Una perspectiva sobre el L1 especializado de Somnia para el metaverso y los juegos, que abarca estrategia, socios, modelo de token, catalizadores y valoración. Para una guía sencilla para nuevos usuarios, haga clic aquí

EN RESUMEN

- L1 especializada para aplicaciones en tiempo real: La arquitectura (Consenso MultiStream, Ejecución Secuencial Acelerada, IceDB) se dirige a cargas de trabajo de "estado caliente" con las que otras cadenas tienen dificultades.

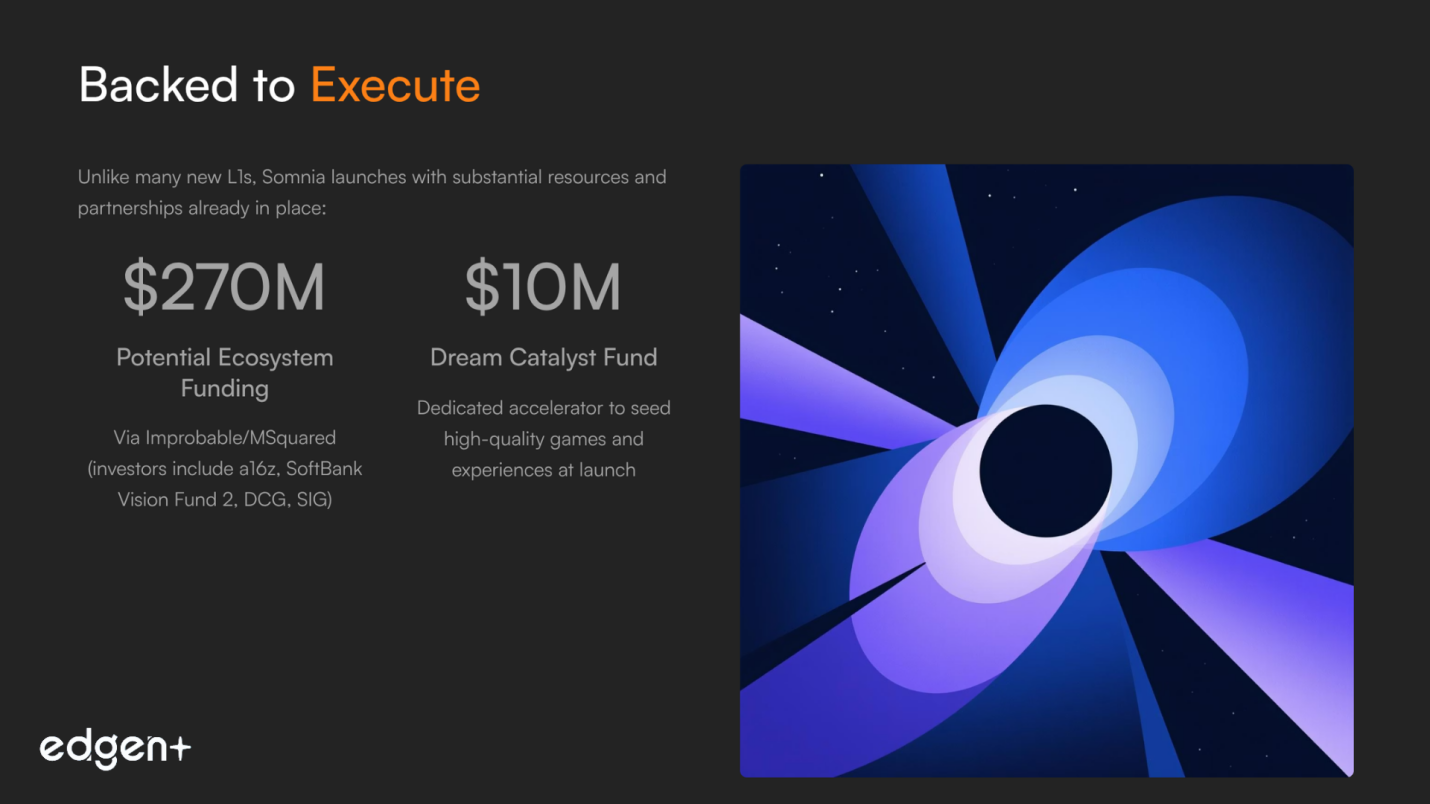

- Apoyado para ejecutar: Hasta 270 millones de dólares en financiación del ecosistema a través de Improbable/MSquared, validador/infraestructura de Google Cloud, y un Dream Catalyst de 10 millones de dólares para sembrar juegos, posicionando a Somnia para convertir la narrativa en productos enviados.

