Aura 101 : Comment transformer vos insights de marché en influence et récompenses

TLDR

- L'Aura est gagnée en accomplissant des actions significatives au sein d'Edgen : quêtes, abonnements et parrainages.

- Les Crédits alimentent les fonctionnalités IA d'Edgen – intelligence de marché, rapports, alertes.

- Des scores Aura élevés débloquent des fonctionnalités anticipées, des récompenses spéciales et un statut au classement.

- Les multiplicateurs (jusqu'à 100x) accélèrent votre gain en fonction de votre niveau d'abonnement.

Qu'est-ce que l'Aura ?

L'Aura d'Edgen vous offre de réels avantages pratiques au sein d'Edgen.

À mesure que votre score d'Aura augmente, vous accédez à des versions anticipées de fonctionnalités, à des programmes bêta exclusifs et à des récompenses potentielles liées à des événements futurs.

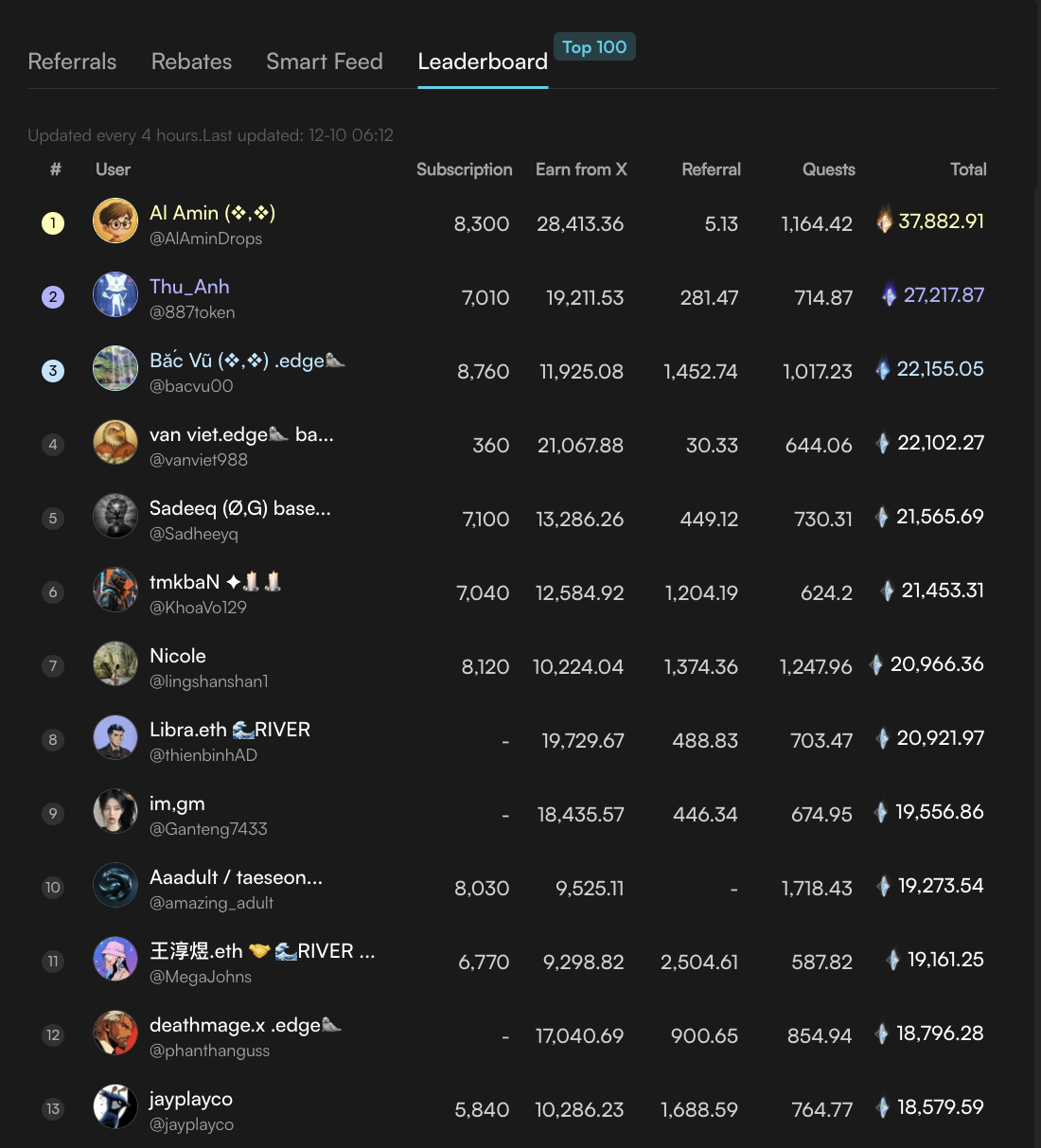

Aura dispose d'un classement. Y grimper vous place dans une classe de traders différente. Plus vous montez, plus vous vous rapprochez de récompenses spéciales, de privilèges uniques et d'un accès que d'autres ne verront pas.

L'Aura aide également les autres traders à reconnaître votre engagement envers la communauté. En termes simples, l'Aura transforme votre présence sur Edgen en valeur durable.

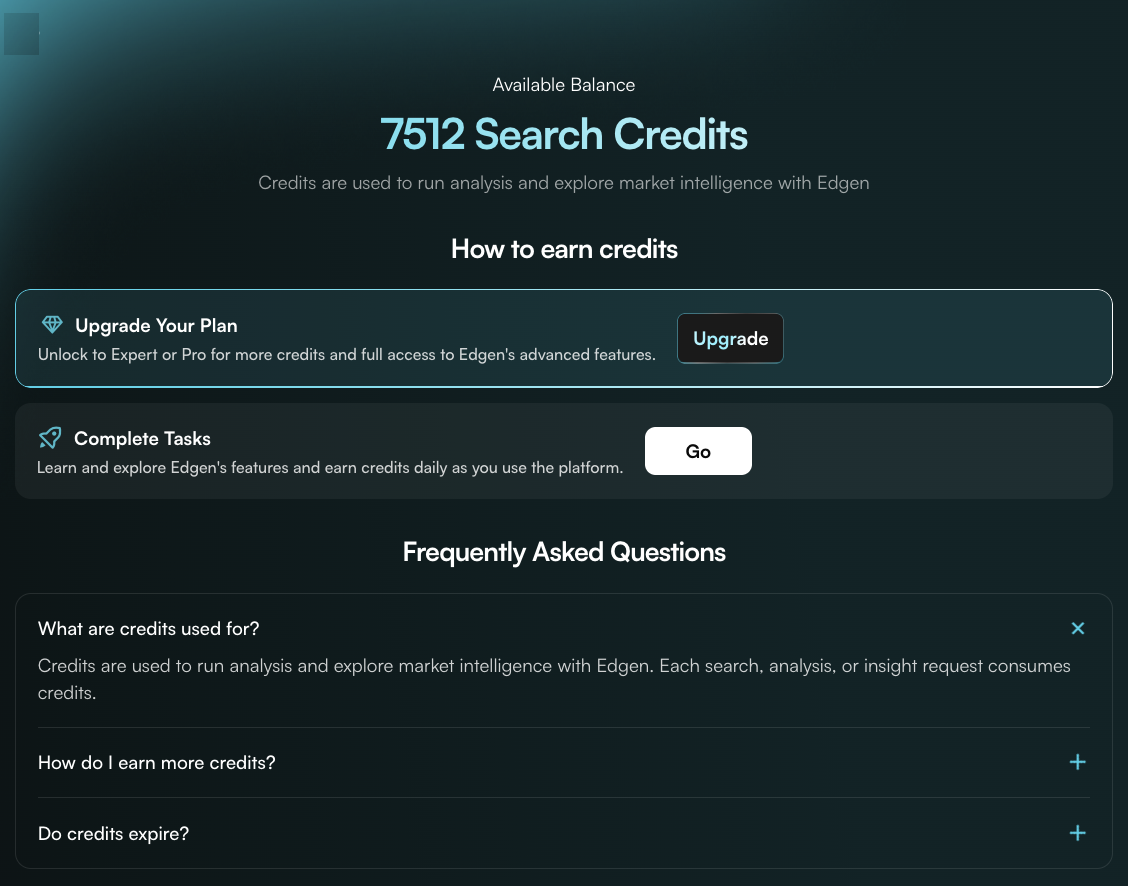

Que sont les Crédits ?

