AI'yi Kullanarak Edgen Radar ile Karlı Kripto İşlem Olanaklarını Belirleme

Kripto Trading'in Geleceği: Yapay Zeka Oyunu Nasıl Değiştiriyor

Kripto işlemeleri ışık hızında ilerler ve geleneksel yöntemler onlarla eşit ritimde ilerleyemez.

Giriş Yap AI: Piyasayı yenebileceğin en iyi arkadaşı. Şunlar gibi platformlar:Edgen Radarzaman kazanmak için yapay zeka kullanarak karlı kripto işlem fırsatlarını hızlıca tanımlayın, borsa verilerini, sosyal duyguyu ve yapay zeka ile desteklenen analizi tek bir akıllı arayüzde birleştirin.

Bu makale, yapay zeka (AI)'nin kripto işlem stratejilerini nasıl devrinde olduğunu ve özellikle nasıl... Edgen AItüm alım satım işlemlerini gerçek zamanlı Alpha sinyalleri, blockchain trendlerinden elde edilen eylem önerileri ve sosyal kripto analizleri ile güçlendirirpompa temelleri."

1. Yapay Zeka, Kripto Ticaret İçin Neden Gereklidir

Kripto aslauykular:fiyatlar anında değişir ve her bir hareketi manuel olarak takip etmek imkansızdır. Bu yüzden yapay zeka kullanmak tamamen oyunu değiştirici bir şeydir.

Yatırım Kararlarınızı Nasıl Geliştirir:

- AI-based sentiment analysis for crypto:Kripto Twitter (X) ve haber akışlarını anında tarar, popüler token'ları ve toplulukları belirlerduygu

- Real-Time On-Chain Monitoring:Token fiyatlarını etkilemeden önce leke balina işlemleri, likidite değişimleri ve akıllı cüzdan faaliyetlerini tespit edin.

- Crypto Alpha Signal powered by Edgen AI:İyileşme potansiyeli olan ve değeri düşük olan varlıkları belirler, diğerlerinin fark etmeden önce size işlem uyarıları gönderir.

Edgen, sadece kripto analitiği, yapay zeka ve sosyal medya görüşlerini benzersiz bir şekilde birleştirmekle kalmaz, aynı zamanda hiçbir kör nokta bırakmaz.

2. Kazançlı Kripto İşlemleri İçin Güçlü Yapay Zeka Stratejileri

Yapay zekanın gücü, büyük veri kümelerini hızlıca filtreleyebilme, kalıpları tanıma ve stratejileri kesin ve anında kurabilme yeteneğinde yatmaktadır; bu da insan kapasitesini çok aşmaktadır. İşte yapay zeka ile kripto ticaret performansınızı nasıl hızlandırabileceğiniz:

1. Duygu Analizi: Piyasa Hırsını Kullanmak

Kripto pazarlar genellikle havadan ve spekülasyondan etkilenir. Yapay zeka destekli duygusal analiz, şu şeyleri analiz ederek alıcı veya satıcı trendlerini tespit eder:

- Token bahsedildiTwitter (X) gibi platformlar üzerinden

- Etkinlik metrikleriakıllı hesaplar tarafından retweet'ler, yorumlar ve takip edilmeler gibi.

- İnfluencer duygusuana fikir liderlerinden (KOL'lar)

