ミームコインから株式まで:AI 取引がグローバル市場を再構築する方法

AIはゲームを再構築している

金融市場は変化しました。からメモコインズ株式に限らず、トレーディングはチャートや手動分析を越えて進化しました。そして、伝統的な戦略では不十分で、トレーダーは過去に閉じ込められることになります。

AIを駆動とするツール、リードされたEdgen AI市場の感情、社会的な勢い、およびブロックチェーン上の動きをリアルタイムで解釈する。この利点により、これまでになく鋭く、賢く、迅速なトレードが可能になる。

なぜAI取引が現在市場を支配しているのか

AIは市場トレンドの読み取りにおいて人間のトレーダーを上回る。ビルリオン単位のデータポイントを瞬時に処理し、AIは他者に先駆けて市場の変化、インフルエンサーのシグナル、そして隠れた物語を非対称な速さで捉える。

AIを駆動とするトレーディングとは:

- 予測分析:他の人が気づく前に市場の物語が形成されているのを見る。

- アルゴリズム取引:マイクロ秒単位で取引を実行する。

- 感情分析:即座にツイッターの話題とインフルエンサーのトレンドをキャプチャする。

- 高度なリスク管理:彼らが攻撃する前に空頭のシグナルを検出する。

結論:AIは市場を予測する。人間は反応する;AIは予測する。

エッジン:部屋の空気を読めるAI

エッジンAIは、リアルタイムのブロックチェーン上データとソーシャル「ポンプメンタルズ「および、行動可能なインサイトに変換した深い市場の知見。主要な意見リーダー(KOL)を特定し、スマートウォレットをモニタリングし、群衆よりも先にアルファを提供します。」

コア機能:

- リアルタイム資産モニタリング:Edgen Radar価格動向とソーシャルセンチメントを同時に追跡する。

- AIで駆動される検索:Edgen Search集約されたデータから即時の市場情報をお届けします。

- コミュニティ主導の分析:Edgen Feedライブで、クラウドソースされたアルファ信号を提供します。

エッジンAIは、すべての取引を駆動する集団的なマインドセットの市場の鼓動を読み取ります。

メモコインそしてAI:自然なマッチ

メモコイン伝統的な評価を超えて運用する。価格の変動は、話題性、コミュニティの関与、ウイルス的飛躍に従う。

この環境ではAIが活躍します。エッジAIは特に、これを処理するのに適した立場にあります。メモコインズリアルタイムでの感情分析を用いて、市場の急激な変化を捉える。

Edgen AI マスターズメムコイン取引者:

- 感情分析:ツイッター/Xをスキャンして即時のポンプサインを検出中。

- オンチェーンのインサイト:トラッキングするホエールウォレットとインフルエンサーの活動をリアルタイムで。

- アルファ検出:価格の急騰前の隠れた指標を見つける。

メモコイン平均的なボラティリティと根拠のない競争。AIがなければ、トレーダーは勝機がない。

AIと現代の投資戦略

市場は基本的な要因を越えて変化した。ソーシャルセンチメント、予測分析、およびブロックチェーン上の取引が現代の戦略を定義している。

AIのスマート投資における役割:

