Cómo usar la IA para inversiones en criptomonedas más inteligentes

Cómo usar la IA para inversiones en criptomonedas más inteligentes

∙ Título SEO: Cómo usar Edgen AI para inversiones en criptomonedas más inteligentes

∙ Descripción: Aprenda cómo Edgen AI combina el análisis on-chain, las señales predictivas y la inteligencia de cartera para ayudar a los inversores en criptomonedas a tomar decisiones más rápidas y basadas en datos.

∙ Palabras clave: Edgen AI, inversión en criptomonedas, análisis blockchain, copiloto de inversión con IA, inteligencia on-chain, señales predictivas, optimización de cartera, descubrimiento de alfa, previsión de mercado

El futuro de la inversión inteligente en criptomonedas

El éxito en cripto depende del momento, los datos y la claridad. Los precios cambian en segundos, el sentimiento puede dar un giro de la noche a la mañana y las oportunidades se desvanecen tan rápido como aparecen. Los inversores que se mantienen a la vanguardia son aquellos que comprenden antes de que el mercado reaccione.

Edgen fue construido con ese propósito. Unifica el análisis de IA, los datos de blockchain y la inteligencia social en un sistema adaptativo. A través de agentes como Technical Signals, Pre-TGE Detector y Trading Mindshare, transforma el ruido del mercado en información estructurada.

Esta guía explica cómo usar el ecosistema de Edgen para tomar decisiones más precisas, gestionar la volatilidad y descubrir oportunidades en todo el panorama de los activos digitales.

II. Entendiendo el ecosistema de Edgen

1. ¿Qué hace que Edgen sea diferente?

Edgen AI fusiona el aprendizaje automático, la transparencia de blockchain y los datos de comportamiento para dar a los inversores una imagen completa del mercado. Su sistema integrado proporciona:

- Información de mercado en tiempo real

- Generación de señales alfa

- Análisis predictivo de riesgos

- Seguimiento del sentimiento del mercado

- Herramientas de optimización de cartera

Todos los módulos operan sincronizados dentro de la aplicación Edgen, por lo que las actualizaciones se mantienen consistentes en todos los dispositivos.

2. Usar la IA para decisiones más inteligentes

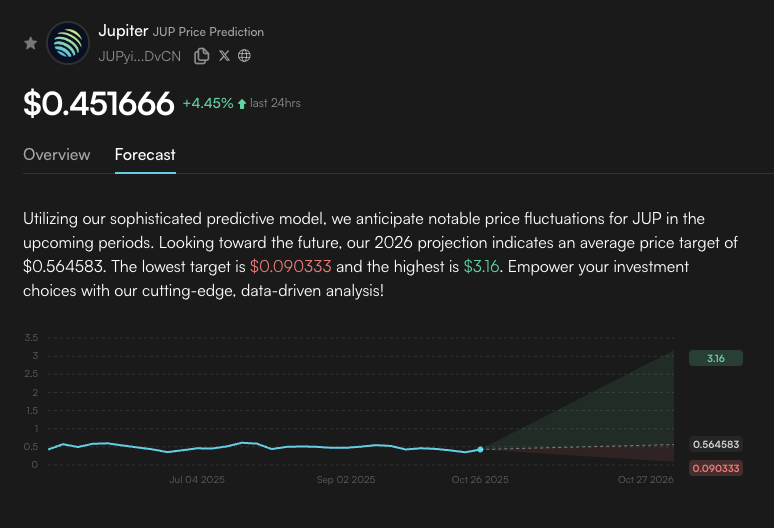

Los algoritmos de Edgen detectan ineficiencias antes de que se hagan visibles. El Informe 360° agrega indicadores técnicos y fundamentales, produciendo pronósticos y análisis de tendencias en tiempo real.

Para los nuevos usuarios, el centro de aprendizaje de Edgen ofrece una ruta de inicio clara para integrar herramientas predictivas en los flujos de trabajo diarios.

3. Integración de análisis On-Chain y señales de mercado

El On-Chain Sniper de Edgen monitorea la actividad de blockchain para identificar movimientos de ballenas y tendencias de acumulación temprana. Combinado con las Señales Alfa, convierte los datos de transacciones en puntos de entrada y salida accionables.

El Detector Pre-TGE destaca los próximos lanzamientos de tokens, ayudando a los usuarios a posicionarse temprano antes de una mayor conciencia del mercado.

4. Gestión de riesgos en condiciones volátiles

La volatilidad de las criptomonedas es oportunidad y riesgo en igual medida. La suite de gestión de riesgos de Edgen permite a los usuarios establecer alertas personalizadas y reglas de automatización para caídas de precios o reversiones de sentimiento.

Durante las recientes fluctuaciones del mercado, este sistema proporcionó advertencias en tiempo real que ayudaron a los traders a asegurar ganancias o reducir la exposición antes de cambios repentinos.

