ファンダメンタルズから「パンプメンタルズ」へ:ソーシャルセンチメントが今、市場を動かす方法

数字から物語へと市場が移行した

金融市場は変化した。収益報告書、貸借対照表、伝統的な指標が価格の変動を支配するようになったのは過去のことである。ソーシャルメディアは今ではウォールストリートそのものだ。強力なインフルエンサーからの1つのツイートや、1つのバズるミームによって、株価は数分で急騰することがある。

伝統的な投資家は収益計算書、EBITDA、債務比率を追跡することに慣れている。現代のトレーダーはソーシャルセンチメント、ブロックチェーンウォレットの動き、ウイルス性のある市場ナラティブを追う。Edgen AI トレーダーがリアルタイムで市場の感情を読み取り、それが影響を及ぼす前に変化を捉えることを可能にします。

基礎知識 vs.ポンプメンタルズ: 新たな現実

財務の基本的な要素とは何か?

伝統的な投資は、企業の健全性に関する指標に焦点を当てます:

- 収益性

- 収益の成長

- 金融の安定性

要するに、投資家は四半期報告書、債務水準および経営の質を分析します。

ポンプメンタルズハッピードリブントレーディングの台頭

その後、ミーム株が登場した。ゲームストップ(GME)、アミューズメント・メディア・コーポレーション(AMC)などの資産価値は、強力な収益を示さずに急騰した。価格はソーシャルメディアの勢いによって急上昇した。

オンラインコミュニティが、過度な宣伝や集団の感情によって、大規模な購入ブームを生み出しました。この現象(ポンプメンタルズ) は現在、市場の現実となっており、注目が価格変動へと変わりつつある。

AIの重要な役割 inポンプメンタルズ

AIは、社会的意見の追跡および予測において不可欠なものとなった。Edgen AIは、以下を活用している:

- ツイッター/X のコンセンサスのトレンド

- リアルタイムブロックチェーンウォレットの活動(ホエールアラート、スマートマネー)

- メン・アセットに関する新興市場の物語

AIツールなしでのトレードは、アルファ信号を失うことになる。Edgen AIトレーダーが市場の変化を早期に予測するのを助けます。

ソーシャルセンチメントの力

社会的感情の定義

ソーシャルセンチメントは、特定の資産に対するオンライン上の熱狂や否定的な感情を反映しています。トレーダーは、ツイッター、リディット、オンラインフォーラムをチェックすることで、伝統的なメディアよりも早く価格の反応を見ることができます。

なぜ感情が現在価格を動かすのか

- 即時情報: ソーシャルメディアは、伝統的な金融ニュースよりも早く信号を伝送する。

- 小売影響力:個人投資家がオンラインで団結し、伝統的な金融を挑戦している。

- AI駆動型のインサイト: Edgen AIは感情の変化を即座に追跡し、重要な初期サインを提供します。

感情のAI追跡

エッジンAIは、ソーシャルメディアおよびブロックチェーン取引を継続的にスキャンします。トレーダーは次のことで優位性を得ます:

- ウイルス的なトレンドを早期に見抜く

- 影響力のあるウォレット(スマートマネーおよびホエール)のモニタリング

- 主要な意見リーダー(KOL)の影響力を評価する

AI取引は現代の投資において不可欠です。

ミーム株とウイルス的投資現象

マーム・ストックス、定義

メンストックは、基本的な価値ではなく、ソーシャルな話題によって急速に上昇する。小口投資家は、r/ などのコミュニティを通じて協調する。ウォールストリートベッツ、爆発的な購入の波を生み出す。

ゲームストップの歴史的な株価上昇

ゲームストップ(GME)は、リディットのコミュニティが盛り上がったまで、低い水準で取引されてきた。大規模な調整された買いがショートセールスを引き起こし、株価が数日で20ドルから500ドルまで上昇した。

伝統的な金融論理はこれを予測できなかった。ソーシャル駆動型の勢いが支配的だった。

行動ファイナンス:投資家が群衆に従う理由

心理的要因の裏にあるポンプメンタルズ

行動ファイナンスは、論理ではなく感情によって駆動される市場の意思決定を説明するものです:Explore key behavioral biases and their impact on financial decisions.

- 「フォモ(FOMO)」:上昇トレンドにある資産を購入するために投資家が急いで買う。

- 記念的行動:人々は伝統的な警告を無視して、人気の流れに従う。

- 確認バイアス:投資家は既存の信念に合致する情報に傾き、リスクを見過ごす。

TheVolfefeインデックス:社会的影響の測定

エリック・マスクのようなインフルエンサーは、資産価格に大きな影響を与えます。マスクのツイートだけで、ドージコインやテスラの価格は大きく変動しました。Volfefeインデックスは、影響力のあるソーシャル投稿の市場への影響を追跡し、Edgen AIのようなAI駆動型のソーシャル分析の重要性を強調しています。

代替データとAI強化型感情分析

代替データの理解

伝統的な投資は財務諸表や四半期報告書を用いていました。現在、トレーダーはレバレッジを活用しています:

- ソーシャルメディアのトレンド

- ブロックチェーン上の暗号通貨取引

- Googleの検索分析

- AI駆動の市場センチメントデータ

代替データは、価格変動に反映される前に市場の機会を明らかにします。

エッジンAI:トレーディングの未来を形作る

エッジンAIがトレーダーにエッジを提供する方法

Edgen AIは、完全な買方取引インフラを提供し、同時に次のものをトラッキングします:

