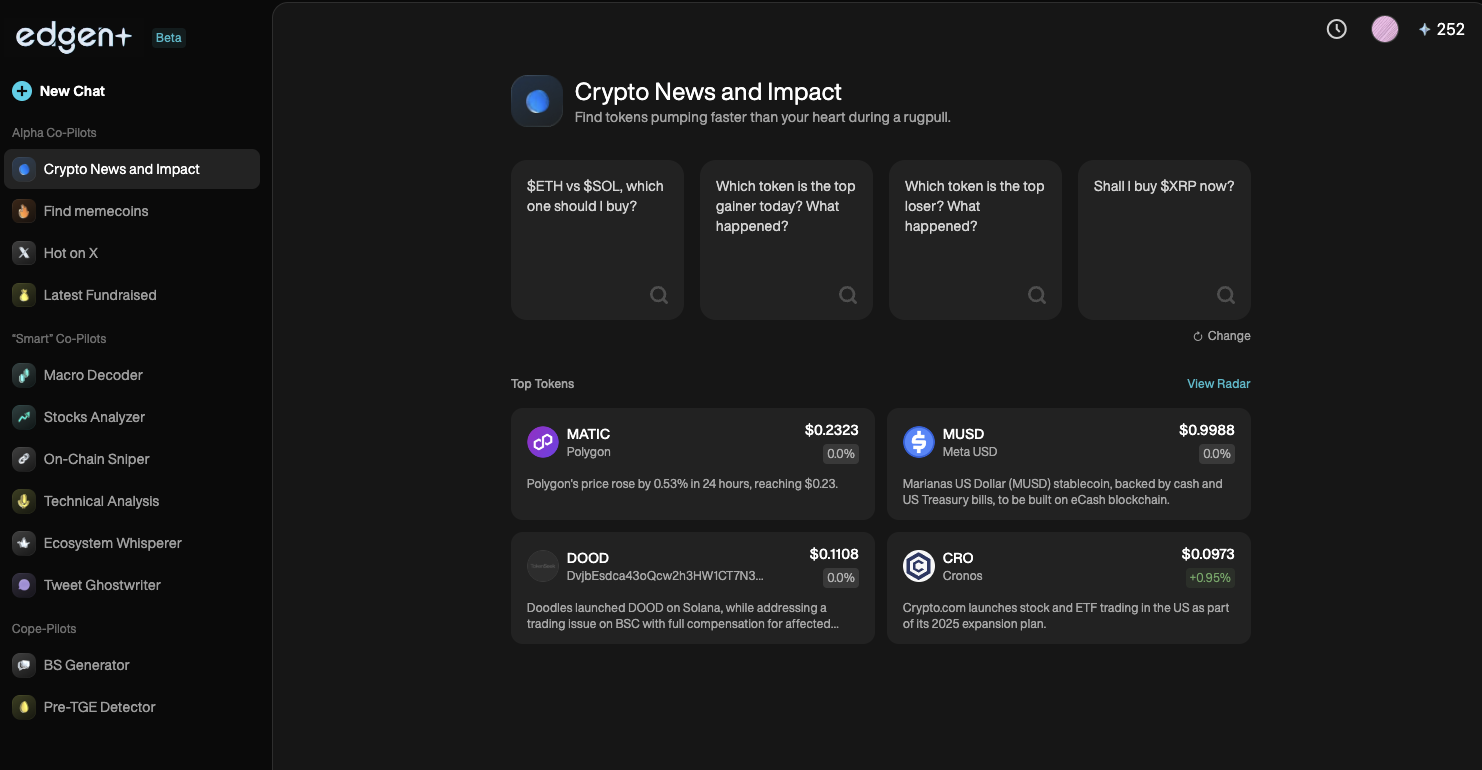

Para detectar estos cambios a tiempo, necesitas herramientas que funcionen más rápido que tú. Edgen Feedmantiene actualizado sobre narrativas en vivo, impulso social y actividad de billeteras en tendencia, todo en tiempo real.