Les Crédits sont la façon dont vous utilisez l'IA d'Edgen.

L'intelligence de marché, les rapports de portefeuille et à 360°, les alertes intelligentes sont tous alimentés par des Crédits. Considérez-les comme votre carburant pour les outils d'Edgen.

Vous pouvez gagner des Crédits gratuitement en accomplissant des tâches dans le Centre des Tâches, ou en obtenir davantage via votre niveau d'abonnement.

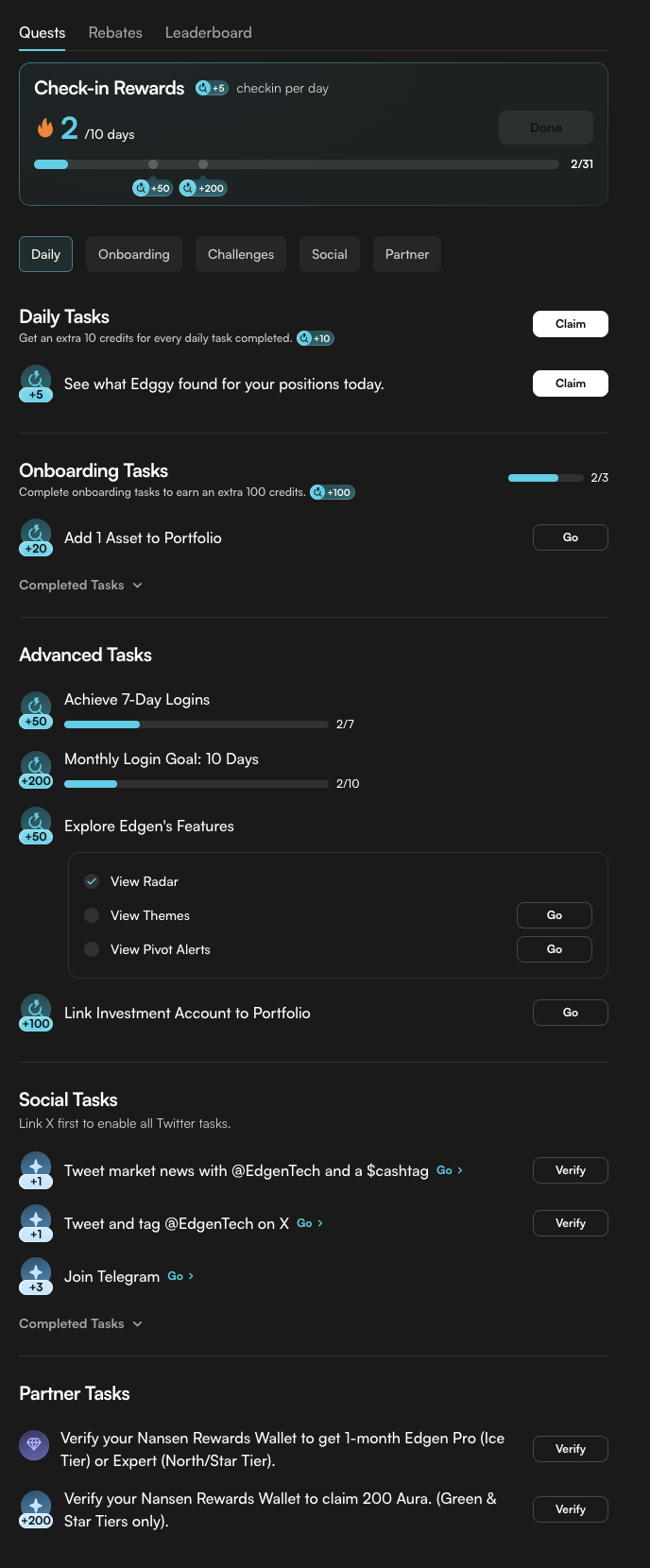

Centre des Tâches : Comment gagner

Le Centre des Tâches est votre plateforme pour gagner à la fois de l'Aura et des Crédits.

