AI'nin Kripto Trading'de Risk Azaltma ve Doğruluk Arttırma Rolü

Kripto işlemecilik, yapay zeka destekli analizler, piyasa hissi ve kesin blok zinciri görüşleri, kimin başarılı olacağını ve kimin başarısız olacağını belirleyen, kanunsuz, 24/7 bir savaştır.

- Geleneksel işlem yöntemleri? Eski moda.

- İçsel hissine göre hareket etmek mi? Daha fazlası.

- Sadece manuel analiz bağımlısı mısınız? Kazanmak için çok yavaştır.

Bu nedenle yapay zeka devreye girmektedir. Platformlar gibiEdgen AIzamanında zincir içi analitikler, otomatik işlem yürütme ve gelişmiş sosyal duygusal takibi birleştirmek, tüccarlar için eşsiz bir pazar avantajı sunmak.

Kripto Trading'da Yapay Zeka: Geleneksel Yöntemler Neden Kayboluyor

Kripto para piyasaları geleneksel finans gibi çalışmaz. Hisse senetleri şirket raporlarına veya kazançlara veya makro haberlere predictable şekilde tepki verir; kripto ise, etkileyicilerin, topluluk havalı havasının ve akıllı cüzdan aktivitesinin ritmine uygun hareket eder.

Yapay zekaya yeniyseniz veya nasıl çalıştığını daha iyi anlamak istiyorsanız, bu şeyi kontrol edinintro to artificial intelligence from AAAI.

Şimdi Ne Farklı?

- "Pumpamentals"Temel Bilgiler Üzerine:"Bugünkü Token'lar (memecoins, altcoin'ler ve hatta en iyi varlıklar bile genellikle sosyal yankı ve etkileyici eylemlere dayalı olarak sıçrayabilir veya çökülebilir.

- Yapay Zeka: Farkı Genişletiyor:İleri yapay zeka, zincir içi ve sosyal verilerin büyük miktarını anında analiz eder, herhangi bir insandan daha hızlı.

- İnsanlar Takip Edemiyor:Piyasalar milisaniyeler içinde değişir. Yapay zeka, manuel tüccarlar farkına varmadan işlem yapar.

Edgen AI Oyunu Nasıl Değiştiriyor:

- Gerçek Zamanlı Piyasa Okuması:Zincir üzerindeki sinyalleri ve sosyal duyguyu sürekli olarak izler.

- Sosyal Zeka:Etkileyici odaklı hikayeleri ve topluluk momentumunu izler.

- Anında Uygulama:İnsani tereddütlüğü ortadan kaldırır, anında kesin, veriye dayalı işlemler sunar.

Yapay zekâ olmadan ticaret? Kör edilmiş bir şekilde, kaçırılmış sinyaller ve ani pazar değişimlerine maruz kalıyorsun.

Kripto Risk Yönetimi'nde Yapay Zeka: Cesurca, Düşünceksizce Değil Ticaret Yapın

Kripto işlemesi bağlayıcı değildir. Bir duygusal işlem portföyünüzü yok edebilir. Yapay zeka, disiplinli risk yönetimi, duygusuz karar verme ve erken dolandırıcılık tespiti ile yatırımlarınızı korur.

Yapay Zeka Trading Risk'ini Nasıl Azaltır:

- Sahtecilik Tespiti:Sizi maruz kalmadan önce bayrak şüpheli token'ları ve kara piyasa faaliyetlerini tespit edin.

- Dinamik Risk Azaltma:Gerçek zamanlı piyasa volatilitüsüne göre maruziyeti otomatik olarak ayarlar.

- Pump-and-Dump Önleme:Fiyatlar çökmeye başlamadan önce pazar manipülasyonlarını tespit eder.

