Kripto'da Alpha Trading: Yapay Zeka Gizli Piyasa Sinyallerini Nasıl Açığa Çıkarır

Kripto Pazarları Hız ve Kesinliği Ödüllendirir

Kripto işlemi hızlı ilerler. Kazançlı işlemler, pazar eğilimlerini net ve erken fark etmeye dayanır. İnsan tüccarları, sınırlı analitik hız ve kapsam nedeniyle kritik sinyalleri sıkça göz ardı eder.

Yapay zeka, diğerlerinin fark etmeden önce gizli pazar hareketlerini ve sinyallerini anında belirler.

Bu, "alpha" ticaretini tanımlar: pazar fırsatlarını önce net bir şekilde görmek ve rakiplerinden önce işlem yapmak.Edgen AIyeni bu standartı belirler, işlemcileri eylem için uygun, zamanında bilgilerle donatır.

AI olmadan işlem yapmak yatırımcıları geride bırakır. Neden AI'nın kripto işlemelerinin geleceği olduğunu ve Edgen AI'nın bugün bunu erişilebilir hale getirdiğini burada bulabilirsiniz.

Kripto'da Alpha Trading'i Anlamak

Alpha ticareti, ana akıma yetişmeden önce karlı fırsatlar hakkında net ve erken bilgiler elde etmeyi ifade eder. Kripto pazarları yüksek volatiliteye sahip olmaya devam etmektedir ve 24 saat boyunca işlem görmektedir, bu da sürekli ve kesin izleme gerektirmektedir.

AI, neticesiz, anlık analiz sunar:

- Zincir Üzeri Veriler:Blok zinciri işlemlerini anında izleme.

- Pazar Eğilimleri:Kazançlı desenleri yaygın olarak fark edilmeden önce tanımlamak.

- Sosyal Duygusal:X (eski adı Twitter) verilerini, Telegram'i, haber kaynaklarını ve popüler konuları analiz etmek.

Geleneksel analiz araçlarından farklı olarak, Edgen AI tarihi verilerin ötesine geçerek mevcut piyasa hissini net bir şekilde ortaya koyar:

- X gibi platformlarda etkili Ana Fikir Liderlerini (KOL'ları) izleme.

- Önemli akıllı cüzdan işlemleri izleniyor.

- Analiz ederek "Pumpamentals" , kripto fiyatlarını hareketlendiren toplumsal itici güç.

Alpha Trading'in Daha da Önem Kazandığı Nedenleri

Web3'te geleneksel finansal metrikler eksik fikirler sunar. Modern kripto pazarları, gerçek zamanlı olarak görülebilen sosyal hissiyat ve blok zinciri aktivitelerine dayanır.

- Akıllı Alım Satımlar:Akıllı para hızlıca hareket eder. Yapay zeka onların toplu işlemlerini anında fark eder.

- Perakende Tüccarı Güveni:Sosyal eğilimler hızlıca ortaya çıkar. Yapay zeka, viral momentum başlamadan önce bu eğilimleri tanıır ve bunlardan yararlanır.

