ミームコイン、アルトコイン、株式:なぜ AI が市場トレンドの鍵なのか

市場は変わった。永遠に。

お金は迅速に移動する。市場はさらに速く動く。

投資はチャート、貸借対照表、および基本的な要素を越えて進化した。今では、マコイン、アルトコイン、株式もソーシャルなブーム、インフルエンサーの感情、およびリアルタイムのブロックチェーン活動に従うようになった。

この変化の背後にあるエンジンはAIであり、トレーダーをより賢い意思決定、明確な予測、迅速な行動へと導いています。Edgen AIこの新しい市場の力は「ポンプァンタメンタルズ(Pumpamentals)」と呼ばれ、社会的な勢い、インフルエンサーの影響力、そしてコミュニティが主導する価格動向の交差点である。

AIなしでの取引は、他の人が明確に見ているシグナルを逃すことを意味する。AI取引が市場の成功を定義する。

メモコイン、アルトコイン、株式の説明

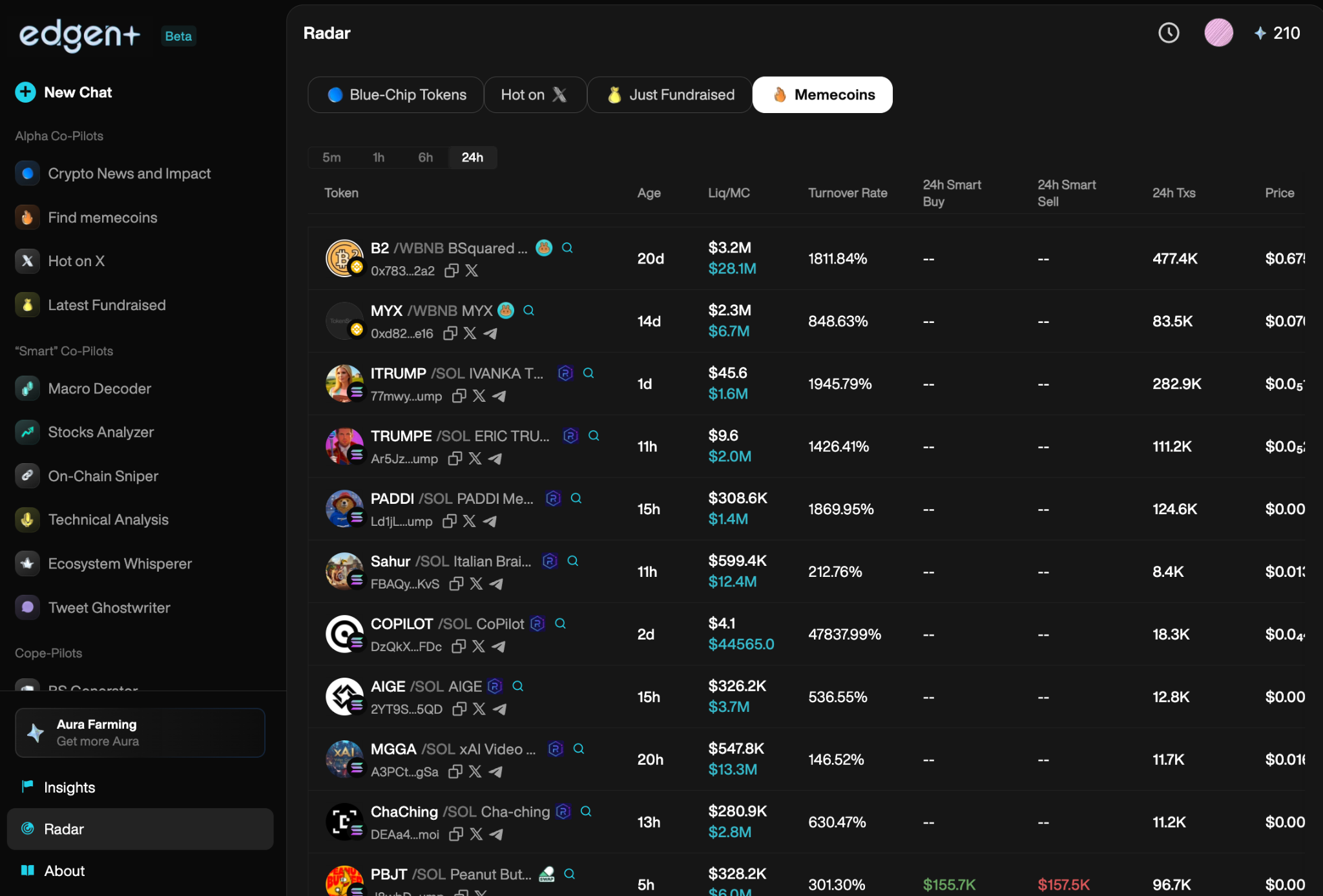

メモコイン:本気の利益をもたらすジョーク

マメコインはインターネットのジョークから始まった。ドジコイン(DOGE)、シバインウ(SHIB)、ペペコイン(PEPE)。伝統的な金融的強みを持たないこれらの資産は、ソーシャルな注目やウイルス的なミームによって急騰する。

メメコインの価格が急騰し、すぐに暴落する。Edgen AIトラックは、ツイッターの感情、ソーシャルエンゲージメント、インフルエンサーの動向を追跡し、パンプが発生する前にそれらを特定します。

アルトコイン:ビットコインの代替品以上のもの

アルトコインはビットコイン以外の暗号通貨を指し、イーサリアム(ETH)、ソラナ(SOL)、そしてAIに焦点を当てたトークンを含みます。 Learn more about altcoins, their types, and how they differ from Bitcoin. メモコインとは異なり、アルトコインは通常、明確な用途、機能、または現実世界での価値を提供します。