Neden Edgen AI Farklılık Yaratır

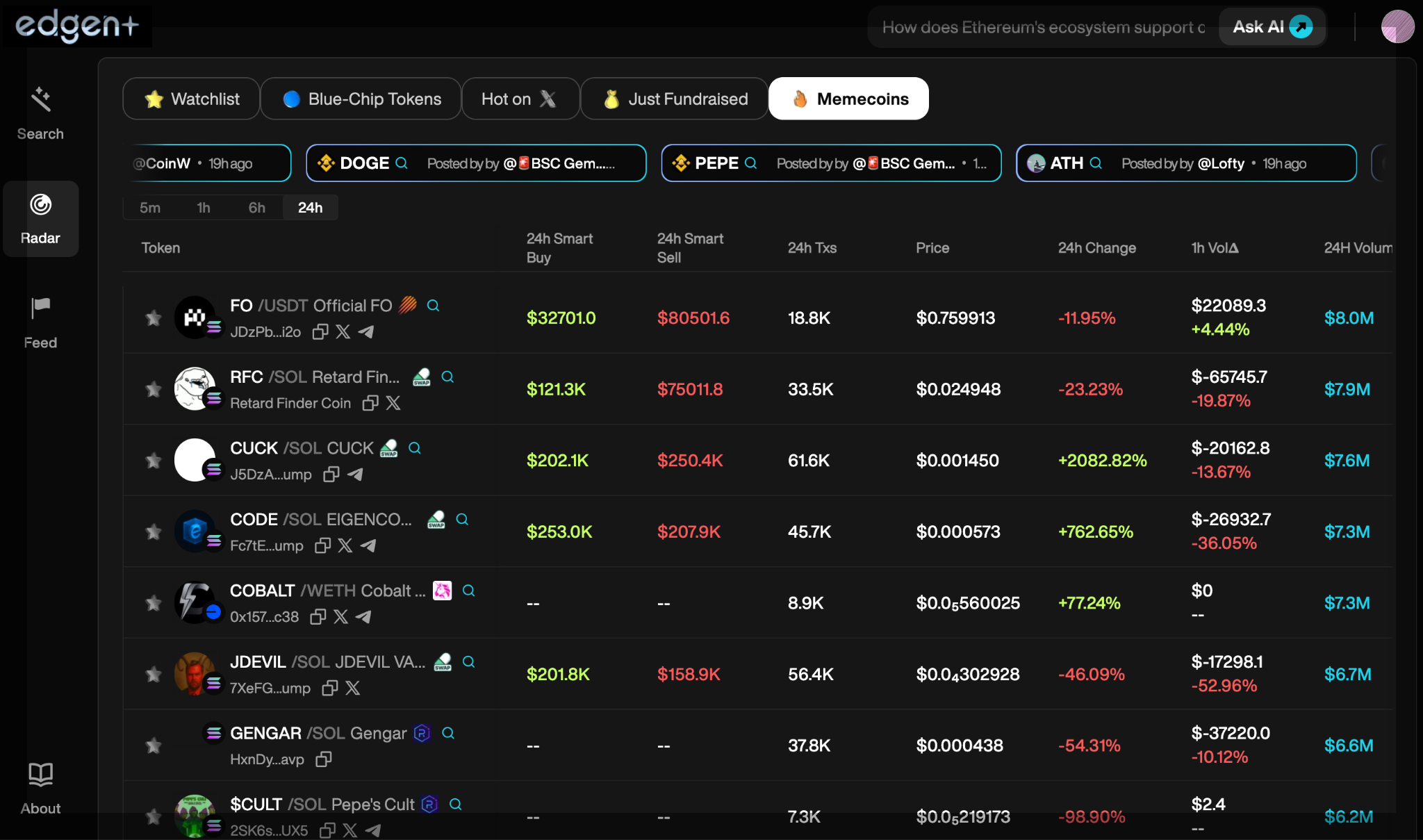

Temel analitik botlardan farklı olarak,Edgen Radarileri blok zinciri risk analizini kapsamlı sosyal duygusal görüşlerle birleştirir, sunar:

- Gerçek zamanlı akıllı cüzdan ve piyasa yapıcı izleme.

- Potansiyel pazar boşaltımları hakkında öngörücü uyarılar.

Yapay zeka ticareti daha akıllı hamleler, daha iyi risk kontrolü ve çok daha yüksek doğruluk anlama anlamına gelir.

Yapay Zeka Pazar Analizi: Olaylar Olmadan Önce Geleceği Tahmin Etme

Bilgisayarlı Zekâ'nın Öngörülü Pazar İhtisaslarını Nasıl Sunuyor:

- Fiyat Tahmini:Doğru kısa ve uzun vadeli pazar tahminleri.

- Sosyal Trend Analizi:İlk olarak, Twitter ve kripto topluluklarını takip ederek ortaya çıkan anlatıları izler.

- Akıllı Cüzdan İzleme:Piyasa hareketlerini öngörmek için etkili cüzdan aktivitesini izler.

