Edgen AI đang cách mạng hóa giao dịch tiền mã hóa với thông tin được hỗ trợ bởi trí tuệ nhân tạo

Tương lai của giao dịch tiền mã hóa là do AI điều khiển

Giao dịch tiền mã hóa là một con thú dữ không ngừng nghỉ. Giá cả biến động trong vài giây, chịu ảnh hưởng bởi mọi thứ từ các giao dịch của những "cá mập" lớn và giao dịch của các tổ chức đến những tweet lan truyền và sự gia tăng đột ngột trong tâm lý thị trường. Không ai, dù có kỹ năng đến đâu, có thể phân tích tất cả dữ liệu trên chuỗi, tiếng ồn xã hội và xu hướng giao dịch cùng lúc.

NhậpEdgen AItrợ lý giao dịch tiền mã hóa được xây dựng chính xác cho sự hỗn loạn này.

Edgen AI tận dụng phân tích thời gian thực trên chuỗi khối, trí tuệ nhân tạo tiên tiến và trí tuệ xã hội sâu sắc để phát hiện các cơ hội đầu tư tiền mã hóa có lợi nhuận trước khi thị trường phản ứng. Các công cụ giao dịch truyền thống có thể tập trung vào biểu đồ giá lịch sử và các chỉ số kỹ thuật, nhưng Edgen đi xa hơn: nó xử lý hoạt động chuỗi khối trực tiếp, cảm xúc xã hội và các thông tin được dẫn dắt bởi AI, mang lại cho người dùng một lợi thế giao dịch rõ ràng.

Bài viết này làm rõ chính xác cách Edgen AI chuyển đổi giao dịch tiền mã hóa và tại sao các thông tin nhận định được hỗ trợ bởi trí tuệ nhân tạo đại diện cho bước tiến tiếp theo trong thị trường tài chính.

Edgen AI là gì? Giao dịch Thông minh Hơn, Không Vất Vả Hơn

Một Cơ sở Hạ tầng Giao dịch Trí tuệ nhân tạo Thế hệ Mới

Edgen AIlà một nền tảng giao dịch AI phía mua thế hệ tiếp theo được thiết kế đặc biệt cho các nhà giao dịch tiền mã hóa cần độ chính xác, tốc độ và sự minh bạch thời gian thực. Nó kết hợp:

- Real-time On-chain AnalysisTheo dõi ngay lập tức các giao dịch blockchain, chuyển động của các quỹ lớn, dòng tiền lưu thông và các hoạt động quan trọng liên quan đến token.

- Thông tin thị trường được hỗ trợ bởi AI:Phát hiện các cơ hội giao dịch ẩn trước khi chúng trở nên rõ ràng.

- Theo dõi Trí tuệ Xã hộiTheo dõi các nhà ảnh hưởng, các chuyên gia có ảnh hưởng (KOLs) và tâm trạng cộng đồng theo thời gian thực để phát hiện các câu chuyện đang nổi lên.

Với Edgen AI, các nhà giao dịch có thể tự tin vượt qua những phức tạp của thị trường tiền mã hóa và liên tục thu được lợi nhuận vượt trội.

Tại sao Công cụ Truyền thống Không Thể Cạnh Tranh Với Edgen AI

Các công cụ tiền mã hóa truyền thống chủ yếu dựa vào dữ liệu giá lịch sử, đường xu hướng cơ bản và các chỉ báo kỹ thuật. Mặc dù các phương pháp này có thể đủ trong thị trường chậm, nhưng chúng không còn đáp ứng được trong bối cảnh hiện nay, nơi mà AI đang phát triển nhanh chóng.

Edgen AI phá vỡ cách tiếp cận truyền thống bằng cách:

- Phân tích dữ liệu chuỗi trực tiếp ngay lập tứcđể phát hiện các chuyển động thị trường ẩn trước khi các nhà giao dịch truyền thống nhận ra.