Qué es Somnia

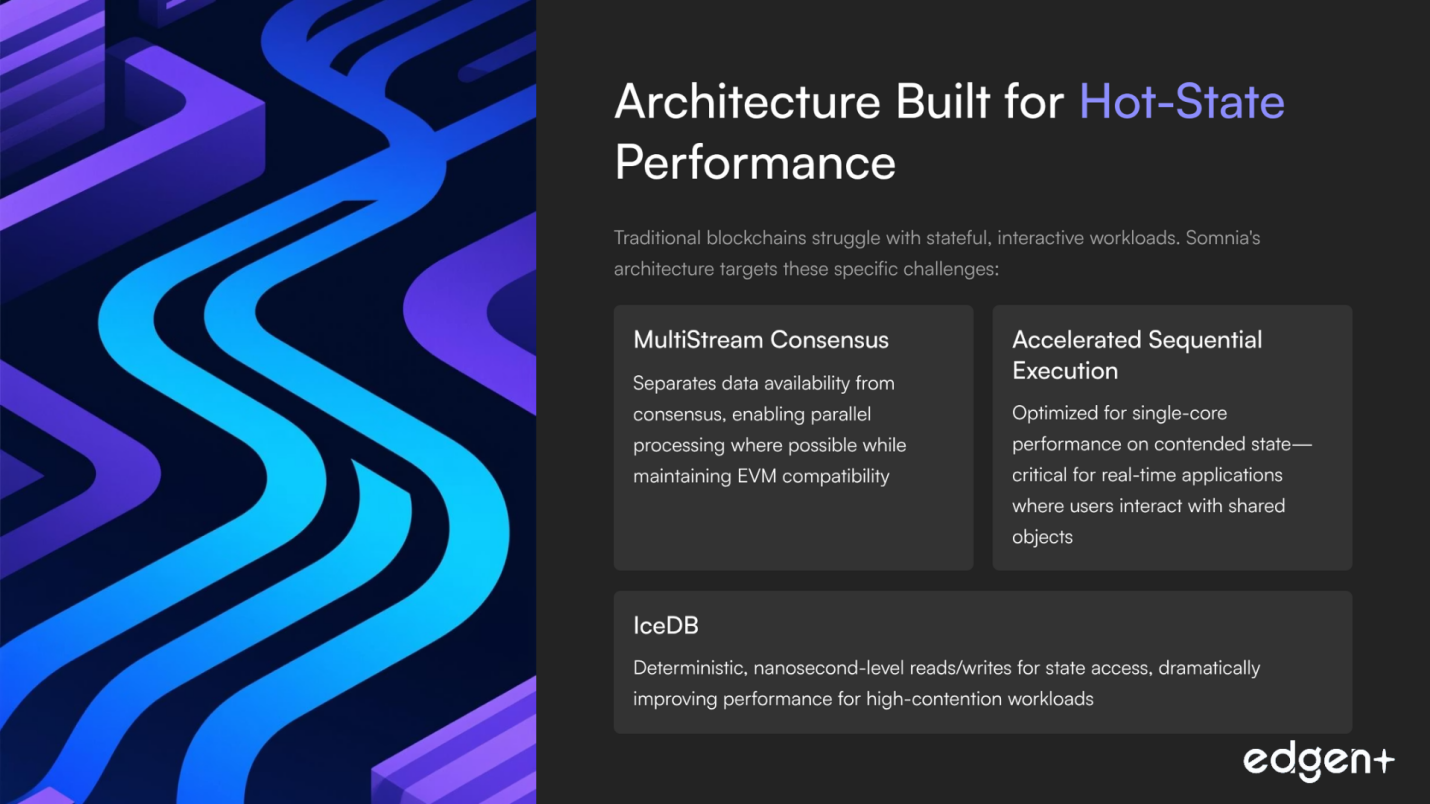

Somnia es una Layer-1 compatible con EVM diseñada para un rendimiento a escala del metaverso: finalidad en sub-segundos, tarifas por debajo del centavo y objetivos de más de 1 millón de TPS. En lugar de perseguir el rendimiento general de DeFi, Somnia está optimizada para cargas de trabajo interactivas y con estado —MMO, grafos sociales, economías en cadena— utilizando un diseño que acelera la ejecución de un solo núcleo para contención caliente mientras aprovecha el paralelismo del hardware. Su Consenso MultiStream separa la disponibilidad de datos del consenso, e IceDB apunta a lecturas/escrituras deterministas a nivel de nanosegundos.

Con el respaldo de la profunda experiencia de Improbable/MSquared en mundos virtuales, Somnia alinea la infraestructura con la realidad del desarrollador: herramientas EVM familiares, una pila de constructores de bajo código (a través de socios) y un acelerador bien financiado para aportar contenido desde el primer día. Con Google Cloud apoyando la validación y los servicios de seguridad de IA/datos, y estudios como Realm (Variance) preparándose para construir, la propuesta de Somnia es clara: una "computadora de ensueño" donde las experiencias Web3 se sienten instantáneas y componibles, listas para los usuarios principales.