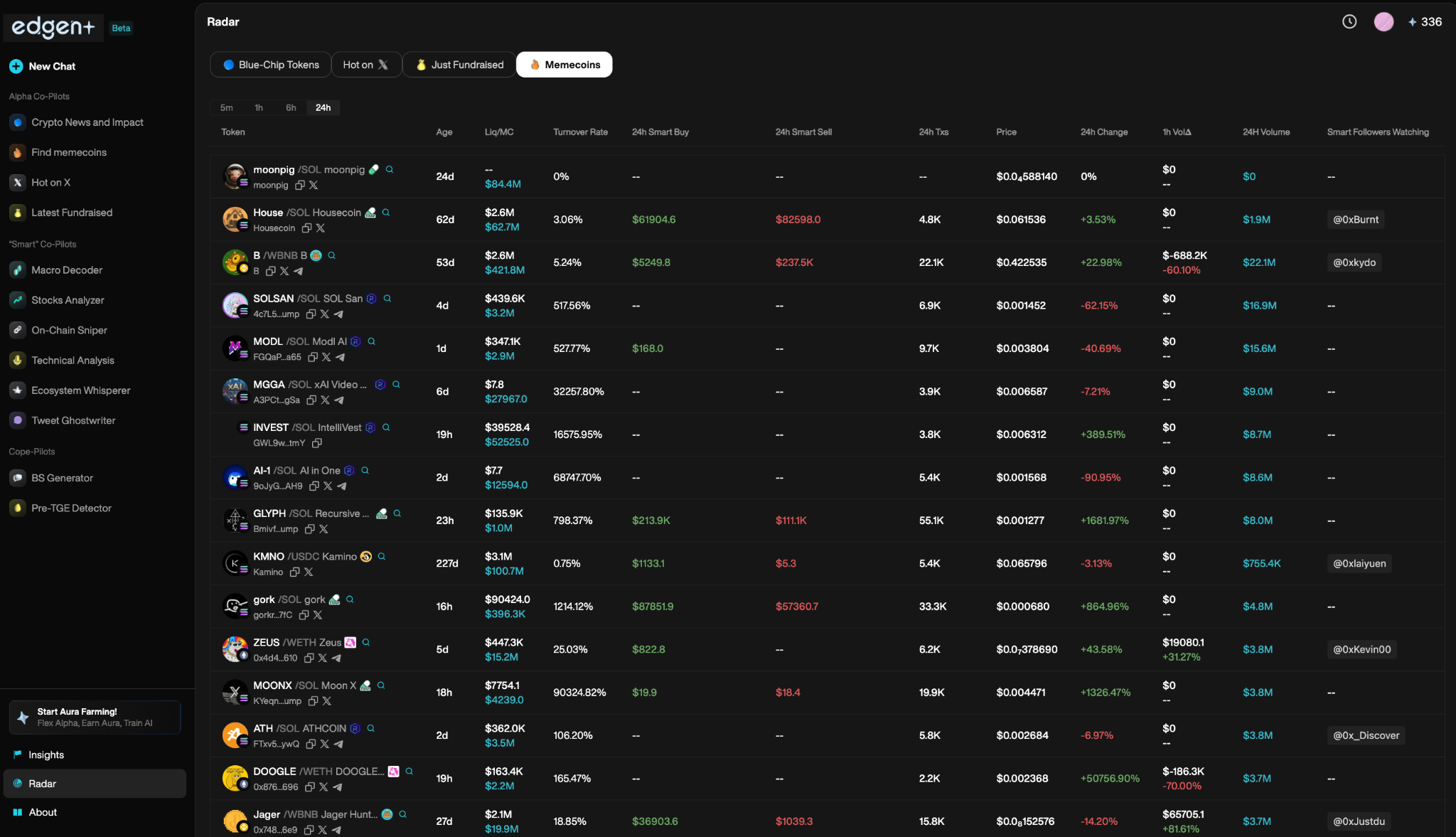

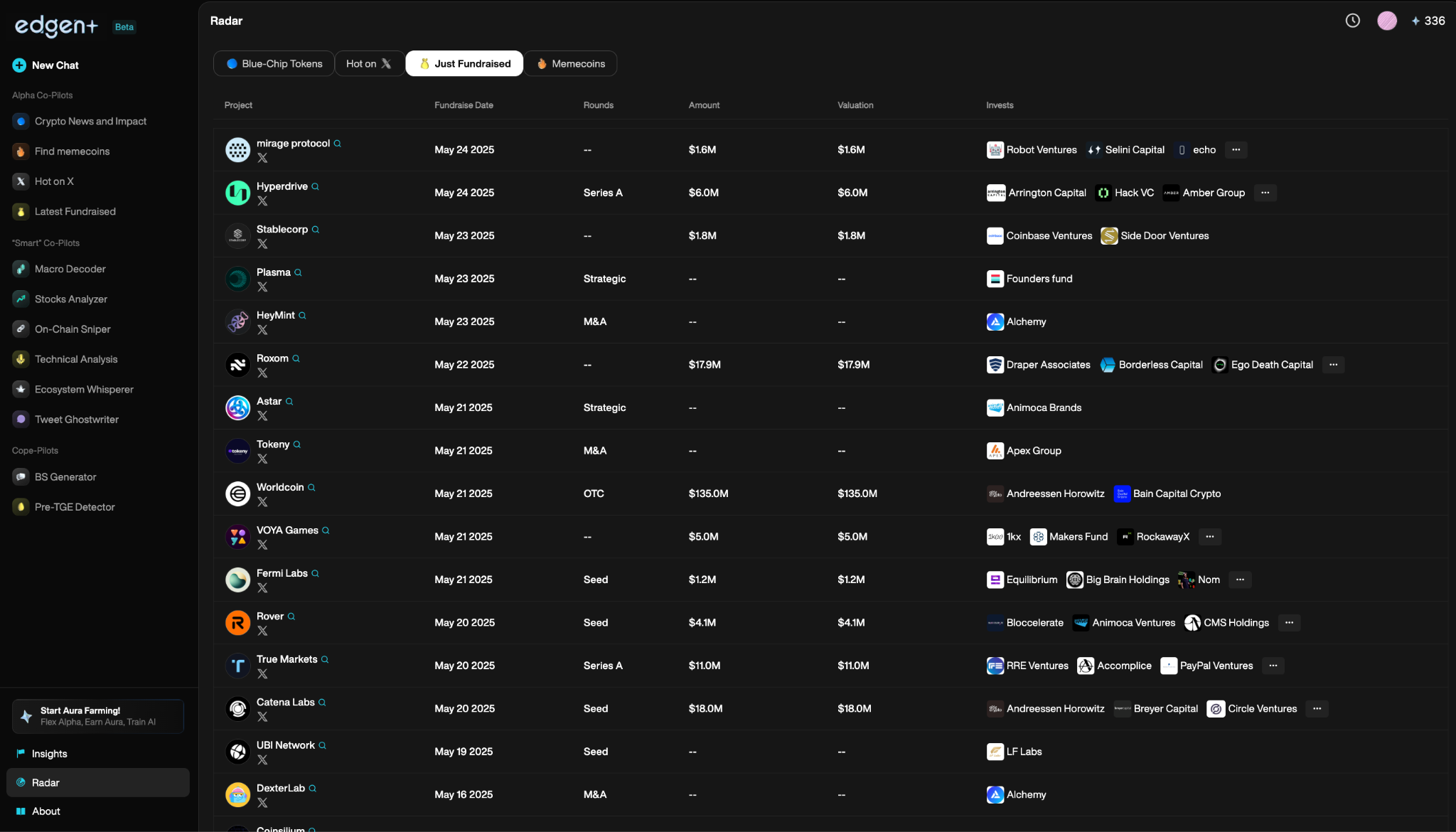

Edgen RadarveEdgen Searchtakipçilerin bu kritik piyasa değişimlerini anında fark etmelerini sağlayın.

Yapay Zeka Gizli Piyasa Sinyallerini Net Bir Şekilde Ortaya Çıkarır

Yapay zeka, kripto ticaretini devrimleştirir, milyonlarca veri noktasını anında işler ve insan tüccarlarının göz ardı ettiği ince sinyalleri yakalar.

Gerçek Zamanlı Yapay Zeka Piyasa Sinyalleri

Edgen AI, analiz ederek anında net ve uygulanabilir işlem sinyalleri üretir:

- Fiyat Hareketleri:Tarihî kalıplar, karlı pozisyonları göstermektedir.

- İşlem Hacmi Değişimleri:Piyasa aktivitesindeki anomali zirvelerini anında tespit edin.

- Sosyal Tren Dinamikleri:Topluluk katılımı ve hırsızlığı ölçerek fiyat hareketlerini önceden tahmin etmek.

Edgen Radardoğru işlem eylemleri için sosyal ve teknik pazar ortamını net bir şekilde görselleştirir.

2. Anlık Duygu Analizi

AI, X ve haber kaynaklarından verileri sürekli olarak analiz eder ve fiyat hareketlerini etkilemeden önce pazar hissini okur.

