Hyperliquid, yüksek performanslı, amaca yönelik olarak inşa edilmiş bir Katman 1 blok zinciri ve merkezi olmayan sürekli vadeli işlem borsasıdır. Merkezi bir borsanın hızı ve kullanıcı deneyimini, merkezi olmayan finansın güvenliği ve şeffaflığıyla birleştiren, birleşik, zincir üstü finansal merkez olmak üzere ilkelerden yola çıkarak tasarlanmıştır. $HYPE Rehberi için buraya tıklayın.

TL;DR

- Hyperliquid, performansta ve kullanıcı deneyiminde yeni bir endüstri standardı belirleyen tamamen zincir üstü bir emir defterini başarıyla inşa ederek dikkat çekici bir temel güç elde etti.

- Protokol, stratejik geri alımlar yoluyla önemli gelirlerinin %90'ından fazlasını HYPE tokenına yönlendiren benzersiz ve güçlü bir değer birikimi döngüsüne sahiptir.

- Hyperliquid, yenilikçi halka açık piyasa araçları aracılığıyla kayda değer kurumsal destek ve doğrulama çekerek, uzun vadeli vizyonunu sofistike sermaye ile uyumlu hale getirdi.

- Proje, hızla büyüyen trilyonlarca dolarlık kripto türev piyasasında önemli bir payı ele geçirecek konumda olup, temel DeFi altyapısının baskın bir parçası olma yolunda net bir yola sahiptir.

Hyperliquid Nedir?

Hyperliquid, sadece bir sürekli vadeli işlem borsasından çok daha fazlası olan çığır açan bir DeFi protokolüdür. Özelleştirilmiş bir konsensüs algoritması ve yürütme ortamıyla amaca yönelik olarak inşa edilmiş, dikey olarak entegre bir Katman 1 blok zinciridir. Bu benzersiz mimari, yüksek performanslı, tamamen zincir üstü bir Merkezi Limit Emir Defteri (CLOB) sunmasını sağlar; bu, merkezi olmayan finansta tarihsel olarak büyük bir zorluk olarak kabul edilen bir başarıdır. Platformun misyonu, geleneksel merkezi borsalara güvenli, şeffaf ve yüksek performanslı bir alternatif sunarak kapsamlı bir zincir üstü finansal sistem olmaktır. Hyperliquid, her iki dünyanın en iyi özelliklerini—CEX düzeyinde hız ve DEX düzeyinde güvenlik—birleştirerek yeni nesil finans için temel altyapıyı inşa etmektedir.

Bölüm I: Temel ve Stratejik Analiz

Stratejik Yön ve Anlatı Yörüngesi

Hyperliquid'in stratejik vizyonu, parçalanmış bir kripto ortamını tek, yüksek performanslı bir L1 altında birleştiren temel bir “DeFi finansal merkezi” olmaktır. Bu hırs, “zincir üstü Binance” olarak nitelendirilmesiyle somutlaşır; bu anlatı, merkezi olmayanlaştırma ve kendi kendine saklama temel ilkeleriyle önde gelen bir merkezi borsanın ürün derinliğini ve kullanıcı deneyimini tekrarlama hedefini etkili bir şekilde iletir. Bu konumlandırma, Hyperliquid'i CEX'lerden DEX'lere devam eden sermaye rotasyonu ve sağlam, yüksek performanslı DeFi altyapısı talebi dahil olmak üzere birkaç güçlü piyasa anlatısının kalbine yerleştirir. Başarısı, bu vizyonu uygulama yeteneğiyle içsel olarak bağlantılıdır; bu vizyonu, blok zinciri karmaşıklıklarını soyutlarken doğrulanabilir, zincir üstü şeffaflığın temel değer tekliflerini koruyan üstün, düşük sürtünmeli bir kullanıcı deneyimiyle göstermiştir.

