AI'nin Ticarette Geleceği: Sosyal Veri ve Zincir Üstü Görünümle Daha Akıllı Yatırımlar

AI, Piyasa Oyununu Revizyona Açıyor

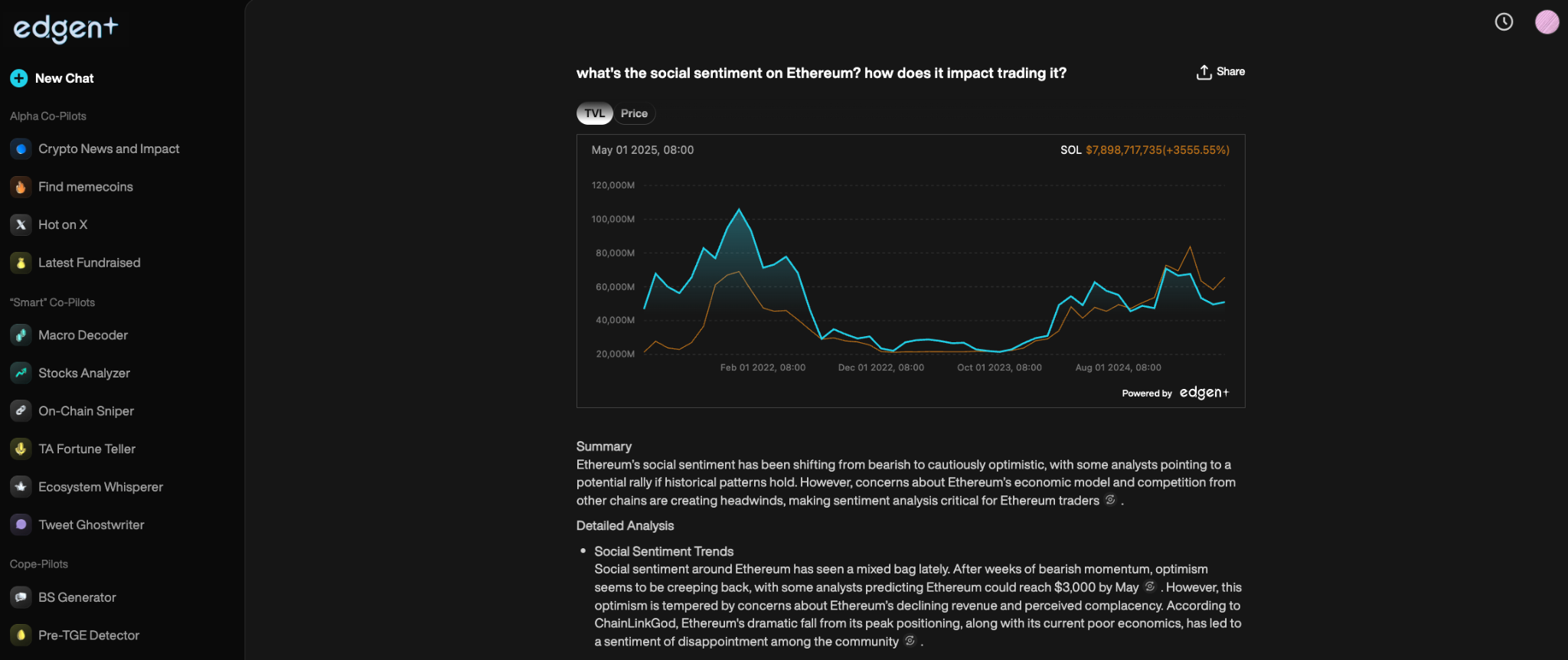

Finansal piyasalar artık sadece grafikler ve temeller tarafından hareket ettirilmemektedir. Sosyal medya sesi, etkili yorumcuların yorumları ve canlı blok zinciri aktivitesi artan oranda varlık fiyatlarını şekillendirmektedir.

