Alpha Trading: Piyasayı Yenmenin Akıllı Yolu

Alpha Trading Nedir?

Çoğu kripto tüccarı para kaybeder. Neden? Kritik bir avantajları yok. "Alpha" adı verilen bir avantaj.

Alpha ticareti, pazar benchmark'lerini sürekli olarak aşmakla ilgilidir. Temel grafikler veya temellerin ötesine geçer. Bugün piyasa hareketleri anlatılar, veri eğilimleri ve sosyal momentum'a göre gerçekleşir.

Yapay zeka destekli platformlar gibiEdgen AI sadece büyük pazar verilerini anında işler, insan ticaretçilerinin kaçırdığı gizli kalıpları ve alfa sinyallerini tespit eder. Blockchain analitiği, sosyal duygusal analiz ve ileri yapay zeka ile birleştirerek Edgen kör noktaları ortadan kaldırır ve rekabet avantajı sağlar.

İşlemde Alpha Tanımlaması

Alpha, standart piyasa performansının ötesinde getirileri ölçer. put:

Örnek için:

- Piyasa referansı %7 artarsa, ancak portföyünüz %12 artarsa, alfanız +5% olur.

- Bu ek %5, daha iyi pazar bilgisi, daha hızlı tepkiler ve daha akıllı kararlar sonucu oluşur.

Bu ek %5, daha iyi pazar bilgisi, daha hızlı tepkiler ve daha akıllı kararlar sonucu oluşur.Portföy performansında alpha'nın nasıl çalıştığını daha ayrıntılı bir şekilde görmek için lütfen aşağıdaki bağlantıyı inceleyinCorporate Finance Institute’s explanation of alpha.

Bugün Piyasa Yatırımcıları Nasıl Alpha Buluyor?

Alpha sinyalleri tanımlanabilir kaynaklardan gelir:

- Yapay Zeka Yönlü Görüşler: Makineler, insan kapasitesinin ötesinde büyük veri kümelerini analiz eder.

- Sosyal Duygu Takibi: Piyasa hareketleri genellikle sosyal medya tarafından yönlendirilen hikayelere uyar.

- Zincir Üzeri Analitik: Önemli cüzdan etkinlikleri potansiyel değişimleri işaret eder.

- Hızlı Pazar Yanıtı: Hızlı tepkiler, volatil pazarlarda karlılığı belirler.

