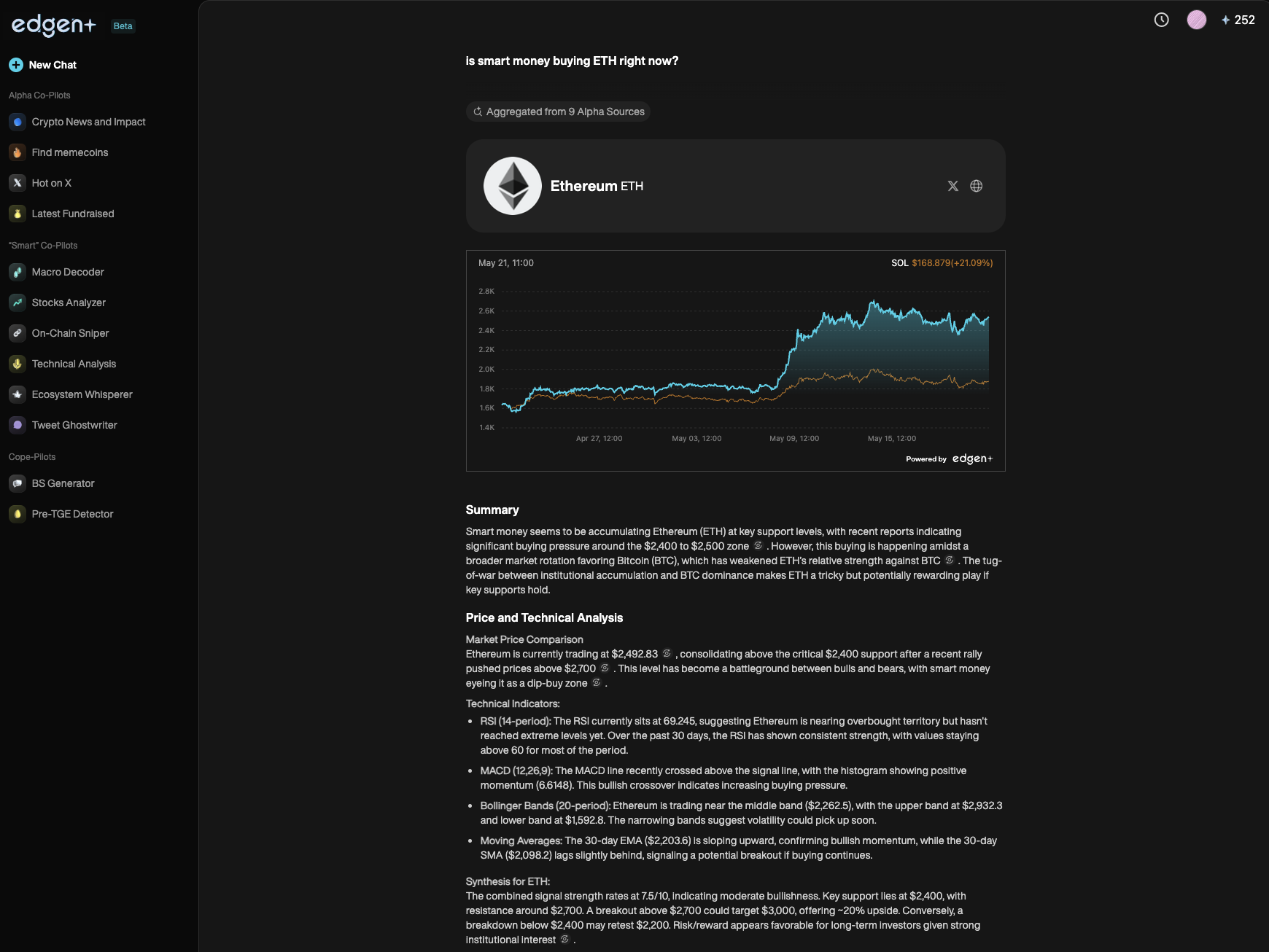

鏈上加密貨幣分析:AI 如何幫助交易員領先市場

加密貨幣市場演進,傳統分析落後於時代

加密貨幣市場變化迅速。傳統分析方法無法及時提供準確的見解。為了保持優勢,交易者需要鏈上分析和人工智慧驅動的策略。

Edgen AI結合區塊鏈洞察、人工智慧與社群訊號,提供一個清晰的解決方案。透過分析即時數據,Edgen 消除盲點,使交易者能及早捕捉有利可圖的行情。

當AI超越人類的數據處理能力時,真正的市場優勢在於區塊鏈活動和社會「泵基礎知識「而非僅憑技術圖表」。

了解鏈上加密貨幣分析

鏈上分析是指追蹤即時的區塊鏈交易,以預測未來的市場趨勢。 MIT Sloan explains this well顯示區塊鏈系統中的透明度如何幫助投資者做出更好的決策,以及為何這種可見性正在重塑加密貨幣市場。

