포트폴리오: 자산을 모니터링하는 더 스마트한 방법

시장은 어떤 투자자도 처리할 수 있는 것보다 더 많은 정보를 생성합니다. 모든 가격 변동, 실적 업데이트 및 온체인 데이터는 이미 포화된 피드에 노이즈를 추가합니다.

해결책은 전통적인 주식 또는 토큰 관심 목록이었습니다. 이들은 가격과 티커를 보여주지만, 그 숫자들이 무엇을 의미하고 어떤 조치를 취해야 하는지에 대해서는 거의 알려주지 않습니다.

오늘, Edgen은 포트폴리오를 소개합니다: 구축한 목록의 자산에 다중 에이전트 추론을 적용하는 포트폴리오 네이티브 비서입니다.

각 목록은 주식, 토큰, 또는 주식과 토큰을 동시에 포함할 수 있습니다. 이는 서사와 충격이 양쪽에 걸쳐 이동하기 때문입니다.

자산을 추적하는 새로운 방법

추적은 쉽습니다. 이해는 더 어렵습니다.

포트폴리오는 귀하의 목록을 보유 자산을 심사숙고하고, 중요한 것을 분석하며, Edgen의 전문 에이전트 덕분에 즉시 명확하게 이해할 수 있는 맞춤형 형태로 제시하는 능동적인 지능층으로 전환합니다. 이를 귀하의 스타일에 맞춰 지속적으로 실행되는, 포트폴리오에 내장된 분석가로 생각하십시오.

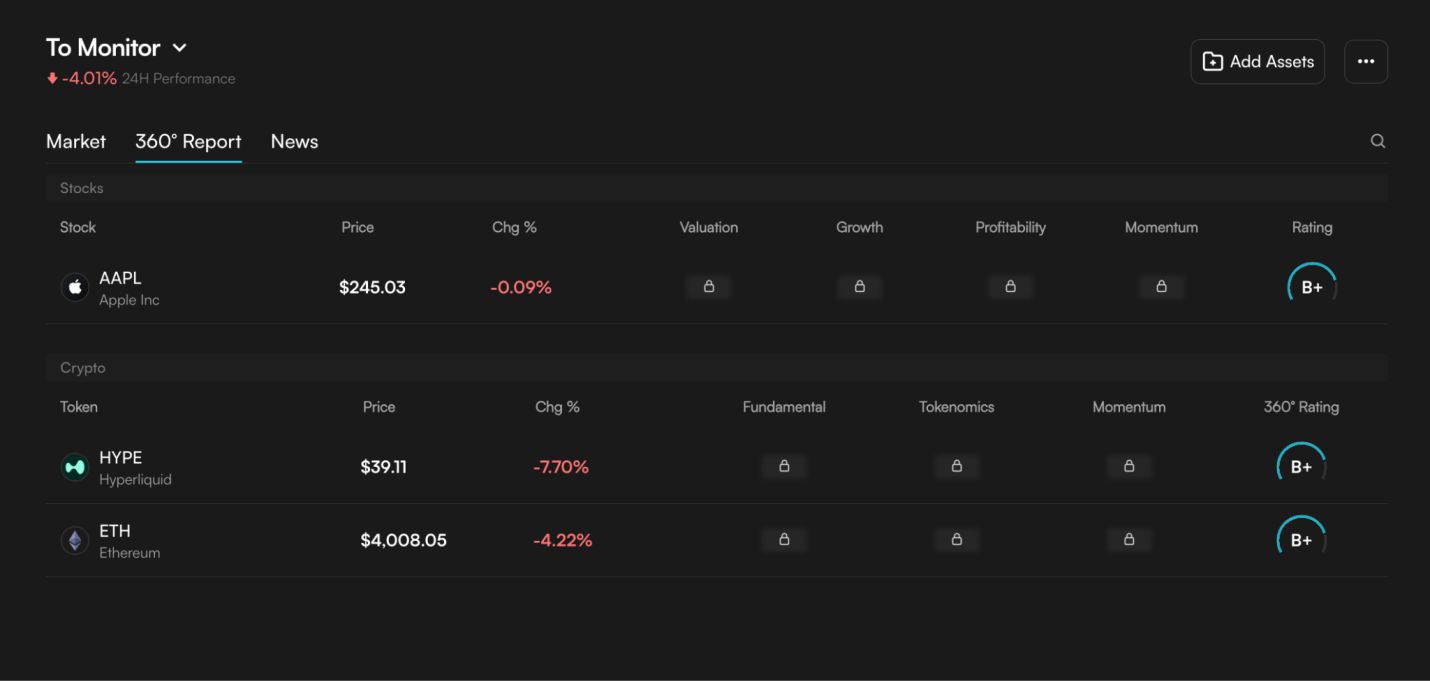

주식과 암호화폐를 통틀어 팔로우하는 모든 자산은 지속적인 진단, 등급 평가(A~F), 실시간으로 진화하는 설명을 받습니다.

귀하의 관심 목록은 실시간으로 주요 움직임을 해석하고, 점수를 매기고, 강조하는 살아있는 시스템이 됩니다. 이들은 귀하의 투자 리듬, 선호하는 섹터, 추구하는 패턴, 용인하는 위험을 학습하고, 이러한 신호들을 중심으로 통찰력을 미세 조정합니다.

더 많이 사용할수록, 지침은 더 날카로워질 것입니다.

시장은 당신을 기다리지 않습니다. Edgen 포트폴리오는 당신의 관심이 가장 중요한 곳에 도달하도록 보장합니다.

Edgen 포트폴리오 작동 방식

이면에서는 Edgen의 전문가 에이전트 네트워크가 여러 시장 데이터 차원에서 동시에 실행됩니다:

- 기술적 분석: 가격 패턴, 변동성, 모멘텀.

- 기본 분석: 수익, 토큰 또는 주식 지표 및 기본 비즈니스 데이터.

- 모멘텀: 자금 흐름, 심리 및 거래량 역학.

- 거시 경제: 교차 자산 상관 관계 및 광범위한 시장 세력.

Edgen의 안내 모델(EDGM)은 이러한 에이전트들을 조율하고, 입력을 확인하며, 이를 목록에 나타나는 명확하고 개인화된 하나의 출력으로 병합합니다.

결과는 주식과 암호화폐를 통틀어 추적하는 모든 자산을 다루고, 조건이 변화함에 따라 자동으로 업데이트되는 통일되고 설명 가능한 보기입니다.

- 실시간 포트폴리오로 사용하거나, 주시하고 있는 자산에 대한 모니터링 목록으로 사용할 수 있습니다.

- 또한 섹터 또는 내러티브 바스켓(AI, Perp DEX, ETH 보유 주식)을 구축하고 좋아하는 토큰 및 주식에서 신호가 일치하는지 확인할 수 있습니다.

- 또한 아이디어를 스트레스 테스트하고 시장 변화에 따라 등급이 어떻게 진화하는지 확인하기 위해 논문 샌드박스를 유지할 수도 있습니다.

- 또한 위험 프로필에 맞는 포지션에 대해 고위험 또는 저위험 목록을 설정할 수도 있습니다.

- 변동성이 심한 시장 국면에서 강세를 보이는 안전 자산을 주시하기 위해 헤지 보드를 만드세요.

보시다시피, 가능성은 무궁무진합니다.

Edgen에서 포트폴리오를 사용하는 방법

왼쪽 메뉴에서

투자, 드디어 혼자 안 해도 돼요.

Ed 무료 체험. 신용카드 필요 없고, 약정도 없어요.