エッジンAIは、アルトコイン市場のシグナル、オンチェーンウォレットの動き、コミュニティの意見の変化を追跡し、早期にトレード機会を特定します。

株式:伝統的な資産の進化

株式はアップル、テスラ、アマゾンなどの主要企業の所有権を表します。従来の投資のルールは依然として適用されますが、AIは株式市場への投資を変革しています。現在、企業は収益報告、ニュース記事、投資家の感情を即座に分析するAI駆動のプラットフォームを使用しており、AIを活用した取引が不可欠となっています。

AIが現代の市場トレンドをどのように定義するか

AIが市場の感情を即座に予測する

投資家の感情が資産価格を決定します。Edgen AIはSNS(Twitter/X)およびブロックチェーンデータをスキャンし、市場の雰囲気の変化を広く認識される前に特定します。

- インフルエンサーおよびコミュニティの意見を即座に追跡します。

- 市場の動きの前に物語の変化を予測する。

AIを活用したブロックチェーンデータの習得

オンチェーン分析は、ウォレットの活動、資金の流れ、スマートマネーの行動などの隠れた市場サインを明らかにします。Edgen AIはブロックチェーンデータを明確に解釈し、ほとんどのトレーダーが気付く前にリアルタイムアラームを提供します。

例: Edgen AI は、低時価のアルトコインを多く保有する顕著なウォレットに気付きます。Edgen のラジオを使用するトレーダーは即座にアラートを受け取り、早期の利益を確保します。

アルファ・シグナル:AIの究極の利点

アルファシグナルは成長が見込まれる未評価の資産を強調しています。Edgen AIは膨大なデータを瞬時に処理し、急騰の兆候を迅速に明らかにします。ライブクエリを実行して、隠れたアルファを探りましょう。 Edgen Searchトレーダー向けのAI対応検索エンジン。