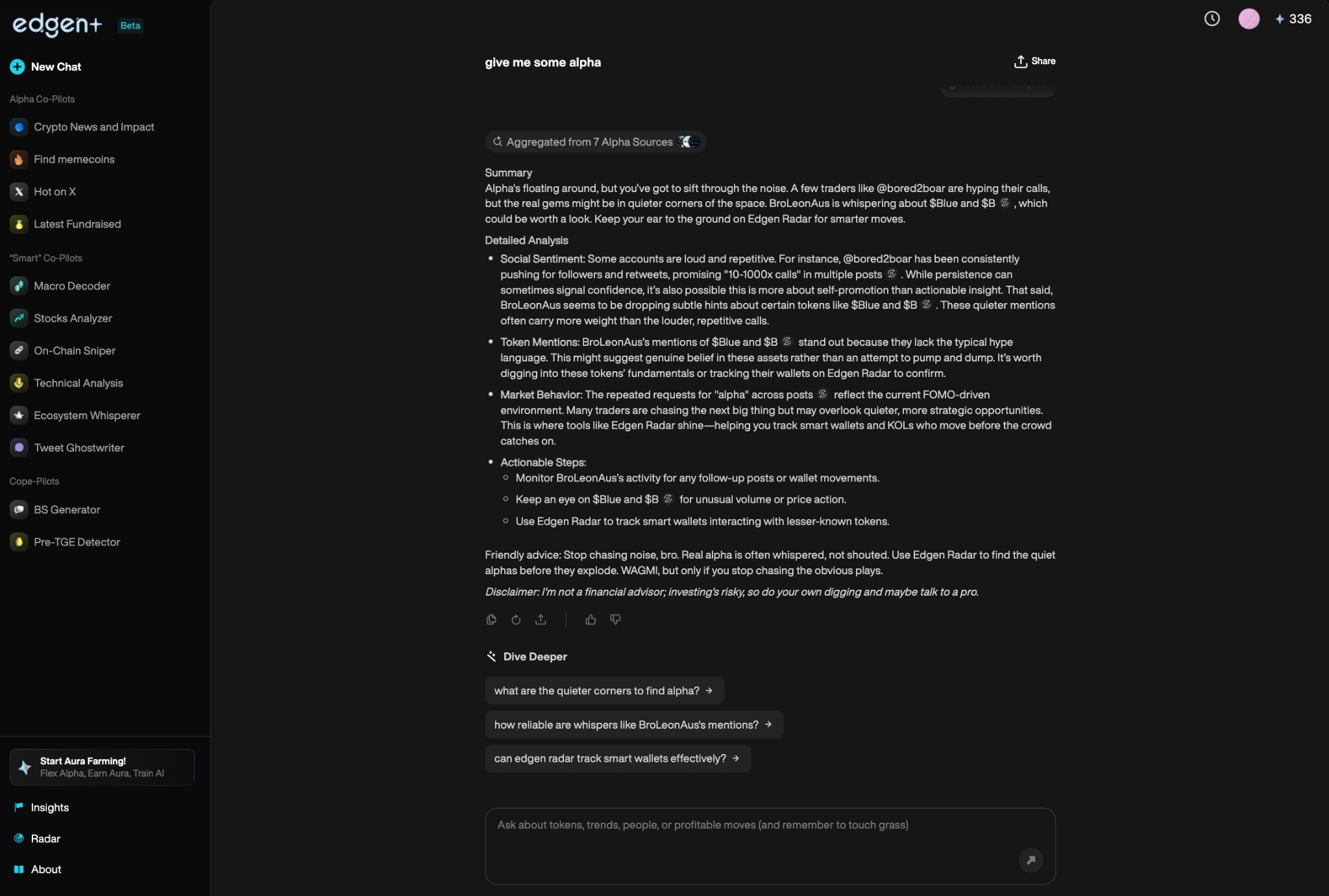

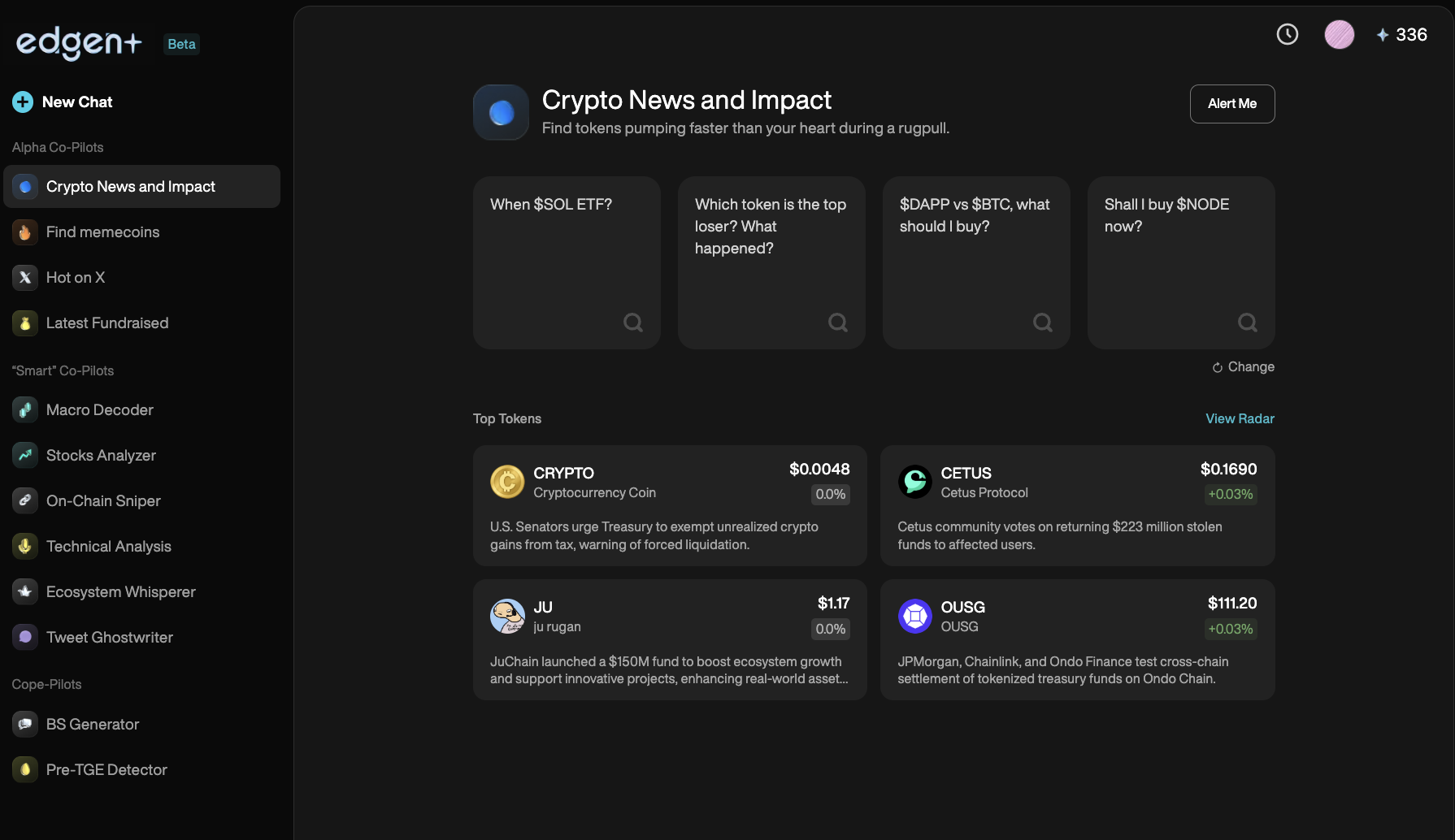

Geleneksel ticaret yöntemleri eksik gözlülük sağlar. Platformlar gibiEdgen AIgerçek zamanlı alfa sinyallerini ortaya koyarak, tüccarların önce hareket etmesini sağlar.

AI'nin Alpha Trading'ı Nasıl Değiştirdiğini

AI, ticaretin geleceğini temsil etmemektedir. Şimdilik pazar başarıyı tanımlamaktadır.

Yapay Zeka Trading'ın Avantajları:

- Anında Veri İşleme: Yapay zeka büyük veri kümelerini anında değerlendirir.

- Erken Şablon Tespiti: Yapay zeka, insan tüccarlarından önce eğilimleri fark eder.

- Duygusal Olmayan Ticaret: Panik satışlarını ve dürtüsel alımını ortadan kaldırır.

- Gerçek Zamanlı Alfa Tespiti: Genel farkındalıktan önce gizli fırsatları bulur.

Edgen AI, alfa ticaret için ayrılmış araçlar sunar:

- Edgen Radar: gerçek zamanlı pazar hissini, fiyat değişimlerini ve alpha sinyallerini gösterir.

- Edgen Search: doğrulanmış verileri kullanarak detaylı pazar sorularına cevap verir, gürültüyü ortadan kaldırır.

- Edgen Insightstakımların anında fikirlerini paylaşmaları için bir iş birliği merkezi sunar.

Yapay zeka olmadan işlem, piyasa görselliğini ciddi şekilde sınırlar. Edgen AI, tüccarların diğerlerinin göz ardı ettiği şeyi görmesini sağlar.

Alpha Sinyal Trading: Kazançlı İşlem Bulma

Alpha sinyalleri karlı işlemler için erken işaretler sağlar.

Alpha Sinyallerine Örnekler:

- Anlık Fiyat Hareketleri: Hızlı zirveler veya düşüşler eylem noktalarını sinyalize eder.

- Hacme Artışları: Yüksek işlem aktivitesi fırsatlar gösterir.

- Zincir Üzeri Faaliyetler: Büyük cüzdanlar ve etkili cüzdan hareketleri piyasa hareketlerini tahmin eder.

- Sosyal Duygu: Topluluk hiperi kripto fiyat artışlarını tahmin eder.