- Theo dõi cảm xúc xã hội thời gian thựcđể hiểu tâm lý thị trường và cộng đồng tiền mã hóa chủ đạocác nguyên lý bơm."

- Phát huy khả năng ra quyết định dựa trên trí tuệ nhân tạođể các nhà buôn có thể thực hiện các chiến lược một cách nhanh chóng, dựa trên dữ liệu thay vì cảm tính.

Sử dụng AI Edgen trực tiếp chuyển đổi thành các chiến lược thông minh hơn, hiểu biết sâu sắc hơn và thực hiện giao dịch nhanh hơn.

Sức mạnh của AI trong giao dịch tiền mã hóa: Lợi thế không công bằng của Edgen

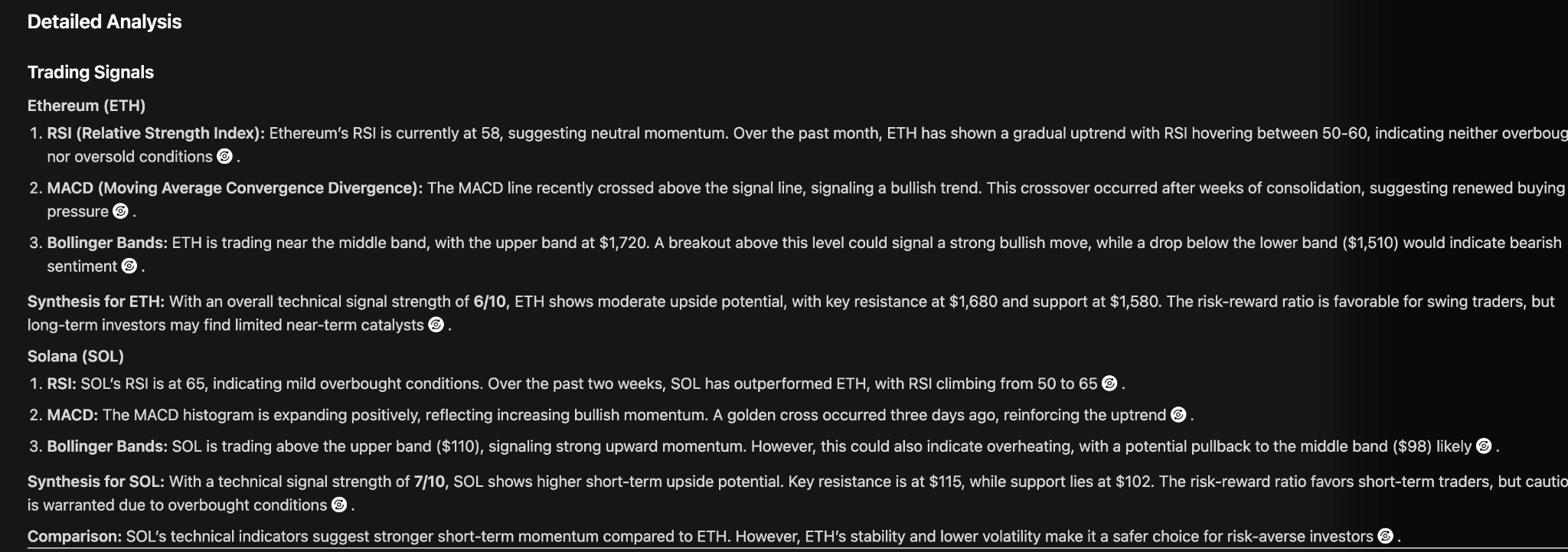

1. Phân tích dự đoán được hỗ trợ bởi AI

Thị trường tiền mã hóa có thể dường như ngẫu nhiên... cho đến khi bạn đưa AI vào. Edgen AI sử dụng phân tích dự đoán tinh vi để phát hiện các mẫu ẩn mà con người không thể nhận ra đủ nhanh:

- Quét hàng triệu điểm dữ liệu mỗi giây để dự báo biến động giá.