- 増加した開発者活動

- トークン保有者数の増加

- ソーシャルメディアでの言及が増加している

AIは、価格がそれらを反映する前にこれらの機会を特定します。

暗号通貨と株式におけるAI駆動型取引アルゴリズム

AI取引ボット:新しい基準

AI取引をより速く、より賢く、感情に左右されずに進めます。

AIは正確に、感情を排除して、異常に高速で取引を行う。高頻度取引(HFT)のボットはミリ秒単位で取引を行い、人間の能力を上回る。

Edgen Radar迅速な取引実行、リアルタイムでのアルファの特定、包括的な市場洞察に特化しています。

人工知能が社会的合意に出会う

技術的分析だけでは不十分です。Edgen AIは、社会的な感情やコミュニティの物語を統合することで、市場の集団的なマインドセットを捉えます:

- スマートウォレットの取引(購入/売却行動)

- キーオピニオンリーダー(KOL)の活動

- ツイッター/Xにおけるトレンドトピックとインフルエンサーの動向

AIが人間よりも早く社会的感情を検出する

ソーシャルな勢い、インフルエンサーのトレンド、コミュニティとの関わりが一晩で価格を押し上げます。Edgen AIはこれらのシグナルを継続的にモニタリングし、明確に評価しています。リアルタイムの市場の会話やコミュニティのアラファをモニタリングしてください。 Edgen Feed以下の英語を日本語に翻訳します。専門的な意味を保ち、書式を変更せず、過度な意訳は避けています:

:

- ビューリッシュなシグナル:ウイルス的エンゲージメント、インフルエンサーの注目が増加していること、ホエールの蓄積。

- 空売りの警告:減少する社会的関心、変化する物語、減退する関与。

AIは感情の変化を最初に捉え、市場の反応よりも先に決定的な取引を可能にする。

AIの未来の市場トレンドにおける重要な役割

AI + DeFi:市場の新たな境界

DeFiは金融をさらに変革し続けており、AIがその成長を加速させている。

エッジンAIは、完全な買方取引インフラに進化しました:

- 貸し出しと借り入れの戦略を自動化する。

- DeFiにおいてリスクを積極的に管理する。

- 最大限の収益を得るために収益農業を最適化する。

人間の分析だけではデファイのスケールにかなわない。AIが今や先頭に立って進んでいる。

ブロックチェーンとAI:パワフルなトレーディングのパートナーシップ

AIとブロックチェーン技術を組み合わせることで、市場の透明性と効率が大幅に向上します:

- AIが潜在的な脆弱性をチェックするためにスマートコントラクトを監査しています。

- 最適なガス料金と取引タイミングの予測。

- より良い取引実行のためのDEX分析の向上。

AIとブロックチェーンは、強力な取引環境を構成します。

なぜ現在、トレーダーにとってAIが不可欠なのか

AIは不可欠なものとなり、トレーディングの成功の未来を形作るようになった。

トレーダーはAIが必要な理由は:

- より迅速な意思決定:数百万のデータポイントを即座に処理。

- 優れた正確性:AIは人間の感情的なバイアスを除去します。

- 継続的な警戒:AIは市場の継続的なモニタリングを提供します。

- 即時のアルファのインサイト: AIはリアルタイムでの感情とオントレイン活動を明確に追跡します。

AIなしでの取引は投資家にとって深刻な不利な状況に陥れる。

トレードを賢く行うか、それとも後れを取るリスクを冒すか

市場は永続的に変化した。マメコイン、アルトコイン、および株式はAIによる洞察、社会的な物語、リアルタイムの分析に大きく依存している。

トレーダーがAIを無視すると苦戦する。エッジンAIなどのプラットフォームを活用する者は、ソーシャルセンチメントやアルファ検出、ブロックチェーン分析を活かし、他とははるかに先を行っている。

未来がやってきた。AIで駆動される取引が勝者と敗者を決定する。あなたの行動が市場での立場を決めます。 Learn more about Edgen AI.

投資、もうひとりじゃない

Ed を無料で試そう。クレカ不要、縛りなし