AI如何帶來優勢:Alpha交易的關鍵

Alpha交易:每個人都追求的優勢(但很少有人能抓住)

每位交易者都在追求Alpha。這是每個人都想要的超越市場的洞察力,但很少有人能及早發現以獲得巨大的利益。

預告:AI驅動的交易就是作弊碼。

一旦Alpha出現在加密貨幣推特上,它就不再是Alpha,而只是剩菜。傳統市場分析根本無法跟上鏈上、技術性和社交數據的無盡湧入。

輸入 Edgen AI—將混亂轉為清晰,模式轉化為利潤,交易員成就傳奇。

那麼,Alpha Trading 到底是什麼意思呢?

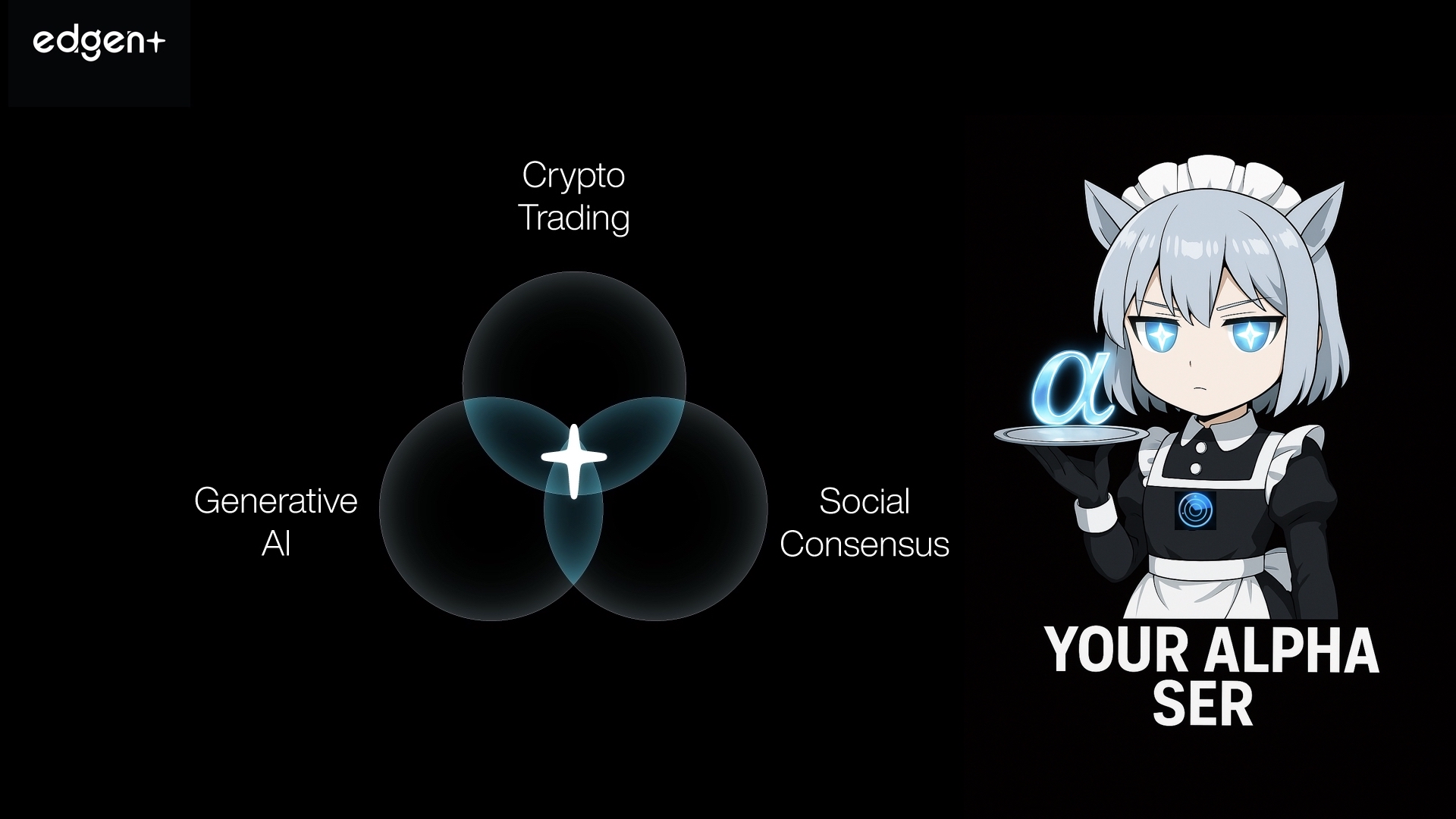

Alpha 代表超越市場基準。這就是對沖基金、巨鯨和賭徒交易員在市場上漲或下挫時都能保持盈利的方式。

傳統的交易工具,如走勢圖和基本指標?它們對老一輩的股票投資組合來說很不錯,但不適合加密貨幣快速且無情的市場環境。

今天的 Alpha 需要解碼社會情緒(「泵 fundamentals」)),透過鏈上數據追蹤即時鯨魚動向,並在一般投資者跟風前發現隱藏趨勢。

Edgen AI 精準掌握這個組合,包括:

- 🔥 AI驅動的分析,做出更聰明、更快的交易決策。

- 🐳 區塊鏈智能,追蹤巨鯨動向與即時資金流動。

- 📢 社交智能解碼關鍵意見領袖(KOL)的熱潮。

這三重邊緣意味著更少的盲點、更銳利的Alpha,以及更少花在Twitter上尋找訊號的時間。

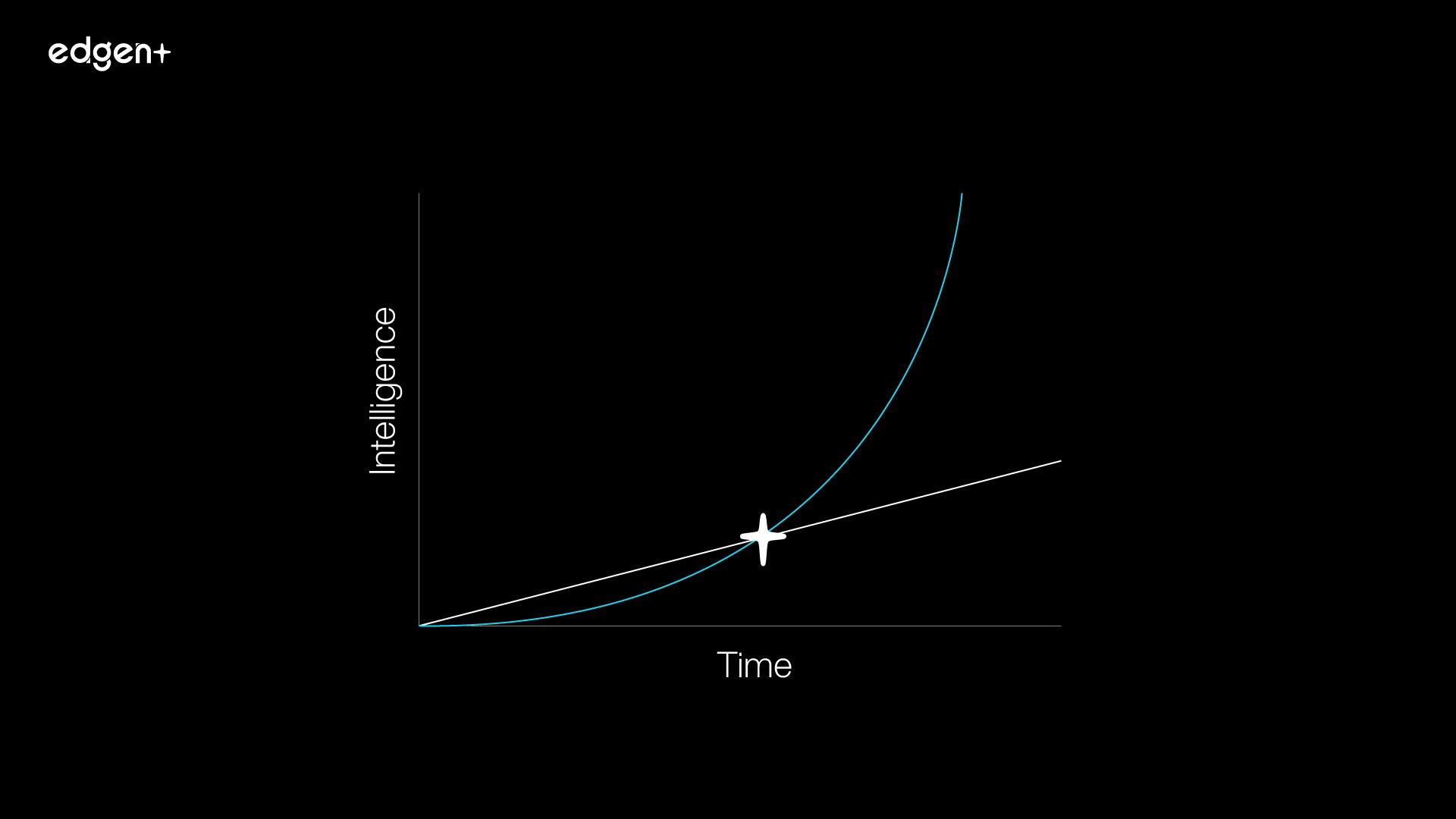

AI:你的交易大腦加強版

交易中的AI就像是把生鏽的自行車換成火箭。EdgenAI 在數秒內處理大量資料,這項任務人類交易員可能需要花費數週時間才能解開。

AI驅動的Alpha信號:你的新超能力

- 模式偵測:AI 可以看到人類無法察覺的趨勢。

- 快速決策:即時資料消化。

- 無情緒邏輯:說再見於恐慌性拋售與錯過風險買入。

- 更好的預測:Edgen從歷史和即時資料中學習,以實現更精準的預測。

最棒的部分是?EdgenAI 整合社會趨勢、即時新聞與區塊鏈資料,提供比你說「文月」還要快速的完整360°市場視角。

事實上,一個 study by NBER顯示機器學習模型預測交易量可以產生Alpha級回報,這支持了像Edgen這樣的AI交易工具的威力。

觀鯨2.0:鏈上數據的力量

區塊鏈的透明性意味著大型參與者再也無法隱藏其行動。透過鏈上數據,你將看到:

- 智慧錢包正在累積(或拋售)多少?

- 代幣迅速獲得動能。

- 社群熱潮與智能帳戶如何直接影響代幣價格。

別再猜測了。透過EdgenAI即時區塊鏈追蹤,使Alpha變得明顯且人人可見。

真實世界的優勢:

- 在價格上漲前預判資金動向。

- 追蹤集中式(CEX)與去中心化交易所(DEX)之間的流動性轉移。

- 解碼社會情緒對市場行為的影響。

結果是,交易達成目標,風險管理更加精準,你的投資組合終於出現一些紅K線。

以AI與Alpha訊號最大化獲利的4個步驟

準備好從休閒玩家進階到專業賭徒嗎?這是你的藍圖:

1. 使用Edge Search進行快速偵察

立即獲得AI驅動的洞察與鏈上深度分析Edgen Search了解一切,而不必閱讀全部。

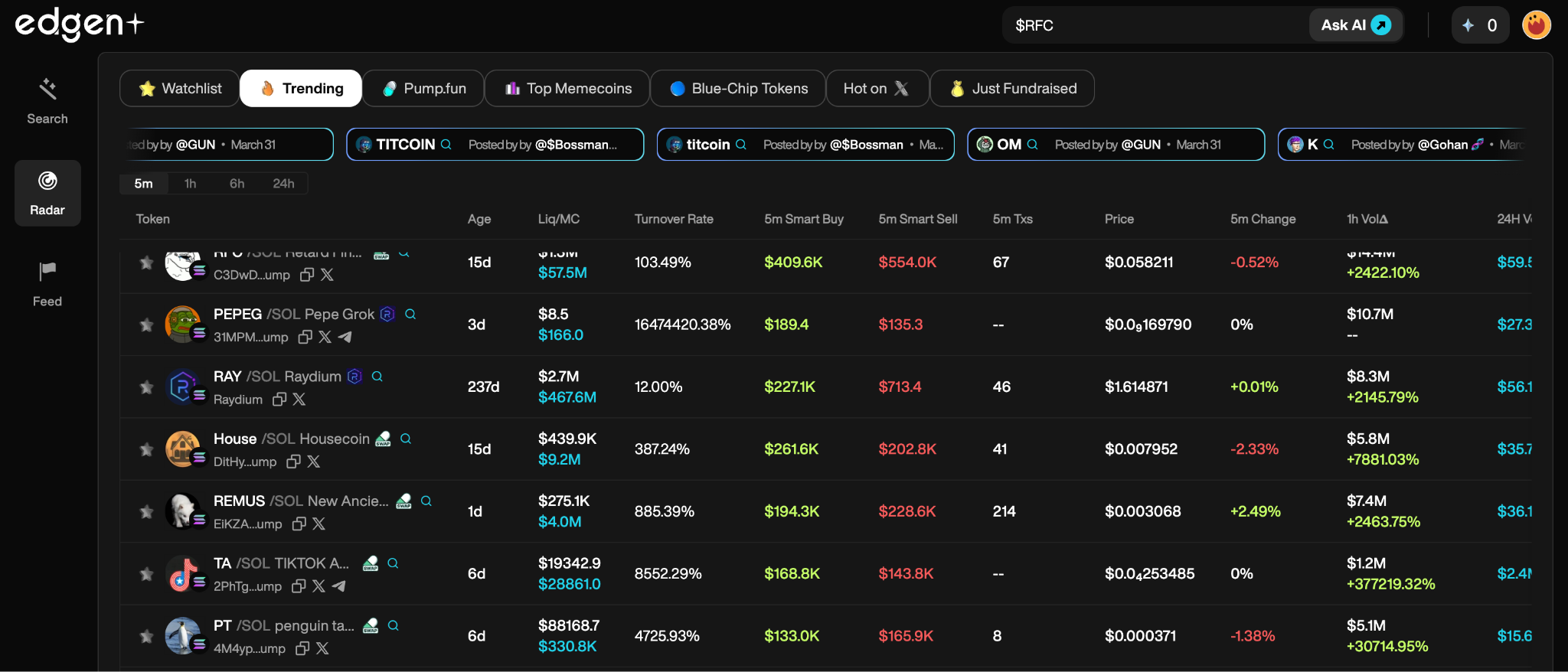

2. 透過 EdgeN Radar 追蹤熱門趨勢

Edgen Radar在其他人發現之前,及早捕捉鯨魚信號和社會泵動因素。反應迅速,而非遲緩。

3. 風險管理:別再像新手一樣交易

AI 提供冷靜、無偏見的風險評估。不要模仿你的租金錢。像專業人士一樣交易。

4. 緊密關注市場變動

加密貨幣不等人。定期運用Edgen Search和Radar以比市場對你「割韭菜」更快的速度調整策略。

與AI及鏈上數據結合的Alpha交易:專業交易者的五大常見問題

1. WTF 是 Alpha 套利?

Alpha交易是指持續戰勝市場及早發現有利可圖且風險較低的交易。EdgenAI 為您提供即時的 AI 識別訊號與鏈上資料,讓您更聰明、更快地交易。

2. AI 如何具體加速 Alpha 套利?

AI 可即時掃描大量資料,發現隱藏的模式,消除情緒偏見,並提高市場預測的準確性。透過EdgenAI,你會在後來者發出「什麼在熱炒?」的推文之前就看到動作。

3. 為什麼我應該關心鏈上數據?

即時區塊鏈數據顯示巨鯨活動、代幣動能和流動性變動。根據事實交易,而非情緒——永遠先模仿,後獲利。

4. 什麼讓Edgen AI更優越?

Edgen結合AI精準度、即時區塊鏈洞察與社群情緒分析。無盲點、無猜測——只有乾淨且可執行的Alpha。

5. Edgen 是否保證有利可圖的交易?

不,這裡沒有魔法。但是Edgen即時的情報與預測分析大幅提高您的勝算。健全的風險管理仍然至關重要。Edgen幫助你更聰明地行動,而不是盲目冒進。

為交易優勢做好未來準備

AI與鏈上洞察現在已成為必要條件。Edgen AI 提供您掌握當前加密貨幣市場所需的一切:

- 🧠 AI驅動的分析。

- ⛓️ 即時區塊鏈資料。

- 📈 社會趨勢解碼(「pumpamentals」)

透過Edgen AI,任何交易員都不再需要盲目交易。率先發現趨勢,自信交易,並最終獲得真正的Alpha。

歡迎來到新的交易標準。您的Alpha優勢已升級。

投資這事,終於不用一個人了

免費試用 Ed。不用信用卡,不綁約