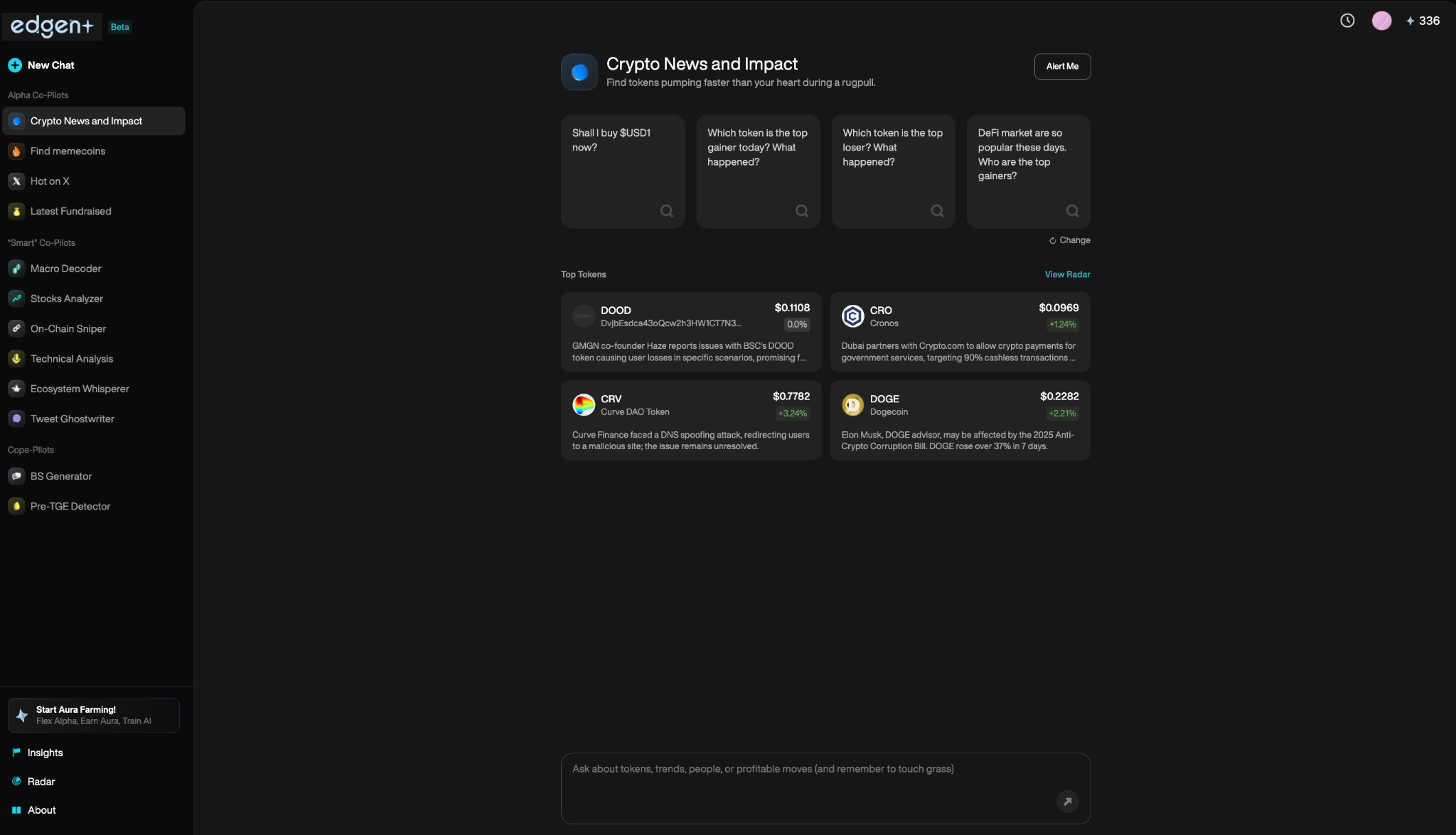

Ticaretçiler kullanırEdgen Searchgerçek zamanlı sorular sorma ve veriye dayalı anlık yanıtlar alma, açıkça.

