Từ Cơ bản đến "Pumpamentals": Cách Tâm lý Xã hội Bây giờ Thúc đẩy Thị trường

Thị trường chuyển từ số liệu sang câu chuyện

Thị trường tài chính đã thay đổi. Các báo cáo lợi nhuận, bảng cân đối kế toán và các chỉ số truyền thống không còn chi phối sự biến động giá. Mạng xã hội là Wall Street hiện nay. Một tweet từ một người có ảnh hưởng mạnh, một meme lan truyền có thể làm tăng giá cổ phiếu trong vài phút.

Nhà đầu tư truyền thống quen thuộc với việc theo dõi báo cáo thu nhập, EBITDA và tỷ lệ nợ. Các nhà giao dịch hiện đại theo dõi tâm lý xã hội, các giao dịch ví blockchain và các câu chuyện thị trường lan truyền.Edgen AI cho phép các nhà giao dịch đọc tâm lý thị trường theo thời gian thực, phát hiện các thay đổi trước khi chúng xảy ra.

Cơ bản vs.PumpamentalsMột Thực tại Mới

Các yếu tố cơ bản tài chính là gì?

Đầu tư truyền thống tập trung vào các chỉ số sức khỏe của công ty:

- Tính khả thi về lợi nhuận

- Tăng trưởng doanh thu

- Ổn định tài chính

Tóm lại, các nhà đầu tư phân tích báo cáo quý, mức độ nợ và chất lượng quản lý.

PumpamentalsSự Bùng Nổ Của Giao Dịch Dựa Trên Sự Hype

Sau đó là các cổ phiếu meme. GameStop (GME), AMC và các tài sản tương tự tăng mạnh mà không có lợi nhuận vững chắc. Giá tăng mạnh do xu hướng trên mạng xã hội.

Các cộng đồng trực tuyến đã tạo ra làn sóng mua sắm khổng lồ, được thúc đẩy bởi sự hào hứng và tâm lý đám đông. Hiện tượng này (các nguyên lý bơm) hiện đã trở thành thực tế trên thị trường, chuyển đổi sự chú ý thành các chuyển động giá.

Vai trò quan trọng của AI trongPumpamentals

AI trở nên thiết yếu trong việc theo dõi và dự báo cảm xúc xã hội. Edgen AI tận dụng:

- Xu hướng đồng thuận Twitter/X

- Hoạt động ví blockchain thời gian thực (cảnh báo cá mập, tiền thông minh)

- Những câu chuyện thị trường mới về tài sản meme

Giao dịch mà không sử dụng công cụ AI có nghĩa là bỏ lỡ các tín hiệu alpha.Edgen AIgiúp các nhà buôn dự đoán các thay đổi thị trường từ sớm.

Sức mạnh của Tâm trạng Xã hội

Định nghĩa Cảm xúc Xã hội

Cảm xúc xã hội phản ánh sự nhiệt tình hoặc tiêu cực trực tuyến đối với các tài sản cụ thể. Các nhà giao dịch theo dõi Twitter, Reddit và các diễn đàn trực tuyến thấy phản ứng giá nhanh hơn so với truyền thông truyền thống.

Tại sao Tâm trạng đang định hình Giá cả hiện nay

- Thông tin Ngay Lập Tức: Mạng xã hội truyền tín hiệu tức thì, nhanh hơn tin tài chính truyền thống.

- Ảnh hưởng Bán lẻ: Các nhà đầu tư cá nhân tổ chức trực tuyến, thách thức tài chính truyền thống.

- Các Nhận định Dựa trên AI: Edgen AI theo dõi sự thay đổi cảm xúc tức thì, cung cấp các tín hiệu quan trọng từ sớm.

Theo dõi Cảm xúc bằng Trí tuệ Nhân tạo

Edgen AI liên tục quét mạng xã hội và giao dịch blockchain. Nhà giao dịch có lợi thế bằng cách:

- Phát hiện xu hướng vi-rút sớm

- Theo dõi các ví ảnh hưởng (tiền thông minh và cá mập)

- Đánh giá tác động của các người có ảnh hưởng chính (KOLs)

Giao dịch AI là thiết yếu đối với đầu tư hiện đại.