I. Análisis fundamental y estratégico

1) Visión y alineación de inversores

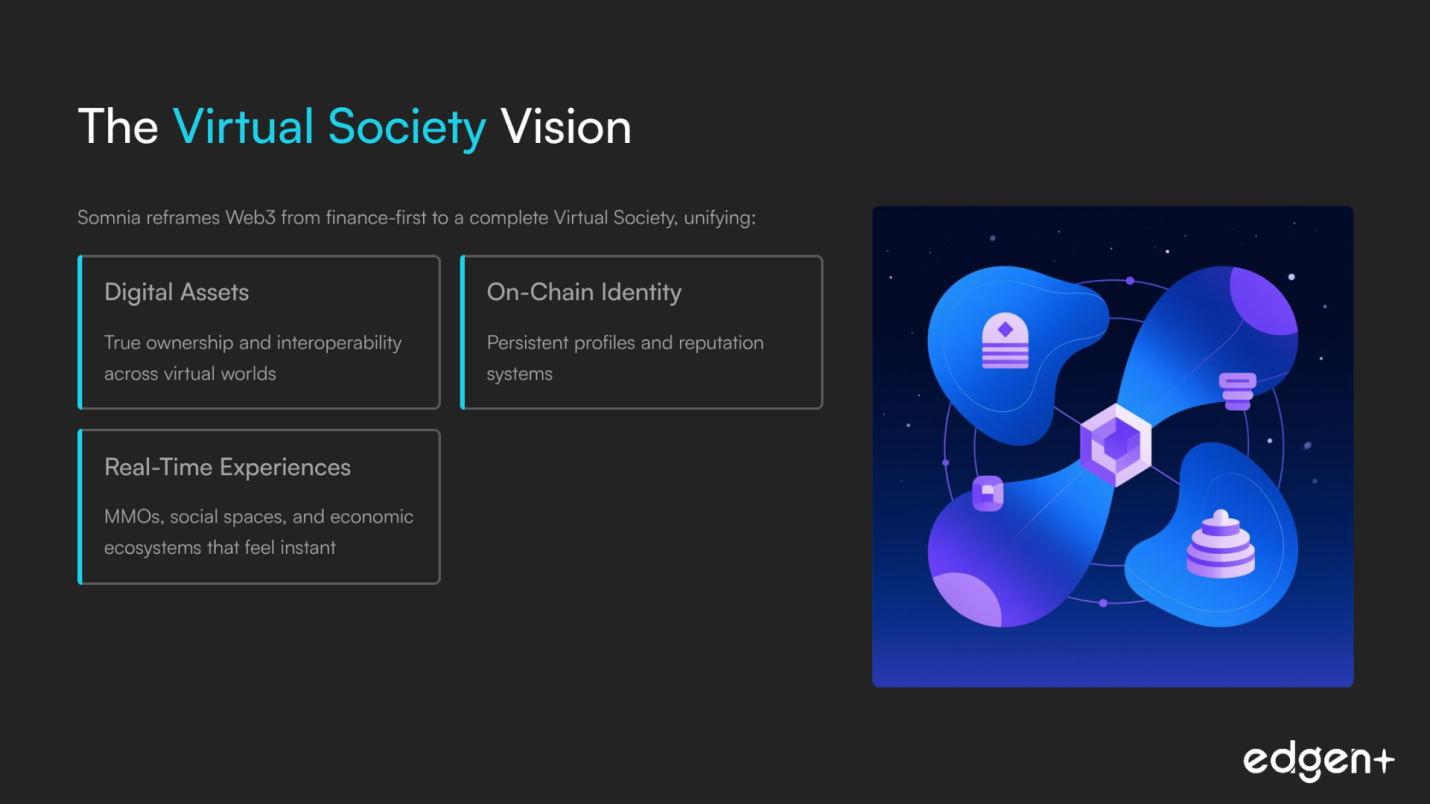

La tesis de Somnia se enfoca en: convertirse en la L1 especializada para metaversos/redes sociales/juegos, donde el rendimiento, la latencia y el costo deciden los ganadores. La estrategia reformula Web3 de financiero primero a Sociedad Virtual, unificando activos, identidad y experiencias. Las asociaciones (por ejemplo, alineación con Yuga Labs) y un acelerador de 10 millones de dólares señalan un compromiso a largo plazo con el contenido y el éxito de los desarrolladores.

2) Equipo y destreza de ejecución

El fundador Paul Thomas (Improbable) aporta una rara profundidad en sistemas distribuidos; Michelle Kang añade experiencia en crecimiento de L1/L2. La combinación de rigor en la infraestructura y conocimientos de GTM (Go-to-Market) apoya la entrega de protocolos complejos y la incorporación del ecosistema, lo cual es muy prometedor para una nueva L1.

3) Capital y avales

En lugar de rondas convencionales, Somnia se beneficia de una financiación del ecosistema de hasta 270 millones de dólares a través de Improbable/MSquared (los inversores incluyen a16z, SoftBank Vision Fund 2, DCG, SIG). Google Cloud valida a nivel empresarial (validador + IA/datos/seguridad), mientras que Sequence y Rarible aceleran la preparación de desarrolladores y del mercado.

4) Oportunidad y adecuación al mercado

Los juegos/metaversos en cadena son un mercado grande y en expansión. Somnia sirve a los desarrolladores que necesitan un rendimiento fiable y de alta contención con la familiaridad de EVM, además de subvenciones, SDKs y distribución, reduciendo así los costos de cambio tanto técnicos como financieros.

5) Posición competitiva y diferenciadores

Compite con cadenas EVM centradas en juegos (Ronin, Immutable zkEVM, GalaChain) y L1 de alto rendimiento (Solana, Aptos). Diferenciación: enfoque en la ejecución de estado caliente, EVM completo, una ambiciosa narrativa de "Sociedad Virtual" y un pedigrí auténtico de mundo virtual de Improbable.

Conclusión fundamental: Notable fortaleza fundamental con capital alineado, socios creíbles y un diseño específicamente creado para mundos en cadena en tiempo real.

II. Ecosistema previo al lanzamiento y estrategia de comercialización

1) Comunidad y momentum narrativo

El crecimiento en la parte superior del embudo es masivo, impulsado por la testnet y los incentivos. La oportunidad ahora es convertir la amplitud en profundidad, institucionalizar las comunicaciones, destacar las dApps enviadas y canalizar la energía de la comunidad hacia el uso de la red principal.