¿Por qué la IA transforma el éxito en el trading de criptomonedas

La IA supera la capacidad humana para procesar grandes volúmenes de datos rápidamente y con precisión. Edgen AI aprovecha las fortalezas de la IA para ofrecer insights de mercado precisos de forma clara, brindando a los usuarios ventajas distintas en el trading:

1. Precisión de la Predicción del Mercado

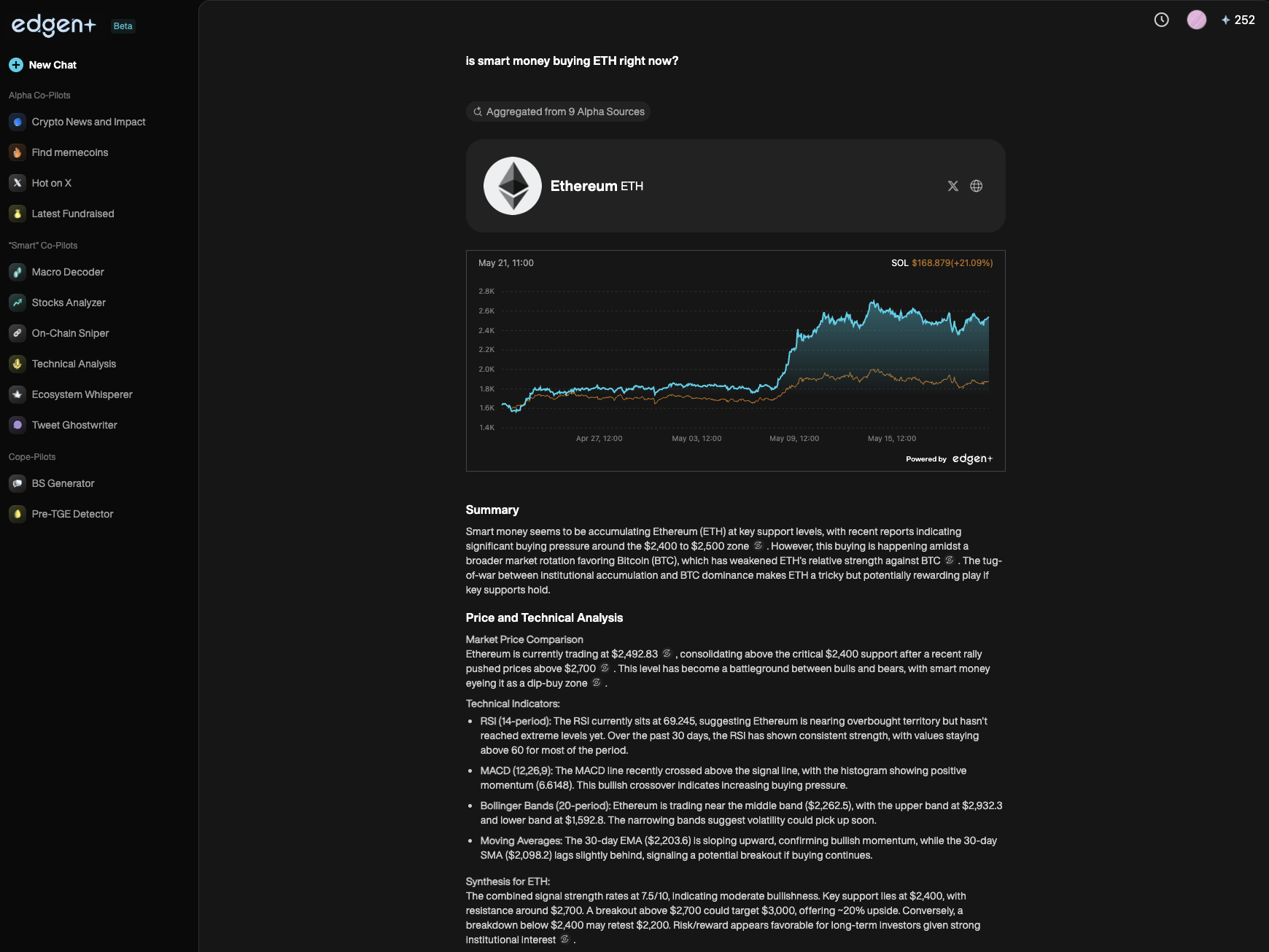

AI identifica oportunidades de comercio antes de que los precios las reflejen. Edgen AI monitorea continuamente los movimientos de la cadena de bloques y el sentimiento social, brindando a los traders información predictiva con bastante antelación.