3. Kesintisiz Piyasa Verisi İzleme

Piyasalar sürekli çalışır. Yapay zeka kesintisiz takip eder:

- Balina İşlemleri: Etkili cüzdan aktivitelerinin anlık izlenmesi.

- Sosyal Sesi: Toplulukla sürülen pompaların ve duygusal değişimlerin erken tespiti.

- Hacim Değişiklikleri: Piyasa likiditesinde kritik değişimler için anında uyarılar.

Edgen AI tüccarları, anlık, bilinçli işlem kararlarını açıkça sağlayarak gerçek zamanlı uyarılar alır.

Yapay Zekânın Ticaret Doğruluğu ve Kesinliği Üzerine Etkisi

Kârlı kripto işlemesi, kesin ve duygusuz analiz gerektirir. Yapay zeka şunları yaparak netlikle doğruluğu sağlar:

- Duygusal Kararları Kaldırma: Yapay zeka kararlarını nesnel duygular yerine verilere dayanarak kesin şekilde alır.

- Yapay Zeka Sinyallerini Filtreleme: Botlar tarafından tetiklenen sahte pompalardan açıkça tanıma ve kaçınma.

- Piyasa Değişimlerini Tahmin Etme: Yaygın piyasa tepkilerinden önce ortaya çıkan duygusal trendleri belirleme.

İlgili olarakInternational Monetary Fund,AI, küresel finans pazarlarını daha verimli hale getirirken aynı zamanda veriye dayalı volatiliteye daha duyarlı hale getiriyor.

Edgen AI, blok zinciri analitiği, sosyal veriler ve net AI görüşlerini birleştirir ve tüccarların sadece gerçek sinyallerle hareket etmesini sağlar.

Gelecek: Yapay Zeka, Alpha Trading'i Nasıl Şekillendirecek

AI'nin kripto para üzerindeki rolü sürekli gelişmeye devam ediyor ve işlem stratejilerine net avantajlar sağlıyor:

AI'ye Dayalı Portföy Optimizasyonu

Ticaretçiler, portföyleri otomatik olarak yönetmek için yapay zekayı artan ölçüde kullanacak ve böylece uzun vadeli getirileri açıkça optimize edecek.

2. İleri Blok Zinciri Analizi

AI, daha fazla hassasiyetle akıllı sözleşmelerin ve büyük cüzdanların davranışlarını anlama konusunda daha derin görsel sunumlar sağlayacaktır. Edgen Radar, etkili cüzdanların ve bunların piyasa etkilerinin net izlenmesini zaten sunmaktadır.

3. İyileştirilmiş Tahmin Pazar Analitikleri

Yapay zeka tahmini daha net ve doğru hale gelecek, tüccarlar için haftalar veya aylar önceden ticaret planlamasını güvenle mümkün kılacak.

4. İnceleştirilmiş Piyasa Hissi Takibi

Sosyal duygusal analiz devam edecek ve piyasa coşkusunun artmaya başladığında tüccarları anında uyarmaya devam edecek. Edgen AI, bu evrimi öncü olarak sürdürüyor ve yapay zeka, blok zinciri verileri ve sosyal bilgiyi sorunsuz bir şekilde entegre ediyor.

Yapay Zeka, Son Kripto Trading Avantajını Tanımlar

Yapay zeka kripto pazarlarını yeniden şekillendirdi. Yapay zeka alpha sinyallerini net bir şekilde tanımlar, işlemleri kesin şekilde otomatikleştirir ve karar verme doğruluğunu önemli ölçüde artırır.

Edgen AI, blok zinciri analitiği, anlık pazar bilgisi ve gerçek zamanlı sosyal görüşleri bir bütün halinde ticaret çözümüne entegre ederek önde durmaya devam ediyor.

Bugün yapay zeka kullanan kripto tüccarları, yarınki pazar düzenini açıkça belirleyecek.

Açıkça önde kal. Yapay zekâya dayalı ticarete açık ol.Edgen AI

Yatırım yapmak artık yalnız bir iş değil.

Edgen'i ücretsiz dene. Kart yok, taahhüt yok.