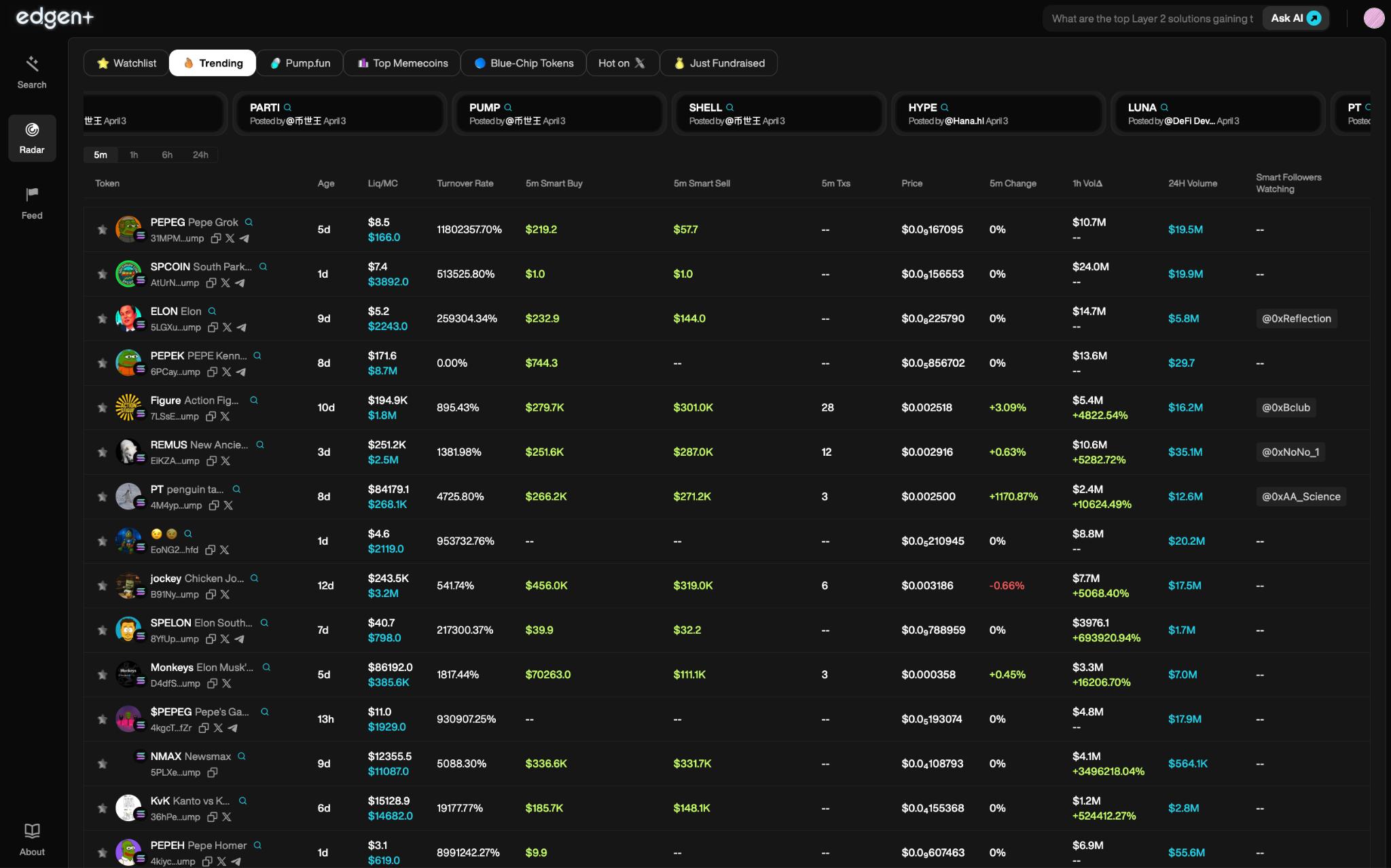

Edgen Radarsosyal takip kazanan token'ları anında işaretler, karlı hamleler için erken pozisyon almanı sağlar.

2. Zincir Üzeri Veri Görünüşleri: Akıllı Cüzdan Etkinliklerini Okuma

Edgen'den AI destekli blok zinciri analizleri, kritik pazar değişimlerini vurgulayarak tüccarlar için faydalıdır:

- Balina aktivitesi:Büyük akıllı cüzdan hareketleri genellikle önemli fiyat değişimlerini önceden gösterir.

- Liquidity Flow:Merkeziyete dayalı borsalar (CEX'ler) ve merkezsiz borsalar (DEX'ler) arasında token hareketlerini izleyin.

- Akıllı Cüzdan Sinyalleri:DeFi protokollerindeki faaliyetleri, staking davranışlarını ve token kullanım göstergelerini takip edin.

Edgen'in kapsamlı dashbordu, tahmin yapma gereğini ortadan kaldıran net, anlık blok zinciri göstergeleri sunar.

