Yapay Zeka Güçlü Token'ları ve Memecoin Tradingi Nasıl Yapılır: Daha Akıllı Kripto Yatırımı İçin Başlangıç Rehberi

Kripto Trading'in Geleceği AI: Edgen AI'yi Tanıyın

Kripto işlemeleri ışık hızında değişir. Göz kırpmazsanız, bir sonraki büyük şeyi kaçıracaksınız. Son zamanlarda iki trend haberlerde yer aldı: Yapay zeka destekli token'lar vememecoinsticaret. Bunlar ne ve neden ilgilenmelisin?

Yapay zekâ destekli token'lar, piyasa hareketlerini tahmin etmek, trendleri tespit etmek ve nokta atış doğruluğuyla işlem yapmak için yapay zekâyı kullanır.MemekoinlarBu arada, internet meme'leri ve çevrimiçi kültüre dayalı oyuncu kripto para birimleridir. Genellikle şakalarla başlar ama bazen ciddi yatırımlara dönüşür (sana bakıyorum, Dogecoin).

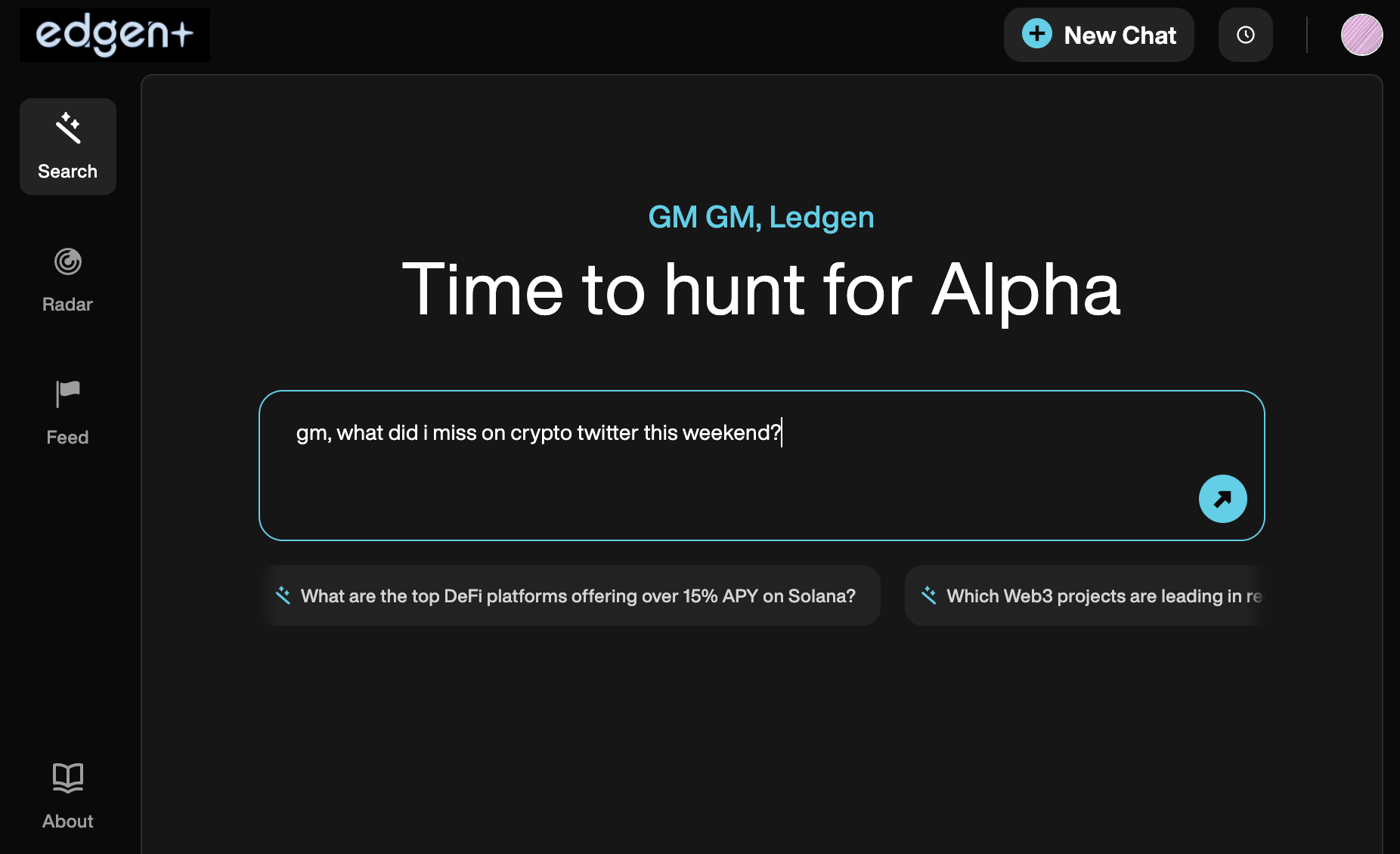

Yayın platformları gibiEdgen AI, tüccarlar, sosyal duygudan bant içi verilere kadar her şeyi izleyen anlık pazar analizi alır. Yeniysen, sabırlı ol: bu rehber token'lar ve hakkında tam olarak ne olduğunu açıklıyor.memecointicaret nedir, nasıl çalışır ve nasıl akıllı ve güvenli yatırım yapabilirsiniz.

AI Güçlü Token Trading Nedir?

Kısaca, yapay zeka destekli ticaret, ileri algoritmalar kullanarak kripto ticareti daha akıllı ve hızlı analiz eder. Veriler, öngörücü modeller ve makine öğrenimi tarafından yönlendirilir.

Neden Yapay Zeka Kripto Ticaretinde Önemlidir:

- Veri İşleme Gücü:AI, pazar verilerinin binlerini anında analiz eder.

- Öngörücü Doğruluk:Küme öncesi nokta fiyat değişimleri.

- Duygusuz Ticaret:İnsani önyargıları ve panikle tetiklenen hataları kaldırır.

