Memecoins'tan Hisse Senetlerine: Yapay Zeka Trading'in Küresel Piyasaları Nasıl Değiştirdiğine Dair

AI Oyunu Yeniden Şekillendiriyor

Finansal piyasalar değişti. Frommemecoinsstoklara, işlemeler grafikler ve manuel analizin ötesine geçti. Ve geleneksel stratejiler yetersiz kalıyor, tüccarları geçmişte kıstırmaya devam ediyor.

Yapay zekâya dayalı araçlar, liderliğindeEdgen AIPiyasa hissini, sosyal ivmeyi ve zincir içi hareketleri anında çöz. Bu avantaj, önceki tüm zamanlarda olduğundan daha keskin, daha akıllı ve daha hızlı ticaret etmenizi sağlar.

Neden Yapay Zeka Trading Piyasayı Şimdiki Zaman Kaptırdı

Yapay zeka, pazar eğilimlerini okumada insan trader'ları geçer. Milyarlarca veri noktasını anında işler, pazar değişimlerini, etkileyici sinyalleri ve gizli hikayeleri eşsiz hızla yakalar.

Yapay zeka destekli işlem:

- Öngörücü analitik:Başkaları fark etmeden pazar hikayelerini görüyorum.

- Algoritmik ticaret:Mikrosaniyelerde işlem yapmak.

- Duygu analizi:Twitter havalisini ve etkileyici eğilimlerini anında yakalayın.

- İleri risk yönetimi:Bunları vurmadan önce aşağı yönlü sinyalleri tespit edin.

Sonuç: Yapay zeka pazarı öngörür. İnsanlar tepki verir; yapay zeka tahmin eder.