- Phát hiện các xu hướng thị trường mới nổi và bất thường trước khi chúng trở nên phổ biến.

- Theo dõi cảm xúc xã hội để xác định các câu chuyện và chu kỳ tăng giá ảnh hưởng đến thị trường.

Với Edgen AI, các nhà giao dịch chủ động hơn thay vì theo đuổi tin tức của ngày hôm qua.

2. Phân tích thị trường thời gian thực với dữ liệu trên chuỗi (on-chain data)

Bỏ qua chi phí dữ liệu blockchainnhà buôncơ hội quý giá. Edgen AI phân tích sâu vào các hoạt động trên chuỗi thời gian thực để phát hiện:

- Chuyển động của cá voiPhát hiện ngay lập tức các giao dịch lớn báo hiệu sự thay đổi giá quan trọng.

- Tương tác Hợp đồng Thông minhPhát hiện các tương tác ví quan trọng với các giao thức DeFi.

- Sự dịch chuyển thanh khoảnDự đoán biến động giá bằng cách theo dõi luồng thanh khoản của token trên các sàn giao dịch.

Tham quan Edgen Radarđể khám phá phân tích chuỗi khối thời gian thực.

3. Giao dịch được hỗ trợ bởi AI so với giao dịch thủ công

Giao dịch thủ công gây mệt mỏi, cảm xúc và dễ mắc sai lầm tốn kém. Edgen AI loại bỏ sự phỏng đoán này bằng cách:

- Quét thị trường 24/7 liên tục, không bao giờ bỏ lỡ một nhịp nào.

- Thực hiện giao dịch tự động dựa trên các tín hiệu chính xác, được dẫn dắt bởi dữ liệu.

- Loại bỏ hoàn toàn định kiến cảm xúc, tập trung nghiêm ngặt vào dữ liệu và chiến lược.

Các nhà buôn sử dụng chiến lược được thúc đẩy bởi AI thường vượt trội hơn những người chỉ dựa vào trực giác.

Đặc điểm chính làm nên sự khác biệt của Edgen AI

Phân tích thị trường toàn diện theo thời gian thực

- Xử lý dữ liệu trên chuỗi và ngoài chuỗi ngay lập tức.

- Giám sát liên tục thanh khoản, chuyển động của các ví lớn và các hoạt động quan trọng của ví.

- Theo dõi cảm xúc trên Twitter tiền mã hóa, Telegram và mạng lưới người có ảnh hưởng.

Khám phá Edgen’s real-time Feedtheo dõi hoạt động thị trường.

2. Tín hiệu giao dịch được hỗ trợ bởi AI

- Thông báo thời gian thực chỉ ra các cơ hội giao dịch có xác suất cao.

- Phân tích dự đoán xác định các token bị định giá thấp từ sớm.

- Các thuật toán tiên tiến tiết lộ các tín hiệu mua và bán ẩn trước khi được công chúng nhận biết.

3. Công cụ Quản lý Rủi ro Thông minh

- Đánh giá rủi ro được thúc đẩy bởi AI để cảnh báo các nước đi có thể gây rủi ro.

- Các khuyến nghị dừng lỗ thông minh và định mức vị thế được tùy chỉnh theo điều kiện thị trường.

- Các hồ sơ rủi ro linh hoạt thích ứng với sở thích của nhà giao dịch.

4. Chiến lược giao dịch tự động

- Thực hiện giao dịch dựa trên AI ngay lập tức dựa trên thông tin thị trường thời gian thực.

- Giao dịch không bị ảnh hưởng bởi cảm xúc, loại bỏ các quyết định bốc đồng.

- Giám sát liên tục đảm bảo bạn tận dụng mọi cơ hội có thể.

Bắt đầu với Edgen searchđể phát hiện các tín hiệu giao dịch và cơ hội thị trường.

Tương lai của AI trong giao dịch tiền mã hóa: Khát vọng của Edgen

1. Dự đoán thị trường được cải tiến nhờ trí tuệ nhân tạo

Trong những năm tới, các nền tảng do AI dẫn dắt như Edgen sẽ:

- Dự báo xu hướng thị trường chính xác hơn nữa.

