Tiền mã hóa meme, tiền mã hóa thay thế và cổ phiếu: Tại sao AI là chìa khóa cho xu hướng thị trường

Thị trường Đã Thay đổi. Vĩnh viễn.

Tiền di chuyển nhanh. Thị trường di chuyển nhanh hơn.

Đầu tư đã vượt ra khỏi biểu đồ, báo cáo tài chính và cơ bản. Tiền mã hóa, tiền thay thế và cổ phiếu hiện nay tuân theo làn sóng xã hội, cảm xúc của người ảnh hưởng và hoạt động chuỗi khối thời gian thực.

AI là động lực đằng sau sự thay đổi này, hướng dẫn các nhà giao dịch đến những quyết định thông minh hơn, dự đoán rõ ràng hơn và hành động nhanh hơn.Edgen AIgọi lực thị trường mới này là "Pumpamentals", sự giao thoa giữa xu hướng xã hội, sức mạnh của người có ảnh hưởng và hành động giá do cộng đồng thúc đẩy.

Giao dịch không có AI có nghĩa là bỏ lỡ các tín hiệu mà những người khác nhìn thấy rõ ràng. Giao dịch bằng AI định nghĩa thành công trên thị trường.

Các đồng tiền meme, Altcoin và Cổ phiếu được giải thích

Tiền xu Meme: Những trò đùa mang lại lợi nhuận nghiêm túc

Memecoins bắt đầu như những trò đùa trên mạng: Dogecoin (DOGE), Shiba Inu (SHIB), Pepe Coin (PEPE). Không có sức mạnh tài chính truyền thống, những tài sản này tăng giá nhờ sự chú ý từ cộng đồng mạng và các meme lan truyền.