2. Monitoreo en Cadena Instantáneo

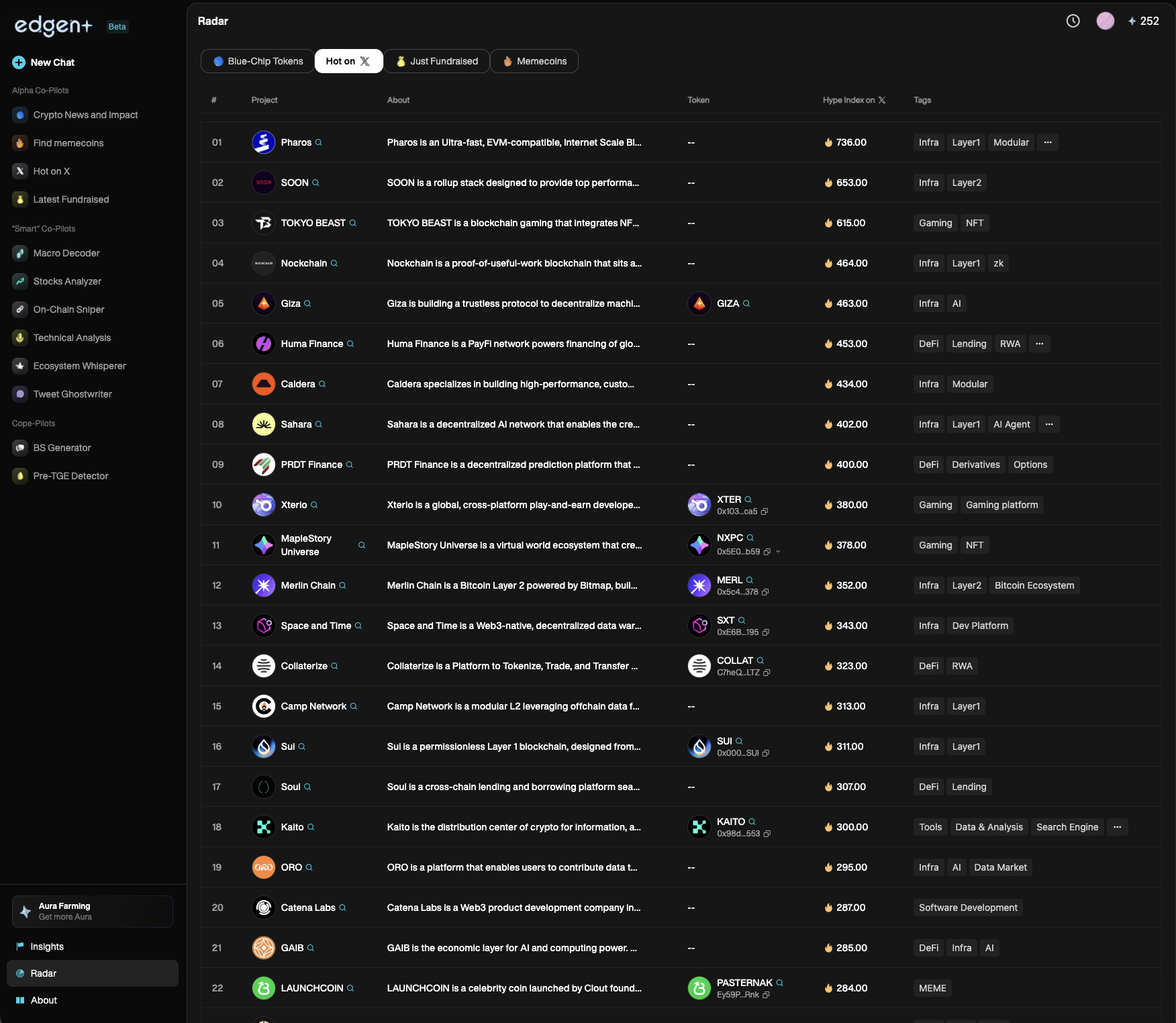

Los mercados no duermen. Tampoco debería hacerlo tu alimentación de datos. Edgen AI escanea constantemente transacciones de alto impacto, movimientos en DeFi y cambios en la liquidez. Herramientas como Edgen Radarrevelar tokens en tendencia y actividad de contratos antes de que la acción del precio llegue a intercambios importantes.

3. Integración de Datos Sociales y Blockchain

Los movimientos del mercado criptográfico resultan de influencias técnicas y sociales. Edgen AI combina el análisis de blockchain y el seguimiento en tiempo real del sentimiento social, destacando señales de alpha valiosas que otros pasan por alto.

Negociar sin IA corre el riesgo de tener una visibilidad incompleta. Edgen AI asegura que los traders vean claramente cada señal importante.

Señales Alpha: Tu Clave para Ganancias en Criptomonedas

Los traders exitosos dependen de señales alfa, que son indicadores tempranos que prevén oportunidades en el mercado antes de que sean reconocidas por la corriente principal.

Cómo Edgen AI Detecta Claramente las Señales Alpha:

- Análisis de Actividad de Billeteras: la IA identifica y rastrea las billeteras de grandes tenedores (whales) e insiders a través de datos de blockchain y comportamiento en redes sociales.

- Monitoreo de Contratos Inteligentes: Las tendencias de DeFi se vuelven claras a través de las interacciones de los contratos antes de que aparezcan en los movimientos de precio.

- Social "Pumpamentals: La IA reconoce de inmediato la tendencia social emergente en plataformas como X/Twitter, anticipando los impactos en los precios antes de que alcancen su punto máximo.

¿Quieres un avance? Edgen Searchte da acceso a los flujos de billetera, las tendencias de contratos y el rumor social en una sola interfaz rápida, así que nunca llegarás tarde a la fiesta de alpha.

