今日AI交易:为何智能钱包和KOL主导市场(现已集成Edgen AI)

AI交易已变得不可阻挡

2025年,人工智能交易正在重塑金融市场——速度更快、更智能,也比以往任何时候都更容易获取。

智能钱包和关键意见领袖(KOL)推动着这一新的交易时代。他们的见解和技术使所有交易者,从新手到专家,都能平等地参与市场。

传统的投资方式已不复存在。现在,交易者通过链上分析、阿尔法信号和社会驱动的市场趋势获得优势。

根据 Wharton University of Pennsylvania人工智能正在通过使系统能够生成新的交易策略、执行交易并实时适应市场状况,从而革新金融行业,进而改变金融服务的格局。

Edgen AI“能够洞察局势的交易AI”,彻底重塑了交易格局。

人工智能交易的兴起

AI交易早已有之,但如今它主导了市场。

交易员不再仅仅依赖直觉。人工智能可以即时评估数十亿个数据点,清晰识别模式,并快速执行交易。

为什么现在AI交易引领市场:

- 速度:AI分析市场趋势的速度比人类可能做到的更快。

- 准确性:在广泛认知之前,就能识别出新兴趋势和市场变化。

- 自动化:AI交易机器人全天候执行交易,不受疲劳或市场交易时间的影响。

像恐慌性抛售或冲动性购买之类的人类情绪已不再影响交易。由人工智能驱动的平台保持稳定、数据驱动且精准。

然而,传统的AI交易工具往往忽视社会叙事和KOL(关键意见领袖)的影响。Edgen AI弥补了这一空白。

Edgen AI革新人工智能交易领域

Edgen AI 将链上洞察与社交“泵 fundamentals(基本面)”相结合,实时评估KOL情绪、智能钱包交易和市场叙事。

Edgen AI 有何独特之处?