3. Teknik ve Temel Analiz: Tümleyici Yapay Zeka Güçlü Görünümü

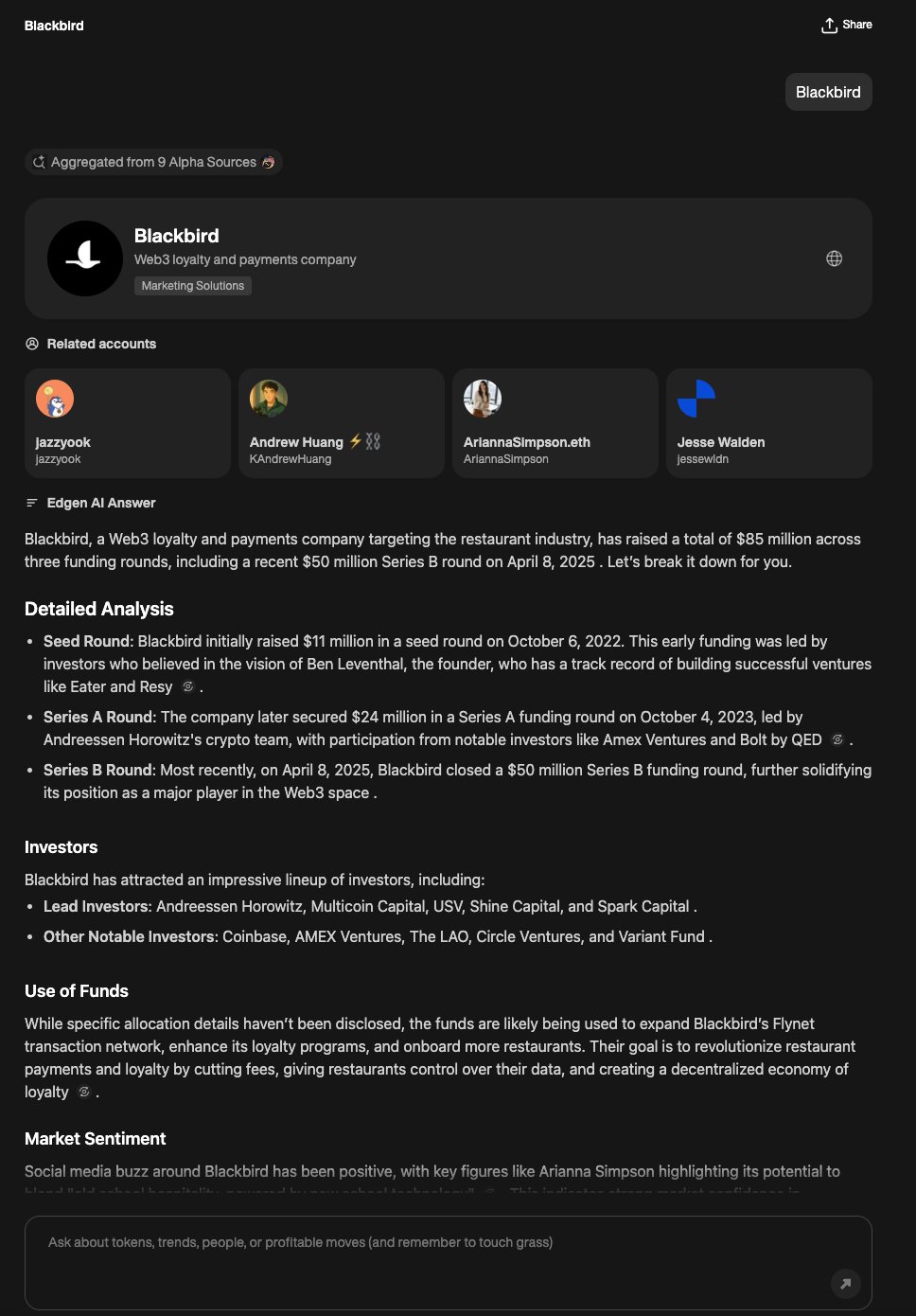

Teknik grafik kalıpları, zincir içi veriler ve sosyal duygusal metrikleri birleştiren, Edgen AI'nın akıllı algoritmaları, yüksek oranda uygulanabilir işlem fırsatlarını otomatik olarak ortaya çıkarır. Gürültülü, parçalı piyasa verilerini manuel olarak sıralamakla zaman kaybetmek yerine, tüccarlar bunlara güvenebilir. Edgen Search’s AI-powered crypto trading enginesaniyeler içinde hızlı, doğru ve veriye dayalı fikirler sunmak. Platformun LLM (Büyük Dil Modeli) teknolojisi, kullanıcıların "Hangi token'lar maymun ilgisini kazanıyor?" veya "Bugün hangi DeFi token'ları popüler?" gibi soruları yazmasına olanak tanıyarak anında ve detaylı cevaplar almasını sağlar. Bu, daha akıllıca işlemek için tasarlanmış bir yol—hız, ölçek ve kesinlik için.

3. Alpha Trading Açıklaması: Yapay Zeka Gizli Fırsatları Nasıl Bulur

Alpha Nedir?

Alpha, pazarın standartlarını düzenli olarak geçme anlamına gelir ve bunu, yaygın şekilde fark edilmeden önce dikkat çekmeyen ticaret fırsatlarını keşfetmek yoluyla yapar.

Edgen AI'nin Alpha Sinyallerini Nasıl Tanıdığı:

- Önemli akıllı cüzdan ve balina hareketlerini takip eder.

- Düşük risk, yüksek ödül olan ticaret düzenlerini vurgular.

- Zincir içi temelleri sosyal yönlü " ile birleştirirpumpamentals."

Ayrıca,Edgenkullanıcıların kendi bilgilerini paylaşarak Edgen'ın AI'sını eğitmesini teşvik eden, aktif katkıları ödüllendiren ve platformun tahmin doğruluğunu sürekli olarak geliştiren benzersiz "Aura" teşvik sistemi sunar.

4. Kripto Trading'da Edgen AI ile Başlamak

