Portefeuilles : une manière plus intelligente de surveiller vos actifs

Les marchés génèrent plus d'informations que n'importe quel investisseur ne peut en traiter. Chaque mouvement de prix, mise à jour des résultats et donnée on-chain ajoute du bruit à un flux déjà saturé.

La solution était auparavant les listes de surveillance traditionnelles d'actions ou de jetons. Elles affichent les prix et les tickers. Mais elles révèlent peu sur ce que ces chiffres signifient et quelles actions entreprendre.

Aujourd'hui, Edgen présente les Portefeuilles : un assistant natif de portefeuille qui applique le raisonnement multi-agents aux actifs figurant sur les listes que vous construisez.

Chaque liste peut contenir des actions, des jetons, ou des actions et des jetons simultanément, car les récits et les chocs se propagent à travers les deux.

Une nouvelle façon de suivre les actifs

Le suivi est facile. La compréhension est plus difficile.

Les portefeuilles transforment vos listes en une couche d'intelligence active qui examine vos avoirs, analyse ce qui compte et le présente sous une forme personnalisée instantanément claire grâce aux agents spécialisés d'Edgen. Considérez-le comme un analyste intégré à votre portefeuille, adapté à votre style et fonctionnant en continu.

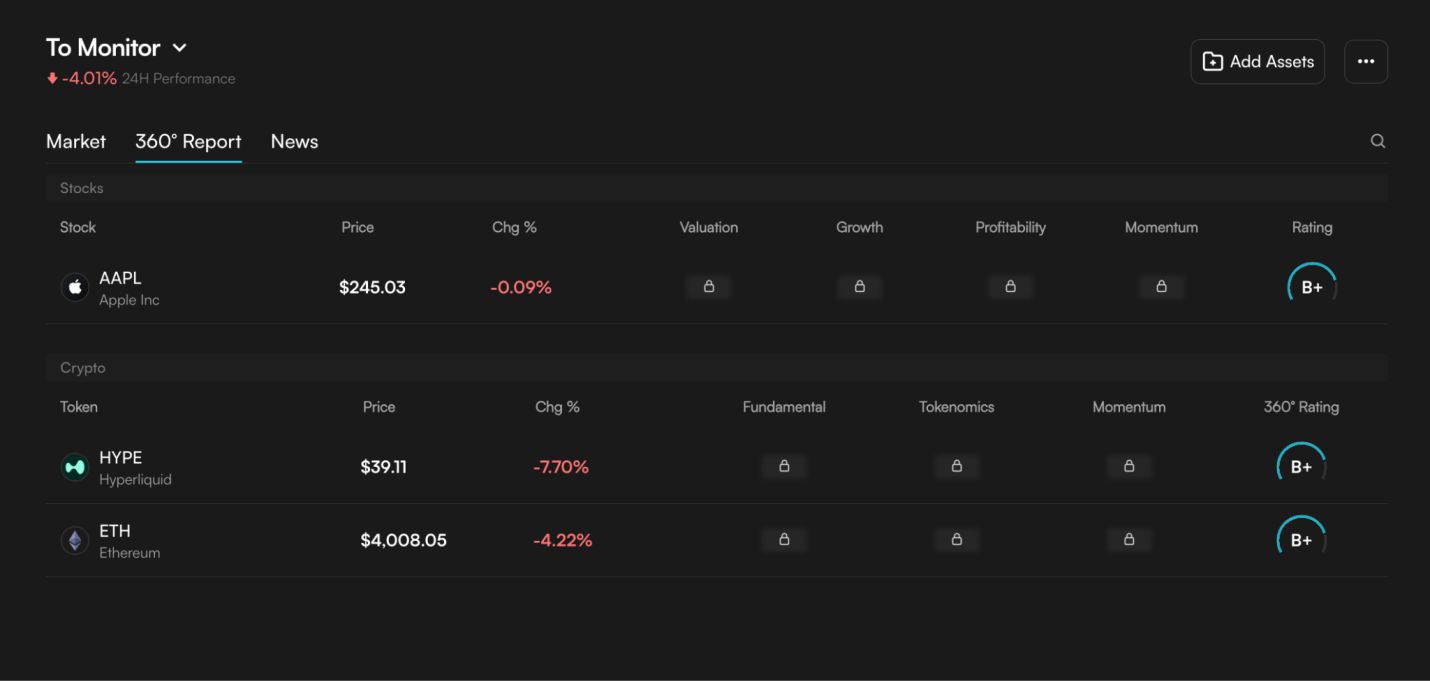

Chaque actif que vous suivez, qu'il s'agisse d'actions ou de cryptomonnaies, reçoit des diagnostics continus, des évaluations par lettres (A à F) et des explications qui évoluent en temps réel.

Votre liste de surveillance devient un système vivant qui interprète, évalue et met en évidence les mouvements clés en temps réel. Ils apprennent vos rythmes d'investissement, les secteurs que vous privilégiez, les tendances que vous suivez, les risques que vous tolérez et affinent les informations autour de ces signaux.