- 社会共识洞察:评估来自X(前身为Twitter)等平台的实时关键意见领袖(KOL)评论和热门话题。

- 链上数据分析:实时追踪交易、巨鲸钱包变动、流动性变化和代币活动。

- AI决策:通过结合传统数据分析和社会动量来预测市场变化。

没有Edge AI,交易者会错过由社交情绪和有影响力的人物产生的隐藏信号。

关键EdgeAI功能,助力交易者

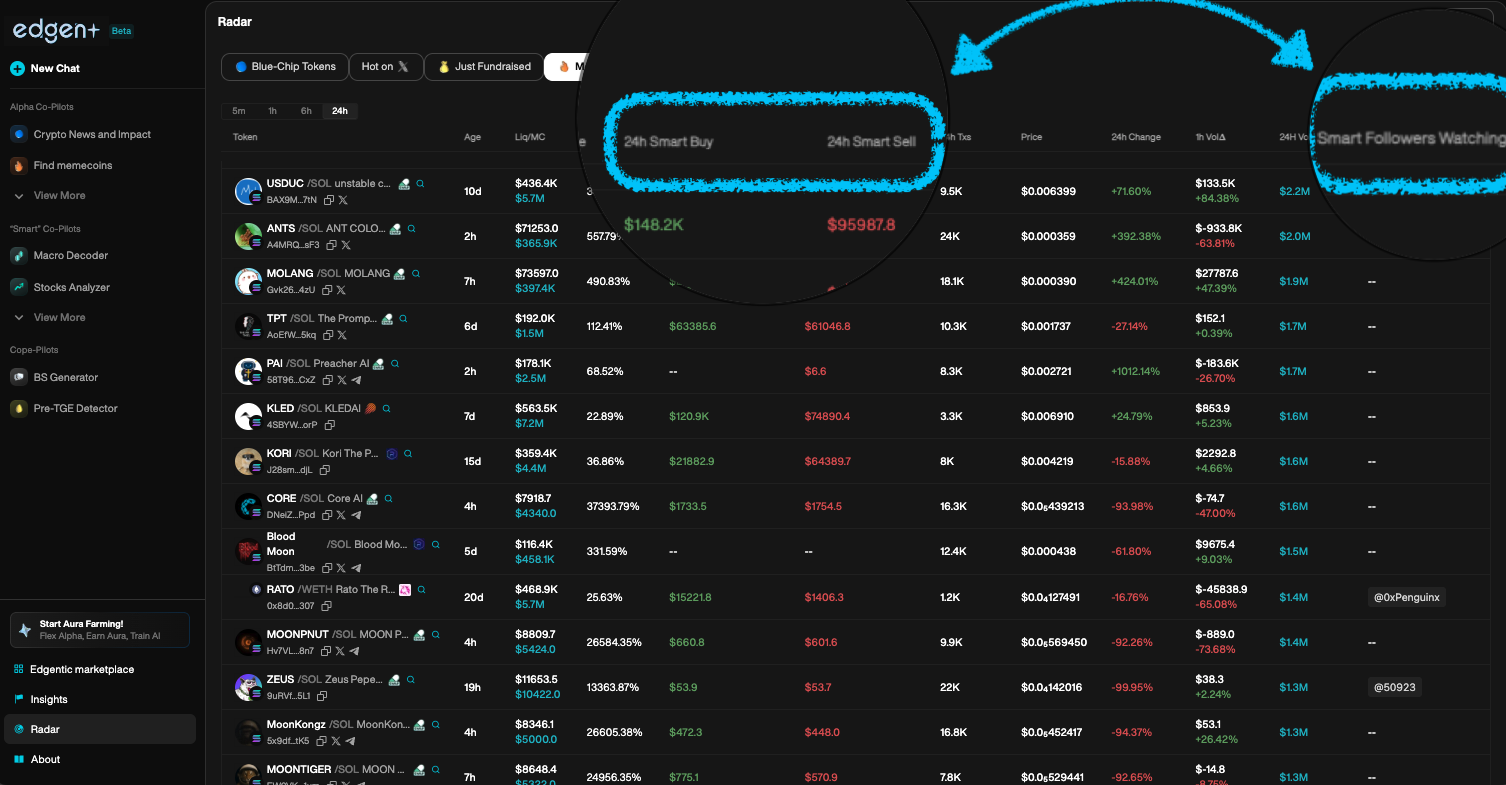

1. 边缘雷达:实时市场可视性

Edgen Radar提供对当前市场状况的实时详细视图:

- 根据实时社交热度和区块链活动突出显示热门代币。

- 清晰追踪鲸鱼和智能钱包的活动。

- 识别由KOL驱动的叙事,预测价格大幅波动。

缺乏这种数据清晰度,交易者可能会做出不明智的决策。

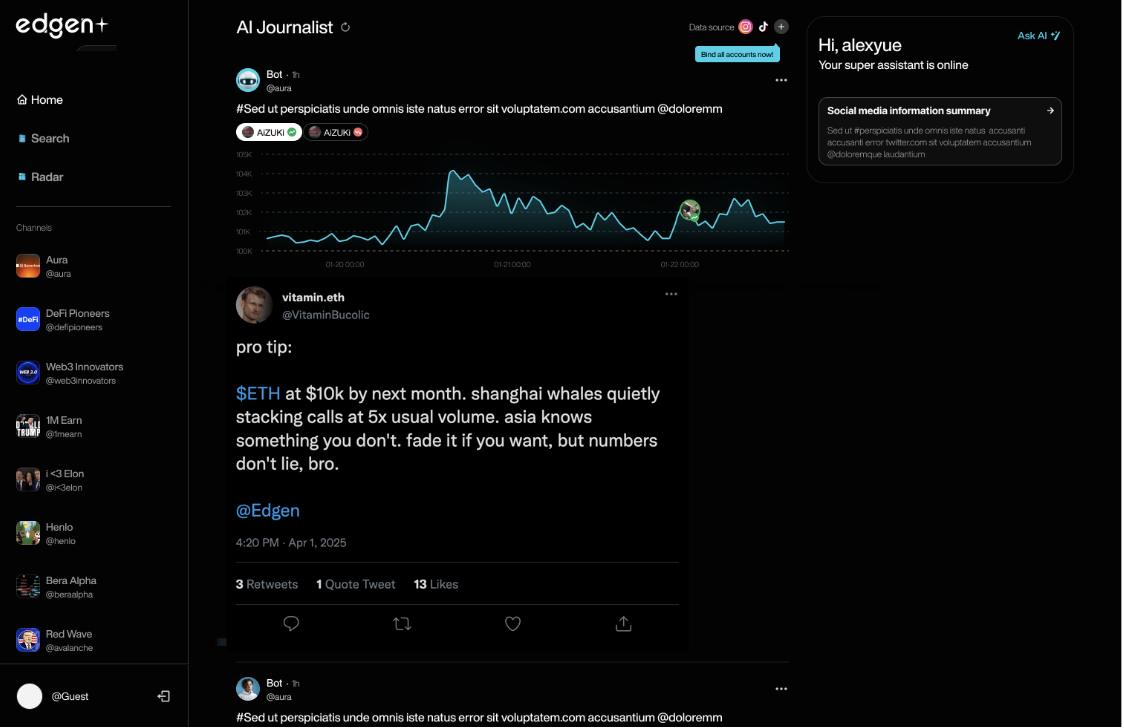

2. 边缘搜索:即时人工智能驱动的市场研究

Edgen Search作为交易员的AI分析师:

- 立即回答与市场相关的问题,提供经过筛选且有数据支持的回复。

- 过滤社交媒体噪音,清晰地提供可操作的见解。

- 快速分析跨平台趋势(X、电报、区块链)。

交易员依赖EdgeN搜索来区分真正的阿尔法机会与短暂的市场炒作。

3. 边缘洞察:社区驱动的阿尔法洞察

Edgen Insights连接交易员、分析师和人工智能:

- 允许交易员实时共享alpha洞察。

- AI审核过滤虚假信息并澄清讨论。

- 专家交易员和分析师提供高质量的、经过验证的见解。

洞察力促进了无需依赖单一权威的透明集体智慧。

智能钱包:人工智能驱动的交易引擎

智能钱包演进为复杂的交易工具,整合了区块链分析和人工智能驱动的策略。

智能钱包如何提升交易:

- 即时区块链监控:在普通交易者意识到之前,提前发现阿尔法信号。

- 快速交易执行:自动化即时交易,避免人工延迟。

- 欺诈预防:AI可清晰检测可疑交易,防止跑路行为。

- Edgen AI集成:智能钱包利用Edgen的社会分析功能,提升交易精度。

没有智能钱包,市场波动太快,无法进行人工交易。

KOLs:定义市场走势的网红

关键意见领袖对市场情绪具有巨大影响力。他们的建议、帖子和叙事会迅速影响加密货币价格。

如何通过KOL推动AI交易:

- 生成“泵 fundamentals”:由KOL引发的社交炒作直接影响资产估值。

- 提供阿尔法机会:内部信息可提供进入盈利交易的早期切入点。

- 影响情绪明确:KOL的乐观或悲观情绪会显著影响市场走势。

忽略KOL驱动的社交信号会严重限制交易效果。Edgen AI能够即时扫描KOL的活动、讨论和情绪趋势,提前预测市场反应。

人工智能交易革命已经到来

AI交易从未来的可能性转变为当前的必要性。

智能钱包、有影响力的KOL以及Edgen AI的尖端分析定义了一个新的交易时代,市场情报结合了社交洞察力和区块链透明度。

在这一人工智能驱动的时代中取得成功的交易者必须:

- 使用人工智能驱动的智能钱包进行快速精准的执行。

- 利用Edge AI清晰追踪由社交驱动的“泵 fundamentals”。

- 遵循KOL观点,但使用区块链分析进行验证。

- 持续监控alpha信号以预判市场走势。

市场迅速变化。下一次重要的价格波动已经开始了。

你准备好在人群之前交易了吗?试试看Edgen AI今天!

投资这事,终于不用一个人了

免费试用 Edgen。不用信用卡,不绑约