- アルファ・ディスカバリー:市場が動く前にシグナルを発見する。

- AIで管理されるポートフォリオ:AIを活用したファンドが最適なリスク管理を提供します。

- ブロックチェーンの統合:スマートマネーを追跡するためのウォレットの動きのモニタリング。

Edgen Radar 新しい基準を設定し、個別の指標ではなく、全体の市場エコシステムを解釈します。

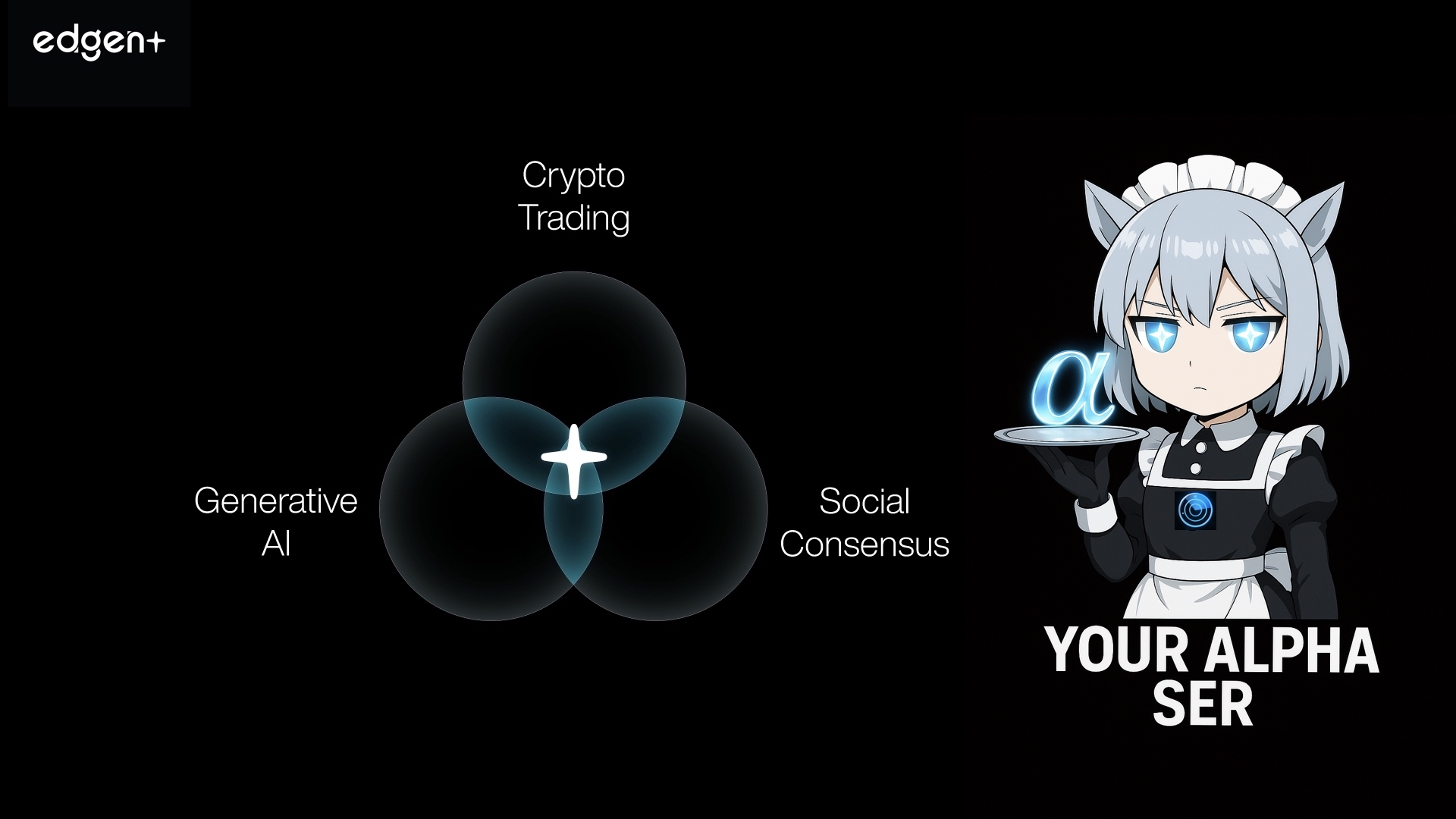

トレーディングの3体問題を解決する

ほとんどのトレーダーは部分的に盲目のように取引する:

- 一部のブロックチェーンデータを追跡するが、ソーシャルな物語を見落としている。

- 他の人々はブームに従うが、流動性の動きを無視する。

- 多くの人はテクニカルチャートにこだわり、市場を動かす話題を無視する。

エッジンAIは、3つの次元を統合することによってこの複雑さを解決します:

- オンチェーン分析:リアルタイムのスマートマネー追跡。

- ソーシャルセンチメント:ホットなトレンドやコミュニティ主導の動きを捉える。

- AIで駆動される実行: 他の人が機会に気付く前に戦略的に取引する。

この統一されたアプローチにより、エッジントレーダーは「PvP」、つまり競争的でゼロサムの市場において決定的な優位性を獲得します。

金融市場におけるAIの未来

AIは取引の未来を支えています。この事実を無視するトレーダーは、永遠に後れをとることになります。

次に何が来るか:

- 自己学習型AIボット:急激に変化する市場トレンドに即座に適応するAI。

- 自動化されたアルファ発見:人間の認識よりも先に隠れた機会を特定する。

- 高度な社会的知性:インフルエンサー主導の物語を即座に解釈する。

- 完全にAI駆動のインフラストラクチャ:Edgen AIは包括的な投資プラットフォームへと進化しています。

研究に関するものから、University of Michigan highlights how AI and algorithmic systems are transforming modern financial markets、エッジンAIのようなプラットフォームが進んでいる方向を強化しています。

エッジンAIはすでにこの現実を構築しており、AIを基本的な市場の力として形作っています。

AI取引の革命はすでに到来している

AIはグローバルな金融市場を再構築しました:メンコインズ株式、暗号通貨、為替。高頻度取引からアルファ検出まで、AIがトレーディングの成功を定義します。

エッジンAIはこの革命をリードし、過酷な市場でトレーダーに戦略的な優位性を提供しています。AIを使わないトレーダーは、より速く動き、より明確に考え、完璧に実行する相手と競争することになります。

市場は進化した。人間同士の取引は消えた。今日ではAI同士の対決である。

準備ができていようがいまいが、そのEdgen AI 時代が到来した!

投資、もうひとりじゃない

Ed を無料で試そう。クレカ不要、縛りなし