Làm thế nào AI có thể mang lại lợi thế: Bí mật đằng sau giao dịch Alpha

Alpha Trading: Sự Cạnh Tranh Mà Mọi Người Đều Mơ Ước (Nhưng Ít Ai Bắt Được)

Mỗi nhà giao dịch đều tìm kiếm Alpha. Ý tưởng vượt trội thị trường mà mọi người muốn trước tiên, nhưng ít ai phát hiện đủ sớm để thu được lợi nhuận lớn.

Lưu ý: Giao dịch được hỗ trợ bởi AI là mã lừa đảo.

Một khi Alpha đến Twitter Tiền mã hóa, nó không còn là Alpha nữa, chỉ còn lại những mảnh vụn. Phân tích thị trường truyền thống đơn giản không thể theo kịp lượng dữ liệu liên tục về chuỗi khối, kỹ thuật và xã hội.

Nhập Edgen AI—biến hỗn loạn thành sự rõ ràng, các mô hình thành lợi nhuận, và các nhà giao dịch thành huyền thoại.

Vậy Alpha Trading Là Gì?

Alpha nghĩa là vượt qua các chỉ số thị trường.Đó là cách các quỹ đầu cơ, những người giàu có và các nhà giao dịch degen duy trì lợi nhuận bất kể thị trường đang tăng hay giảm.

Các công cụ giao dịch truyền thống như biểu đồ và các chỉ báo cơ bản? Chúng tuyệt vời cho danh mục cổ phiếu của thế hệ boomer, nhưng không phù hợp với môi trường nhanh chóng và khắc nghiệt của crypto.

Ngày hôm nay, Alpha yêu cầu giải mã cảm xúc xã hội ("pumpamentals")), theo dõi chuyển động cá voi thời gian thực qua dữ liệu trên chuỗi, và xác định các xu hướng ẩn trước khi những người bình thường bắt chước.

Edgen AI làm tốt sự kết hợp này với:

- Phân tích được cấp bằng AI để đưa ra các quyết định giao dịch thông minh và nhanh chóng.

- Thông tin trên chuỗi để theo dõi chuyển động của cá mập và dòng tiền thời gian thực.

- 📢 Giải mã xu hướng từ các KOLs (Người có ảnh hưởng chính) bằng Trí tuệ Xã hội.

Đường viền ba lớp này có nghĩa là ít điểm mù hơn, Alpha sắc nét hơn và ít thời gian lướt Twitter để tìm tín hiệu.

AI: Não Gian Giao Dịch Của Bạn Với Steroids

Trí tuệ nhân tạo trong giao dịch giống như việc bạn đổi chiếc xe đạp gỉ sét của mình lấy một tên lửa.EdgenAI xử lý dữ liệu khổng lồ trong vài giây, một nhiệm vụ mà các nhà giao dịch con người có thể mất hàng tuần để giải mã.

Tín hiệu Alpha Đã Được Cung Cấp Bằng AI: Sức Mạnh Mới Của Bạn

- Phát hiện mẫu:AI nhận thấy các xu hướng mà con người không thể.

- Ra quyết định nhanh chóng:Tiêu hóa dữ liệu tức thì.

- Logic Không Cảm Xúc:Tạm biệt việc bán tháo hoảng loạn và mua theo tâm lý FOMO.

- Dự đoán Tốt Hơn:Edgenhọc từ dữ liệu lịch sử và thời gian thực để đưa ra dự báo chính xác hơn một cách nhất quán.

Phần tốt nhất?EdgenAI tổng hợp các xu hướng xã hội, tin tức nóng và dữ liệu blockchain, cung cấp cái nhìn toàn diện 360° về thị trường nhanh hơn bạn kịp nói "wen moon".

Thực tế, một study by NBERcho thấy các mô hình học máy dự đoán khối lượng giao dịch có thể tạo ra lợi nhuận ở cấp độ Alpha, ủng hộ sức mạnh đằng sau các công cụ giao dịch AI như Edgen.