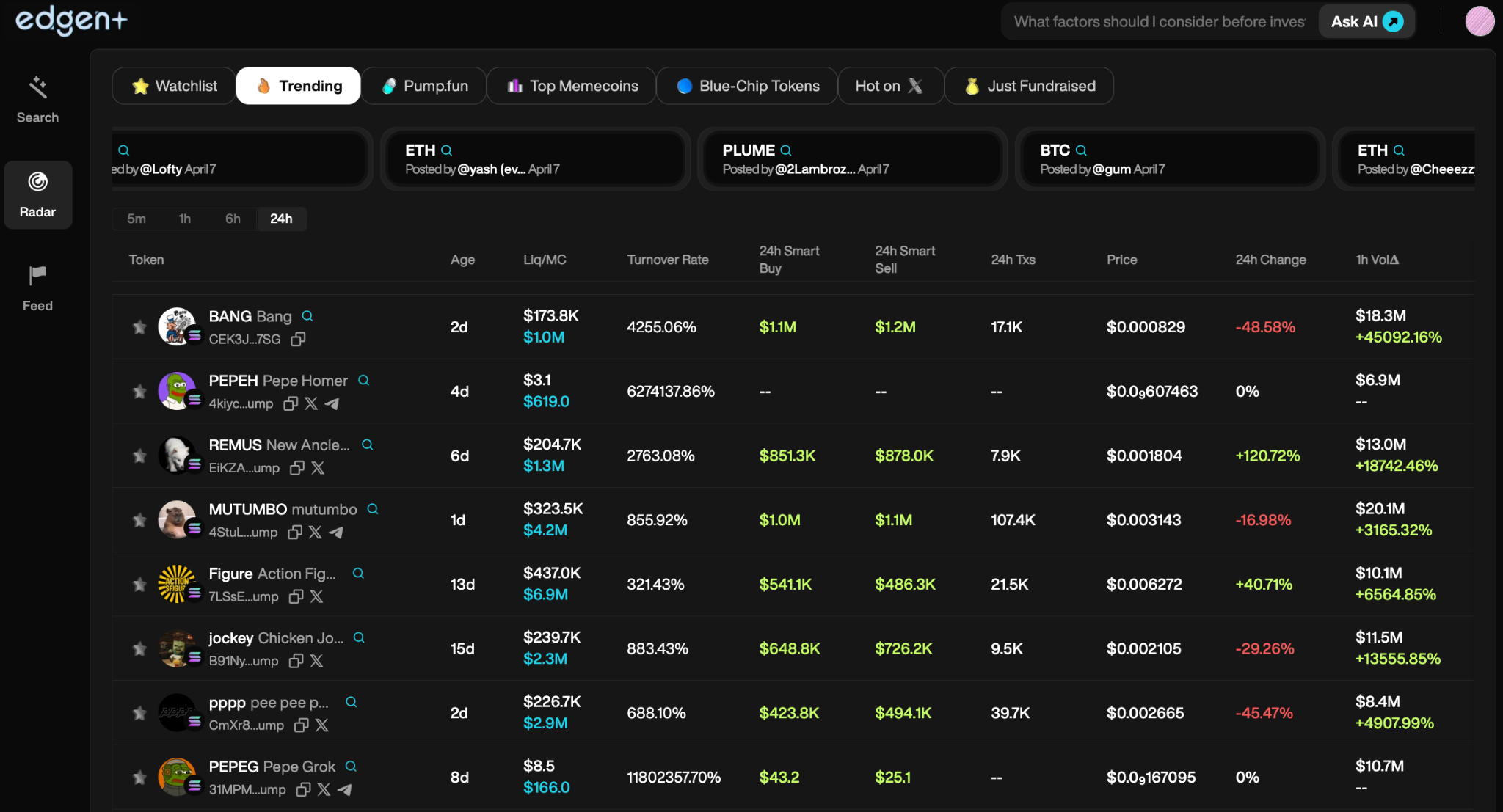

- Sosyal Duygu Takibi:Araçlar kullanarak erken hiperti tespit eder gibi Edgen Radar

Kripto para ile ticaret yaparken AI olmadan? Bu harika... ama eski.

MemekoinlarAçıklama: Sadece Şakalar mı?

Memekoinlarİnternet kültürü ve şakalarını yakalayan kripto para birimleridir, viral popülerliği kripto değere dönüştürür. Şaka kaynaklı olarak doğarlar, topluluk hırsı ve viral momentum üzerinde gelişirler.

ÜnlüMemekoinlar:

- Dogecoin (DOGE):Orijinalmemecoin, bir şakadan doğdu, şimdi ciddi bir oyuncu.

- Shiba Inu (SHIB):Popüler Dogecoin rakibi, büyük topluluk, büyük volatilite.

- Pepe Coin (PEPE):Sıkı Pepe the Frog cizgi dizisi tarafından esinlendi, hızlıca kult statüsü kazandı.

Neden Yatırım YapmalıyızMemekoinlar?

- Topluluk Yönlü Büyüme:MemekoinlarHype, FOMO ile karşılaştığında patlar.

- Yüksek Ödül Potansiyeli:Hızlı kazançlar (ve kayıplar) sıklıkla olur.

- Kültürel Eğlence:Yatırım yapmakmemecoinsgenellikle canlı bir toplulukla birleşmek anlamına gelir.

Amamemecoinsyüksek riskli uyarı ile gelirler: volatil ve tahmin edilemezdir. KullanımEdgen Radar, tüccarlar gerçek zamanlı sosyal trendleri izleyebilir, bu da ... içinde yaratıcı bir avantaj sağlarmemecoindağ treni

Yapay Zeka, Kripto Ticareti Nasıl Devrimleştiriyor

Yapay zeka sadece lüks değil; modern yatırımda yeni standarttır. Piyasa tahmini ve otomatik işlemeye kadar, yapay zeka tüccarlar için doğrulukla çalışmayı sağlar. Bu teknolojilerin geleneksel finansı nasıl dönüştürdüğünü keşfetmek istiyorsan, bakın: CFA Institute’s report on AI in asset management.