- Khám phá các tín hiệu alpha ẩn mà các nhà giao dịch con người đơn giản không thể phát hiện.

- Giảm thiểu rủi ro giao dịch thêm nữa với các mô hình dự đoán tiên tiến hơn.

2. Dữ liệu trên chuỗi trở nên thiết yếu

- AI sẽ chuẩn hóa việc theo dõi nhanh các xu hướng DeFi, giao dịch của các "whale" và tâm lý xã hội.

- Tính minh bạch từblockchain datasẽ trở thành nền tảng cho các chiến lược thành công.

3. Sự thống trị của giao dịch AI tự động

- Các robot giao dịch được hỗ trợ bởi AI sẽ trở thành tiêu chuẩn thay vì ngoại lệ.

- Giao dịch thủ công sẽ giảm đáng kể khi AI liên tục chứng minh được hiệu quả vượt trội.

Edgen AI đang ở vị trí lý tưởng để dẫn đầu sự thay đổi này.

Giao dịch Thông minh Hơn, Bắt Đầu Ngay Hôm Nay Với Edgen AI

Giao dịch tiền mã hóa đang phát triển nhanh chóng, và tương lai chắc chắn thuộc về các nhà giao dịch được điều khiển bởi AI. Edgen AI cung cấp cho bạn các công cụ cần thiết để:

- Khám phá thông tin thị trường sâu sắc hơn, cải thiện việc ra quyết định và lợi nhuận.

- Tận dụng phân tích chuỗi khối thời gian thực để luôn đi trước một bước.

- Loại bỏ cảm xúc khỏi giao dịch, để dữ liệu dẫn đường.

Đừng giao dịch khó hơn: hãy giao dịch thông minh hơn.Đón nhận tương lai giao dịch tiền mã hóa dựa trên AI ngay hôm nay với Edgen AIvà luôn đi trước thị trường.

Ưu điểm SEO của bài viết

✅Tiêu đề & Mô tả Meta Mạnh:

- Tiêu đề chứa từ khóa và hấp dẫn.

- Mô tả meta ngắn gọn và hấp dẫn, tóm tắt các điểm chính đồng thời bao gồm các từ khóa liên quan như"Những cái nhìn được hỗ trợ bởi AI","trading tiền mã hóa", v.v.

✅Sử dụng hiệu quả các tiêu đề (H1, H2, H3, v.v.)

- Bài viết được trình bày rõ ràng với các tiêu đề rõ ràng.

- Nó bao gồm các chủ đề chính theo thứ tự hợp lý, điều này cải thiện khả năng đọc và SEO.

✅Tối ưu hóa từ khóa:

- Bài viết bao gồm các từ khóa có giá trị cao liên quan đến tiền mã hóa và trí tuệ nhân tạo như:

- "Những cái nhìn được hỗ trợ bởi AI,"

- "trên"dữ liệu chuỗi,"

- "alphacác tín hiệu giao dịch,

- "phân tích thị trường thời gian thực,"

- Những từ khóa này giúp cải thiện thứ hạng cho các tìm kiếm liên quan đến giao dịch tiền mã hóa được điều khiển bởi AI.

✅Độ sâu nội dung và chuyên môn:

- Bài viết cung cấp những hiểu biết chi tiết, các trường hợp nghiên cứu và giải thích, cho thấy sự chuyên môn về chủ đề này.

- Google ưu tiên nội dung được nghiên cứu kỹ lưỡng và sâu sắc cho thứ hạng SEO.

✅Khả năng đọc và tương tác:

- Các đoạn văn ngắn và ngôn ngữ đơn giản, trực tiếp cải thiện trải nghiệm người dùng và thời gian lưu trú.

Đầu tư, cuối cùng không phải một mình nữa.

Dùng thử Edgen miễn phí. Không cần thẻ, không ràng buộc.