Cổ phiếu Meme và Hiện tượng Đầu tư Lan truyền

Cổ phiếu Meme, được định nghĩa

Cổ phiếu meme tăng nhanh do sự lan truyền trên mạng xã hội chứ không phải do cơ bản. Các nhà đầu tư bán lẻ phối hợp thông qua các cộng đồng như r/WallStreetBetstạo ra làn sóng mua sắm mạnh mẽ.

Cuộc bùng nổ giá cổ phiếu lịch sử của GameStop

GameStop (GME) giao dịch ở mức thấp cho đến khi các cộng đồng Reddit tập hợp lại.Hệ thống phối hợp quy mô lớnviệc mua đã kích hoạt một cuộc bán khống, đẩy giá cổ phiếu từ 20 đô la lên 500 đô la trong vài ngày.

Logic tài chính truyền thống không thể dự đoán được điều này. Xung lực do xã hội thúc đẩy chiếm ưu thế.

Tâm lý tài chính: Tại sao các nhà đầu tư theo đám đông

Nguyên nhân tâm lý đằng sauPumpamentals

Tài chính hành vi giải thích các quyết định trên thị trường do cảm xúc chứ không phải lý trí:Explore key behavioral biases and their impact on financial decisionsHãy dịch đoạn văn tiếng Anh sau sang tiếng Việt. Giữ nguyên cấu trúc và thuật ngữ kỹ thuật chính xác. Tránh dịch quá mức.

- Sự lo sợ bỏ lỡ (FOMO): Các nhà đầu tư nhanh chóng mua các tài sản đang tăng giá.

- Hành vi truyền bá: Mọi người tuân theo xu hướng phổ biến, bỏ qua các lời cảnh báo truyền thống.

- Thiên kiến xác nhận: Các nhà đầu tư ưu tiên thông tin phù hợp với niềm tin hiện tại, bỏ qua các rủi ro.