Plus vous l'utilisez, plus les conseils seront pertinents.

Les marchés ne vous attendent pas. Les Portefeuilles Edgen s'assurent que votre attention se porte là où elle compte le plus.

Comment fonctionnent les portefeuilles Edgen

En coulisses, le réseau d'agents spécialisés d'Edgen fonctionne simultanément sur plusieurs dimensions de données de marché :

- Techniques : modèles de prix, volatilité et momentum.

- Fondamentaux : bénéfices, métriques de jetons ou d'actions, et données commerciales sous-jacentes.

- Momentum : flux, sentiment et dynamique des volumes.

- Macro : corrélations entre actifs et forces macroéconomiques plus larges.

Le modèle de guidance d'Edgen (EDGM) coordonne ces agents, vérifiant les entrées et les fusionnant en une sortie claire et personnalisée apparaissant dans votre liste.

Le résultat est une vue unifiée et explicable qui couvre chaque actif que vous suivez, à la fois les actions et les cryptomonnaies, et se met à jour automatiquement à mesure que les conditions changent.

- Vous pouvez l'utiliser comme votre portefeuille en direct, ou comme une liste de surveillance pour les actifs que vous surveillez.

- Vous pouvez également créer un panier sectoriel ou narratif (IA, Perp DEX, actions détenant de l'ETH) et observer l'alignement des signaux sur vos jetons et actions préférés.

- Vous pouvez également conserver un bac à sable de thèses pour tester des idées et voir comment les évaluations évoluent à mesure que les marchés changent.

- Vous pouvez également définir une liste à risque élevé ou faible pour les positions qui correspondent à votre profil de risque.

- Créez un tableau de couvertures pour garder un œil sur les actifs refuges qui montrent de la force pendant les phases de marché turbulentes.

Comme vous pouvez le constater, les possibilités sont illimitées.

