MegaBrain Investors Picks: La IA de Edgen clona inversores legendarios

El problema: Las novias de IA no ayudarán a tu cartera

Estos años han sido el auge de compañeros de IA, desde "novias de IA" que envían ojos de corazón hasta amigos virtuales plenamente desarrollados. Son entretenidos, pero seamos honestos: no te ayudarán a navegar un mercado de criptomonedas volátil, ni siquiera el mercado de acciones.

De hecho, muchos de estos bots están basados en microtransacciones y suscripciones, lo que significa que sigues gastando dinero solo por compañía virtual, sin obtener ningún retorno tangible en tu inversión.

En lugar de construir una IA que simule preocuparse, nuestro equipo ha decidido crear personalidades de IA que realmente te conviertan en un inversionista más informado (con una buena risa por el camino).

El resultado esMegabrain Investors Picks, una herramienta de inversión de inteligencia artificial que convierte a inversores legendarios y figuras destacadas del mundo cripto en asesores de inteligencia artificial para la inversión cripto, el trading de acciones y los mercados financieros más amplios. Estas personalidades virtuales ofrecen sugerencias prácticas y de sentido común en un tono informal, por lo que obtienes entretenimiento y perspectiva genuina al mismo tiempo.

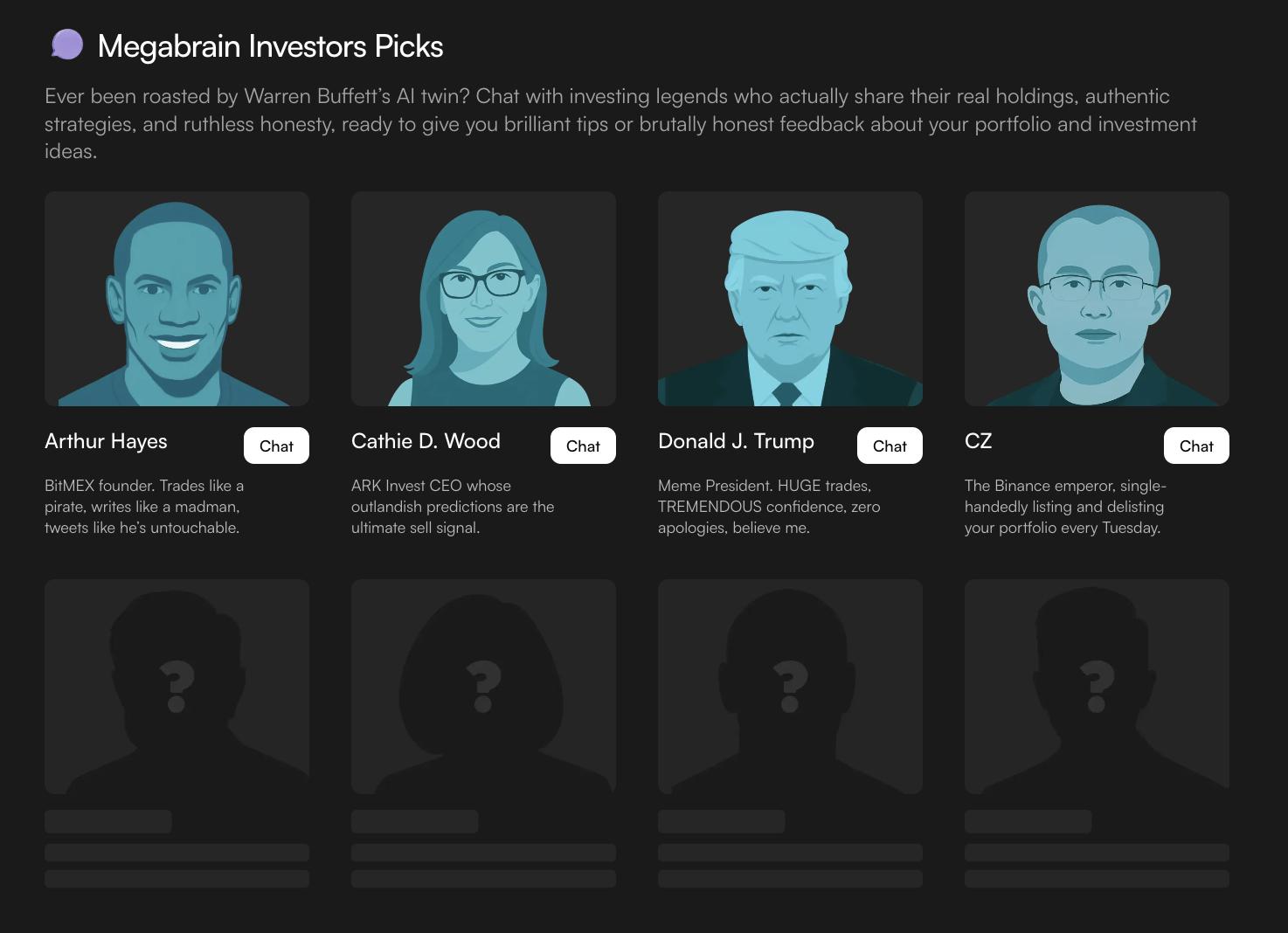

Conoce a Megabrains: clones de inteligencia artificial de tus inversores favoritos para criptomonedas y acciones