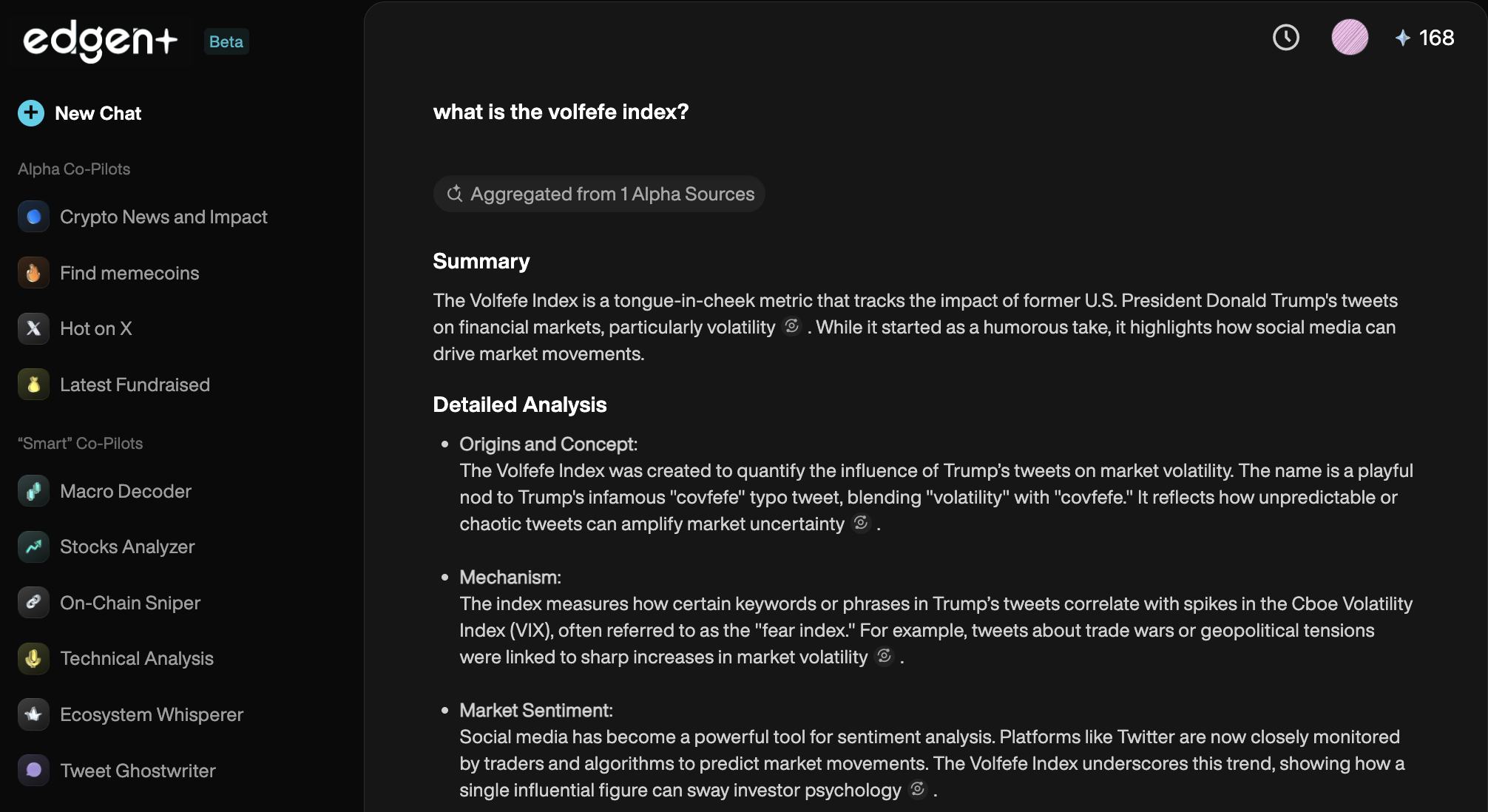

TheVolfefeChỉ số: Đo lường ảnh hưởng xã hội

Những người có ảnh hưởng như Elon Musk tác động đáng kể đến giá tài sản. Những bài đăng trên Twitter của Musk đã gây ra những biến động mạnh trong Dogecoin và Tesla.VolfefeChỉ số theo dõi tác động của thị trường từ các bài đăng xã hội có ảnh hưởng, nhấn mạnh tầm quan trọng của phân tích xã hội dựa trên AI như Edgen AI.

Dữ liệu Thay thế và Phân tích Cảm xúc Được Nâng Cao Bằng Trí Tuệ Nhân Tạo

Hiểu về Dữ liệu Thay thế

Đầu tư truyền thống sử dụng báo cáo tài chính và báo cáo quý. Bây giờ các nhà giao dịch tận dụng:

- Xu hướng mạng xã hội

- Giao dịch tiền mã hóa trên chuỗi (on-chain)

- Phân tích tìm kiếm Google

- Dữ liệu cảm xúc thị trường được điều khiển bởi AI

Dữ liệu thay thế tiết lộ cơ hội thị trường trước khi chúng được phản ánh trong hành động giá.

Edgen AI: Định hình tương lai của giao dịch

Cách Edgen AI Mang Lại Ưu Thế Cho Nhà Giao Dịch

Edgen AI cung cấp cơ sở hạ tầng giao dịch phía mua hoàn chỉnh, đồng thời theo dõi:

- Các chuyển động của ví thông minh (cá mập và người có ảnh hưởng)

- Sự đồng thuận xã hội và các câu chuyện lan truyền (Twitter/X)

- Sự thay đổi cảm xúc do AI thúc đẩy

Giao dịch hôm nay mà khôngNhững cái nhìn được thúc đẩy bởi AIgiống như đầu tư với bịt mắt.

Đặc điểm chính của Edgen AI:

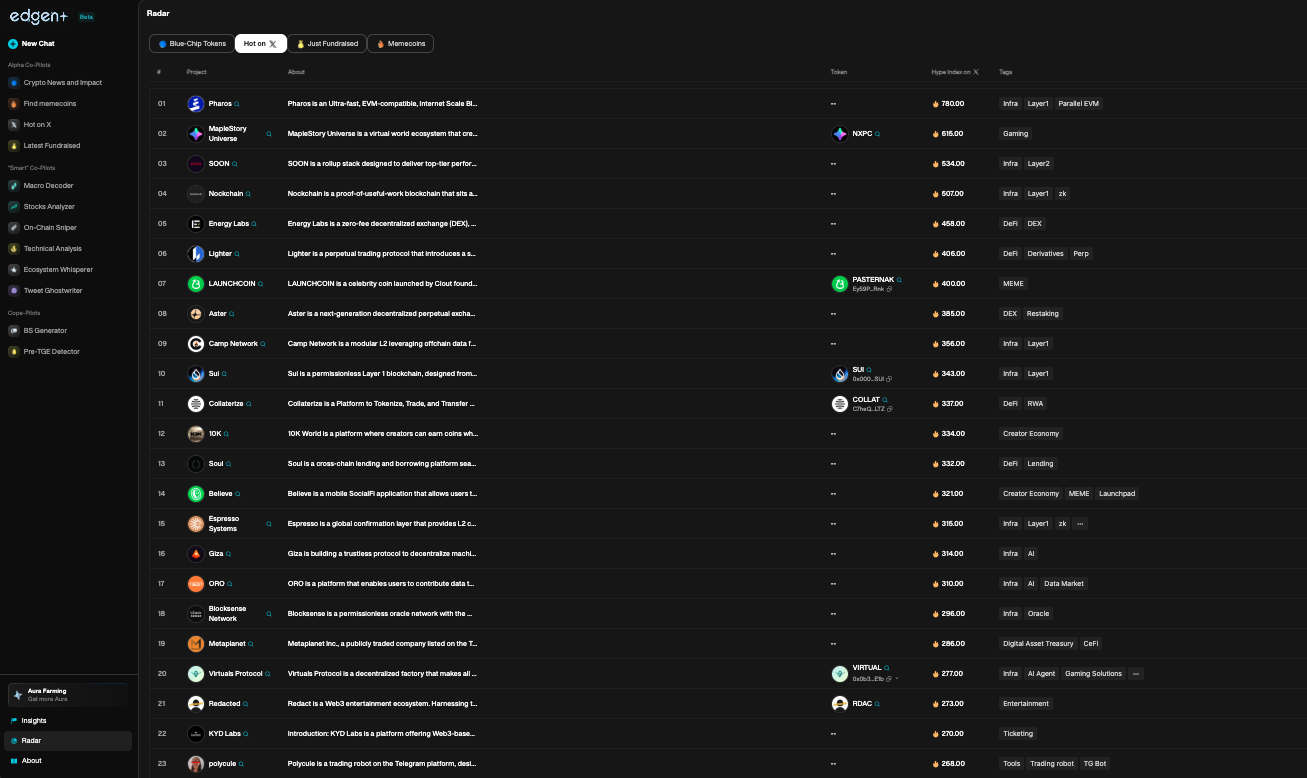

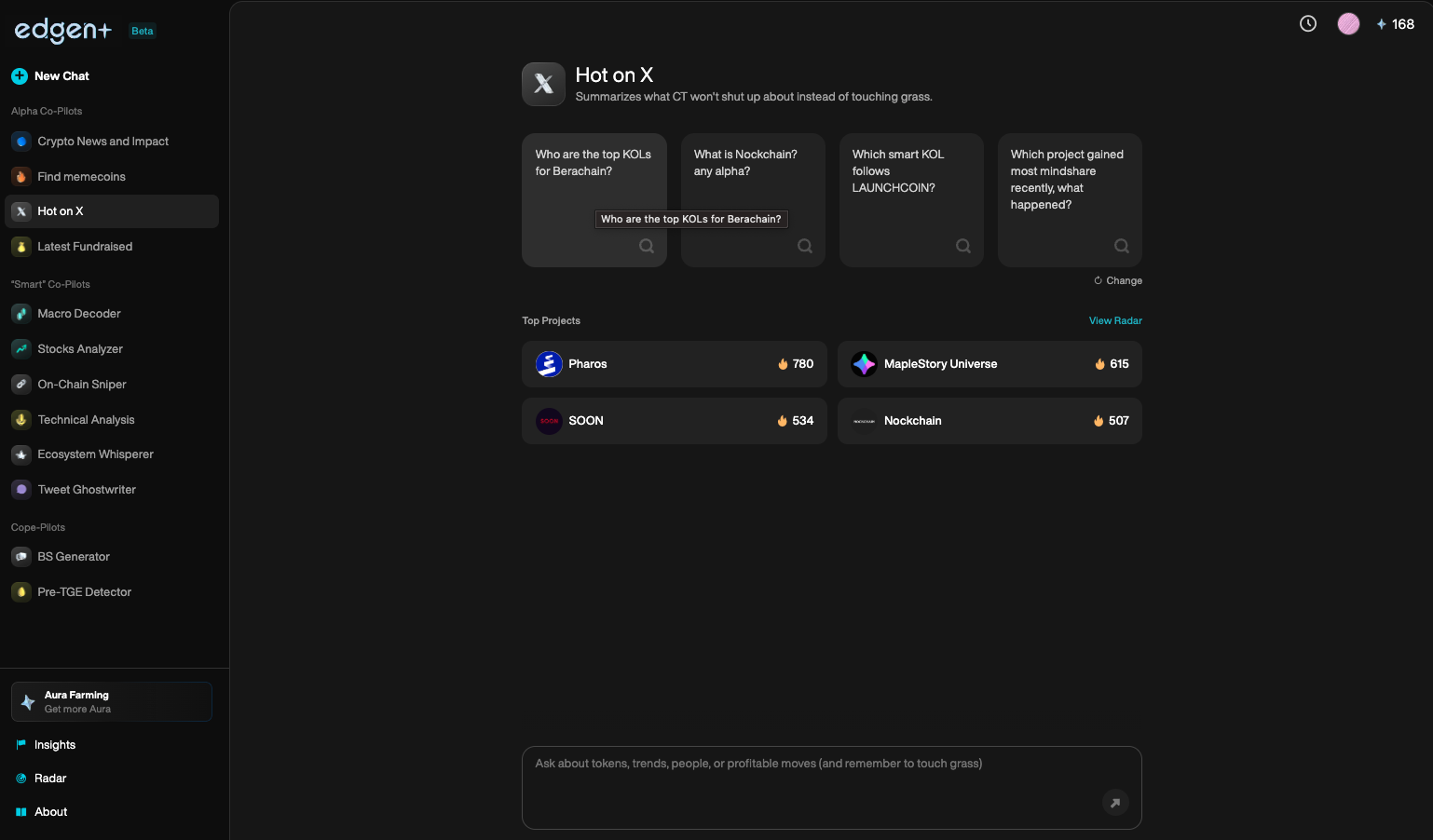

- Edgen RadarTheo dõi tâm lý thị trường và xu hướng theo thời gian thực.

- Edgen SearchCâu trả lời tức thì được hỗ trợ bởi các insight định hướng thị trường.

- Edgen InsightsThông tin thị trường alpha và kịp thời được thu thập từ cộng đồng.

Tại sao điều này lại quan trọng

Các tài sản meme và thị trường tiền mã hóa phát triển nhờ vào các chu kỳ hào hứng. Các nền tảng nhưWallStreetBetscho thấy động lực xã hội vượt trội hơn các chỉ số tài chính truyền thống trong biến động giá.

Edgen AIgiúp các nhà buôn xác định và thực hiện những điều nàycác nguyên lý bơmsớm, bắt giữ alpha trước khi xu hướng xuất hiện đầy đủ.

Thích nghi hoặc trở nên lỗi thời

Bối cảnh đầu tư đã thay đổi. Báo cáo tài chính riêng lẻ không còn là yếu tố thúc đẩy thị trường. Thay vào đó, tâm lý trên mạng xã hội, các câu chuyện từ người có ảnh hưởng và phân tích do AI dẫn dắt định hình giao dịch.

Edgen AI trang bị cho các nhà giao dịch để:

- Theo dõi và phản hồi các thay đổi về cảm xúc theo thời gian thực

- Giám sát các chuyển động của tiền thông minh

- Phản ứng quyết đoán với các câu chuyện thị trường mới nổi

Những nhà buôn bỏ qua các thông tin được dẫn dắt bởi AI sẽ đối mặt với những đối thủ giao dịch nhanh hơn, thông minh hơn và được cung cấp thông tin tốt hơn.

Tương lai đã đến. Thành công trong giao dịch hiện nay phụ thuộc vào khả năng bạn khai thác các công cụ AI. Thời đại củaEdgen AIgiao dịch bắt đầu. Hãy ở lạitrước, hoặcỞ lại phía sau. Lượt của bạn.

Đầu tư, cuối cùng không phải một mình nữa.

Dùng thử Edgen miễn phí. Không cần thẻ, không ràng buộc.