III. Características avanzadas que redefinen la conciencia del mercado

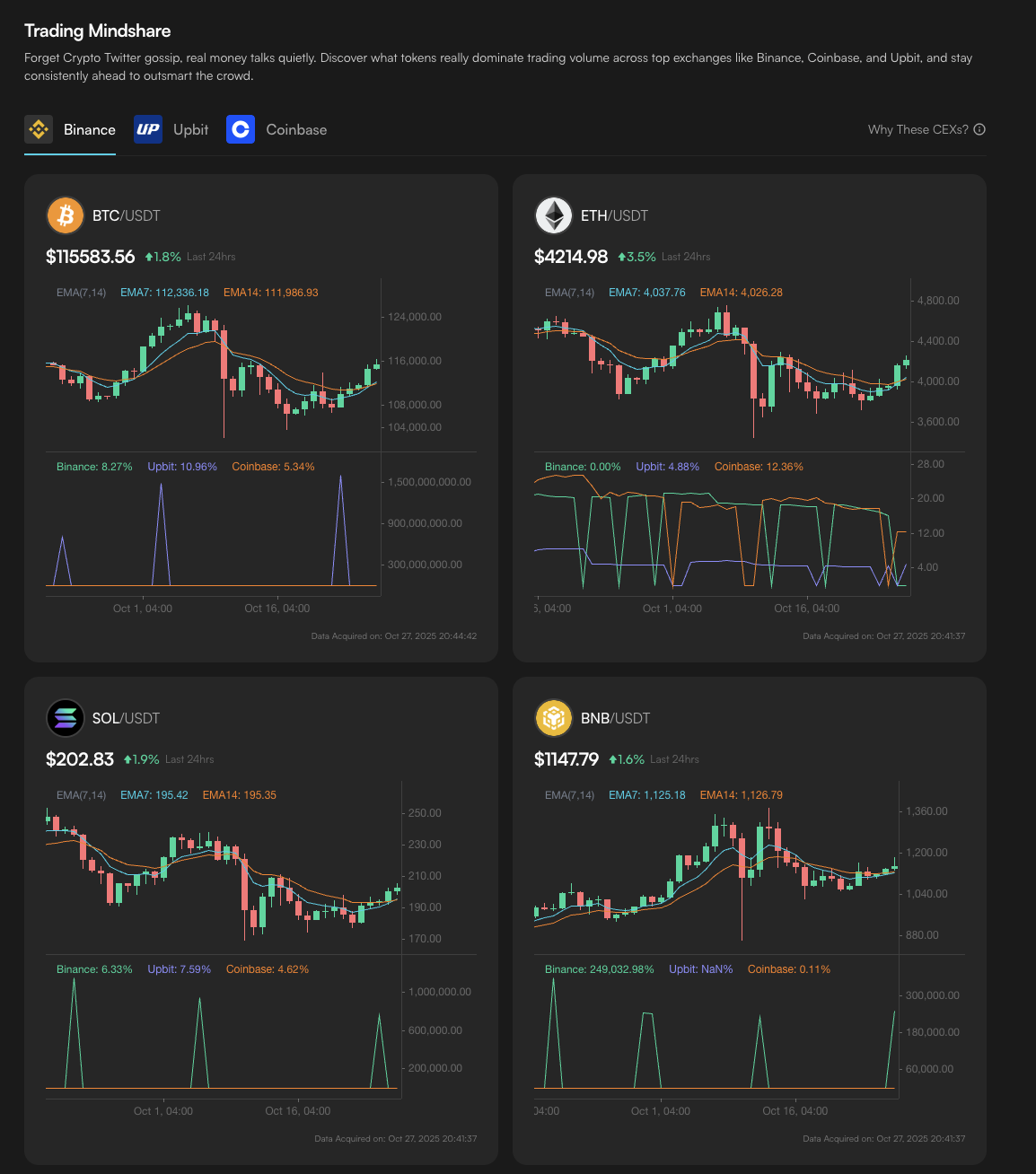

1. Participación en el pensamiento comercial (Trading Mindshare)

Este agente mide los flujos de liquidez analizando datos de las principales bolsas. Interpreta los cambios en el tono y el nivel de interés de la comunidad, proporcionando una primera medida del estado de ánimo concreto del mercado más allá del sentimiento social.

2. Señales técnicas

Edgen evalúa indicadores como RSI, MACD y Bandas de Bollinger a través del aprendizaje automático. Cada resultado se verifica contra el comportamiento histórico del mercado para garantizar la fiabilidad.

3. Diagnósticos de cartera

El Informe 360° integra las tenencias, las métricas de sentimiento y el posicionamiento on-chain en un resumen de rendimiento continuo. Junto con Pivot Alert, permite una gestión proactiva de la cartera a través de alertas tempranas y recomendaciones de reequilibrio.

IV. Mantenerse informado con noticias integradas

Edgen agrega actualizaciones verificadas de múltiples fuentes del mercado.

Los usuarios pueden seguir:

- Análisis de la red Bitcoin y Ethereum

- Informes del sector DeFi y flujos de tokens

- Desarrollos del mercado NFT

- Cambios regulatorios y macroeconómicos que afectan a los activos digitales

Este flujo garantiza que las decisiones se basen en un contexto preciso y actualizado.

V. Construyendo una rutina de inversión inteligente

La fortaleza de Edgen radica en conectar todas las capas de inteligencia de mercado en un único bucle de retroalimentación.

- El análisis on-chain muestra lo que están haciendo los grandes tenedores.

- Las señales técnicas revelan dónde las tendencias se fortalecen o se desvanecen.

- Los datos de sentimiento explican cómo evolucionan las narrativas.

- Los diagnósticos de cartera traducen todo esto en recomendaciones claras.

Cuanto más consistentemente use Edgen, más rápido se adaptarán sus modelos a sus hábitos de inversión, refinando alertas y pronósticos según su estrategia personal.

VI. Domina el mercado con Edgen

Los datos son el activo más valioso en el trading. Edgen AI brinda a los inversores la capacidad de interpretar esos datos con precisión y confianza.

A través del análisis predictivo, el descubrimiento de alfa y el control de riesgos, transforma la información en una ventaja estratégica.

Comience a usar Edgen AI today para explorar cómo la inteligencia, la claridad y el momento pueden definir la próxima etapa de su viaje de inversión en criptomonedas.

Invertir, por fin, ya no es cosa de uno solo.

Prueba Ed gratis. Sin tarjeta, sin compromiso.