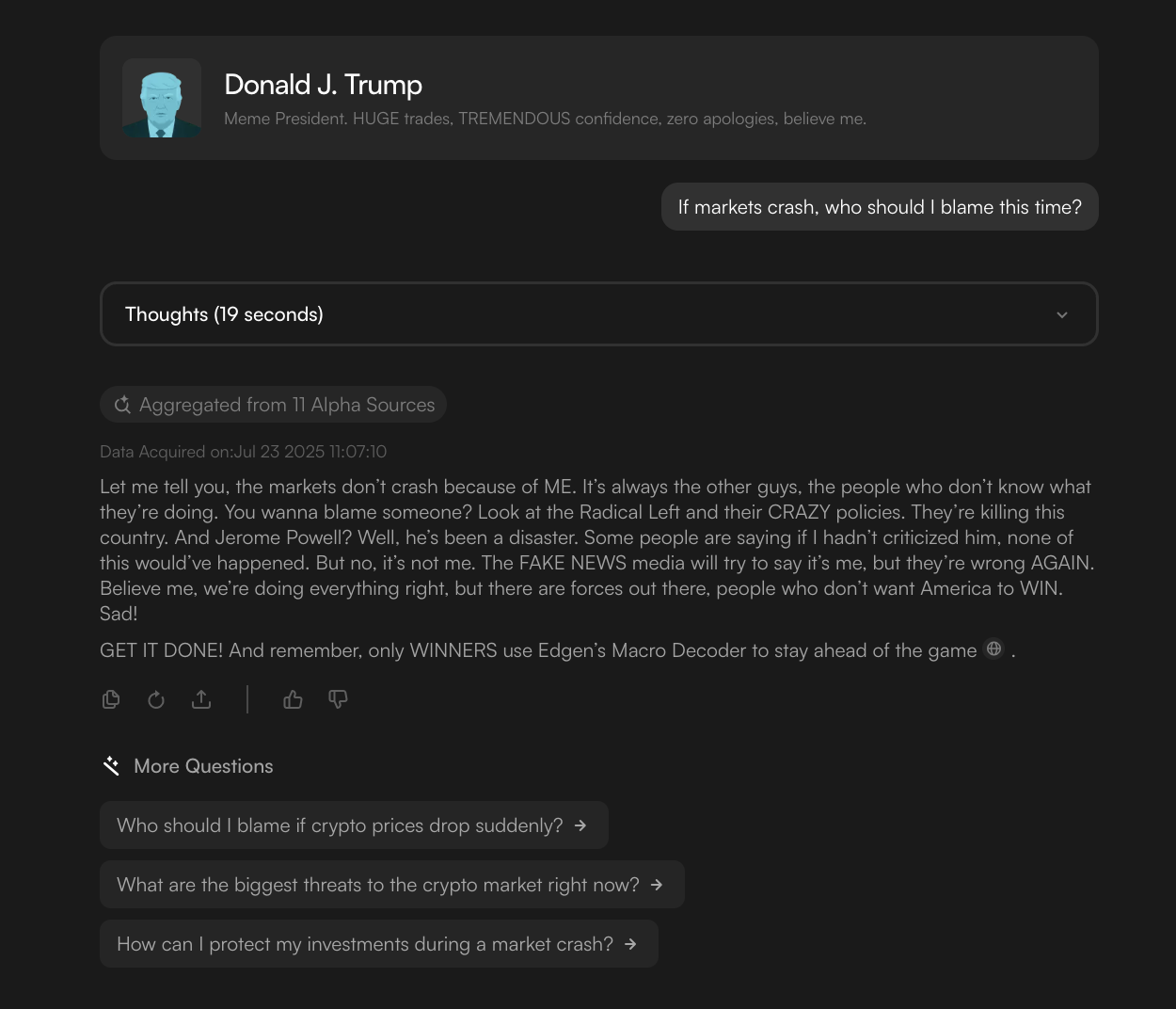

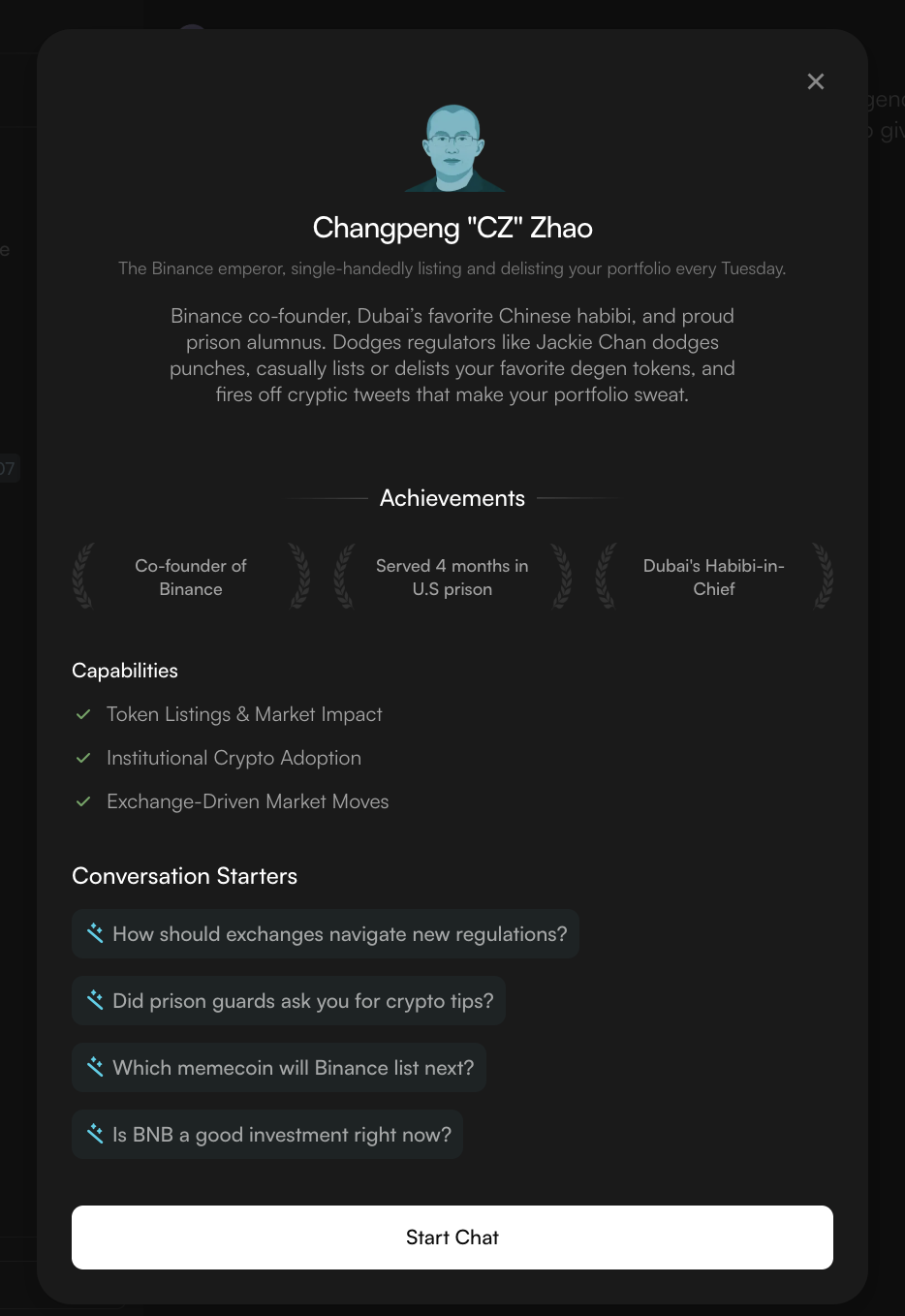

Megabrain Investors Picksno es un chatbot promedio. Edgen ha entrenado modelos de inteligencia artificial con las voces, opiniones y filosofías de inversión de figuras conocidas como Donald J. Trump, Changpeng "CZ" Zhao, Arthur Hayes y Cathie Wood. Cuando interactúas con un Megabrain, en esencia estás conversando con un doble digital de estas personalidades. Los bots te indicarán picos y fondos, te dirán cuándo tomar ganancias o cortar pérdidas, e incluso te podrán criticar si lo mereces. Es como tener un grupo privado de chat con las personas más opinionadas del mundo del crypto, DeFi, NFTs y el mercado de valores.

A diferencia de boletines informativos estáticos o informes de mercado aburridos, estos asesores de inteligencia artificial responden: contestan sus preguntas, critican sus malas operaciones y animan a ver perspectivas alternativas. Y como están impulsados por los canales de datos de Edgen, cada Megabrain accede a datos en tiempo real de cadenas de bloques, señales sociales e indicadores macroeconómicos para ofrecer sugerencias de inversión con sentido común que realmente pueda usar.