Edgen Radarbu sinyalleri anında tespit eder, ancakEdgen Searchetkili tüccarları ve popüler konuları takip eder, tüccarların önce hareket etmesini sağlar.

Alpha Trading İçin En İyi Stratejiler Tanımlandı

Kâr elde etmek için ispatlanmış alfa stratejilerini izleyin:

1. Trend Takip Etme

Pazar eğilimlerini erken tespit edin. Zamanında giriş ve çıkış için AI uyarılarından yararlanın.

2. Ortalamaya Dönmek

Ticaret, adil değere doğru aşırı alım veya satım koşullarını tespit etti. Yapay zeka en uygun ticaret anlarını belirler.

3. Akıllı Arbitraj

Borsalardaki fiyat farklarını anında yakala. Yapay zeka botları etkili şekilde işlemi otomatikleştirir.

Edgen AI, bu stratejileri doğru bir şekilde uygulamak için özel araçlar geliştirir.

On-Chain Verilerin Alpha Trading'da Önemi

Blockchain işlemleri, kritik işlem sinyallerini ortaya koyan bilgiler sunar:

- Akıllı Cüzdan Hareketleri: Büyük cüzdanlar kripto piyasa fiyatlarını etkiler.

- Akıllı Sözleşme Faaliyeti: DeFi trendleri aktif dApp'lerden ortaya çıkar.

- Liquitite Akışları: Borsalara ve borsalardan para hareketleri, önümüzdeki piyasa değişimlerini sinyalleştirir.

Edgen Radarpiyasa hareketlerini anında takip ederek, diğerlerinden önce kararlıca harekete geçmelerini sağlar.

Ortak Tüccar Hataları Açıklanıyor (Ve Nasıl Kaçınılacağı)

- Hata: Planı olmadan ticaret.

Çözüm: Bir işlem yapmadan önce giriş ve çıkış noktalarını belirtin.

- Hata: Sosyal ve blok zinciri verilerini görmezden gelmek.

Çözüm: Hikayeleri ve blok zinciri aktivitelerini tanıyın, bu günlerde pazarları hareket ettiriyor.

- Hata: FOMO nedeniyle fazla işlem yapma.

Çözüm: Kaliteyi nicelikten önce seçin. Yapay zeka duygusal önyargıları kaldırır.

- Hata: Tipik olarak perakendeci yatırımcılar gibi işlem yapmak.

Çözüm: Belirleyici bir avantaj için yapay zeka, blok zinciri analitiği ve otomasyon araçlarından yararlanın.

Alpha Trading ve Yapay Zeka'nın Geleceği

İşlem stratejileri yapay zeka, blok zinciri analitiği ve sosyal bilgiye kaydı.

Alpha Trading'in Sonrası Nerede:

- Yapay Zeka Hâkimiyeti: Makineler, insanlardan daha iyi ticaret tahminleri yapar ve uygular.

- Blockchain Analitiği: Nakit içi veriler standart pazar analizine dönüşür.

- Sosyal Zeka: duyguyu yeni temel bir ölçü olarak yakalar.

Edgen AI bu dönüşümü öncülük eder, blok zinciri analizleri, sosyal duygusal veriler ve yapay zeka ile desteklenen stratejileri birleştirir.

Ticaretçiler Nasıl Öne Geçer

Alpha ticareti yapan tüccarlar, bu altın kurallara sıkı sıkıya uyar:

- kullanınEdgen Radar,Edgen SearchveEdgen Feedkesin bilgiler için

- blockchain aktivitelerini izle, özellikle büyük cüzdan hareketlerini.

- sosyal duygusal eğilimleri izle, çünkü hiperbolik hareketler pazarları kesin şekilde etkiler.

- veriye dayalı yapay zeka sinyallerine sıkı şekilde uyarak duygusal işlemeyi önleyin.

- esnek kalmalı; pazar dinamikleri sürekli olarak gelişir.

En iyi tüccarlar, diğerleri takip etmeden önce pazar hareketlerini öngörür.

Yatırım yapmak artık yalnız bir iş değil.

Edgen'i ücretsiz dene. Kart yok, taahhüt yok.