Giao dịch Alpha trong Tiền mã hóa: AI Khai thác Tín hiệu Thị trường Ẩn

Thị trường Tiền mã hóa thưởng cho Tốc độ và Chính xác

Giao dịch tiền mã hóa diễn ra nhanh chóng. Các giao dịch mang lại lợi nhuận phụ thuộc rất nhiều vào việc nhận diện xu hướng thị trường một cách rõ ràng và sớm. Các nhà giao dịch con người thường bỏ lỡ các tín hiệu quan trọng do tốc độ và phạm vi phân tích bị giới hạn.

Trí tuệ nhân tạo xử lý các tập dữ liệu khổng lồ một cách tức thì, nhận diện rõ ràng những chuyển động và tín hiệu thị trường ẩn trước khi người khác nhận ra.

Điều này định nghĩa "giao dịch alpha": nhận thấy cơ hội thị trường trước và thực hiện giao dịch nhanh hơn đối thủ cạnh tranh.Edgen AIđặt ra tiêu chuẩn mới, trao quyền cho các nhà giao dịch với những thông tin có thể hành động và kịp thời.

Giao dịch không có AI khiến các nhà đầu tư tụt hậu. Đây là lý do tại sao AI định hình tương lai của giao dịch tiền mã hóa và cách Edgen AI giúp nó trở nên dễ tiếp cận ngay hôm nay.

Hiểu về Giao dịch Alpha trong Tiền mã hóa

Giao dịch Alpha nghĩa là có được những nhận thức rõ ràng, sớm về các cơ hội sinh lời trước khi phần lớn thị trường nhận ra. Thị trường tiền mã hóa vẫn rất biến động, hoạt động 24/7, đòi hỏi việc giám sát liên tục và chính xác.

AI cung cấp phân tích liên tục, thời gian thực một cách rõ ràng:

- Dữ liệu trên chuỗi:Theo dõi giao dịch blockchain theo thời gian thực.

- Xu hướng thị trường:Nhận diện các mô hình mang lại lợi nhuận trước khi chúng trở nên rõ ràng đối với đại chúng.

- Cảm xúc Xã hội:Phân tích dữ liệu từ X (trước đây là Twitter), Telegram, các nguồn tin tức và chủ đề đang được quan tâm.

Khác với các công cụ phân tích truyền thống, Edgen AI đi xa hơn dữ liệu lịch sử, làm rõ tâm lý thị trường hiện tại:

- Theo dõi các KOL có ảnh hưởng trên các nền tảng như X.

- Giám sát các giao dịch ví thông minh quan trọng.

- Phân tích "Pumpamentals"tốc độ lan truyền xã hội thúc đẩy giá tiền mã hóa.

Tại sao Giao dịch Alpha Quan trọng Hơn Bao giờ hết

Trong Web3, các chỉ số tài chính truyền thống cung cấp cái nhìn không đầy đủ. Các thị trường tiền mã hóa hiện đại dựa trên tâm lý xã hội và hoạt động chuỗi khối, rõ ràng nhìn thấy được theo thời gian thực.

- Các Giao dịch Thông minh & Bán:Tiền thông minh di chuyển nhanh. AI phát hiện các giao dịch tập hợp của họ ngay lập tức.

- Cảm giác của Nhà buôn bán lẻ:Xu hướng xã hội nhanh chóng xuất hiện. Trí tuệ nhân tạo nhận diện và tận dụng những xu hướng này trước khi có sự bùng phát lan rộng.