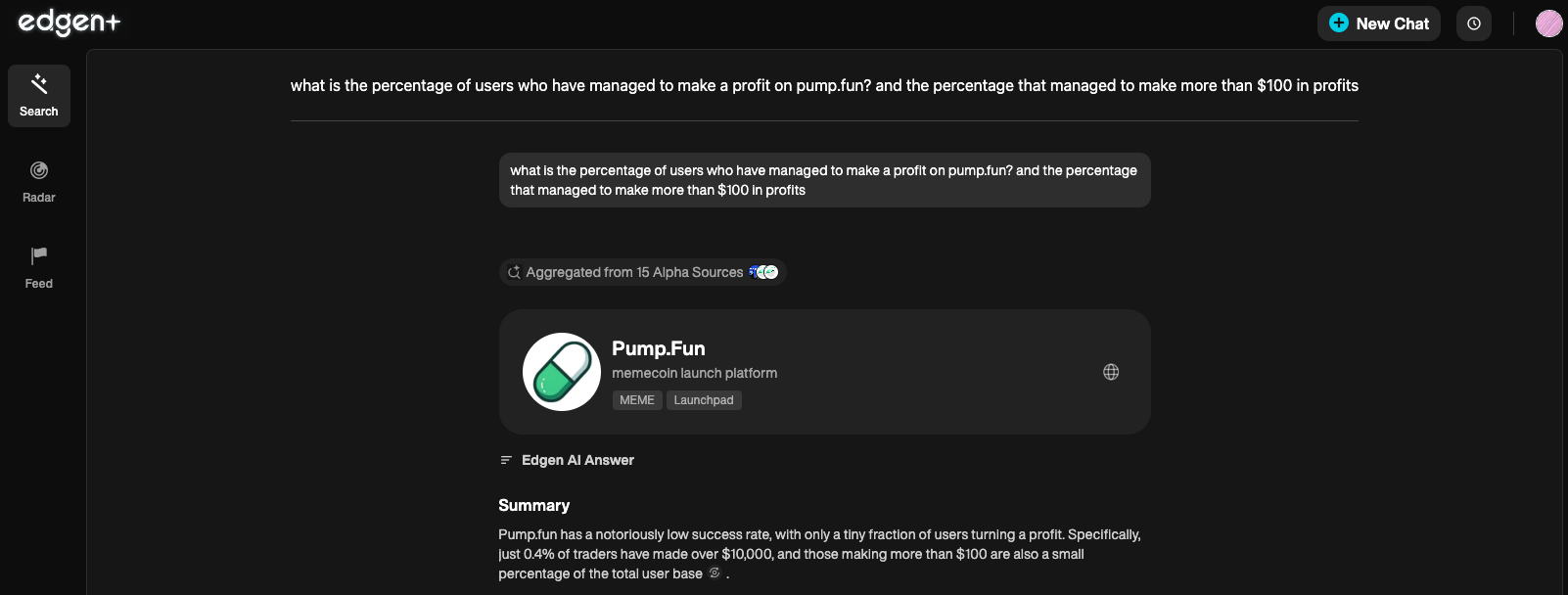

Edgen Arama Pazar Bilgi Sistemi:

- Piyasa sorularını AI onaylı görüşlerle anında yanıtla.

- Yanlış bilgi ve sahte havayı kesin.

- Piyasa hareketlerini şu anda neyin yönlendirdiğini tam olarak anlayın.

Çelişen görüşlerin arasında kaybolma. Yapay zeka anında, uygulanabilir netlik sunar.

AI'nin Kripto Ticaretindeki Geleceği: Geliş veya Geride Kalın

Yapay zeka hızlı bir şekilde gelişmeye devam ediyor. Bugün yapay zekayı entegre eden tüccarlar, yarınki kripto pazarlarını yönetecek ve tereddüt gösterenler ise eskiyenin eşiğine gelecek.

Yapay Zeka Güçlü Kripto Nedir?

- AI'ya Dayalı DeFi Trading:Daha güvenli, daha akıllı dağıtık finans yatırımları.

- İyileştirilmiş Pazar Tahminleri:Pazar eğilimlerini tahmin etmede eşsiz doğruluk.

- İleri Seviye Sahtecilik Tespiti:Kripto dolandırıcılığına karşı daha da akıllı koruma.

Edgen AIpazarında rekabet avantajınızı sürekli olarak geliştirirken kesinlikle en önde kalır.

Daha Akıllı Ticaret Yapın, Daha Az Zorlanın: Yapay Zeka Gereklidir

- AI artık zorunludur. Edgen AI pazar kör noktalarını kaldırır ve ticaret hassasiyetinizi artırır.

- Zincir içi analitikler, gerçek zamanlı AI sinyalleri ve sosyal duyguya dayalı takip, kripto işlemenin geleceği olarak öne çıkar. Edgen AI ile kripto savaşı alanında hakimiyet kuracaksınız.

Kripto hızlı hareket eder. Yapay zeka, ileride kalmak için sadece güvenilir yoldur.

Kripto Eğrisiyle Öne Çıkmak ve Daha Akıllı Ticaret Yapmak Hazır Mısınız?

Duygusal işlemler ve yavaş tepkilerin avantajını bozmasına izin vermeyin.

Gerçek zamanlı AI analizleri, sosyal duygusal takip ve zincir içindeki analitiklerle,Edgen AIgüvenle volatil piyasalarda egemen olmanıza yardımcı olur.

Yatırım yapmak artık yalnız bir iş değil.

Edgen'i ücretsiz dene. Kart yok, taahhüt yok.