2) Huella en cadena

La actividad de la red de pruebas ha sido a escala de estrés, un campo de pruebas útil para los sistemas. El KPI clave después del TGE es el uso de calidad (DAU, carteras retenidas, dApps en vivo), no las transacciones en bruto.

3) Asociaciones y preparación

- Google Cloud: validador + integración de IA/datos/seguridad para desarrolladores.

- Sequence: carteras inteligentes, SDK de Unity/Unreal, pila de mercado para Somnia Builder.

- Uprising Labs: Dream Catalyst de 10 millones de dólares para sembrar juegos de alta calidad.

Juntos, estos elementos reducen la fricción desde el código hasta los usuarios y ayudan a asegurar contenido desde el primer día.

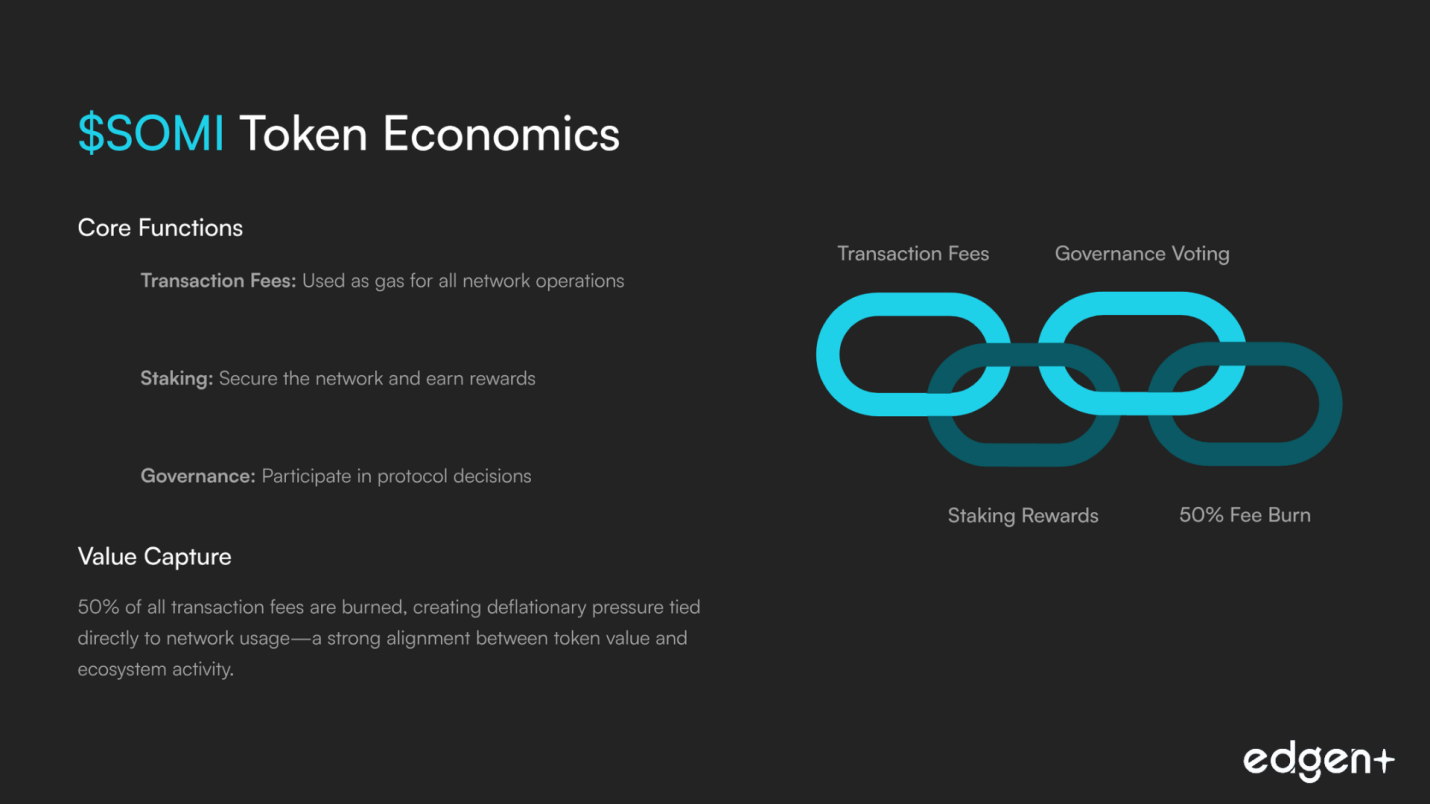

4) Tokenómica y acumulación de valor (hoy)

$SOMI: gas, staking, gobernanza. La quema del 50% de las tarifas alinea el valor con el uso. El Airdrop (5% del suministro) se distribuye a través de misiones semanales en la red principal (20% líquido en TGE; ~80% restringido por actividad durante ~60 días) para fomentar una participación real desde el principio.

Conclusión del GTM: Muy prometedor. La pila tecnológica, los programas y los socios apuntan a una fuerte velocidad de los desarrolladores; las operaciones de lanzamiento (custodia/MM/comunicaciones de liquidez) deben aclararse para maximizar la confianza el primer día.