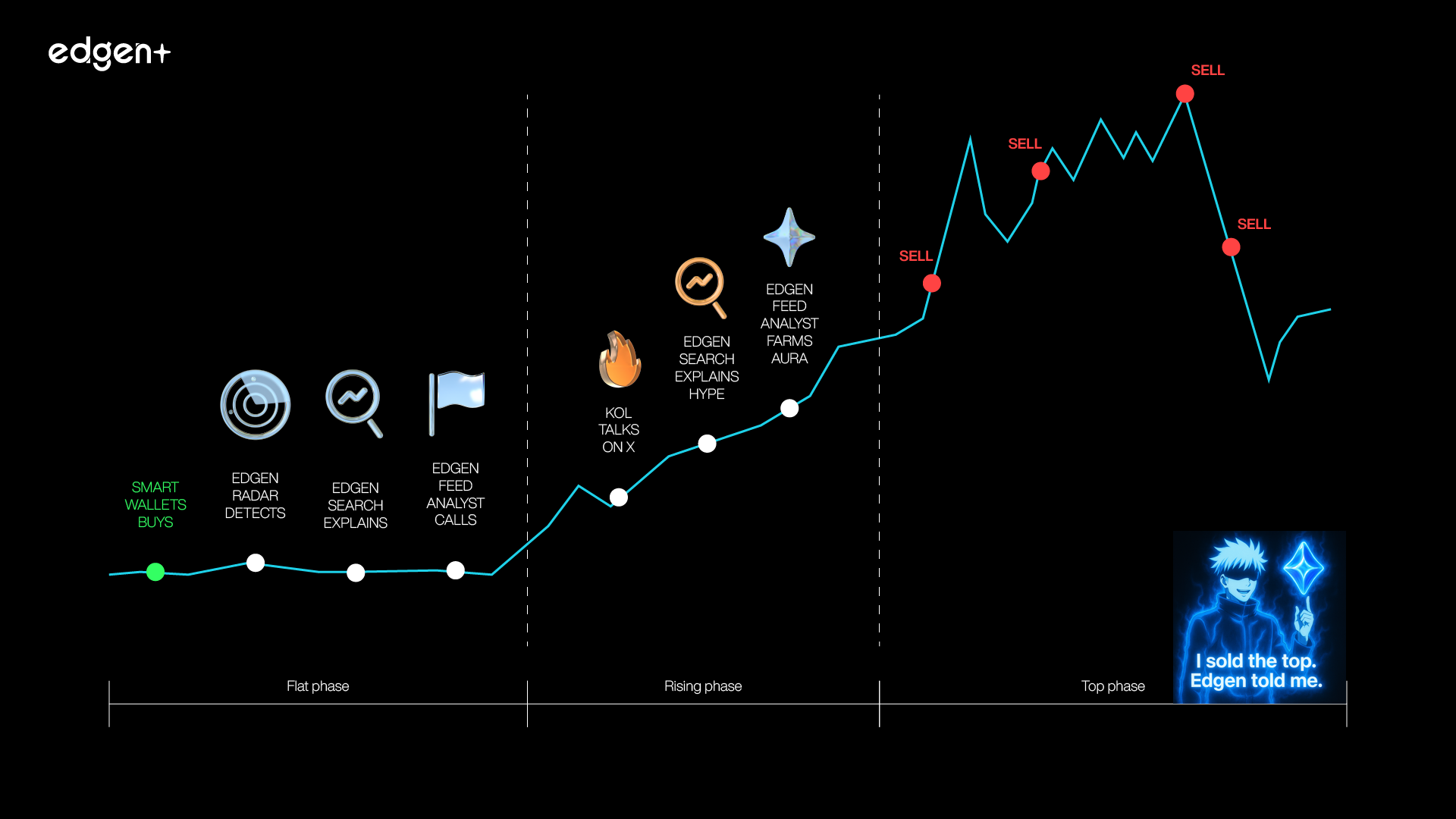

Quan sát Cá voi 2.0: Sức mạnh của Dữ liệu Trên Chuỗi

Tính minh bạch của blockchain có nghĩa là các bên lớn không còn thể giấu những bước đi của họ nữa. Với dữ liệu trên chuỗi, bạn sẽ thấy:

- Số lượng ví thông minh đang tích lũy (hoặc bán tháo) là bao nhiêu.