Comment utiliser les portefeuilles sur Edgen

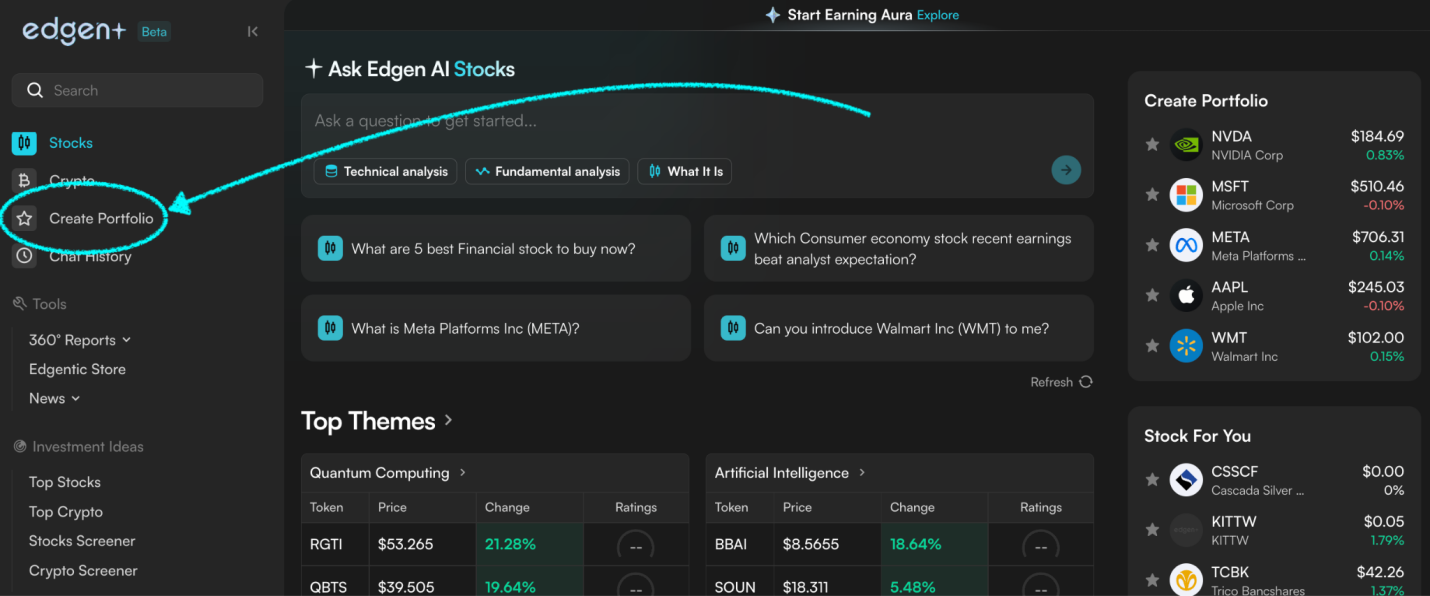

Dans le menu de gauche, cliquez sur « Créer un portefeuille » et nommez-le.