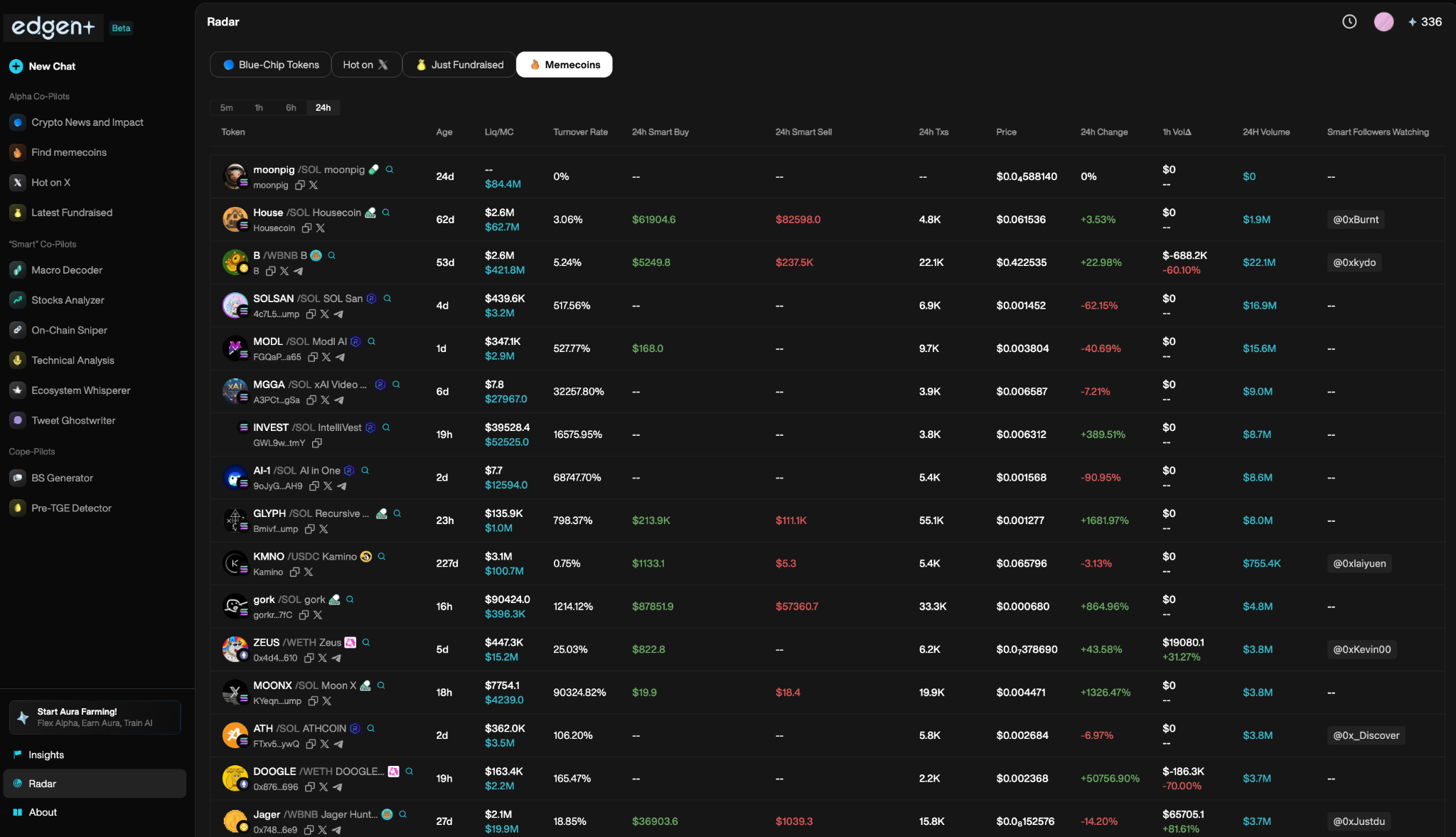

Edgen RadarvàEdgen Searchđảm bảo các nhà buôn có thể nhận thấy ngay lập tức những bước chuyển quan trọng trong thị trường này.

Làm thế nào AI Làm nổi bật các tín hiệu thị trường ẩn một cách rõ ràng

Công nghệ trí tuệ nhân tạo cách mạng hóa giao dịch tiền mã hóa, xử lý tức thì hàng triệu điểm dữ liệu và nắm bắt các tín hiệu tinh tế mà các nhà giao dịch con người bỏ lỡ.

1. Tín hiệu giao dịch AI thời gian thực

Edgen AI tạo ra ngay lập tức các tín hiệu giao dịch rõ ràng và có thể thực hiện được bằng cách phân tích:

- Các Biến Động Giá:Các mô hình lịch sử chỉ ra các cơ hội sinh lời.

- Sự thay đổi khối lượng giao dịch:Phát hiện các đợt tăng hoạt động thị trường bất thường ngay lập tức.

- Động lực Xu hướng Xã hội:Đo lường sự tham gia của cộng đồng và sự hào hứng để dự đoán xu hướng giá cả.

Edgen Radartrình bày rõ ràng bức tranh thị trường xã hội và kỹ thuật để thực hiện các hành động giao dịch chính xác.