- Các token đang tăng tốc nhanh.

- Làm thế nào sự hào nhoáng xã hội và các tài khoản thông minh ảnh hưởng trực tiếp đến giá trị của token.

Hãy quên đi việc đoán mò. VớiEdgenTheo dõi chuỗi khối thời gian thực của AI, Alpha trở nên rõ ràng và dễ tiếp cận với bất kỳ ai.

Lợi ích thực tế:

- Nhận biết các bước đi của tiền thông minh trước khi giá tăng mạnh.

- Theo dõi sự dịch chuyển thanh khoản giữa các sàn giao dịch tập trung (CEX) và các sàn giao dịch phi tập trung (DEX).

- Giải mã tác động của tâm trạng xã hội đến hành động thị trường.

Kết quả? Các giao dịch đạt mục tiêu, quản lý rủi ro được cải thiện, và danh mục đầu tư của bạn cuối cùng cũng có những cây nến xanh.

4 Bước để Tối đa Hóa Lợi Nhuận Với Trí Tuệ Nhân Tạo và Dấu Hiệu Alpha

Sẵn sàng nâng cấp từ người chơi nghiệp dư lên chuyên nghiệp? Đây là bản thiết kế của bạn:

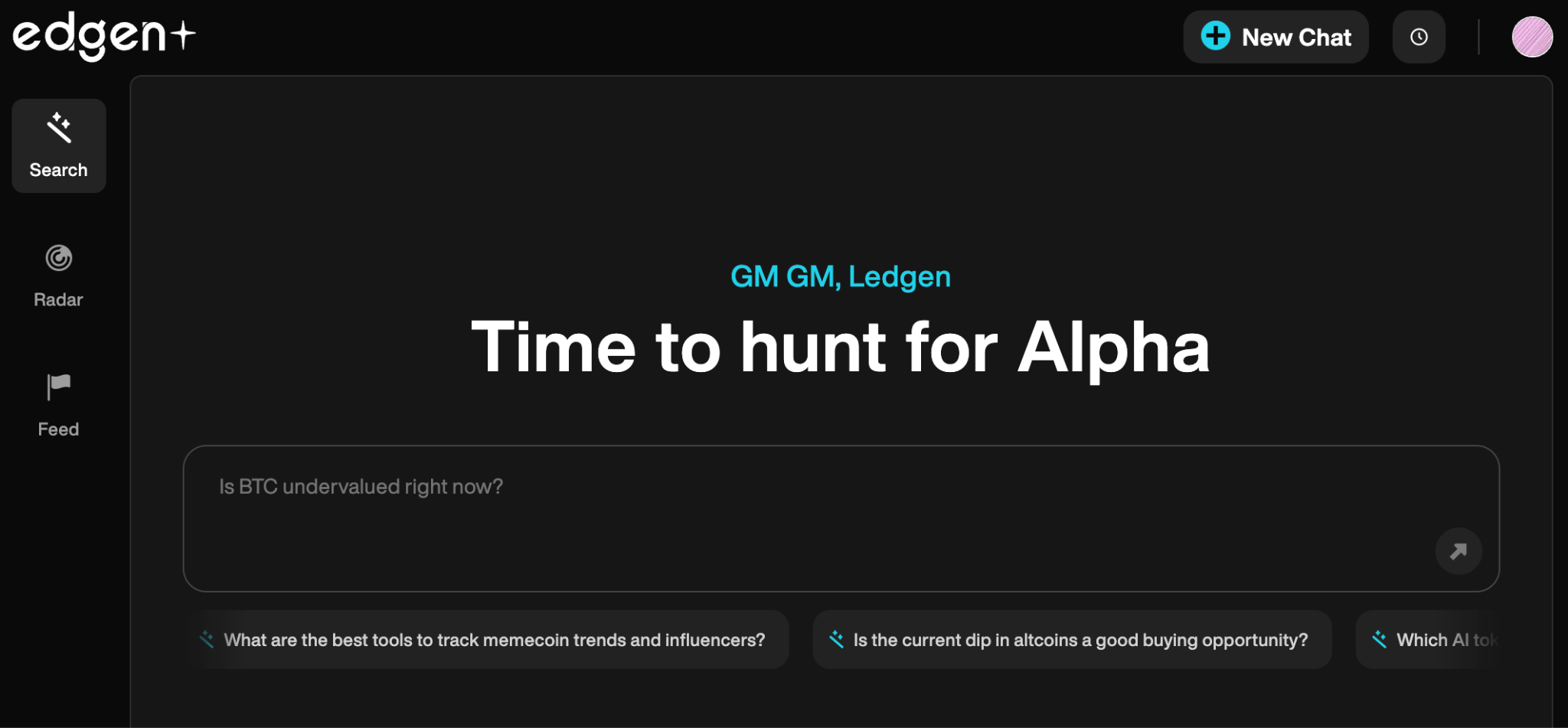

1. Sử dụng Edgen Search để tiến hành khám phá nhanh chóng

Nhận ngay các thông tin nhận diện do AI cung cấp và phân tích sâu trên chuỗi khối vềEdgen SearchBiết mọi thứ, mà không cần đọc hết mọi thứ.

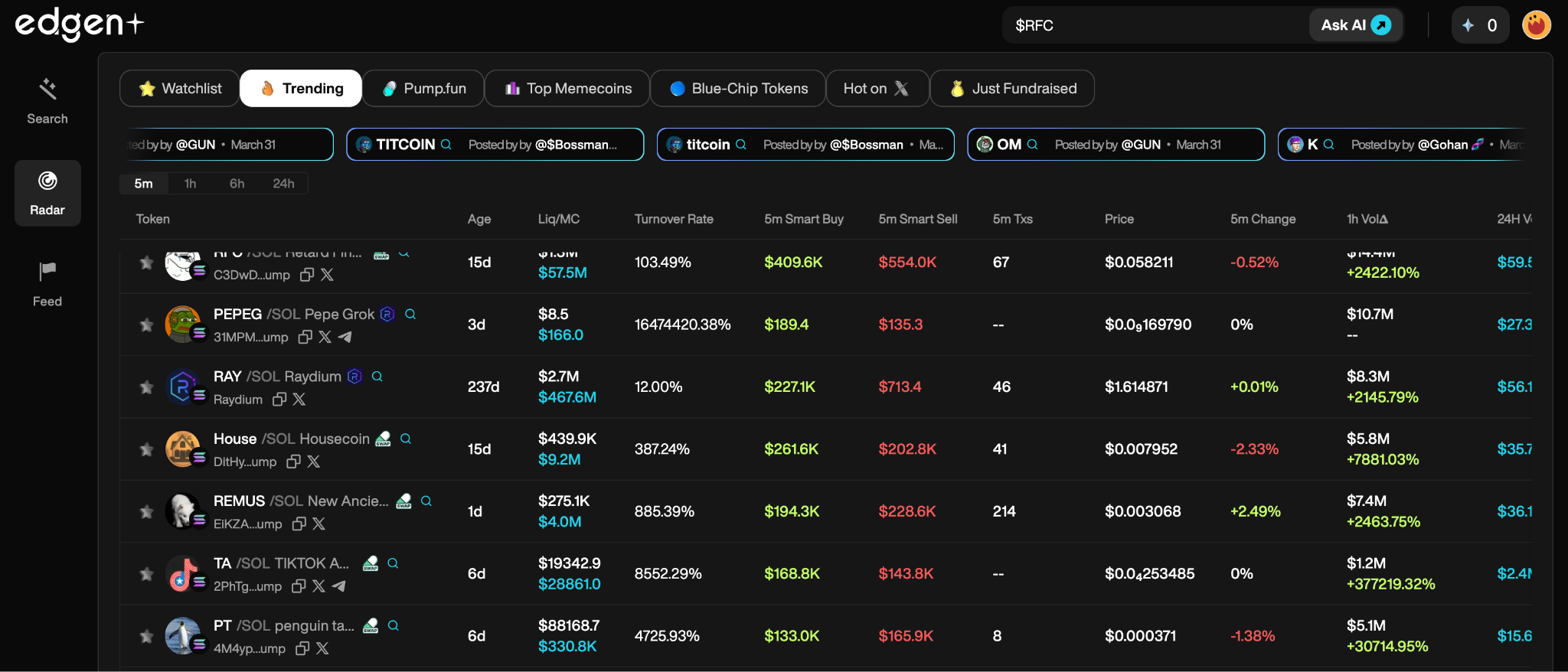

2. Theo dõi Xu hướng Nóng Với Edgen Radar

Edgen RadarBắt tín hiệu cá voi sớm và các yếu tố xã hội trước người khác nhận ra. Phản ứng nhanh, không nên chậm trễ.