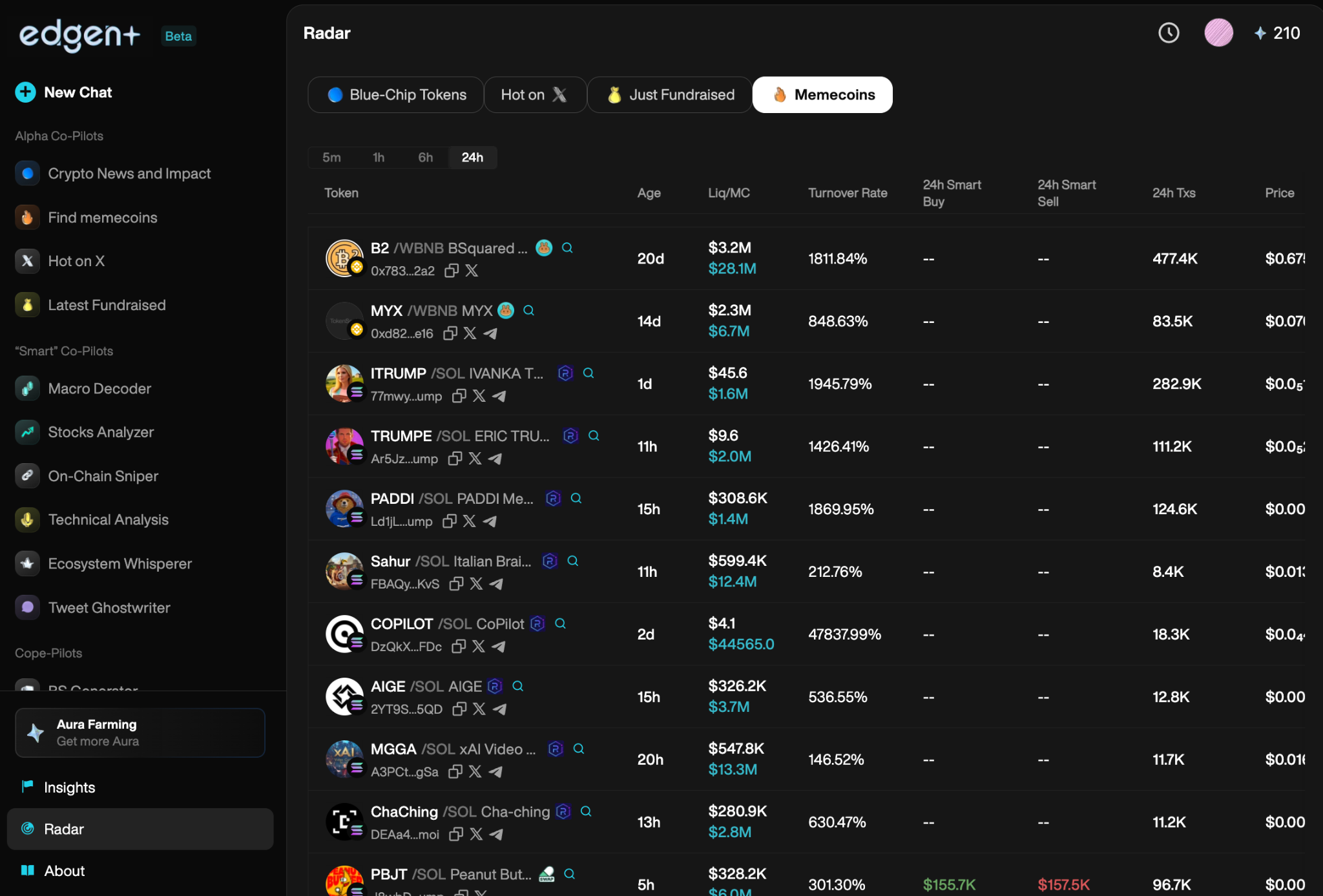

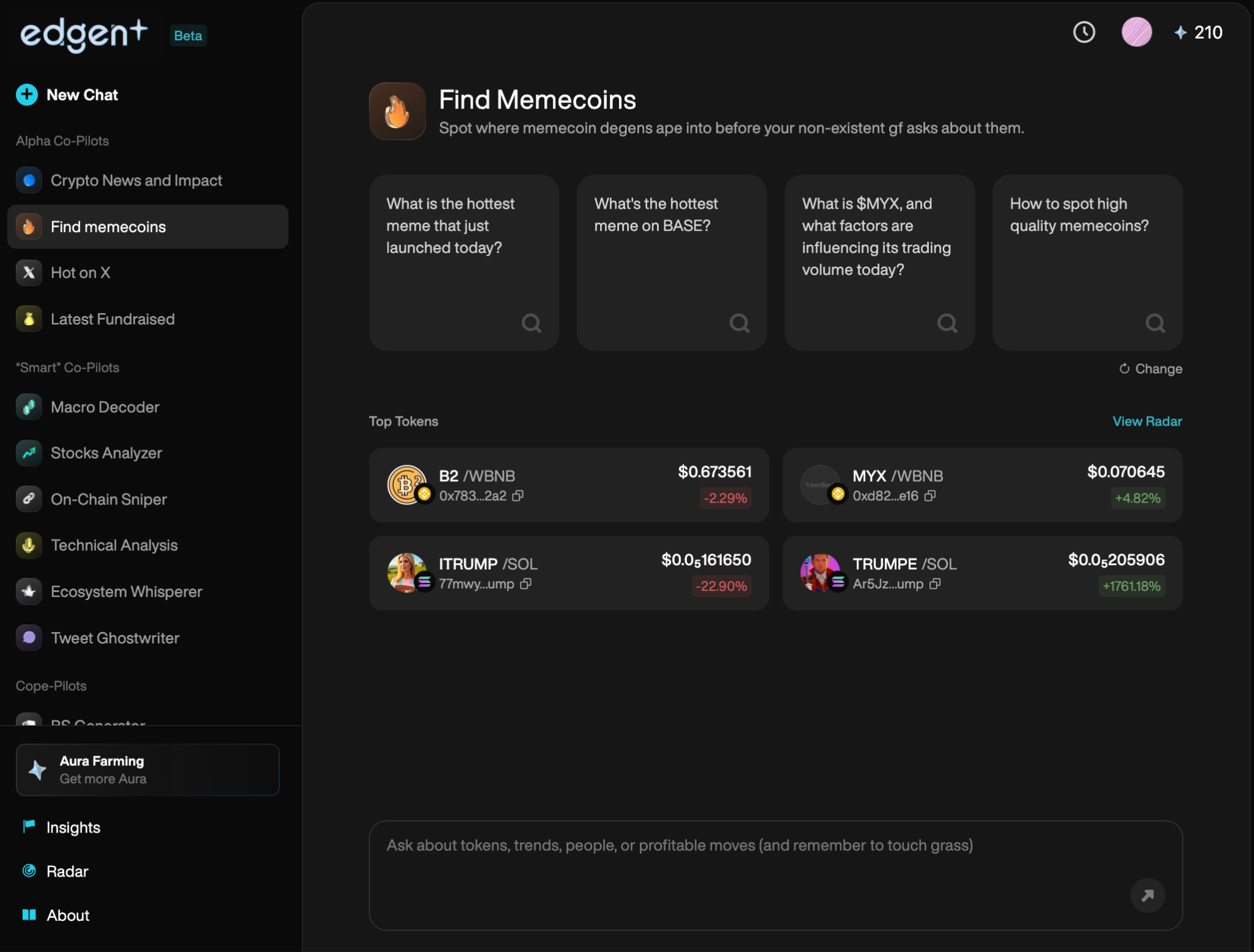

Giá tiền mã hóa tăng vọt và sụp đổ nhanh chóng.Edgen AItheo dõi cảm xúc trên Twitter, sự tương tác xã hội và các hành động của người có ảnh hưởng, phát hiện các đợt tăng giá trước khi xảy ra.

Tiền điện tử thay thế: Nhiều hơn chỉ là lựa chọn thay thế cho Bitcoin

Các đồng tiền thuật toán (altcoins) đại diện cho các loại tiền mã hóa khác ngoài Bitcoin, bao gồm Ethereum (ETH), Solana (SOL) và các token tập trung vào trí tuệ nhân tạo. Learn more about altcoins, their types, and how they differ from BitcoinKhác với memecoins, altcoins thường cung cấp các trường hợp sử dụng, tiện ích hoặc giá trị thực tế rõ ràng.

