Edgen × Kaito 360°チャレンジ:市場を出し抜け!

[更新] Kaitoの公開リーダーボードおよびXのプラットフォームポリシーの最近の変更に伴い、Kaitoのリーダーボードは廃止されました。これはEdgenには影響しません。AuraおよびEdgenリーダーボードは完全に独立して機能しており、今後のクエストはポートフォリオをより良く管理し、より情報に基づいた投資判断を下すことに焦点を当てています。

誰もが独自の意見を持っていますが、誰もが洞察力を持っているわけではありません。

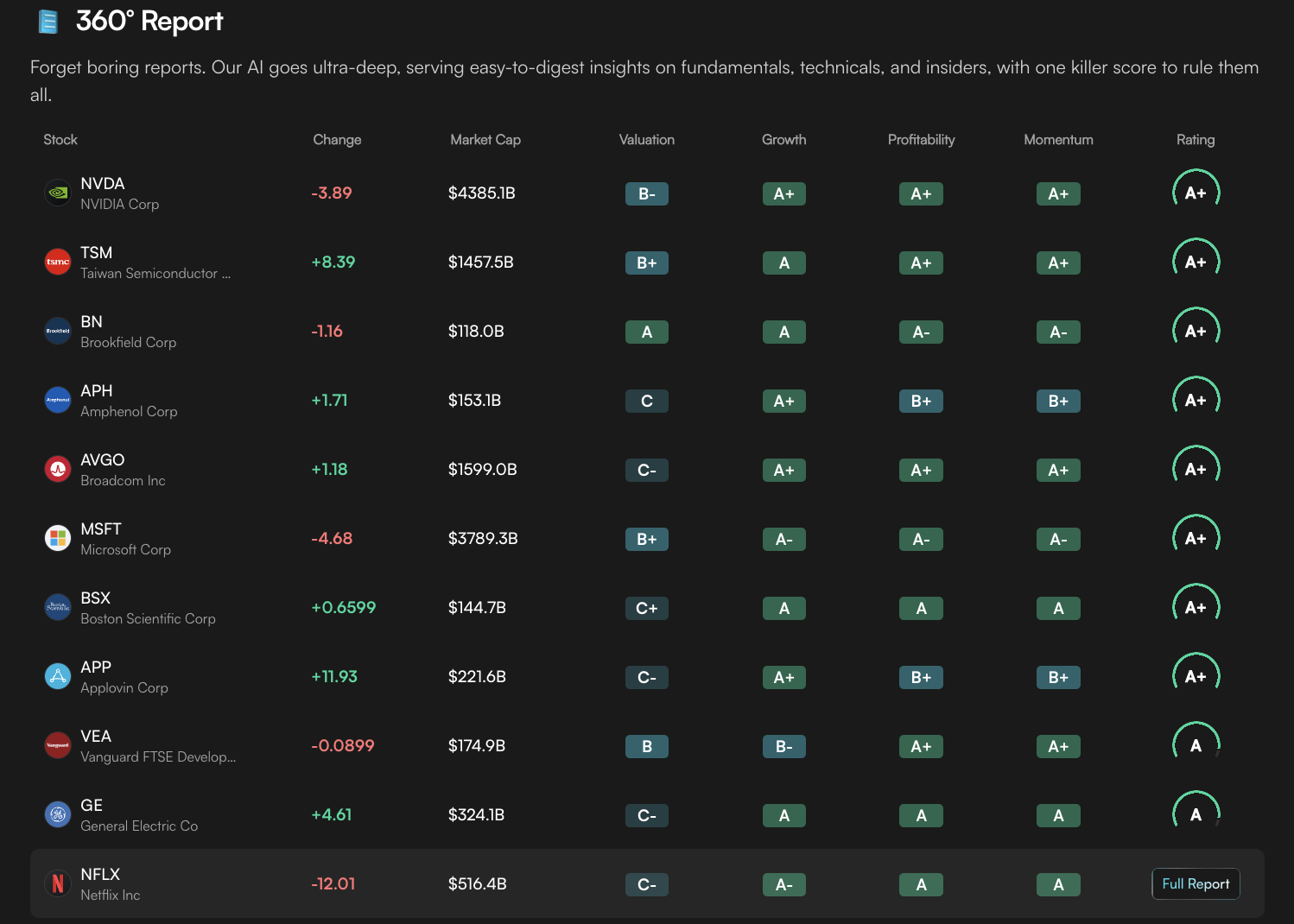

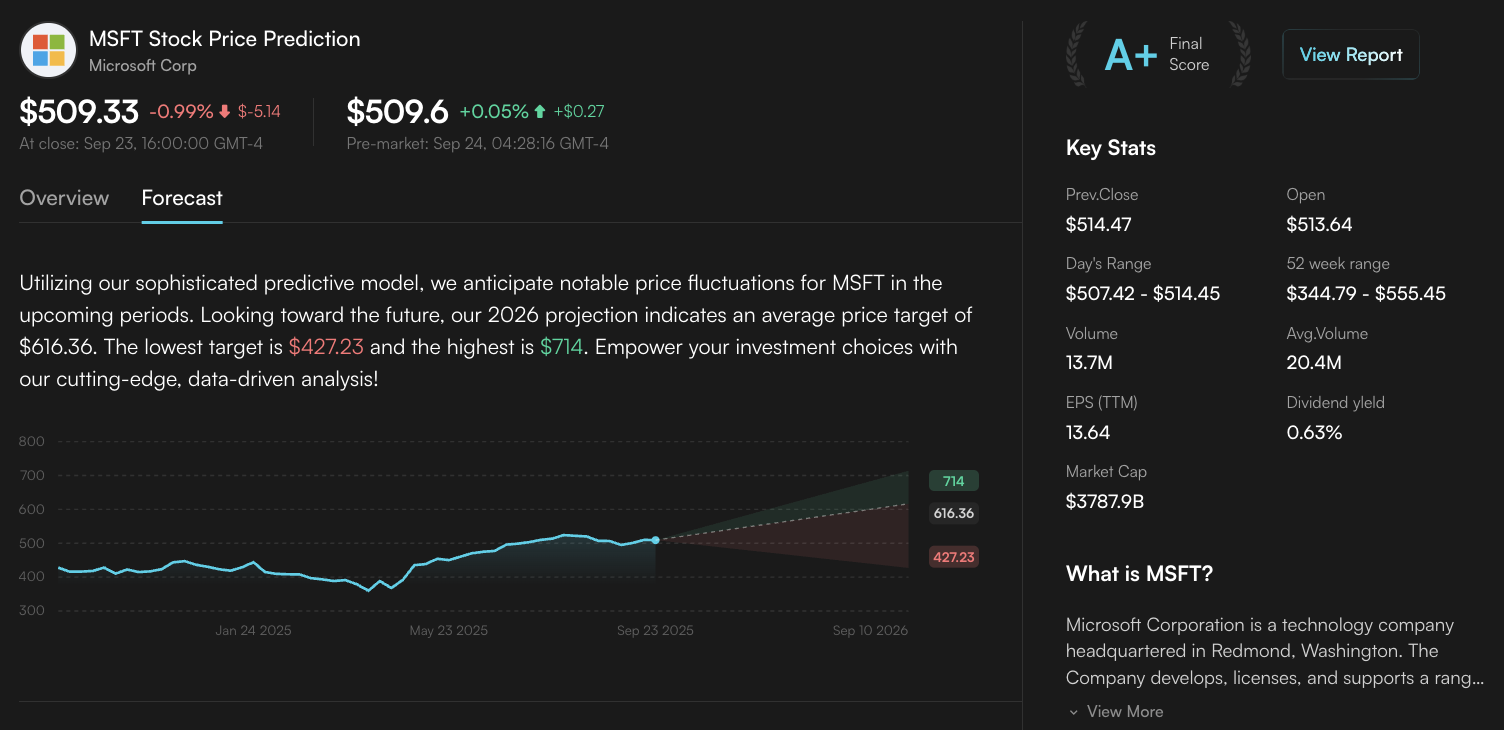

Edgen は、当社の360°レポートと予測ページにより、株式と暗号資産を1つの画面に統合することで、これらの洞察を提供します。