Edge: Odada Okuyabilen Yapay Zeka

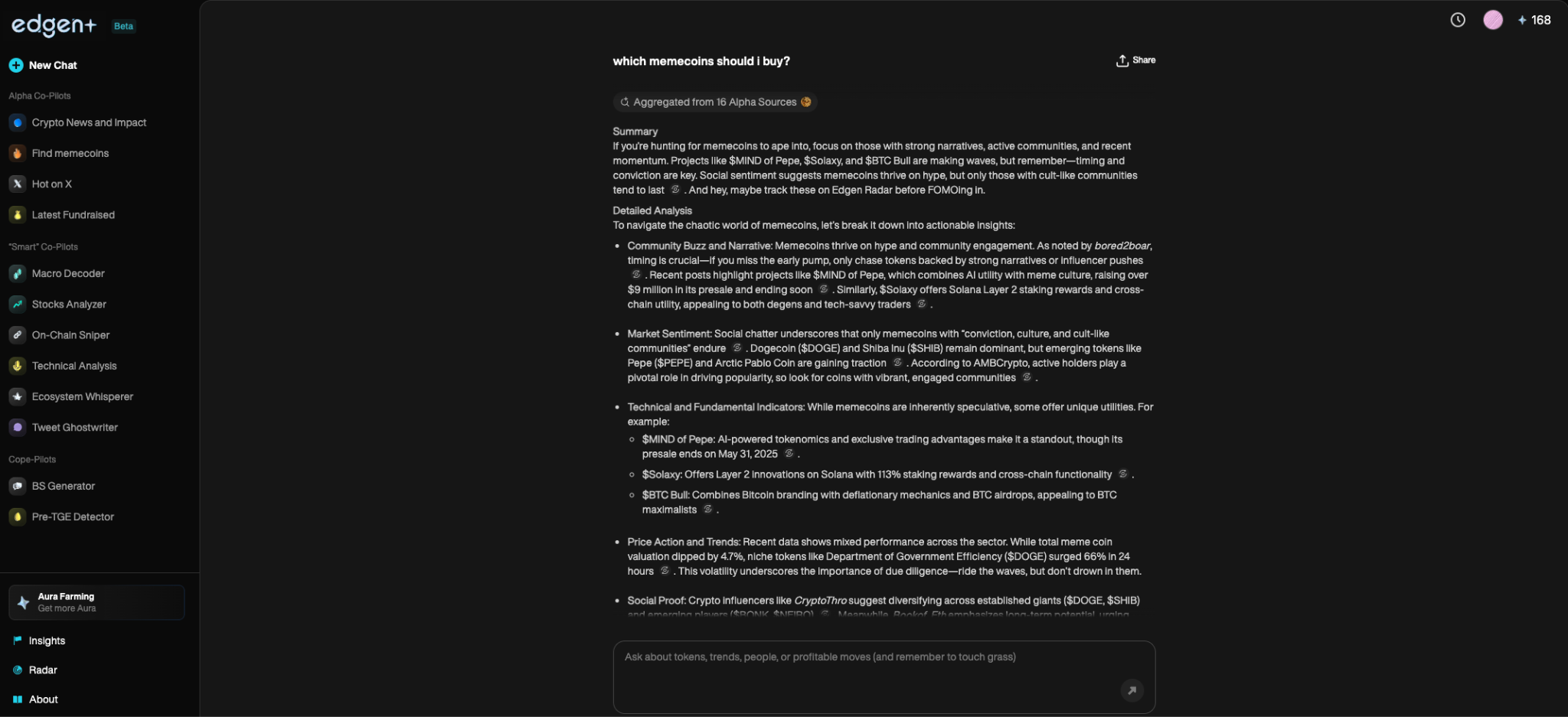

Edgen AI, gerçek zamanlı blok zinciri verileri ve sosyal "pompa temelleri"ve derin pazar bilgisiyi eylemli görüşlere dönüştürür. Ana fikir liderlerini (KOL'ları) tespit eder, akıllı cüzdanları izler ve kalabalıktan önce alpha sağlar.

Temel Özellikler:

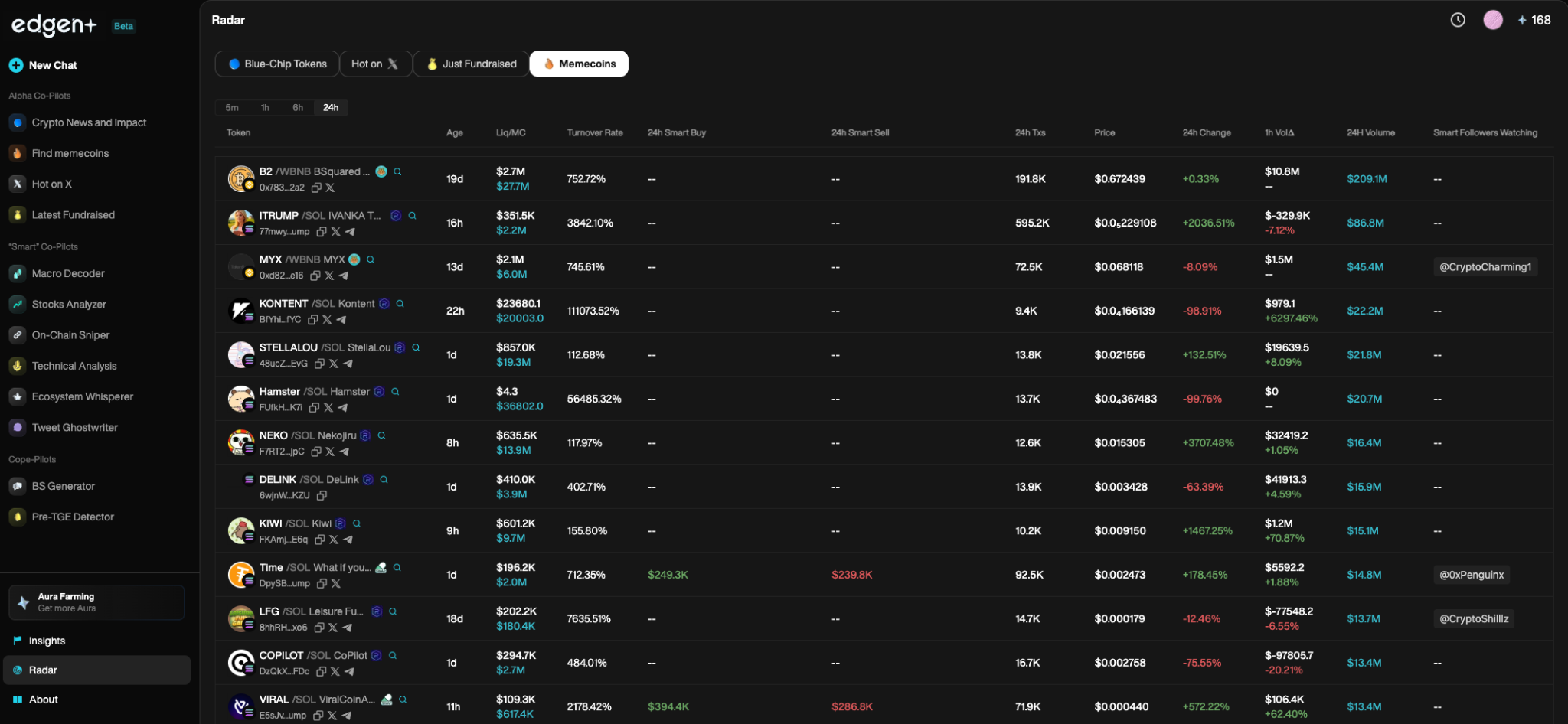

- Anlık Varlık İzleme:Edgen Radarfiyat hareketini sosyal duyguya göre takip eder.

- Yapay Zeka Destekli Arama:Edgen Searchtoplanmış verilerden anlık pazar bilgisi sunar.

- Topluluk Yönlü Analiz:Edgen Feedcanlı, topluluk kaynaklı alfa sinyalleri sağlar.