- スマートウォレットの動き(ホワイトとインフルエンサー)

- 社会的合意とウイルス的な物語(Twitter/X)

- AI駆動型の感情の変化

今日の取引はなしAI駆動のインサイトブラインドフォルドをつけて投資するようなものだ。

Edgen AIのコア機能:

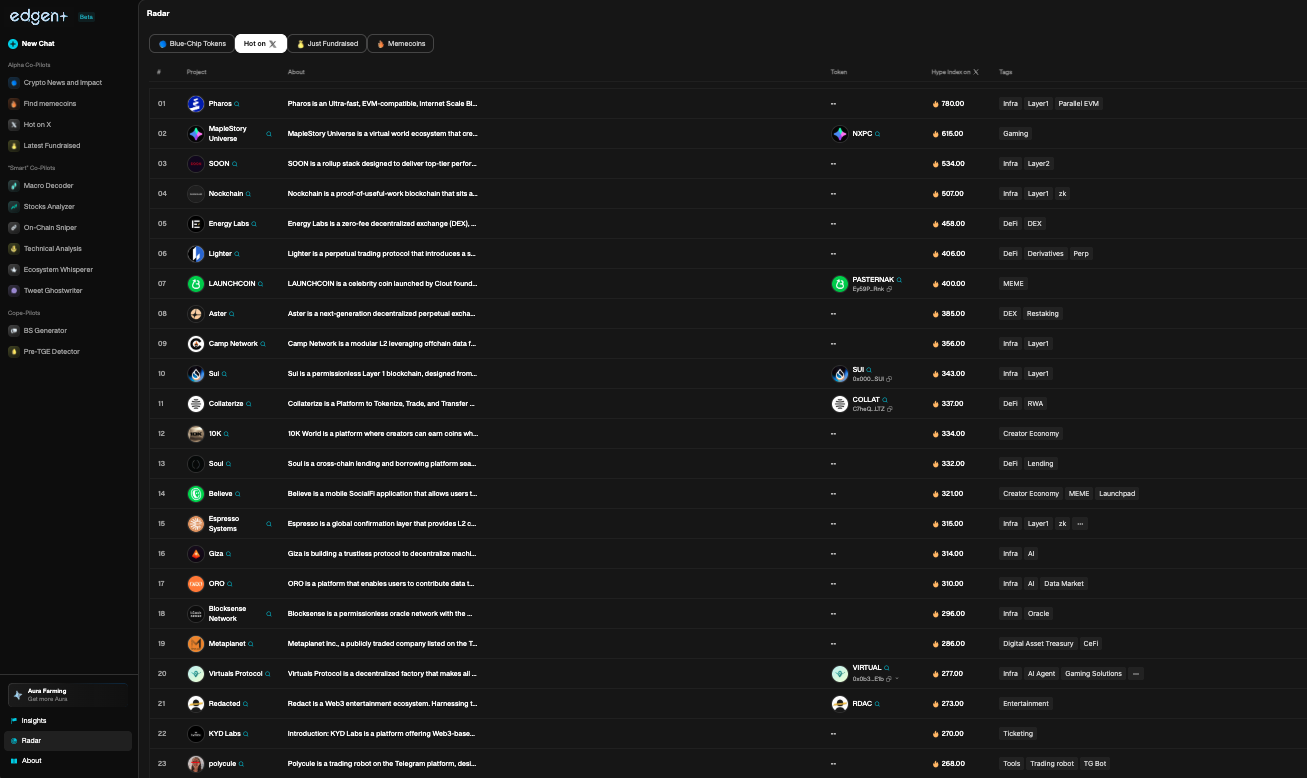

- Edgen Radarリアルタイムでの市場の感情とトレンドのモニタリング。

- Edgen Search: Instant answers backed by market-driven insights.

- Edgen Insightsコミュニティから抽出されたアルファとタイムリーな市場情報。

なぜこれが重要なのか

メン・アセットと暗号通貨市場は、ブームのサイクルに支えられて成長しています。プラットフォームのようにウォールストリートベッツ価格の変動において、社会的モーメンタムが伝統的な金融指標を上回ることを示した。

Edgen AIトレーダーがこれらの機会を特定し、対応するのを支援しますポンプメンタルズ早期に、トレンドが完全に現れる前にアルファを獲得する。

Adapt or Become Obsolete

The investing landscape evolved. Financial reports alone no longer drive markets. Instead, social media sentiment, influencer narratives, and AI-driven analytics shape trading.

Edgen AI equips traders to:

- リアルタイムで感情の変化を追跡し、対応する

- スマートマネーの動きをモニタリングする

- 急 emerging market の物語に即座に対応する

トレーダーがAI駆動のインサイトを無視すると、より速く、より賢く、より情報に詳しい相手と取引することになる。

未来がやってきた。トレードの成功は今や、AIツールを活用するあなたの能力にかかっている。時代の。Edgen AI取引が開始されました。Stay前へ、または残る。あなたの番だ。

投資、もうひとりじゃない

Ed を無料で試そう。クレカ不要、縛りなし