Kaito は声を集めます。コミュニティの貢献をリアルタイムで追跡し、ランキング付けすることで、思慮深い投稿が上位に表示されるようにします。

最も説得力のある分析を称えるため、私たちは共同で1週間のチャレンジを開始します。

AIの判断、人間の声:あなたの360°の洞察が重要な理由

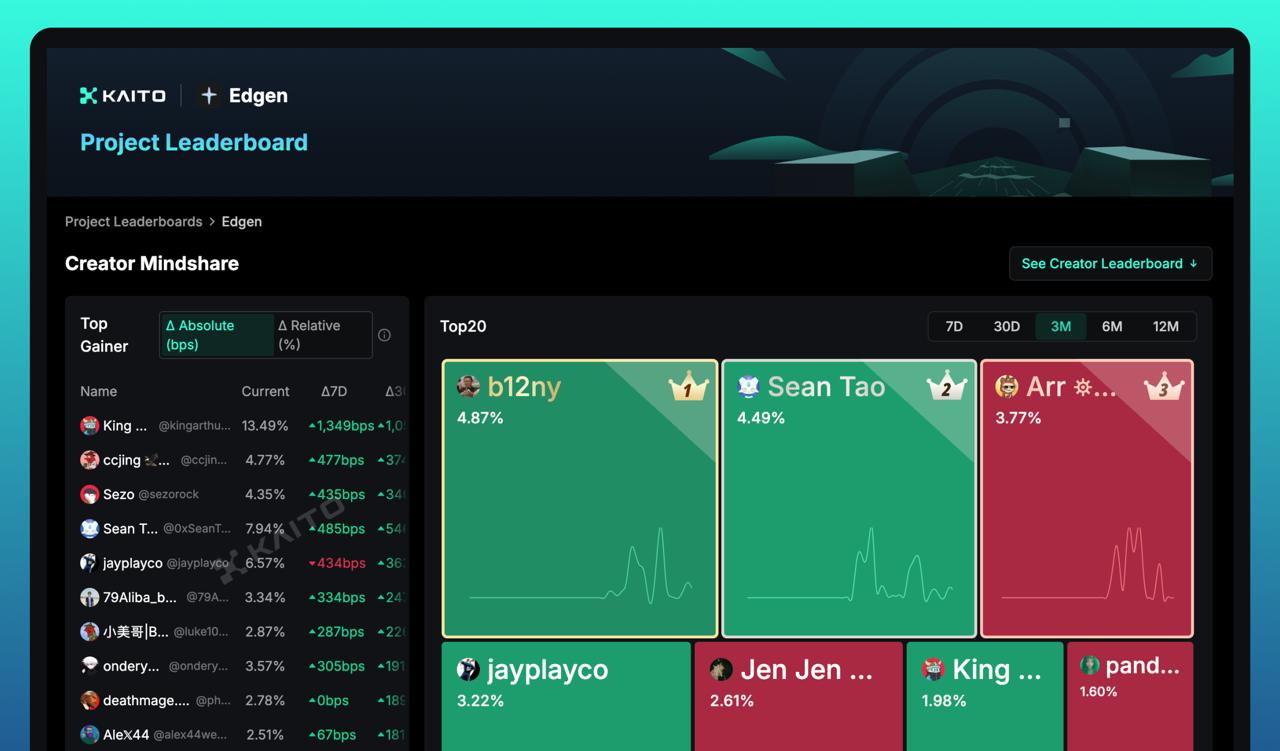

KaitoのYapperリーダーボードは、あらゆるブランドやトピックに対する貢献を追跡し、ランク付けする公開ダッシュボードです。参加を奨励し、誰にでも公平な機会を与え、コミュニティエンゲージメントを楽しい体験に変えます。人々はリーダーボードを使用して、質の高いクリエイターを称賛し、功績に基づいた貢献を評価します。

このアプローチはEdgenのミッションと一致しています。当社の360°レポートは、人々がファンダメンタルズ、テクニカル、モメンタムを深く掘り下げ、ビットコイン、Solana、優良株のいずれであっても、すべての情報を各資産の単一スコアに凝縮するのに役立ちます。

当社の予測ページは、予測モデルを適用して将来の価格範囲を予測し、人々が平均、安値、高値の目標を提供することで市場予測を行うのに役立ちます。EdgenのデータとKaitoのAIランキングを組み合わせると、あなたの分析は可視性と評価を得ます。

アリーナへ足を踏み入れよう:あなたの360°の見解を示しましょう

⏰ 期間:2025年9月24日~2025年9月30日(キャンペーンはUTC 15:59:59に終了)

🎯 トピック:関心のある資産を選び、その360°レポートまたは予測ページを開いてください。その1枚のレポートを使って、Xであなた自身の見解をまとめましょう:目立つ点を強調し、指標を結びつけ、あるいはあなたが先に見据える触媒を指摘してください。暗号資産でも株式でも、あなたの選択です!

📌 やること:

- Edgen Xコミュニティ内に分析を投稿し、フォロワーにも見てもらえるようにしてください

- @EdgenTechをタグ付けして、カウントされるようにしてください

- 参加フォームを記入して、エキスパートテーブルに座るチャンスを得ましょう

最も重要なのは質です。リーダーボードは量よりも独創的で思慮深い分析を評価します。

あなた自身の視点をもたらし、市場全体の洞察を結びつけ、データがあなたにとって何を意味するのかを説明してください。

エキスパートテーブルの席

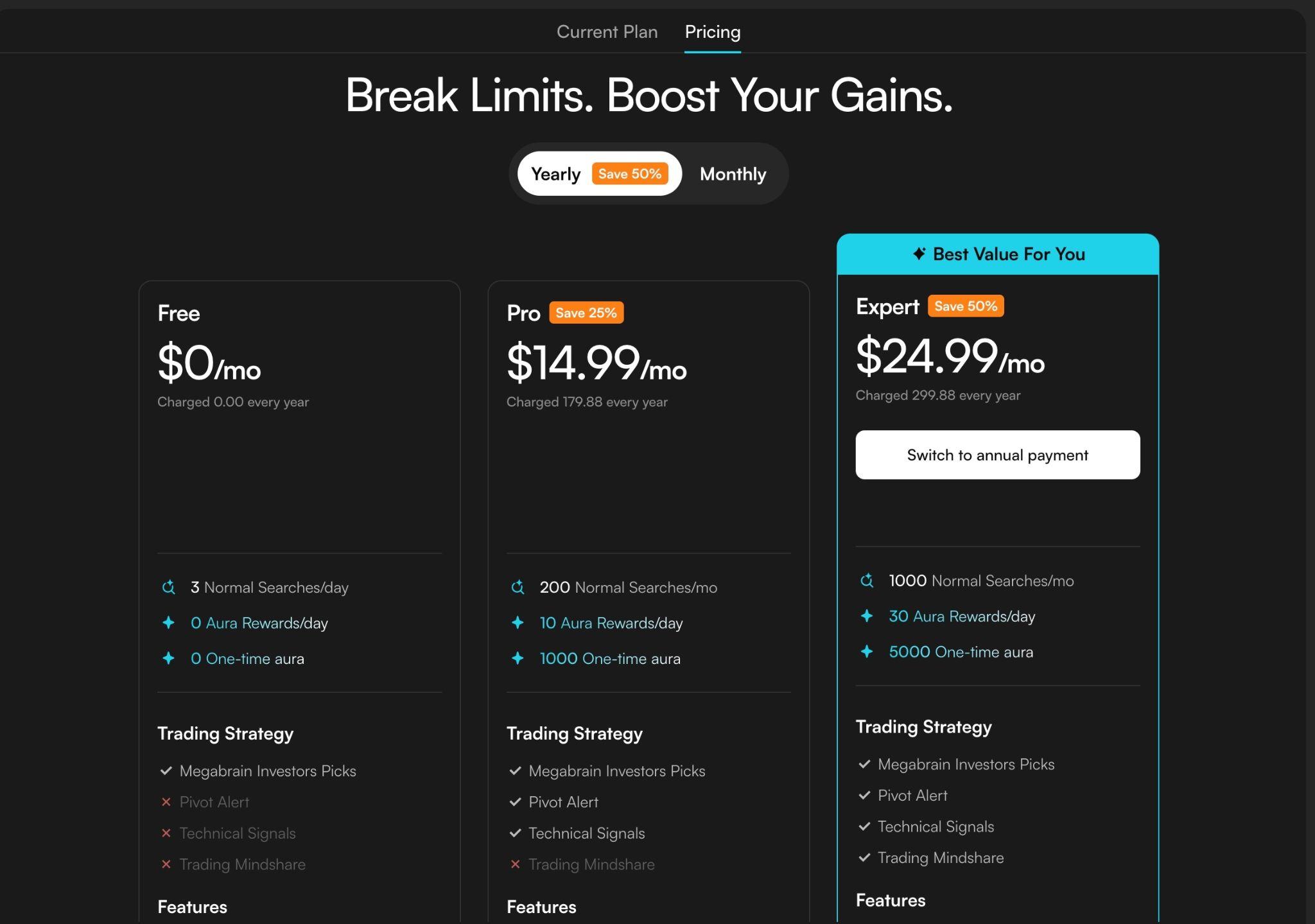

その週の終わりに、Edgen年間エキスパートプランに参加する3名の傑出した貢献者を選出します。エキスパートメンバーは、新機能への早期アクセス、より高速なAura処理、より深い分析、および高度なエージェントアクセスを利用できます。これは、あなたの投資の旅のターボボタンです。

リーダーボードを駆け上がろう

- 独創的であること:Yapperリーダーボードは、独自の視点をもたらすクリエイターを強調します。

- 全体像を捉えること:360°レポートは、ファンダメンタルズ、トークンエコノミクス、モメンタム、センチメントをカバーしています。それらがどのように関連しているかを示しましょう。

- 先を見据えること:予測ページの価格帯を、あなた自身の論文の足がかりとして使いましょう。その予測に同意しますか?同意する理由、または同意しない理由は何ですか?

- 参加し、盛り上げること:他の投稿にコメントし、質問し、会話を盛り上げる手助けをしましょう。リーダーボードは交流によって活気づきます。

あなたの番です:会話に参加しましょう

このチャレンジは、あなたの考え方を示し、市場への理解を深め、その功績を認められる機会です。あなたの声は、年間エキスパートプランを獲得し、トレーダーが毎日最初にチェックするものになるかもしれません。

Edgen Xコミュニティにアクセスし、360°レポートまたは予測ページを選び、あなたの見解を共有し、@EdgenTechをタグ付けして、フォームから参加してください。皆様がどのような貢献をしてくださるか、楽しみにしております。

LFG Ledgens!

投資、もうひとりじゃない

Ed を無料で試そう。クレカ不要、縛りなし