Yapay zeka destekli araçlar gibiEdgen AIverileri olağanüstü hızla analiz ederek, tüccarlar için anında bilgiler ve güçlü tahminler sunar. Bu araçları kullanan tüccarlar, manuel analizlere dayananlardan daha iyi performans gösterir.

AI'nin Daha Akıllı Yatırım Stratejileri Oluşturması

Yapay Zeka, İnsanlardan Daha Hızlı Piyasayı Analiz Ediyor

Geleneksel yöntemler, modern pazar hızına yetişememektedir. İnsanlar milyarlarca veri noktasını gerçekçi şekilde izleyememekte, canlı haberleri işlememekte ve piyasa hareketlerini anında tahmin edememektedir.

Yapay zekâ destekli platformlar insan yeteneklerini şu şekilde aştığı için:

- Büyük gerçek zamanlı veri kümelerini hızlıca işleyin.

- Sosyal medya sinyalleri ve blok zinciri işlemlerinden piyasa hareketlerini tahmin etmek.

- Daha kötü yatırım kararlarına neden olan duygusal önyargıları ortadan kaldırmak.

Bu, anlık veriye dayalı analizlere dayanan daha akıllı yatırım kararları sonucuna neden olur.

Sosyal Veri Analizi: Konuşmaları Pazar İhtisascına Dönüştürme

Sosyal Veri Analizini Anlamak

Sosyal veri analizi, varlık fiyatlarını etkileyen çevrimiçi sohbetleri, duygusal değişimleri ve ortaya çıkan eğilimleri izler. Yapay zeka hızlıca kaynakları tarar, bunlar arasında:

- Twitter/X: Etkileyici konuşmaları, perakende alıcı duygusu.

- Finans Haberleri & Bloglar: Piyasa hareketi oluşturan açıklamalar.

- Zincir Üzeri Etkinlik: Gerçek zamanlı cüzdan hareketleri ve blok zinciri işlemleri.

AI, ticaretçilerin ana akım pazarların bilinçli olmasından önce trendleri tespit etmelerini sağlar.

Yapay Zeka Sosyal Verileri Eylem Uyarılarına Dönüştürür

Edgen AI gelişmiş makine öğrenimi kullanır, natural language processing (NLP)ve büyük veri analizi ile sosyal verilerden kritik desenleri belirlemek için, örneğin:

- Pozitif duygusal artışlar alım fırsatları için uyarılar tetikler.

- Negatif duygusal büyüme, fiyat düşüşlerini işaret eder.

- Etkili görüş değişiklikleri, trend tersliklerini erken sinyal verir.

Gerçek zamanlı sosyal duygusal analiz, tüccarlar için kritik zaman avantajları sağlar.

Duygu Analizi: Piyasanın Duygularını Çözmek

Duygu Analizi Nedir?

Duygu analizi, çevrimiçi metinlerde insan duygularını ve tutumlarını yorumlar ve pazar tartışmalarını şu kategorilere ayırır:

- Alıcı (Pozitif):Muhtemel fiyat artışlarını gösterir.

- Alçalıcı (Negatif):İşaret fiyat düşüşlerini potansiyel olarak belirtir.

- Nötr (Belirsiz):Yaklaşan volatiliteyi önerir.

Edgen AI, aynı anda binlerce çevrimiçi sohbeti analiz ederek, karar verme süreçlerine net duygusal bilgiler sağlar.

Edgen AI, Hisse Senedi Analizi ile Nasıl Ticareti Geliştirir

Sosyal tartışmaları hızlıca tarayarak, Edgen AI, tüccarları şu şekilde donatır:

- Fiyatlar artmadan önce pazar coşkusunu fark edin.

- Düşüşlerden önce olumsuz duygusal değişimleri belirleyin.

- Online aktiviteyi sahte veya yapay olarak artırılan şekilde tespit edin.

Ticaretçiler tarafından kullanılarak Edgen FeedCanlı hissi, ortaya çıkan token konuşmaları ve kitlelerin tahmin ettiği alfa'ya erişerek anlık avantaj kazanın.