Plataforma de Análisis de Criptomonedas con Inteligencia Artificial

Para mantenerse competitivos, los operadores necesitan una plataforma impulsada por inteligencia artificial que ofrezca perspectivas claras y en tiempo real sobre blockchain:

El AI de Edgen integra datos de blockchain y señales sociales en una plataforma integral, ofreciendo señales claras de alfa combinadas con una ejecución impulsada por inteligencia artificial precisa.

Edgen AI combina de manera única el análisis de blockchain, la inteligencia artificial y el análisis de sentimiento social en tiempo real dentro de una solución de trading unificada.

El Futuro del Comercio Pertenece a la IA: ¿Estás Listo?

El trading de criptomonedas ahora implica fundamentos de blockchain, sentimiento social e ejecución instantánea impulsada por inteligencia artificial.

Puntos Clave para los Comerciantes:

- El análisis de blockchain impulsado por IA supera claramente a los métodos tradicionales.

- Social "pumpamentalsimpulsar significativamente los mercados de criptomonedas.

- Edgen AIproporciona la única solución de comercio en el mercado que integra claramente los datos de blockchain, las perspectivas sociales y la ejecución de inteligencia artificial simultáneamente.

- Los operadores que utilizan inteligencia artificial ahora dominan los movimientos del mercado futuro.

¿Quieres saber cómo funciona Edgen en segundo plano? Visita Edgen's About page y descubra por qué los traders más inteligentes están cambiando a la IA ahora.

No te quedes atrás

Las criptomonedas se mueven rápidamente. Los traders que tienen éxito son aquellos que utilizan herramientas que ven más rápido, piensan de manera más inteligente y actúan antes. Avanza. Negocia de manera más inteligente.

UseEdgen AI.

Invertir, por fin, ya no es cosa de uno solo.

Prueba Edgen gratis. Sin tarjeta, sin compromiso.