2. Phân tích cảm xúc tức thì

AI liên tục phân tích dữ liệu từ X và các hãng tin tức, đọc cảm xúc thị trường trước khi nó ảnh hưởng rõ rệt đến hành động giá.

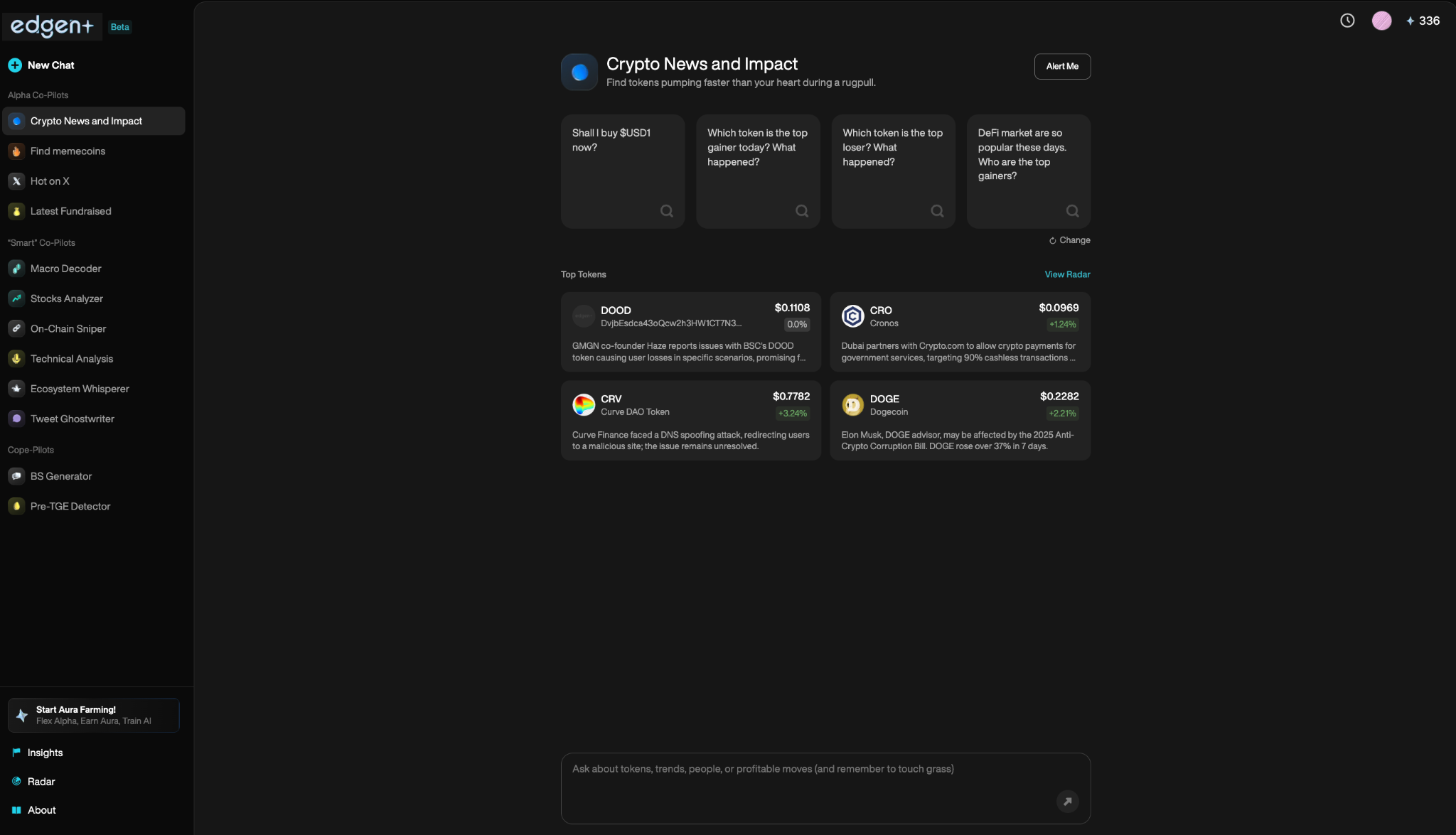

Các nhà buôn sử dụngEdgen Search, hỏi các câu hỏi thời gian thực và nhận được phản hồi tức thì dựa trên dữ liệu.

3. Giám sát dữ liệu thị trường liên tục

Thị trường hoạt động liên tục. AI theo dõi không ngừng:

- Giao dịch Cá voi: Giám sát tức thì các hoạt động của ví có ảnh hưởng.

