AI 거래 오늘: 스마트 월렛과 KOL이 시장에서 주도하는 이유 (에지엔 AI와 통합됨)

AI 거래는 더 이상 멈출 수 없게 되었다

2025년 AI 거래는 금융 시장을 빠르고 지능적이고 접근하기 쉬운 방식으로 변화시킨다.

스마트 지갑과 키 오피니언 리더(KOL)가 이 새로운 거래 시대를 이끌고 있습니다. 그들의 통찰력과 기술은 초보자부터 전문가에 이르기까지 모든 트레이더에게 균등한 환경을 제공합니다.

전통적인 투자 방법은 사라졌습니다. 이제 트레이더들은 체인 내 분석, 알파 신호 및 소셜 기반 시장 동향을 통해 우위를 점하고 있습니다.

에 따르면 Wharton University of PennsylvaniaAI는 새로운 거래 전략을 생성하고, 거래를 실행하며, 실시간으로 시장 조건에 적응할 수 있도록 하여 금융 서비스 환경을 변화시키고 있다.

Edgen AI"방안을 읽는 트레이딩 AI"는 거래 환경을 완전히 재구성합니다.

AI 거래의 부상

AI 거래는 이미 존재했지만, 오늘날에는 시장을 지배하고 있다.

트레이더들은 더 이상 직관에만 의존하지 않습니다. AI는 수십억 개의 데이터 포인트를 즉시 평가하고, 명확하게 패턴을 식별하며, 빠르게 거래를 실행합니다.

왜 AI 거래가 지금 시장을 선도하는가:

- 속도: AI는 인간이 할 수 있는 것보다 시장 동향을 더 빠르게 분석합니다.

- 정확성: 대중적인 인식이 이르기 훨씬 전에 등장하는 트렌드와 시장 변화를 식별합니다.

- 자동화: AI 거래 로봇은 피로나 시장 운영 시간에 영향을 받지 않고 24시간 연중무휴로 거래를 실행합니다.

공포 매도나 즉흥 구매와 같은 인간의 감정은 더 이상 거래에 영향을 미치지 않습니다. 인공지능 기반 플랫폼은 안정적이고 데이터 중심이며 정확합니다.

그러나 전통적인 AI 거래 도구는 종종 사회적 스토리와 KOL의 영향을 간과합니다. Edgen AI는 이 공백을 메웁니다.

엣지엔 AI, 인공지능 거래 분야를 혁신하다

엣지엔 AI는 온체인 인사이트와 소셜 "펌펀다멘탈"을 통합하여, KOL 감정, 스마트 월렛 거래 및 시장 내러티브를 실시간으로 평가합니다.

엣지엔 AI가 다른 점은 무엇인가요?

- 사회적 합의 인사이트: X(구 트위터)와 같은 플랫폼에서 실시간 KOL 코멘트 및 유행하는 담론을 평가합니다.

- 체인 내 데이터 분석: 거래, 화이트 지갑 이동, 유동성 변화 및 토큰 활동을 실시간으로 추적합니다.

- AI 의사결정: 전통적인 데이터 분석과 사회적 동력을 결합하여 시장 변화를 예측합니다.

엣지나 AI가 없으면 트레이더는 소셜 감정과 영향력 있는 인물에 의해 생성된 숨겨진 신호를 놓친다.