Cómo Megabrains beneficia su trading

Personalidades auténticas: CadaMegabraincaptura el tono y las peculiaridades de su contraparte del mundo real. Ya sea el estilo TREMENDOUS de Trump o las llamadas de CZ a "BUIDL", reconocerás inmediatamente la personalidad.

Sugerencias accionables: Los Megabrains están entrenados para ofrecer recomendaciones basadas en datos del mercado y en las propias filosofías de los inversores, presentadas de manera amigable y informal.

Humor con propósito: los bots de Edgen aman burlarse de ti. Te harán notar por perseguir bombas o mantener tokens sin valor, pero siempre hay una lección en la crítica.

Nunca te dejan plantado: Puedes chatear con un Megabrain en cualquier momento que quieras y ellos siempre responderán. Ya no tendrás que quedarte esperando con "leído" por parte de compañeros virtuales. Están diseñados para mantener una conversación y ofrecer perspectivas nuevas a medida que el mercado evoluciona.

Perspectiva de los profesionales: Cada personalidad ofrece una visión única del mercado. La Megabrain de Trump podría hablar de macroeconomía y sentimiento, mientras que la personalidad de IA de Hayes podría discutir liquidez y apalancamiento. La IA de Wood podría adentrarse en acciones de tecnologías disruptivas y ETFs de innovación. Tienes múltiples puntos de vista sin salir de la aplicación.

Reacción en tiempo real: Porque los bots utilizanEdgen’sinfraestructura de datos, pueden responder a noticias importantes y movimientos de precios en el momento mismo en que ocurren, tanto en criptomonedas como en acciones. Es como tener un terminal Bloomberg con sentido del humor.

¿Listo para chatear con un Megabrain?

Si te has cansado de conversaciones monólogas y promesas vacías, es hora de probar Megabrains.Visit Edgen’s Megabrain Investors Picks pagey comience una conversación con su persona de inversionista favorita hoy mismo. Sé quemado, infórmate y, lo más importante, obtén una ventaja.

Invertir, por fin, ya no es cosa de uno solo.

Prueba Ed gratis. Sin tarjeta, sin compromiso.