Il comporte 5 types de quêtes :

- Quotidiennes : connectez-vous, réclamez des récompenses

- Intégration : configurez votre Portefeuille, affûtez votre avantage sur le marché

- Défis : atteignez des jalons, débloquez des bonus

- Sociales : partagez vos analyses de marché ou vos actualités

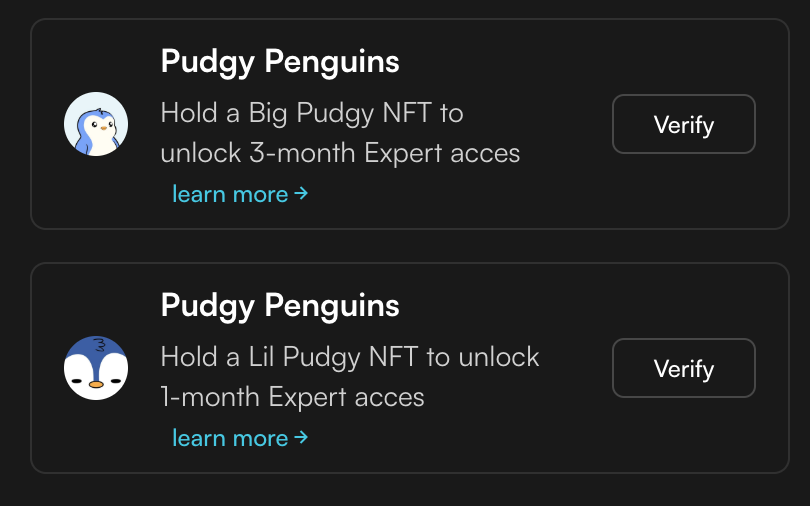

- Partenaires : collaborations à durée limitée avec des projets comme Nansen, Pudgy Penguins, et plus encore

Certaines tâches rapportent des Crédits. D'autres rapportent de l'Aura.