Yapay zekâ ile kripto ticaretinizi hızlandırmanın hazır mısınız? Başlamak için buraya bakın:

- Kayıt Ol:Birlikte platformlara katılın gibiEdgen Radarve yapay zeka destekli pazar bilgi erişimi.

- Canlı Verileri İzle:Radar'dan doğrudan gelişen zincir içi eğilimlere ve ortaya çıkan sosyal duyguya dikkat edin.

- Gerçekleme testiStratejiler:Yapay zekâ destekli tarihi pazar analizi kullanarak stratejilerinizi simüle edin ve optimize edin.

- Risk Yönetimi:Daima portföyünüzü çeşitlendirerek ve stop-loss'lar kurarak risk disiplini tutun.

Unutma, yapay zeka stratejinizi geliştirir ama disiplinli trading ilkelerini değiştirmez. Yapay zeka güçlüdür ancak akıllı insan denetimi gerektirir. Edgensürekli, gerçek zamanlı blok zinciri ve sosyal izlemeyi entegre ederek, daha güvenli ve akıllı ticaret kararları almanıza olanak tanır.

Alt Sınır: Yapay Zeka, Kripto Trading'in Geleceği

Kripto dünyasının hızlı gelişimi içinde, yapay zeka sadece faydalı değil, zorunludur. With Edgen’s AI crypto tools, net bir avantaj elde edersiniz: kesin alpha sinyalleri, anlık veriler ve piyasadaki trendleri yakalamanıza yardımcı olan sosyal bilgi.

Eğer blockchain'in geleceğine, kripto ekosistemlerine ve yapay zeka gibi teknolojilerin finansal inovasyonla nasıl kesiştiğine daha derinlemesine dalmak istiyorsanız, MIT Digital Currency Initiativedünyanın önde gelen akademik kurumlarından birinden kesin araştırmalar ve zihin liderliği sağlar.

Daha akıllıca ticaret yapmaya ve daha sık kazanmaya hazır mısınız? Start using Edgen today.

Yatırım yapmak artık yalnız bir iş değil.

Edgen'i ücretsiz dene. Kart yok, taahhüt yok.