트레이더를 강화하는 키 에지언 AI 기능

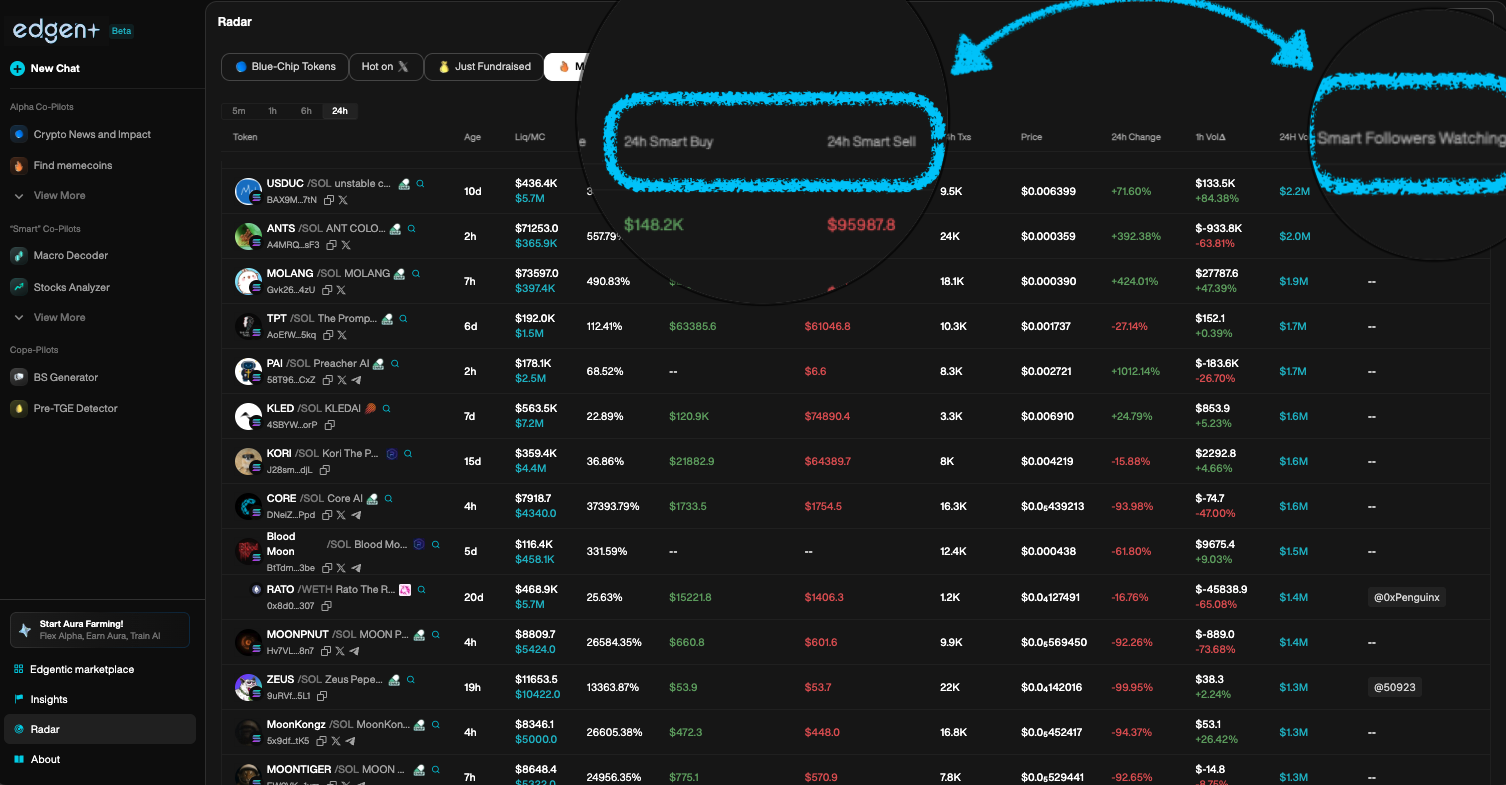

1. 에지너 레이더: 실시간 시장 가시성

Edgen Radar현재 시장 상황의 실시간이고 세부적인 모습을 제공합니다:

- 실시간 소셜 블랙과 블록체인 활동을 기반으로 트렌딩 토큰을 강조합니다.

- 트랙을 통해 고래와 스마트 지갑 활동을 명확하게 확인하세요.

- KOL 중심의 내러티브를 식별하여 중요한 가격 변동을 예측합니다.

이 데이터 명확성이 없으면 거래자는 정보가 부족한 결정을 내릴 위험이 있습니다.