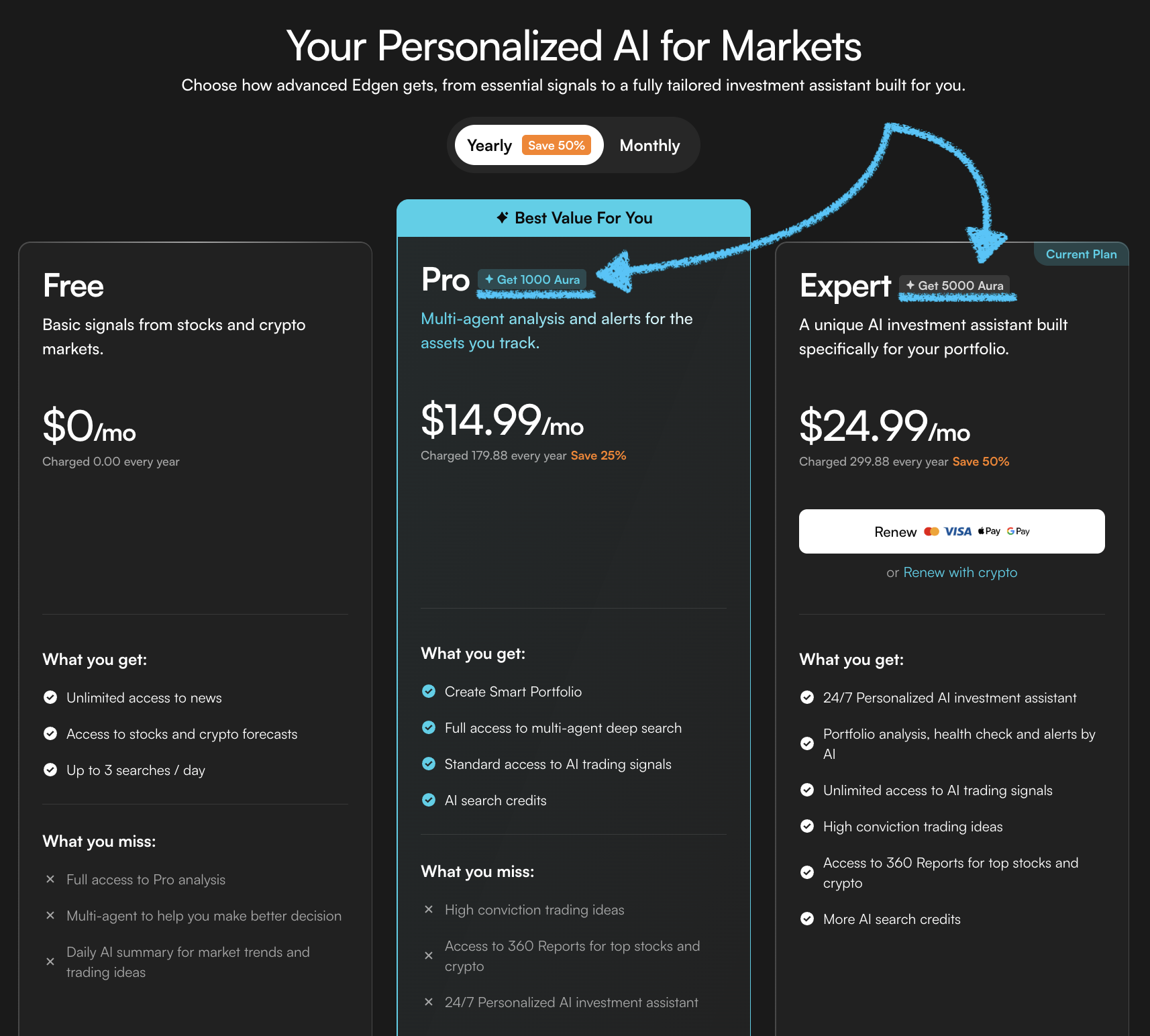

Multiplicateurs : Gagnez plus vite

Votre niveau de plan et votre période (mensuel/annuel) déterminent la vitesse à laquelle vous gagnez de l'Aura grâce aux tâches :

- Gratuit = 1x

- Pro = 20-30x

- Expert = 80-100x

Mêmes tâches, récompenses très différentes.

Les multiplicateurs s'appliquent à l'Aura gagnée grâce aux tâches, de sorte que la mise à niveau de votre plan ne débloque pas seulement des fonctionnalités, elle accélère également votre position dans le classement.

Aura d'abonnement

L'abonnement à Pro ou Expert vous donne un accès complet aux outils d'IA d'Edgen. Mais votre abonnement apporte également des avantages Aura :

- Vous recevez un bonus Aura unique lorsque votre abonnement commence.

- Pendant votre abonnement, les vérifications quotidiennes vous rapportent de l'Aura chaque jour.

Ces récompenses constantes vous aident à augmenter votre score d'Aura de manière cohérente au fil du temps.

Aura de parrainage

Invitez des amis à rejoindre Edgen. Lorsqu'ils s'inscrivent et terminent l'intégration, vous gagnez tous les deux de l'Aura.

Edgen suggère quels amis inviter pour maximiser votre bonus.

Si vos amis parrainés deviennent des abonnés Pro ou Expert, vous pouvez également gagner une partie de leur abonnement via des remises.

Quêtes Partenaires

De temps en temps, Edgen s'associe à des projets fiables pour publier des quêtes en édition limitée.

L'accomplissement des tâches partenaires récompense d'une Aura supplémentaire ou d'avantages comme un accès Expert gratuit, et vous permet de découvrir de nouveaux outils et écosystèmes connectés à Edgen.

Commencez maintenant

L'Aura offre des avantages précieux aujourd'hui, et son importance grandira à mesure que l'écosystème se développera.

Construire votre Aura tôt vous place dans une position forte pour les opportunités futures.

Commencez dès aujourd'hui : accomplissez une quête, explorez les outils, abonnez-vous si cela correspond à vos besoins, ou invitez un ami. Chaque action ajoute à votre Aura, et chaque point devient une partie de votre identité au sein d'Edgen.

Investir, enfin, tu n'es plus seul.

Essaie Ed gratuitement. Sans carte, sans engagement.