Edgen AI, piyasa nabzını okur, her işlemi hareket ettiren toplu düşünceyi.

Memekoinlarve Yapay Zeka: Doğal Bir Uyum

MemekoinlarGeleneksel değerlemelerin ötesinde işlem yapar. Fiyat hareketleri, yankı, topluluk katılımı ve viral ivme takip eder.

AI bu ortamda gelişir. Edgen AI, bunu işlemek için benzersiz bir konumda bulunmaktadır.memecoinsgerçek zamanlı duygusal takip kullanarak hızlı pazar değişimlerini yakalamak için.

Edgen AI yüksek lisansmemecoinalış-verişi yapan:

- Duygu Analizi:Twitter/X'ı anında pompa sinyalleri için tarama.

- Zincir Üzeri Gözlemler:Köpek balina cüzdanlarını ve etkileyici aktivitelerini canlı takip edin.

- Alpha Tespiti:Fiyat patlamalarından önce gizli göstergeleri bulmak.

Memekoinlarortalama volatilite ve dayanılmaz rekabet. Yapay zeka olmadan, tüccarlar hiçbir şansı yok.

Yapay Zeka ve Modern Yatırım Stratejileri

Piyasalar temellere uzanmaya devam etti. Sosyal duygusal durum, öngörücü analiz ve blok zinciri işlemleri modern stratejileri tanımlar.

Daha akıllı yatırım da AI'nın rolü:

- Alpha Keşfi:Piyasa hareket etmeden önce sinyalleri bulmak.

- Yapay zeka yönetilen portföyler:Yüksek performanslı risk yönetimi sağlayan yapay zeka destekli fonlar.

- Blockchain Entegrasyonu:Akıllı para izlemek için cüzdan hareketlerini izleme.

Edgen Radar yeni bir standart belirler, yalnızda izole edilmiş metrikler değil, tüm pazar ekosistemlerini yorumlar.

Trading'in 3-Cisim Problemini Çözmek

Çoğu tüccar kısmen kör olarak işlem yapar:

- Bazıları zincir üzerinde veri izler ama sosyal hikayeleri kaçırmakta.

- Başkaları hiperbolik hareketleri takip ederken likidite hareketlerini göz ardı eder.

- Çok sayıda kişi, piyasa hareketlerini etkileyen hikayeleri görmezden gelerek teknik grafiklere sadık kalır.

Edgen AI, bu karmaşıklığı üç boyutu entegre ederek çözer:

- Zincir Üstü Analitik: Gerçek zamanlı akıllı para izleme.

- Sosyal Duygusal: Hype döngülerini ve toplulukla ilerleyen hareketleri yakalamak.

- Yapay Zeka ile Sürdürme: Başkaları fırsatı göremezken stratejik olarak işlem yapın.

Bu birleşik yaklaşım, Edgen tüccarlar için "PvP", rekabetçi, sıfır toplamlı piyasalarda belirleyici bir avantaj sağlar.

Yapay Zekâ'nın Finansal Piyasalardaki Geleceği

AI, ticaretin geleceğini besler. Bu gerçeği göz ardı eden tüccarlar kalıcı olarak geride kalmaya mahkumdur.

Bir sonraki adım nedir:

- Kendini Öğrenen Yapay Zeka Botları: Çıkan pazar eğilimlerine anında uyum sağlayan yapay zeka.

- Otomatik Alfa Keşfi: İnsanların farkına varmadan önce gizli fırsatları belirleme.

- İleri Sosyal Zeka: Etkileyici odaklı anlatıları anında yorumlama.

- Tamamen Yapay Zeka (AI) Tabanlı Altyapı:Edgen AIbütünleşik bir yatırım platformuna dönüşüyor.

Araştırma from theUniversity of Michigan highlights how AI and algorithmic systems are transforming modern financial markets, Edgen AI gibi platformların izlediği yöne dayanmak.

Edgen AI zaten bu gerçeği inşa ediyor, yapay zekâyı temel bir pazar gücü haline getiriyor.

Yapay Zeka Piyasa Devrimi Zaten Burada

Yapay zeka küresel finansal pazarları yeniden şekillendirdi:memecoinshisse senedi, kripto, döviz. Yüksek frekanslı ticaretten alfa tespitine kadar, yapay zeka ticaretin başarısını belirler.

Edgen AI bu devrimi öncülük eder ve tüccarlar için sert pazarlarda stratejik bir avantaj sunar. Yapay zekâ olmadan yarışan tüccarlar, daha hızlı hareket eden, daha net düşünen ve eksiksiz şekilde uygulayan rakiplerle karşı karşıya kalır.

Piyasalar gelişti. İnsanlar arası ticaret ortadan kalktı. Bugün AI ile AI'ya karşı.

Hazır ol veya olma,Edgen AI Era geldi!

Yatırım yapmak artık yalnız bir iş değil.

Edgen'i ücretsiz dene. Kart yok, taahhüt yok.