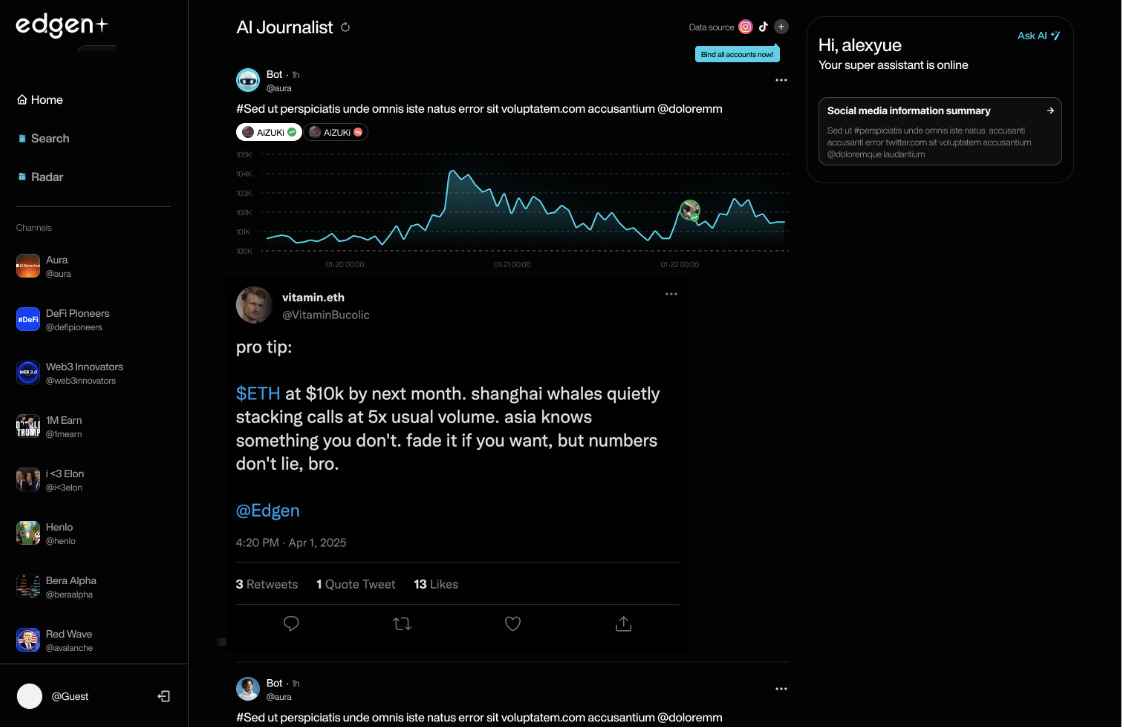

2. 에지엔 검색: 즉시 실행되는 AI 기반 시장 조사

Edgen Search트레이더의 AI 분석가로 작동합니다:

- 시장 관련 문의에 즉시 대답하여 검증된 데이터 기반의 답변을 제공합니다.

- 소셜 미디어 노이즈를 필터링하여 명확한 실행 가능한 통찰을 제공합니다.

- 크로스 플랫폼 트렌드(X, 텔레그램, 블록체인)를 빠르게 분석합니다.

트레이더들은 실질적인 알파 기회를 일시적인 시장 화제와 구분하기 위해 Edgen Search에 의존합니다.

3. Edge Insights: 커뮤니티 기반 알파 인사이트

Edgen Insights트레이더, 분석가 및 AI를 연결합니다:

- 트레이더 간 알파 인사이트의 실시간 공유를 가능하게 합니다.

- AI 모니터링 필터는 오보도를 필터링하고 토론을 명확히 합니다.

- 전문 거래자 및 분석가는 검증된 고품질의 통찰을 기여합니다.

인사이트는 단일 권위에 의존하지 않고 투명한 집단 지능을 촉진합니다.

스마트 월렛: 인공지능 기반 거래 엔진

스마트 지갑은 블록체인 분석과 인공지능 기반 전략을 통합한 고도화된 거래 도구로 진화했다.

스마트 월렛이 거래를 높이는 방법:

- 즉시 블록체인 모니터링: 일반 거래자들이 인식하기 전에 알파 신호를 조기에 탐지합니다.

- 신속한 거래 실행: 수동 지연 없이 자동화된 즉시 거래.

- 사기 방지: AI가 의심스러운 거래를 명확하게 감지하여 루그 풀을 방지합니다.

- 엣지엔 AI 통합: 스마트 지갑은 엣지엔의 소셜 분석을 활용하여 거래 정확도를 향상시킵니다.

스마트 지갑 없이는 수동 거래로는 시장 변동이 너무 빠르게 발생한다.

KOL: 시장 동향을 정의하는 인플루언서

주요 의견 리더는 시장 심리에 큰 영향을 미칩니다. 그들의 추천, 게시물 및 서사가 암호화폐 가격에 빠르게 영향을 미칩니다.

KOL이 AI 거래를 이끄는 방식:

- "펌페르티널리즘(Pumpamentals)" 생성: KOL에 의해 주도되는 소셜 화제는 자산 평가에 직접적인 영향을 미친다.

- 오퍼 알파 기회: 내부 정보는 수익 있는 거래에 대한 조기 진입점을 제공합니다.

- 감정을 명확하게 영향을 미치다: KOL의 낙관주의 또는 비관주의가 시장 방향에 중대한 영향을 미친다.

KOL 중심의 소셜 신호를 무시하면 거래 효과성이 크게 제한된다. Edgen AI는 KOL의 활동, 토론 및 감정 트렌드를 즉시 스캔하여 시장 반응을 사전에 예측한다.

AI 트레이딩 혁명이 도래했다

AI 거래는 미래의 가능성이 아닌 현재의 필수 요소로 변모했다.

스마트 지갑, 영향력 있는 KOL, 엣지 AI의 최첨단 분석은 시장 정보가 사회적 통찰과 블록체인 투명성을 결합하는 새로운 거래 시대를 정의합니다.

이 인공지능 기반 시대에서 성공하는 거래자들은 다음과 같아야 한다:

- AI 기반 스마트 지갑을 사용하여 빠르고 정확하게 실행하세요.

- 에드진 AI를 활용하여 소셜 기반의 "펌멘탈"을 명확하게 추적하십시오.

- KOL 인사이트를 따르되 블록체인 분석을 통해 검증하라.

- 알파 신호를 일관되게 모니터링하여 시장 동향을 예측합니다.

시장은 빠르게 변한다. 다음으로 중요한 가격 이동은 이미 진행 중이다.

더 많은 사람들이 거래하기 전에 거래할 준비가 되셨나요? 시도해 보세요Edgen AI오늘!

투자, 드디어 혼자 안 해도 돼요.

Edgen 무료 체험. 신용카드 필요 없고, 약정도 없어요.