Ürün ve Teknoloji Yeterliliği

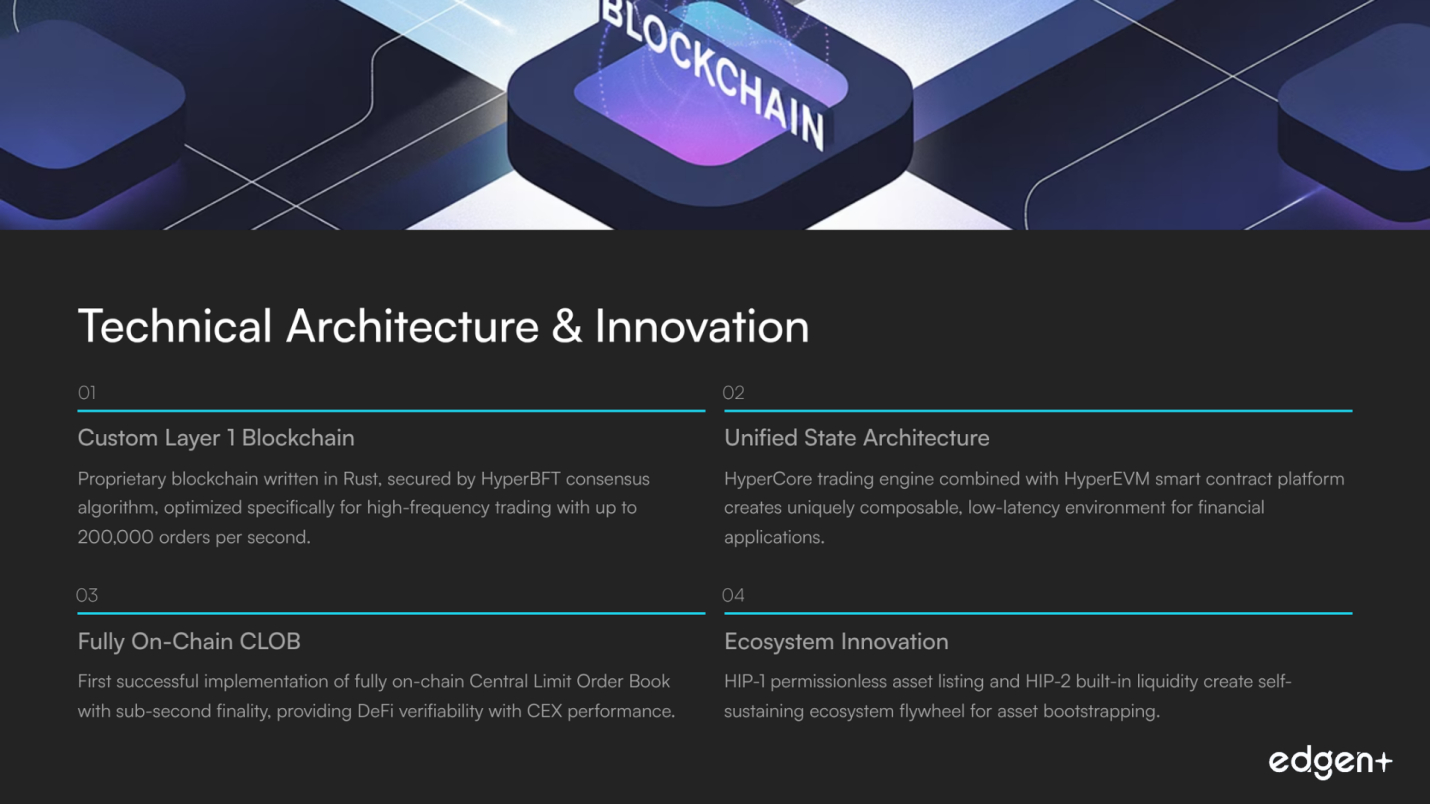

Hyperliquid platformu, zincir üstü emir defterlerinde tarihsel performans sınırlamalarının üstesinden gelmek için ilkelerden yola çıkarak tasarlanmış özel, dikey olarak entegre bir teknoloji yığını üzerine inşa edilmiştir.

- Çekirdek Mimari: Protokol, Rust dilinde yazılmış, HyperBFT adlı özel bir konsensüs algoritmasıyla korunan tescilli bir Katman 1 blok zinciridir. Bu mimari, yüksek frekanslı ticaret için benzersiz bir şekilde optimize edilmiştir ve saniyeler altı kesinlikle olağanüstü yüksek iş hacmi (saniyede 200.000'e kadar emir) sağlar. HyperCore ticaret motorunu genel amaçlı bir akıllı sözleşme platformu olan HyperEVM ile birleştiren birleşik durum mimarisi, finansal uygulamalar için benzersiz bir şekilde birleştirilebilir ve düşük gecikmeli bir ortam oluşturur.

- Temel Yenilikler: Hyperliquid'in teknik üstünlüğü, tamamen zincir üstü bir CLOB'ye olan tavizsiz taahhüdünde yatmaktadır. Bu, bir CEX'ten beklenen performanstan ödün vermeden DeFi'nin doğrulanabilirliğini sağlar. Protokolün izinsiz varlık listeleme (HIP-1) ve yerleşik likidite (HIP-2) için yenilikçi Hyperliquid İyileştirme Teklifleri (HIP'ler), rakiplerin kopyalaması zor olan varlık bootstrapping için yeni, kendi kendini idame ettiren bir ekosistem döngüsü oluşturmuştur.

Piyasa Benimsenmesi ve Geliştirici Aktivitesi

Hyperliquid, dikkat çekici bir piyasa benimsenmesi elde etti ve güçlü bir ivme gösteriyor. Platformun kullanıcı tabanı, rekor kıran işlem hacimleriyle 600.000'den fazla kullanıcıya ulaştı. Temmuz 2025'te platform, rekor kıran 319 milyar dolar işlem hacmiyle, herhangi bir DeFi sürekli vadeli işlem platformu için kaydedilen en yüksek aylık rakama ulaştı. Bu, güçlü bir ürün-piyasa uyumunun açık bir göstergesidir. Geliştirme cephesinde, çekirdek protokol olgunlaşırken, daha geniş ekosistem önemli bir ivme gösteriyor. 175'ten fazla ekip HyperEVM üzerinde açıkça inşa yapıyor ve platformun faydasını ve ağ etkilerini daha da artıran canlı bir araç ve uygulama ekosistemi yaratıyor.

Ekip ve Destekçiler

Projenin başarısı, çekirdek ekibinin olağanüstü teknik yeterliliğine doğrudan bağlanabilir. Eski bir fizik dehası ve seçkin yüksek frekanslı ticaret şirketi Hudson River Trading (HRT)'nin emektarı olan kurucu ortak Jeff Yan liderliğindeki ekip, üstün bir ticaret alanı için teknik gereksinimler hakkında derinlemesine, ilk elden bir anlayışa sahiptir. 10-11 üyeli çekirdek ekip, önde gelen akademik kurumlardan ve lider nicel finans şirketlerinden gelen son derece yetenekli profesyonellerden oluşmaktadır.

Yatırım yapmak artık yalnız bir iş değil.

Ed'i ücretsiz dene. Kart yok, taahhüt yok.