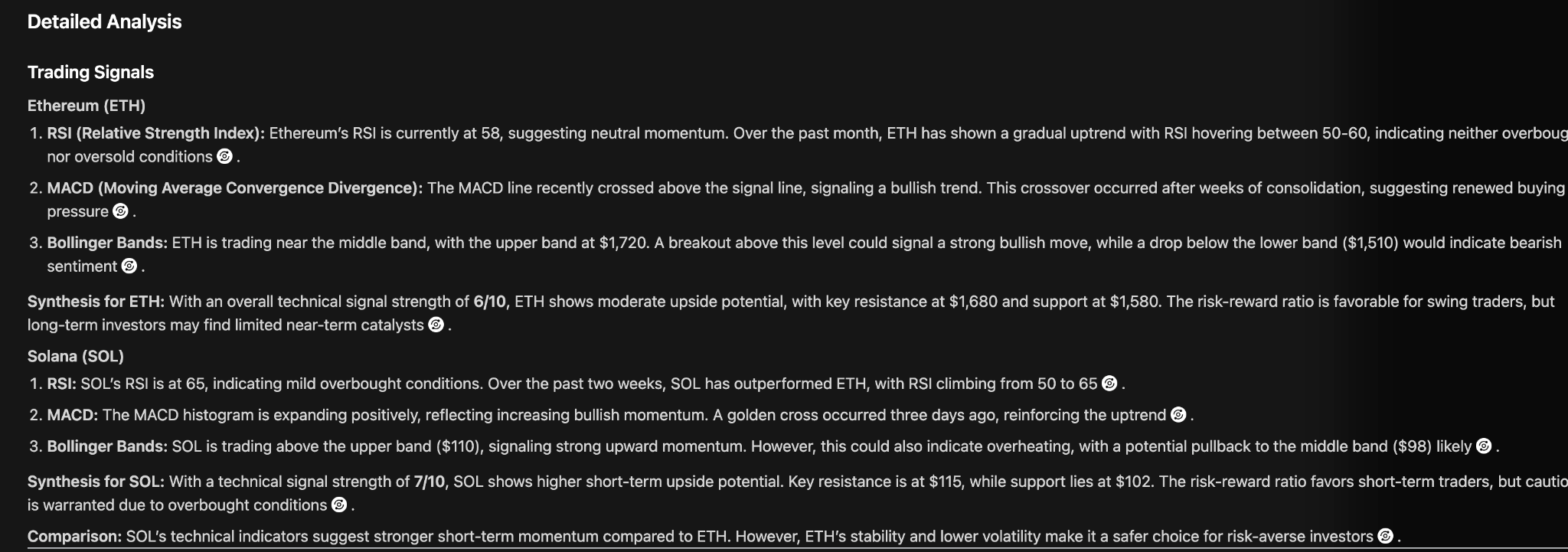

Öngörücü Pazar Analitikleri

AI, insan ticaretçilerinin tepki vermesinden daha hızlı kalıpları analiz eder ve pazar dalgalanmalarını tahmin eder.

2. Otomatik Trading Bot'ları

AI bot'lar, alışveriş verimliliğinizi kesintisiz olarak maksimize ederek 24/7 stratejileri uygular.

3. Gerçek Zamanlı Duygusal ("Pumpamentals")

Edgen AIakıllı hesapları, KOL'ları ve sosyal havalığı takip eder. Bir sonraki viral şeyi fark edersinmemecoinerken, geç değil.

4. Duyguları Kaldırma

İnsanlarpanik,AI yapmaz. İşlem kararları veriye dayalı, disiplinli ve güvenilirdir.

5. Güçlendirilmiş Güvenlik

AI, dolandırıcılığı, şüpheli aktiviteyi ve sahtekârlığı daha hızlı tespit ederek kriptonuzu daha güvende tutar.

Adım Adım Kılavuz: Token'lara Yatırım veMemekoinlarYapay Zeka ile

Daha akıllıca alım satım yapmaya hazır mısınız? İşte oyun planınız:

Adım 1: Profesyonel Bir Şekilde Araştırmak

KullanımEdgen Searchtoken tarihine, kullanım senaryolarına, piyasa hareketlerine ve sosyal yankıya derinlemesine inmek için kullanın.

Adım 2: Güvenilir Bir Borsa Seçin

Güvenilir DEX (Uniswap,Pancakeswapveya CEX (Binance, Coinbase, Kraken) ile sorunsuz bir şekilde bağlandıktan sonraEdgen Radar.