Alternatif Veriler: Daha Fazlasını Görmeyen Piyasa Sinyallerini Ortaya Çıkarma

Geleneksel finansal metrikler ve temeller yeterli değildir. İşçiler şimdi eşsiz işlem sinyalleri için alternatif veri kaynaklarına bağımlıdırlar. EDGEN AI alternatif verileri takip eder, örneğin:

- Zincir Üzerindeki İşlemler:İçten ticareti ortaya çıkarır, açık olmadan önce.

- Arama Eğilimleri:Virüslenmeden önce ortaya çıkan token'ları izleyin using Edgen Radar Trendingzincir içi momentum ve sosyal zirvelerle güçlendirilmiştir.

- Sosyal Medya Davranışı:Yüksek perakende yatırımcı ilgisini gösterir.

Edgen Radarbu veri akışlarını sürekli olarak analiz eder ve tüccarlara karar vermede avantaj sağlar.

Yapay Zeka Yönlü Trading'in Geleceği: Bir Sonraki Adım Nedir?

Yapay zeka ticaret araçlarının evrimi hızlanmaktadır. Yaklaşan yenilikler şunlardır:

- İyileştirilmiş Sosyal Zeka:Etkileyici hikayelerini ve çevrimiçi duyguyu doğru şekilde takip edin.

- İleri Seviye Zincir İçi Analizler:Karmaşıklık blok zinciri verilerinin yapay zeka ile çözülmesi ve akıllı para hareketlerinin belirlenmesi.

- Tamamen Otomatik Trading Bot'ları:Kendini öğrenen, gelişmiş stratejileri otomatik olarak uygulayan yapay zeka.

Neden Edgen AI Yapay Zeka Piyasa Devrimini Liderlik Ediyor

Edgen'in arka planındaki yapay zeka altyapısının ne kadar etkili olduğunu öğrenin. About Edgen, burada tüccarlar için gerçek zamanlı görüşler, öngörücü analizler ve toplulukla desteklenen sinyaller sağladığını keşfedeceksiniz.

- Zincir içi temel verilerin ve sosyal "gerçek zamanlı analizipompa temelleri."

- Edgen Searchsaniyeler içinde herhangi bir insanın yazma, kaydırma veya filtreleme yapmasından daha hızlı derin pazar görebilirlikleri ortaya çıkarır.

- Yapay zeka destekli topluluk tarafından üretilen işlem sinyalleri.

Traders, Edgen AI'yi kullanarak sürekli olarak artan yapay zeka destekli pazarlarda önde kalır.

Yapay Zeka Trading'ı Benimseyerek Pazar Avantajını Koruyun

AI, ticareti temelden yeniden şekillendirir: sosyal duygusal durum, blok zinciri verileri ve algoritmik hassasiyet artan şekilde yatırım kararlarını yönlendirir.

Edgen AI gibi yapay zeka çözümlerini benimseyerek, tüccarlar şunları yapabilir:

- Piyasa değişimlerini anlık duygusal analizlerle hızlıca tanımlayın.

- Yapay zekâ destekli algoritmalar kullanarak hızlı ve kesin ticaret yapın.

- Öngörücü analitiklerle yatırım risklerini proaktif şekilde yönetin.

Gelecek, yapay zeka destekli zekâsının yeteneklerini benimseyen tüccarlarındır. Daha akıllı ticaret yapmaya ve pazar avantajınızı korumaya hazır mısınız?

Küçük Grup Öncesi Alfa Bulmaya Hazır Mısın?

Piyasa hızlı hareket eder, geride kalmayın. ile Edgen Search, blok zinciri eğilimlerini, sosyal duyguyu ve ortaya çıkan hikayeleri anında tarama imkanı sunarak, popüler olmadan önce gerçek alfa'ya ulaşabilirsiniz.

Şimdi Edgen Search ile keşfetmeye başla ve daha akıllı, daha hızlı işlem kararları ver.

Yatırım yapmak artık yalnız bir iş değil.

Edgen'i ücretsiz dene. Kart yok, taahhüt yok.