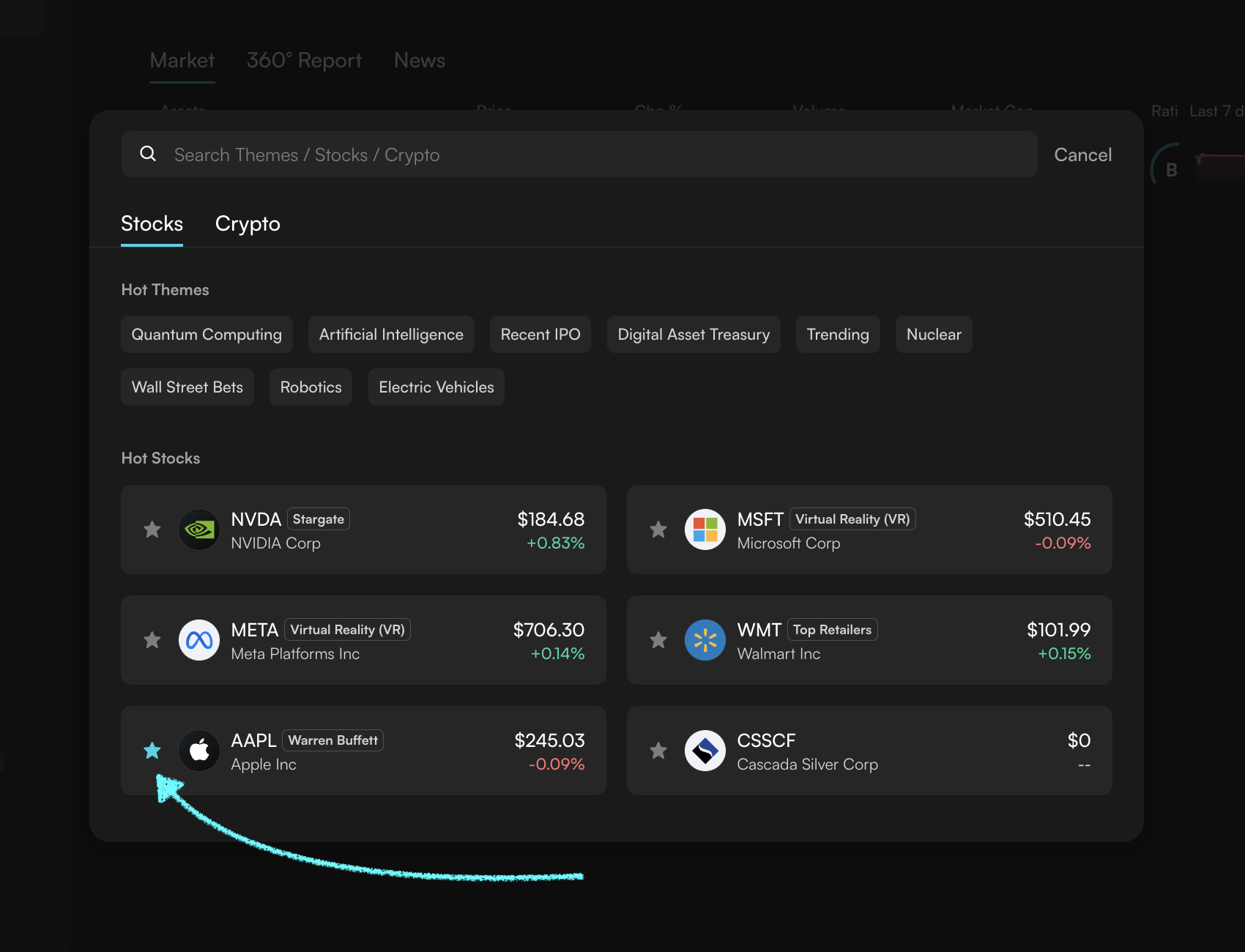

Ajoutez un actif depuis n'importe quelle section d'Edgen, ou simplement en cliquant sur « Ajouter des actifs maintenant » sur votre portefeuille intelligent actuel, et cliquez sur l'étoile à côté de votre ticket d'actif :

Chaque portefeuille peut contenir jusqu'à 30 actifs, actions et cryptomonnaies confondues.