Adım 3: Kripto Para Alın

Bekleyen fonları yatır, token'larını değiştir ve onları güvenli bir şekilde sakla.

Adım 4: Yapay Zeka ile Piyasaları İzle

Fayda sağlamaEdgen Radargerçek zamanlı pazar sinyalleri için, hem blockchain aktivitelerini hem de sosyal trendleri izleyin.

Adım 5: Riskleri Akıllıca Yönetin

Sorumlu yatırım yapın. Her iki token vememecoinsyüksek riskli,yüksek ödüllüoynar. Tüm tasarrufunuzu YOLO yapmayın.

Riskler ve Gerçeklikler: Her İşçi'nin Bilmesi Gerekenler

Çok heyecan verici mi? Kesinlikle. Riskli mi? Kesinlikle değil. Şunlara dikkat etmelisin:

Aşırı Volatilite

Kripto pazarlar tahmin edilemezdir ve hatta yapay zeka her tek yuvarlak topu yakalayamaz.

2. Rug Pull'ler ve Sahtecilikler

Her zaman yatırım yapmadan önce projeleri kontrol edin. Kullanın Edgen Searchsahtecilikleri filtrelemek için

3. Yapay Zeka Sihir Değildir

AI, tarihsel verilere dayanır ve her zaman gelecekteki hareketleri %100 doğru şekilde tahmin etmez.

4. Düzenleyici Riskler

Hükümet eylemleri, kripto arayüzünü gece yarısında değiştirebilir.

SSS: Başlangıç Yapanlar En Çok Ne Sorar

1.Yapay zekâ ile token alım satımı iyi bir yatırım mı?

Potansiyel olarak evet. Veriye dayalı görüşler ve hızlı işlem yürütme sunar ancak hâlâ piyasa riski taşır. Her zaman detaylı araştırmalar yapın.

2.Yapay zeka ticaret botları nasıl çalışır?

Bot'lar gerçek zamanlı pazar ve sosyal verileri analiz eder, ardından işlemleri anında otomatikleştirir. Platformlar gibiEdgen Radarakıllı cüzdanları ve piyasa eğilimlerini izleyin, sizin önde olmanızı sağlayın.

3.Ne var?memecoinriskler?

Memekoinlarçok volatil ve spekülasyon odaklıdır. Fiyat, katı temeller yerine topluluk ve yankı tarafından belirlenir. Pompa ve dökme düzenlerine ve dolandırıcılıklara dikkat edin.

4.AI, kripto fiyatlarını doğru şekilde tahmin edebilir mi?

AI tahminleri önemli ölçüde geliştirir, ancak kripto hâlâ tahmin edilebilir değildir. Ancak dış faktörler (düzenleme, haberler, büyük olaylar) pazarları hâlâ şaşırtabilir.

5.Başlangıç seviyesindeki yatırımcılar nasıl yatırım yapmaya başlar?

Kullanım Edgen Search, iyi bir borsa seçin, güvenli yatırın ve yolculuğunuzu yolu izleyin via Edgen Feed.

Sonuç: Yapay Zeka +Memecoinİşlem Devrimi

Kripto ticaretin geleceği, yapay zeka zekâsıyla toplulukla beslenen hiperbolün birleşimidir. Yapay zeka, tüccarlar için karmaşıklığı yönlendirirken,memecoinsçekici, ancak riskli kültürel yatırımlar sunuyor.

Platform'lar gibiEdgen AIbu revolüsyonu liderlik et, gerçek zamanlı zincir üzerindeki görüşleri sosyal analizlerle birleştir. Bunun hakkında herkesinkinden daha akıllı ve hızlı olarak şimdikini net bir şekilde görmek.

Yapay zekâ destekli token'ları benimsemeye hazır mısın vememecoinsÖnce küçük başla, akıllı ticaret yap, bilgilendir, ve letEdgen AIsizleri kripto pazarının dinamiklerini yönetmeye yardımcı olun.

Yatırım yapmak artık yalnız bir iş değil.

Edgen'i ücretsiz dene. Kart yok, taahhüt yok.