III. Análisis prospectivo (Catalizadores y oportunidades)

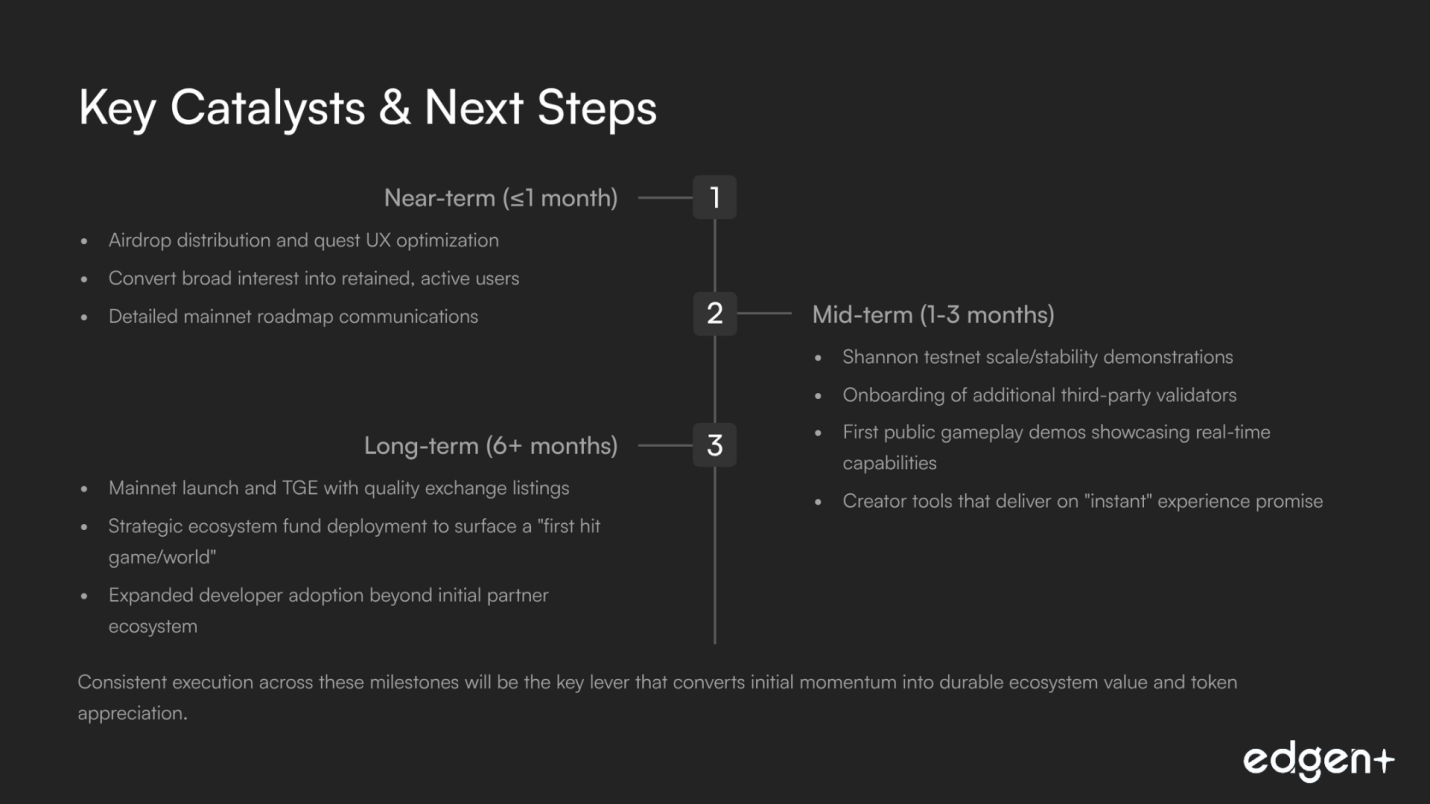

Corto plazo (≤1 mes):

- Comunicar los aprendizajes del airdrop + una UX de misión clara como el cristal. Convertir un interés amplio en usuarios felices y retenidos puede restablecer el sentimiento rápidamente.

Medio plazo (1-3 meses):

- Prueba de escala/estabilidad de la testnet Shannon y más validadores de terceros; primeros gameplays públicos y herramientas de creación que se sienten instantáneos.

Largo plazo (6+ meses):

- Mainnet + TGE con listados de calidad y liquidez; despliegue de fondos del ecosistema que dé lugar a un “primer juego/mundo exitoso”.

La cadencia de ejecución es la palanca que convierte el impulso en valor duradero.