3. Quản lý rủi ro: Ngừng giao dịch như một người mới bắt đầu

AI cung cấp các đánh giá rủi ro lạnh lùng, không thiên vị. Đừng bắt chước chi phí thuê nhà của bạn. Giao dịch như các chuyên gia làm.

4. Duy trì sự tập trung vào các thay đổi của thị trường

Tiền mã hóa không chờ ai. Thường xuyên tận dụngEdgen SearchvàRadarđể thay đổi chiến lược nhanh hơn thị trường có thể lừa bạn.

Alpha Trading với Trí tuệ nhân tạo và Dữ liệu trên chuỗi: 5 Câu hỏi thường gặp hàng đầu cho các nhà giao dịch nghiêm túc

1. Alpha trading là gì?

Giao dịch Alpha là việc vượt qua thị trường một cách nhất quánbằng cách phát hiện các giao dịch có lợi nhuận, rủi ro thấp từ sớm.EdgenAI cung cấp cho bạn các tín hiệu AI thời gian thực và dữ liệu trên chuỗi để giao dịch thông minh và nhanh hơn.

2. AI làm cho giao dịch Alpha nhanh hơn như thế nào?

AI quét dữ liệu khổng lồ một cách nhanh chóng, phát hiện các mô hình ẩn, loại bỏ thiên lệch cảm xúc và cải thiện độ chính xác của các dự báo thị trường. VớiEdgenAI, bạn sẽ thấy những bước đi trước khi những người đến muộn có thể tweet "Điều gì đang được đẩy mạnh?"

3. Tại sao tôi nên quan tâm đến dữ liệu trên chuỗi?

Dữ liệu chuỗi khối thời gian thực tiết lộ hoạt động của các "whale", xu hướng token và sự dịch chuyển thanh khoản. Giao dịch dựa trên bằng chứng, không phải cảm xúc — luôn bắt chước trước, lợi nhuận sau.

4. Điều gì khiến Edgen AI tốt hơn?

Edgenkết hợp độ chính xác của AI, thông tin phân tích chuỗi khối thời gian thực và phân tích cảm xúc xã hội. Không có điểm mù, không cần đoán mò—chỉ có Alpha rõ ràng và có thể hành động.

5. Edgen có đảm bảo giao dịch có lợi nhuận không?

Không. Không có phép thuật ở đây. NhưngEdgennâng cao đáng kể khả năng của bạn với thông tin thời gian thực và phân tích dự đoán. Quản lý rủi ro vững chắc vẫn rất quan trọng.Edgengiúp bạn thông minh hơn, không phải làm nhiều hơn.

Đảm bảo lợi thế giao dịch của bạn trong tương lai

Các thông tin nhận định từ AI và chuỗi khối là bắt buộc hiện nay. Edgen AI cung cấp đầy đủ những gì bạn cần để thống trị thị trường tiền mã hóa ngày nay:

- Phân tích được hỗ trợ bởi AI.

- ⛓️ Dữ liệu chuỗi khối thời gian thực.

- 📈 Giải mã xu hướng xã hội ("pumpamentals")

Với Edgen AI, không nhà giao dịch nào phải giao dịch mù mờ nữa. Phát hiện xu hướng trước, giao dịch tự tin và cuối cùng bắt đầu thu về Alpha thực sự.

Chào mừng bạn đến với tiêu chuẩn giao dịch mới. Lợi thế Alpha của bạn đã được nâng cấp.

Đầu tư, cuối cùng không phải một mình nữa.

Dùng thử Edgen miễn phí. Không cần thẻ, không ràng buộc.