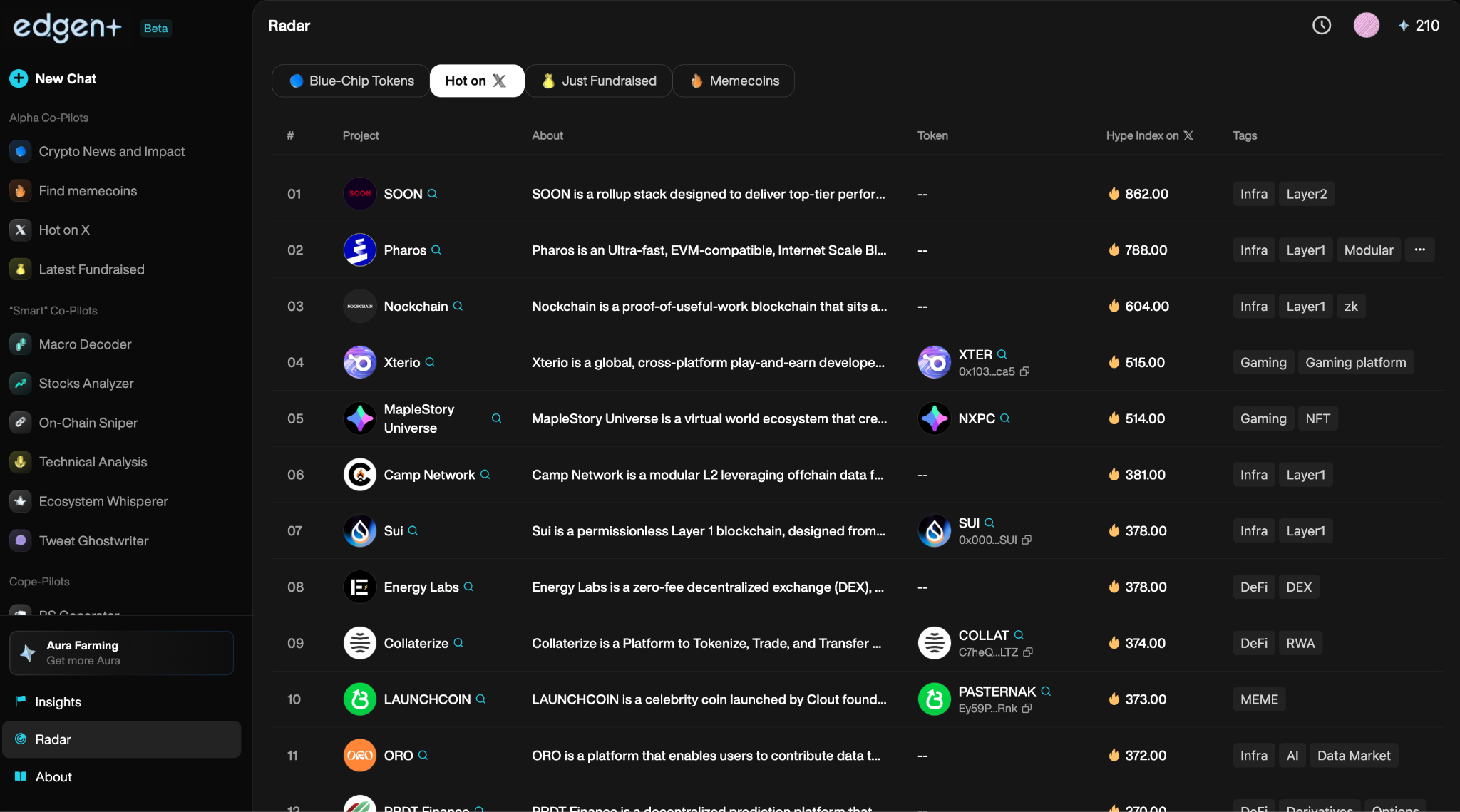

Edgen AI theo dõi các tín hiệu thị trường altcoin, chuyển động ví trên chuỗi và sự thay đổi trong cảm xúc cộng đồng để phát hiện cơ hội giao dịch sớm.

Cổ phiếu: Tài sản truyền thống đã phát triển

Cổ phiếu đại diện cho phần vốn của các công ty lớn như Apple, Tesla và Amazon. Mặc dù các quy tắc đầu tư truyền thống vẫn còn hiệu lực, nhưng AI đã thay đổi cách đầu tư vào thị trường chứng khoán. Các công ty hiện nay sử dụng các nền tảng do AI điều khiển để phân tích ngay lập tức các báo cáo lợi nhuận, tiêu đề tin tức và tâm lý nhà đầu tư, khiến giao dịch được hỗ trợ bởi AI trở nên thiết yếu.

Cách AI định hình xu hướng thị trường hiện đại

AI Dự đoán tâm lý thị trường ngay lập tức

Tâm lý nhà đầu tư quyết định giá trị tài sản. Edgen AI quét mạng xã hội (Twitter/X) và dữ liệu blockchain, xác định các thay đổi trong tâm trạng thị trường trước khi được nhận biết rộng rãi.

- Dự đoán các thay đổi trong cốt truyện trước các chuyển động của thị trường.

Chủ động dữ liệu trên chuỗi với AI

Phân tích trên chuỗi cho thấy các tín hiệu thị trường ẩn như hoạt động ví, dòng tiền và hành động của các quỹ lớn. Edgen AI giải thích dữ liệu blockchain một cách rõ ràng, cung cấp thông báo thời gian thực trước khi đa số các nhà giao dịch nhận ra.

Edgen AI phát hiện một ví lớn đang tích lũy một đồng tiền thuật toán có vốn hóa thấp. Các nhà giao dịch sử dụng Radar của Edgen nhận được thông báo tức thì, nắm bắt lợi nhuận sớm.

Tín hiệu Alpha: Lợi thế Tuyệt đối của Trí tuệ Nhân tạo

Các tín hiệu Alpha làm nổi bật các tài sản bị định giá thấp đang chờ tăng trưởng. Edgen AI xử lý lượng dữ liệu khổng lồ một cách tức thì, nhanh chóng tiết lộ các chỉ báo bứt phá. Khám phá alpha ẩn giấu bằng cách chạy các truy vấn trực tiếp qua Edgen Search, công cụ tìm kiếm được tích hợp AI cho các nhà giao dịch.

- Hoạt động của nhà phát triển tăng lên

- Số lượng người nắm giữ token đang tăng lên

- Số lượng đề cập trên mạng xã hội tăng lên

AI nhận diện những cơ hội này trước khi giá cả phản ánh chúng.

Thuật toán giao dịch được điều khiển bởi AI trong tiền mã hóa và cổ phiếu

Các Bot Giao dịch AI: Tiêu chuẩn Mới

Trí tuệ nhân tạogiao dịch nhanh hơn, thông minh hơn và không có cảm xúc.

AI giao dịch chính xác, không cảm xúc và với tốc độ phi thường. Các bot giao dịch tần suất cao (HFT) thực hiện giao dịch trong vài mili giây, vượt qua khả năng của con người.

Edgen Radarchuyên về thực hiện giao dịch nhanh, phát hiện alpha theo thời gian thực và cung cấp cái nhìn toàn diện về thị trường.