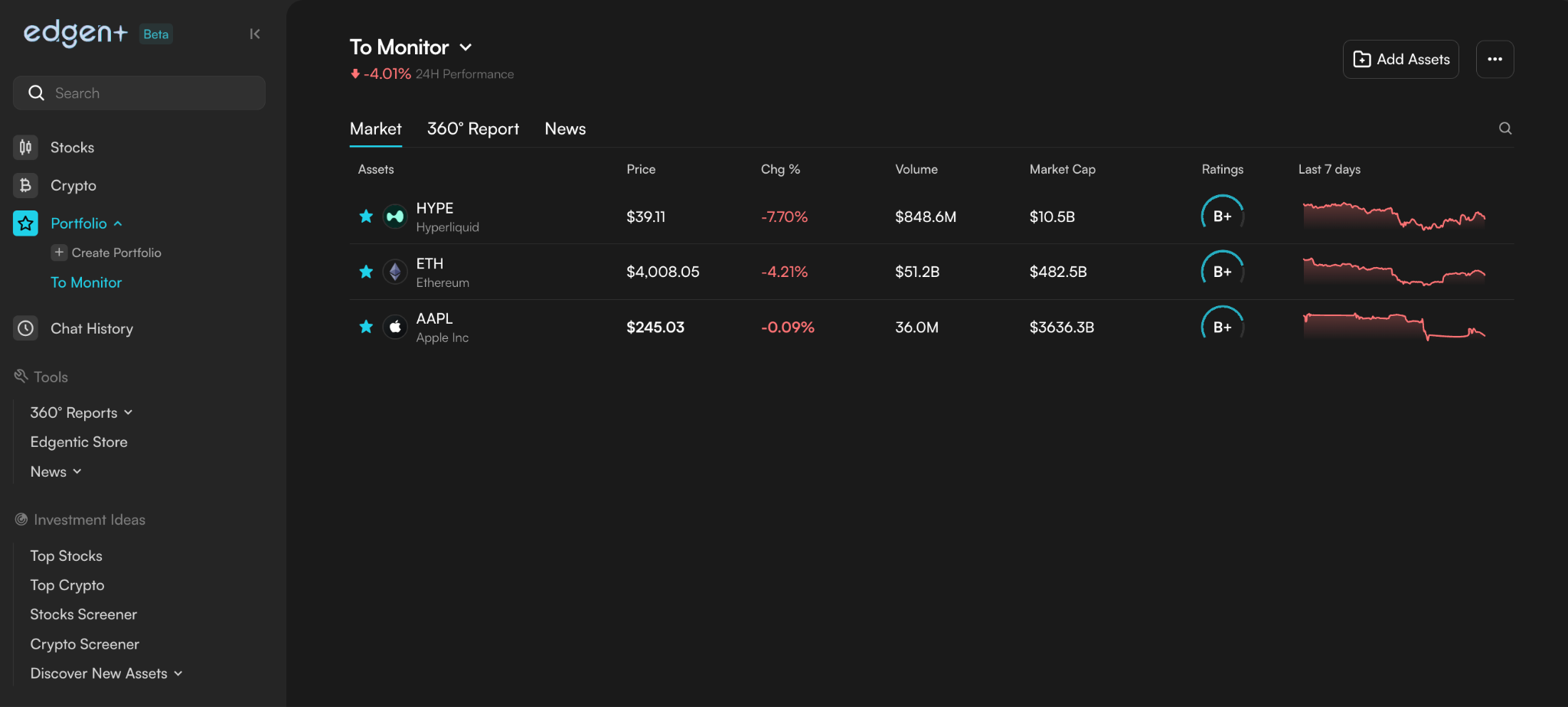

Pour chaque liste, 3 onglets prennent vie :

- Vue du marché : la vue par défaut, avec les prix en direct, les sparklines et les notes

- Vue des rapports à 360° : diagnostics entièrement détaillés, rafraîchis en continu.

- Vue des actualités : titres et articles pertinents filtrés selon votre portefeuille exact

Basculez entre eux fluidement. Plongez plus profondément chaque fois que vous avez besoin de contexte.

Cela ressemble moins à la surveillance d'une liste et plus à la collaboration avec un analyste personnalisé qui ne dort jamais.

Chaque portefeuille peut contenir jusqu'à 30 actifs, actions et cryptomonnaies confondues.

Les utilisateurs du plan gratuit peuvent utiliser jusqu'à 2 portefeuilles, le plan Pro en inclut 10, et le plan Expert en inclut 20.

Conçu pour l'avenir

Ce lancement ne marque que la première étape de l'intelligence native de portefeuille d'Edgen.

Les prochaines versions étendront le système avec des outils de comparaison, des alertes de pivot de prix personnalisées et un raisonnement plus approfondi qui renforcera votre prise de décision.

Chaque étape nous rapproche d'une vision : une interface unifiée qui comprend votre perspective de marché. Et évolue avec elle.

Essayez-le maintenant

Créez votre première liste. Ajoutez vos actions et jetons préférés.

Et observez-les prendre vie avec analyse, clarté et objectif.

Créez votre propre portefeuille intelligent sur Edgen dès maintenant : https://www.edgen.tech/app/

Investir, enfin, tu n'es plus seul.

Essaie Ed gratuitement. Sans carte, sans engagement.