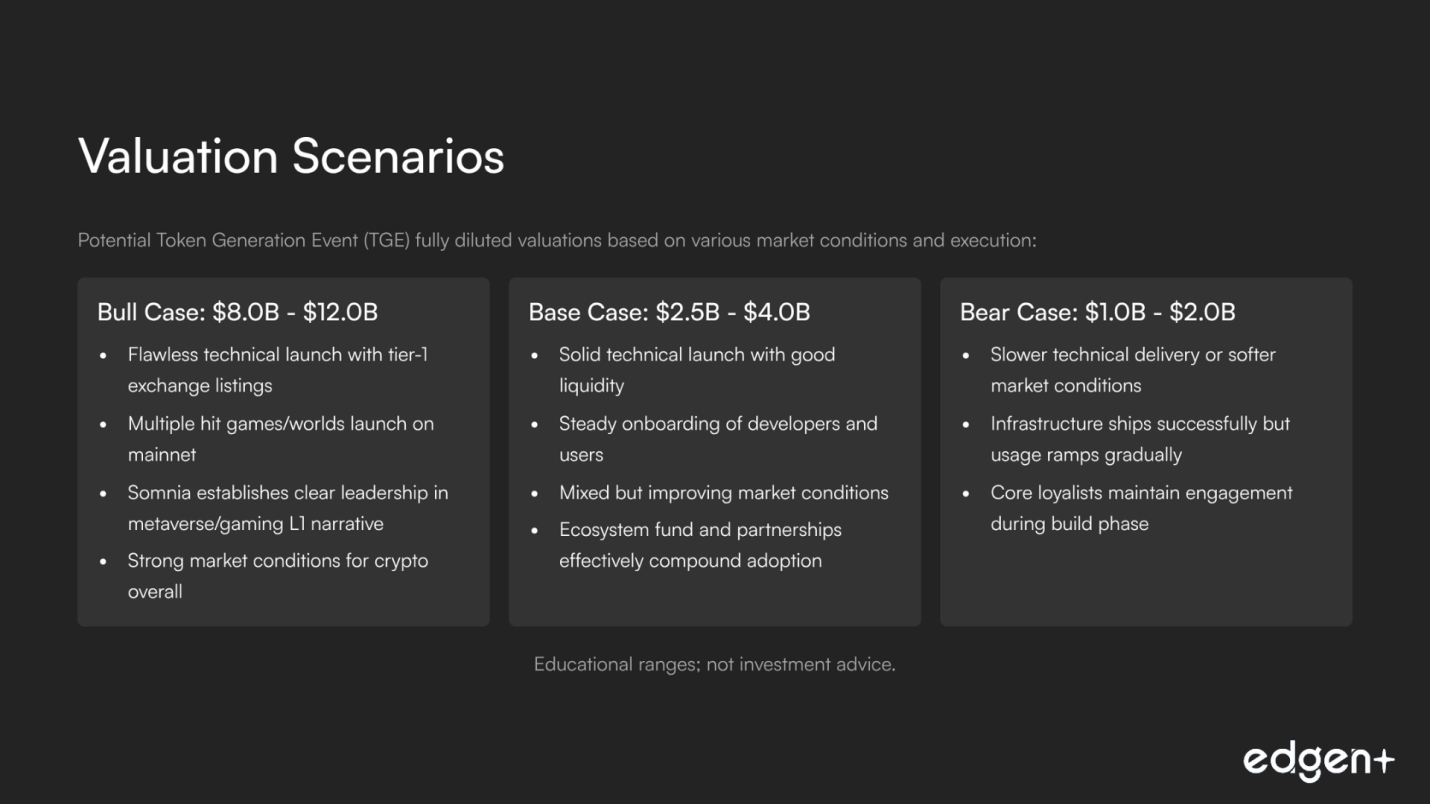

IV. Análisis de escenario de valoración (FDV de TGE)

Escenario | FDV (miles de millones de USD) | Breve narrativa |

Caso alcista | 8.0 – 12.0 | Lanzamiento impecable + listado de nivel 1; juegos exitosos en vivo; Somnia lidera la narrativa L1 de metaverso/juegos. |

Caso base | 2.5 – 4.0 | Tecnología sólida + incorporación constante en un mercado mixto; fondo + socios compuestas la adopción. |

Caso bajista | 1.0 – 2.0 | Entrega más lenta o mercado más suave; la infraestructura se envía, el uso aumenta gradualmente con los leales principales. |

Rangos educativos; no es asesoramiento de inversión.

Panorama de la competencia (ángulo del token en/cerca del TGE)

Red | Token | Enfoque | Posición en el caso base vs Somnia |

Ronin | EVM L1 para juegos (liderado por el editor) | Sólida trayectoria probada; Somnia compite en un alcance de mundo abierto más amplio y objetivos de rendimiento brutos. | |

Immutable zkEVM | $IMX | L2 para juegos, fuerza de mercado | Estudios e infraestructura profundos; Somnia contrarresta con rendimiento L1 + EVM + quema de tarifas. |

Solana | L1 de alto rendimiento (ejecución paralela) | Ecosistema maduro; Somnia se diferencia por su historia de rendimiento de estado caliente y la familiaridad con EVM. | |

Aptos | L1 de alto rendimiento (Move) | Tecnología fuerte; Somnia reduce la fricción de desarrollo a través de EVM + narrativa especializada de metaverso. |

Conclusión final

Somnia parece muy prometedor: un L1 especializado y compatible con EVM con un plan realista para potenciar mundos en cadena en tiempo real. Con una financiación de ecosistema significativa, socios de primera línea y un diseño dirigido directamente a cargas de trabajo de estado caliente, está configurado para transformar la visión en uso. El camino hacia una valoración en la banda superior es sencillo pero estricto: operaciones de lanzamiento claras como el cristal, juegos tempranos visibles, un TGE fluido y envíos consistentes.

Contenido educativo; no es asesoramiento financiero.

Invertir, por fin, ya no es cosa de uno solo.

Prueba Edgen gratis. Sin tarjeta, sin compromiso.