Trí tuệ nhân tạo gặp gỡ sự đồng thuận xã hội

Phân tích kỹ thuật một mình là không đủ. Edgen AI kết hợp cảm xúc xã hội và các câu chuyện cộng đồng để nắm bắt tư duy tập thể của thị trường:

- Các chuyển động ví thông minh (hành động mua/bán)

- Hoạt động của Người có ảnh hưởng chính (KOL)

- Chủ đề nổi bật và động lực của người có ảnh hưởng trên Twitter/X

AI Phát hiện Tâm trạng Xã hội Nhanh hơn Con người

Xu hướng xã hội, xu hướng người có ảnh hưởng và sự tham gia của cộng đồng làm tăng giá cả chỉ trong một đêm. Edgen AI liên tục theo dõi và đánh giá các tín hiệu này một cách rõ ràng. Theo dõi các cuộc trò chuyện thị trường trực tiếp và thông tin cộng đồng trên nền tảng Edgen Feed:

- Các tín hiệu tích cực: tương tác lan truyền, sự chú ý của người ảnh hưởng đang tăng lên, tích lũy của "cá mập".

- Cảnh báo tiêu cực: sự suy giảm quan tâm xã hội, các câu chuyện thay đổi, và mức độ tương tác giảm dần.

AI phát hiện các thay đổi cảm xúc trước, cho phép thực hiện giao dịch quyết đoán trước phản ứng của thị trường.

Vai trò thiết yếu của AI trong xu hướng thị trường tương lai

AI + DeFi: Bước tiến mới của thị trường

DeFi tiếp tục cách mạng hóa tài chính, và AI thúc đẩy sự phát triển của nó.

Edgen AI phát triển thành cơ sở hạ tầng giao dịch bên mua hoàn chỉnh:

- Tự động hóa các chiến lược vay và cho vay.

- Quản lý rủi ro chủ động trong DeFi.

- Tối ưu hóa nông nghiệp lợi nhuận để đạt được lợi nhuận cao nhất.

Phân tích của con người riêng lẻ không thể theo kịp quy mô của DeFi. AI hiện đang dẫn đầu xu hướng.

Blockchain và Trí tuệ nhân tạo: Một liên minh giao dịch mạnh mẽ

Kết hợp công nghệ AI và blockchain cải thiện đáng kể tính minh bạch và hiệu quả của thị trường:

- Kiểm tra hợp đồng thông minh bằng AI để phát hiện các lỗ hổng tiềm ẩn.

- Dự đoán phí gas tối ưu và thời điểm giao dịch.

- Nâng cao phân tích DEX để thực hiện giao dịch tốt hơn.

AI và blockchain cùng nhau tạo nên một môi trường giao dịch mạnh mẽ.

Tại sao Trí tuệ nhân tạo (AI) lại quan trọng đối với các nhà giao dịch hiện nay

AI trở nên thiết yếu, định hình tương lai của thành công trong giao dịch.

Nhà buôn cần AI vì:

- Quyết định nhanh hơn: Xử lý tức thì hàng triệu điểm dữ liệu.

- Độ chính xác cao: Trí tuệ nhân tạo loại bỏ thiên lệch cảm xúc của con người.

- Sự cảnh giác liên tục: AI cung cấp giám sát thị trường liên tục.

- Nhận diện alpha tức thì: AI theo dõi cảm xúc thời gian thực và hoạt động trên chuỗi một cách rõ ràng.

Giao dịch mà không có AI khiến nhà đầu tư ở thế bất lợi nghiêm trọng.

Thương mại Thông minh hơn hoặc Rủi ro Bị Lạc hậu

Thị trường đã thay đổi mãi mãi. Tiền mã hóa, tiền thuật toán và cổ phiếu phụ thuộc rất nhiều vào các phân tích do AI tạo ra, các câu chuyện xã hội và phân tích thời gian thực.

Những nhà buôn bỏ qua AI gặp khó khăn. Những người nắm bắt các nền tảng như Edgen AI tận dụng cảm xúc xã hội, phát hiện alpha và phân tích blockchain, luôn ở trước rất nhiều.

Tương lai đã đến. Giao dịch được hỗ trợ bởi AI xác định người thắng và người thua. Lượt đi của bạn xác định vị trí thị trường của bạn. Learn more about Edgen AIHãy dịch đoạn văn tiếng Anh sau sang tiếng Việt. Giữ nguyên cấu trúc và thuật ngữ kỹ thuật chính xác. Tránh dịch quá mức.

Đầu tư, cuối cùng không phải một mình nữa.

Dùng thử Edgen miễn phí. Không cần thẻ, không ràng buộc.