- Tiếng ồn Xã hội: Phát hiện sớm các máy bơm do cộng đồng thúc đẩy và sự thay đổi cảm xúc.

- Thay đổi Khối lượng: Cảnh báo tức thì về những thay đổi quan trọng trong thanh khoản thị trường.

Các nhà giao dịch AI Edgen nhận được cảnh báo thời gian thực, giúp đưa ra quyết định giao dịch tức thì và có thông tin chính xác.

Tác động của AI đến độ chính xác và độ chính xác trong giao dịch

Giao dịch tiền mã hóa mang lại lợi nhuận đòi hỏi phân tích chính xác và không cảm xúc. Trí tuệ nhân tạo đảm bảo độ chính xác rõ ràng bằng cách:

- Loại bỏ các quyết định mang tính cảm xúc: Trí tuệ nhân tạo đưa ra quyết định dựa hoàn toàn trên dữ liệu chứ không phải trên cảm xúc chủ quan.

- Lọc các tín hiệu can thiệp: Xác định rõ và tránh các cuộc bơm giả do bot tạo ra.

- Dự đoán các thay đổi thị trường: Nhận diện xu hướng cảm xúc mới nổi một cách rõ ràng, trước khi có phản ứng rộng rãi trên thị trường.

Theo đóInternational Monetary Fund,AI đang định hình lại thị trường tài chính toàn cầu, khiến chúng hiệu quả hơn nhưng cũng nhạy cảm hơn với biến động dựa trên dữ liệu.

Edgen AI kết hợp phân tích blockchain, dữ liệu xã hội và các insight AI rõ ràng, đảm bảo các nhà giao dịch hành động dựa trên các tín hiệu thực sự.

Tương lai: Trí tuệ nhân tạo sẽ định hình giao dịch Alpha như thế nào

Vai trò của AI trong tiền mã hóa tiếp tục phát triển, mang lại lợi ích rõ rệt cho các chiến lược giao dịch:

1. Tối ưu hóa danh mục đầu tư được tăng cường bởi AI

Các nhà môi giới sẽ ngày càng sử dụng trí tuệ nhân tạo để quản lý danh mục đầu tư tự động, rõ ràng tối ưu hóa lợi nhuận dài hạn.

2. Phân tích chuỗi khối tiên tiến

AI sẽ cung cấp cái nhìn sâu sắc hơn về các hoạt động hợp đồng thông minh và hành vi của ví cá mập với độ chính xác được cải thiện. Edgen Radar đã cung cấp khả năng theo dõi rõ ràng các ví có ảnh hưởng và tác động của chúng đến thị trường.

3. Phân tích thị trường dự đoán cải tiến

Dự báo bằng AI sẽ trở nên rõ ràng và chính xác hơn, cho phép các nhà giao dịch lên kế hoạch giao dịch một cách tự tin từ vài tuần đến vài tháng trước.

4. Theo dõi Tâm lý Thị trường Tinh chế

Phân tích cảm xúc xã hội sẽ tiếp tục được cải thiện, cảnh báo rõ ràng cho các nhà giao dịch ngay lập tức khi sự nhiệt tình của thị trường bắt đầu hình thành. Edgen AI dẫn đầu quá trình này, tích hợp liền mạch trí tuệ nhân tạo, dữ liệu blockchain và trí tuệ xã hội.

AI Định Nghĩa Lợi Thế Giao Dịch Tiền Điện Tử Tuyệt Đối

Trí tuệ nhân tạo đã định hình lại thị trường tiền mã hóa. AI xác định rõ các tín hiệu alpha, tự động hóa giao dịch chính xác và cải thiện đáng kể độ chính xác trong việc ra quyết định.

Edgen AI vẫn đứng đầu, tích hợp rõ ràng phân tích blockchain, thông tin thị trường tức thời và cái nhìn xã hội theo thời gian thực vào một giải pháp giao dịch toàn diện.

Các nhà giao dịch tiền mã hóa sử dụng trí tuệ nhân tạo hôm nay sẽ rõ ràng thống trị bức tranh thị trường của ngày mai.

Giữ vững vị trí dẫn đầu. Đón nhận giao dịch được điều khiển bởi AI vớiEdgen AI

Đầu tư, cuối cùng không phải một mình nữa.

Dùng thử Edgen miễn phí. Không cần thẻ, không ràng buộc.