由於加密資產運行在透明的公共分類賬上,交易者可以精確監控關鍵指標,例如:

- 智慧錢包交易:大額轉帳可能表示資產價值的變動。

- 交易所資金流入與流出:透過交易所活動明確識別買賣壓力。

- DeFi 合約互動:去中心化金融合約中的活動顯示出新興趨勢。

- 社會情緒訊號:在X(前稱Twitter)等平台上具有影響力的帳戶對加密貨幣情緒有顯著影響。

要及早捕捉這些變化,你需要比你更快的工具。 Edgen Feed即時讓您掌握現場敘事、社群動態及熱門錢包活動。

為什麼AI能改變加密貨幣交易的成功率

AI 優於人類處理大量數據的速度和準確性。Edge AI 借助 AI 的優勢,清晰地提供精確的市場洞察,為用戶帶來獨特的交易優勢:

1. 市場預測準確性

AI 在價格反映之前就能精準鎖定潛在交易。Edgen AI 持續監控區塊鏈的動態與社群情緒,為交易者提供提前的預測性洞察。

2. 即時鏈上監控

市場不會休息。你的資料輸送也不該停頓。Edgen AI 持續監測高影響力的交易、DeFi 動向及流動性變動。類似這樣的工具還有 Edgen Radar在價格行動影響主要交易所之前,揭露熱門代幣與合約活動。

3. 社會與區塊鏈資料整合

加密貨幣市場的波動來自技術和社會因素的影響。Edgen AI 結合區塊鏈分析與即時社群情緒追蹤,強調其他機構忽略的有價值alpha信號。

沒有AI的交易會導致視野不完整。Edgen AI確保交易者能清楚看到每個關鍵訊號。

Alpha信號:您賺取加密貨幣利潤的關鍵

成功的交易者依賴alpha訊號,這些是市場機會的早期指標,在主流意識覺察之前就能預測市場機會。

Edgen AI 如何明確檢測 Alpha 訊號:

- 錢包活動分析:AI透過區塊鏈資料和社群媒體行為來識別與追蹤巨額錢包及內部人士錢包。

- 智慧合約監控:透過合約互動,可以在價格波動出現前就能觀察到DeFi的趨勢。

- 社會 "泵基礎知識:AI能立即識別X/推特等平台上的新興社會熱潮,在價格達到高峰前預測其影響。

想要先發制人嗎? Edgen Search讓您透過一個快速的介面存取錢包流量、合約趨勢和社群熱度,確保您從不落後於Alpha派對。

AI驅動的加密貨幣分析平台

為了保持競爭力,交易員需要一個由人工智慧驅動的平台,提供清晰即時的區塊鏈洞察:

Edgen AI 將區塊鏈資料與社交訊號整合至一個全面的平台,提供清晰的alpha信號,並結合精準的AI驅動執行。

Edgen AI 將區塊鏈分析、人工智慧與即時社會情緒分析獨特地結合於一個整合的交易解決方案中。

未來的交易屬於人工智慧:你準備好了嗎?

加密貨幣交易現在涉及區塊鏈基礎知識、社群情緒以及由人工智慧驅動的即時執行。

交易者重點事項:

- AI驅動的區塊鏈分析明顯優於傳統方法。

- 社會 "泵基礎知識「驅動加密貨幣市場顯著波動。」

- Edgen AI提供市場唯一同時整合區塊鏈資料、社群洞察與AI執行的交易解決方案。

- 交易者運用AI現在主導未來市場走勢。

想了解Edgen背後運作的方式嗎?請訪問 Edgen's About page 並了解為何最聰明的交易員現在正轉向人工智慧。

不要落後

加密貨幣的走勢快速,成功交易者都是使用能更快看見、更聰明思考、更早行動的工具。率先一步。智慧交易。

投資這事,終於不用一個人了

免費試用 Ed。不用信用卡,不綁約